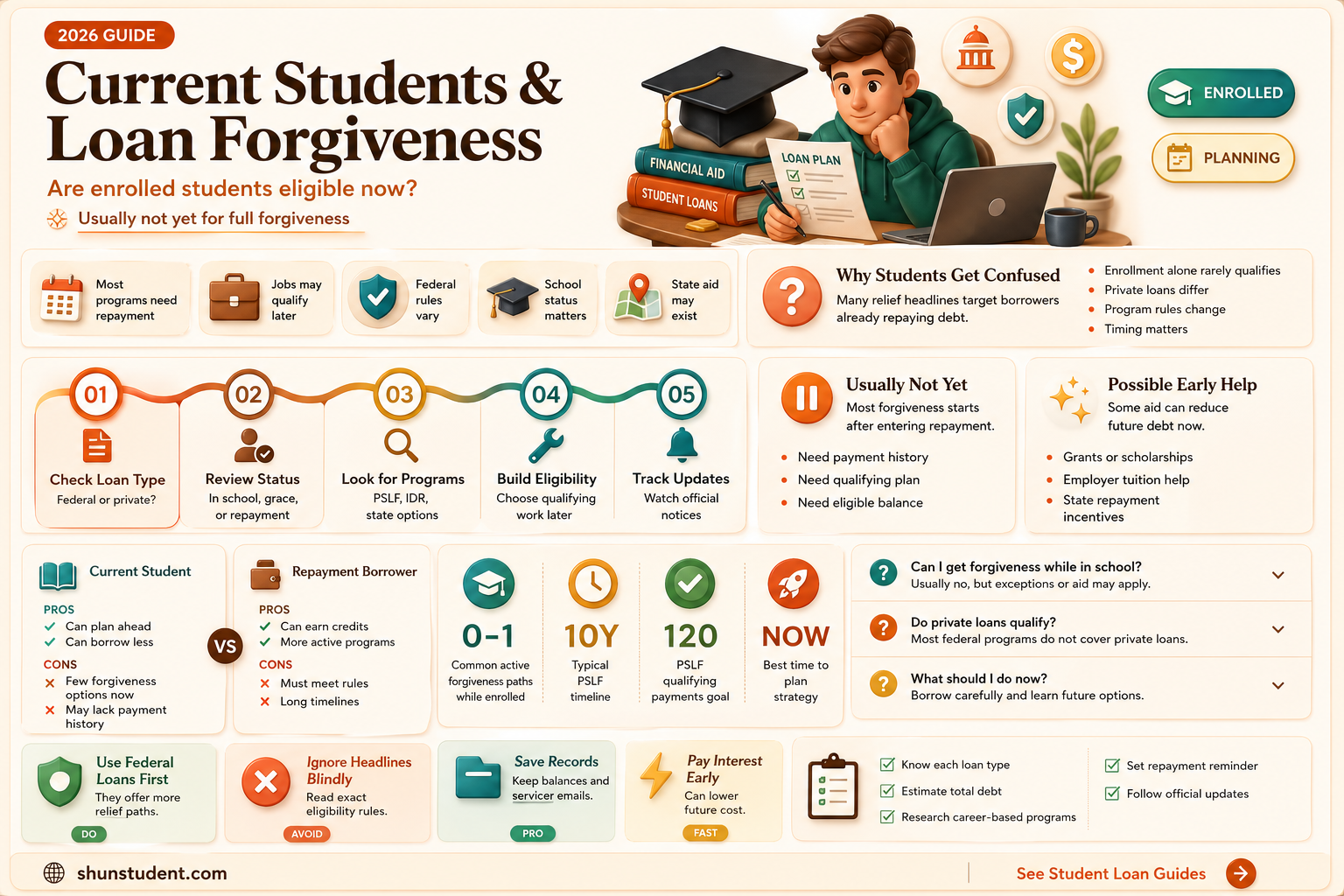

The topic of student loan forgiveness has been a subject of intense debate and discussion, particularly in light of the growing burden of student debt on current and former students. With the rising cost of education and the increasing number of students relying on loans to finance their studies, many are left wondering whether current students will be included in any potential loan forgiveness programs. As the government and educational institutions explore various options to alleviate this financial strain, it is essential to examine the eligibility criteria, potential benefits, and long-term implications of such initiatives for current students, who may be struggling to balance their academic pursuits with the looming prospect of substantial debt repayment.

| Characteristics | Values |

|---|---|

| Eligibility for Current Students | Generally, current students are not eligible for loan forgiveness programs like Public Service Loan Forgiveness (PSLF) or income-driven repayment (IDR) forgiveness until they graduate or leave school. |

| Exceptions | Some state-based or institutional programs may offer limited forgiveness for current students, but these are rare and specific. |

| Federal Loan Forgiveness Programs | Programs like PSLF, IDR forgiveness, and Teacher Loan Forgiveness require borrowers to be in repayment status, which excludes current students. |

| COVID-19 Relief Measures | Temporary relief measures (e.g., payment pauses) apply to current students with existing loans but do not include forgiveness. |

| Future Forgiveness Plans | Proposals like Biden's student loan forgiveness plan (as of 2023) typically exclude current students, focusing on past borrowers. |

| Private Loans | Private loan forgiveness is rare and does not typically include current students. |

| Institutional Policies | Some colleges offer forgiveness for institutional loans, but this varies widely and is not common for current students. |

| State-Based Programs | A few states offer limited forgiveness for specific fields (e.g., healthcare, education), but eligibility often requires graduation. |

| Repayment Status Requirement | Most forgiveness programs require borrowers to be in repayment, which current students are not. |

| Impact of Enrollment Status | Enrolled students are typically in deferment or forbearance, making them ineligible for forgiveness programs. |

Explore related products

What You'll Learn

- Eligibility Criteria: Current students' enrollment status and its impact on loan forgiveness eligibility

- Enrollment Date: Forgiveness rules based on enrollment before or after program start

- Loan Types: Which federal loans held by current students qualify for forgiveness

- Payment Status: How in-school deferment affects forgiveness for current students

- Future Programs: Potential inclusion of current students in upcoming forgiveness initiatives

![]()

Eligibility Criteria: Current students' enrollment status and its impact on loan forgiveness eligibility

Current students often wonder whether their enrollment status affects eligibility for loan forgiveness programs. The answer hinges on the specific program’s criteria, but a common thread exists: active enrollment typically disqualifies borrowers from immediate forgiveness. For instance, the Public Service Loan Forgiveness (PSLF) program requires borrowers to make 120 qualifying payments while employed full-time in public service, a process that cannot begin until after graduation or departure from school. Similarly, income-driven repayment (IDR) plans, which offer forgiveness after 20–25 years of payments, also exclude periods of in-school deferment from the qualifying payment count.

Analyzing these programs reveals a strategic takeaway: current students should focus on minimizing debt accumulation rather than relying on forgiveness. For example, federal loans offer in-school deferment, which pauses payments but allows interest to accrue on unsubsidized loans. Students can mitigate this by making interest payments during enrollment or choosing subsidized loans, which do not accrue interest while in school. Additionally, exploring scholarships, grants, or work-study programs can reduce reliance on loans altogether, positioning borrowers for faster forgiveness eligibility post-graduation.

A comparative look at state-based forgiveness programs highlights variations in eligibility. Some states, like California and New York, offer loan forgiveness for specific professions (e.g., teachers or healthcare workers) but require borrowers to be actively employed, not enrolled in school. Others, like Minnesota’s Loan Forgiveness for Public Service Employees, mandate a minimum service period post-graduation. Current students can prepare by researching state-specific programs and aligning their career goals with eligibility requirements, ensuring a smoother transition into forgiveness-eligible roles after completing their studies.

Persuasively, current students should view their enrollment period as a critical planning phase for future forgiveness. For instance, borrowers pursuing PSLF can use this time to secure qualifying employment immediately after graduation, ensuring no gap in their payment timeline. Similarly, those considering IDR plans can estimate their post-graduation income and select the most advantageous plan (e.g., Revised Pay As You Earn, or REPAYE) to maximize forgiveness potential. Practical steps include creating a repayment strategy, staying informed about policy changes, and maintaining meticulous records of employment and payments to streamline the forgiveness application process later.

In conclusion, while current students are generally not eligible for loan forgiveness during enrollment, this period offers a unique opportunity to strategize for future eligibility. By understanding program criteria, minimizing debt, and planning for post-graduation repayment, students can position themselves to benefit from forgiveness programs more effectively. Proactive steps taken now can significantly reduce the long-term burden of student loans.

Does PSLF Forgive Graduate Student Loans? A Comprehensive Guide

You may want to see also

Explore related products

![]()

Enrollment Date: Forgiveness rules based on enrollment before or after program start

The timing of your enrollment in a loan forgiveness program can significantly impact your eligibility and the amount forgiven. Programs often differentiate between students who enrolled before and after the program's official start date, creating a critical divide in benefits. For instance, the Public Service Loan Forgiveness (PSLF) program requires borrowers to make 120 qualifying payments while working full-time in public service. If you enrolled in a qualifying repayment plan before the PSLF program began in 2007, your payments may not count toward forgiveness unless you consolidate into a Direct Loan. This highlights the importance of understanding enrollment date rules to maximize your forgiveness potential.

Consider the Income-Driven Repayment (IDR) plans, which offer forgiveness after 20–25 years of qualifying payments. If you enrolled in an IDR plan before recent reforms, you might have faced challenges due to poor plan administration or misapplied payments. However, the 2023 IDR Account Adjustment allows the Department of Education to retroactively credit borrowers for time spent in certain repayment statuses, effectively bridging the gap for those who enrolled before recent improvements. This example underscores how enrollment timing can affect both eligibility and the administrative handling of your loans.

To navigate these rules effectively, follow these steps: First, verify the official start date of the forgiveness program you’re targeting. Second, check your enrollment date in your repayment plan or loan type against this benchmark. Third, if you enrolled before the program began, explore consolidation or other corrective actions to align your loans with current requirements. For example, consolidating FFEL or Perkins Loans into a Direct Loan can make pre-2007 payments eligible for PSLF. Finally, document all communications and payments to ensure accurate tracking, as administrative errors are common in these programs.

A cautionary note: Enrollment date rules are often rigid, with little room for exceptions. Missing the cutoff by even a day can disqualify years of payments from counting toward forgiveness. For instance, the one-time IDR Adjustment ends in April 2024, meaning borrowers who fail to act before this deadline will lose the chance to correct past payment discrepancies. Similarly, the PSLF waiver, which expired in October 2022, offered a temporary reprieve for pre-2007 payments but is no longer available. These deadlines emphasize the need for proactive management of your enrollment timing.

In conclusion, enrollment date rules are a critical but often overlooked aspect of loan forgiveness programs. By understanding how your enrollment timing aligns with program start dates, you can take strategic steps to ensure your payments count toward forgiveness. Whether consolidating loans, applying for retroactive credits, or meeting strict deadlines, staying informed and acting promptly can make the difference between full forgiveness and years of additional payments. Treat enrollment dates as a cornerstone of your forgiveness strategy, and you’ll be better positioned to navigate the complexities of these programs.

Student Loan Forgiveness: What Borrowers Need to Know Now

You may want to see also

Explore related products

![]()

Loan Types: Which federal loans held by current students qualify for forgiveness

Current students holding federal loans may wonder if they qualify for forgiveness programs. The answer hinges on the type of loan and the specific forgiveness program. Not all federal loans are created equal, and understanding these distinctions is crucial for navigating the complex landscape of loan forgiveness.

Direct Loans: The Primary Candidates

The most common federal loans held by current students are Direct Subsidized and Unsubsidized Loans. These loans are eligible for several forgiveness programs, including Public Service Loan Forgiveness (PSLF) and income-driven repayment (IDR) forgiveness. PSLF requires 120 qualifying payments while working full-time for a qualifying employer, such as a government or non-profit organization. IDR forgiveness, on the other hand, is available after 20-25 years of payments, depending on the plan. For instance, the Revised Pay As You Earn (REPAYE) plan offers forgiveness after 20 years for undergraduate loans and 25 years for graduate loans.

Perkins Loans: A Limited Opportunity

Federal Perkins Loans, although less common today, still exist in some portfolios. These loans may qualify for cancellation under specific circumstances, such as teaching in a low-income school or serving in the military. For example, teachers can receive up to 100% cancellation over 5 years, with 15% cancelled after the first and second years, 20% after the third and fourth years, and 30% after the fifth year. However, Perkins Loans are not eligible for PSLF or IDR forgiveness unless consolidated into a Direct Consolidation Loan.

FFEL and Consolidation Loans: A Nuanced Approach

Federal Family Education Loan (FFEL) Program loans, which include Stafford, PLUS, and Consolidation Loans, are not automatically eligible for PSLF or IDR forgiveness. However, borrowers can consolidate these loans into a Direct Consolidation Loan to access these programs. This strategy requires careful planning, as consolidation may reset the payment clock for IDR forgiveness. For instance, if a borrower has made 5 years of payments under an FFEL loan, consolidating it into a Direct Loan will restart the 20- or 25-year forgiveness timeline.

Practical Tips for Maximizing Forgiveness Potential

To optimize their chances of loan forgiveness, current students should:

- Verify loan types: Confirm the specific federal loans held through the National Student Loan Data System (NSLDS).

- Explore consolidation options: Consider consolidating FFEL loans into a Direct Consolidation Loan to access PSLF and IDR forgiveness.

- Choose the right repayment plan: Select an IDR plan that aligns with financial goals and forgiveness timelines.

- Monitor employment eligibility: Ensure employers qualify for PSLF, if applicable, and submit the Employer Certification Form annually.

By understanding the nuances of federal loan types and forgiveness programs, current students can make informed decisions to minimize their loan burden and maximize their financial well-being.

Unemployed and Struggling: Can You Get Student Loan Forgiveness?

You may want to see also

Explore related products

![]()

Payment Status: How in-school deferment affects forgiveness for current students

Current students often wonder whether their in-school deferment status impacts their eligibility for loan forgiveness. The short answer is yes—but the relationship between deferment and forgiveness is nuanced. In-school deferment pauses required payments on federal student loans while enrolled at least half-time, but this pause doesn’t automatically count toward forgiveness programs like Public Service Loan Forgiveness (PSLF) or income-driven repayment (IDR) plans. For forgiveness, payments—not deferment periods—are what matter. However, strategically using deferment can help borrowers avoid delinquency and maintain eligibility for forgiveness programs later.

Consider this scenario: A borrower enrolled in an IDR plan returns to school and enters deferment. During this time, their loan balance doesn’t accrue interest (if subsidized), but the clock on their 20- or 25-year forgiveness timeline effectively stops. For PSLF, deferment periods don’t count as qualifying months unless the borrower is employed full-time in public service while in school. The takeaway? Deferment protects borrowers from default but doesn’t actively advance forgiveness progress.

To maximize forgiveness potential, current students should understand the interplay between deferment and their repayment plan. For instance, if pursuing PSLF, working part-time in a qualifying public service role while in school can allow borrowers to make small, income-driven payments that count toward forgiveness. Similarly, those on IDR plans can recertify their income annually to ensure payments remain low, even if deferment is an option. Proactive management of payment status during school can set the stage for smoother forgiveness later.

A cautionary note: Misunderstanding deferment’s role can lead to costly mistakes. For example, assuming deferment counts toward forgiveness could delay a borrower’s timeline by years. Additionally, unsubsidized loans accrue interest during deferment, potentially increasing the balance forgiven under IDR plans. Borrowers should weigh the benefits of deferment against the long-term impact on their forgiveness strategy. Consulting a loan servicer or financial advisor can provide clarity tailored to individual circumstances.

In summary, in-school deferment is a tool, not a shortcut, for loan forgiveness. It preserves financial stability during education but requires careful planning to align with forgiveness goals. By understanding how deferment interacts with repayment plans and forgiveness programs, current students can navigate their loans more effectively. The key is to stay informed, proactive, and strategic—ensuring that time in school doesn’t become a setback for future forgiveness.

Will Student Loan Forgiveness Dates Shift Again? What Borrowers Need to Know

You may want to see also

Explore related products

![]()

Future Programs: Potential inclusion of current students in upcoming forgiveness initiatives

Current student loan forgiveness programs primarily target borrowers who have already completed their education, leaving many current students wondering if they will ever benefit from such initiatives. However, as the burden of student debt continues to grow, policymakers are increasingly considering the inclusion of current students in future forgiveness programs. This shift could address the root causes of debt accumulation and provide relief to a broader population of borrowers.

One potential model for including current students involves income-driven repayment (IDR) plans with built-in forgiveness components. For instance, a program could cap monthly payments at a certain percentage of discretionary income (e.g., 10%) and automatically forgive remaining balances after a set period, such as 20 years for undergraduate loans. Current students opting into such plans would benefit from predictable, manageable payments and the assurance of eventual forgiveness, reducing long-term financial stress.

Another approach could tie forgiveness to public service or high-need career paths. For example, a program might offer $5,000 in annual loan forgiveness for current students committing to work in underserved areas or critical sectors like education, healthcare, or renewable energy. This not only alleviates debt but also incentivizes students to pursue careers with societal impact. Clear eligibility criteria and application processes would be essential to ensure transparency and accessibility.

However, including current students in forgiveness initiatives raises challenges. Critics argue that such programs could inflate tuition costs if institutions assume students will rely on future forgiveness. To mitigate this, policymakers could pair forgiveness with tuition regulation measures, such as caps on annual increases or increased funding for public institutions. Additionally, means-testing could ensure that forgiveness benefits those most in need, rather than subsidizing students from higher-income backgrounds.

In conclusion, the potential inclusion of current students in future loan forgiveness programs represents a proactive approach to addressing the student debt crisis. By designing initiatives that combine repayment flexibility, career incentives, and safeguards against unintended consequences, policymakers can create a system that supports both current and future borrowers. As discussions evolve, stakeholders must prioritize equity, sustainability, and long-term economic benefits to ensure these programs achieve their intended goals.

Nonprofit Student Loan Forgiveness: A Step-by-Step Application Guide

You may want to see also

Frequently asked questions

Yes, current students with federal student loans may be eligible for loan forgiveness under certain programs, such as Public Service Loan Forgiveness (PSLF) or income-driven repayment (IDR) plans, provided they meet specific criteria.

Yes, current students with federal student loans held by the Department of Education may qualify for one-time forgiveness initiatives, such as those announced in 2022, depending on their income and loan type.

It depends on the program. For some initiatives, like PSLF, current students must make qualifying payments while employed in eligible public service jobs. However, payment pauses or waivers may apply during certain periods, such as the COVID-19 pandemic.