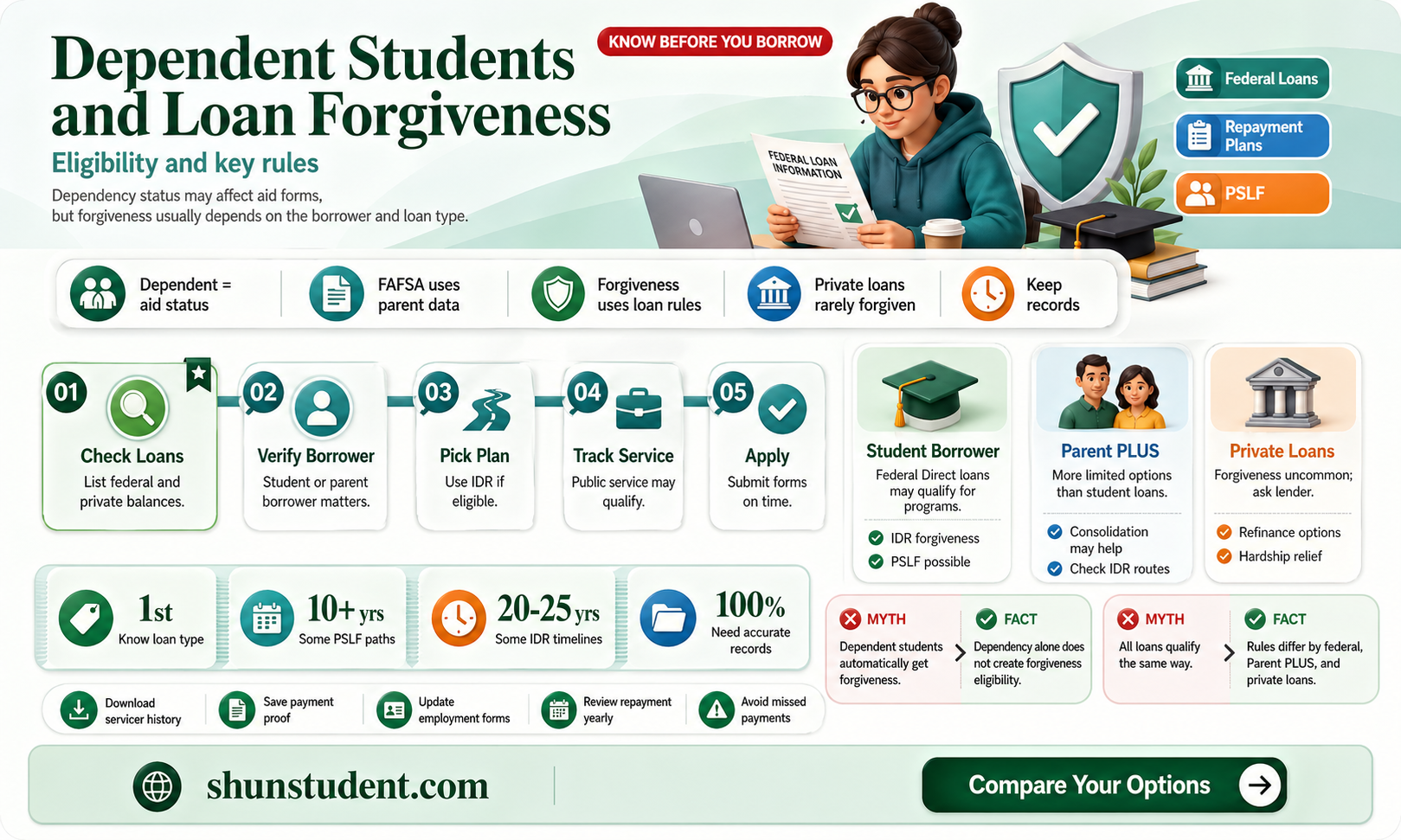

Dependent students, typically those who rely on their parents' financial information to determine eligibility for federal student aid, may wonder if they qualify for loan forgiveness programs. While dependency status primarily affects the initial application for financial aid, it does not directly impact eligibility for loan forgiveness. Most forgiveness programs, such as Public Service Loan Forgiveness (PSLF) or income-driven repayment (IDR) forgiveness, focus on factors like employment, repayment plan, and loan type rather than dependency status. However, dependent students may face challenges if their parents' income limits their access to certain repayment plans or if their parents have taken out Parent PLUS loans, which have separate forgiveness criteria. Understanding these distinctions is crucial for dependent students seeking relief from student loan debt.

| Characteristics | Values |

|---|---|

| Eligibility for Loan Forgiveness | Dependent students may be eligible for loan forgiveness under certain programs, but eligibility depends on the specific program and their dependency status. |

| Dependency Status Impact | Dependency status (as determined by the FAFSA) does not directly disqualify students from loan forgiveness but may affect eligibility for certain programs. |

| Income-Driven Repayment (IDR) Forgiveness | Dependent students can qualify for IDR forgiveness after 20-25 years of payments, depending on the plan. Parental income is not considered for IDR eligibility. |

| Public Service Loan Forgiveness (PSLF) | Dependent students are eligible for PSLF if they work full-time for a qualifying employer and make 120 qualifying payments. Dependency status does not affect eligibility. |

| Teacher Loan Forgiveness | Dependent students may qualify if they teach full-time for five consecutive years in a low-income school. Dependency status does not impact eligibility. |

| Disability Discharge | Dependent students with a permanent disability can apply for loan discharge. Dependency status does not affect eligibility. |

| Borrower Defense to Repayment | Dependent students may qualify if their school misled them or violated certain laws. Dependency status does not impact eligibility. |

| FAFSA Dependency Rules | Dependency status is determined by FAFSA guidelines, not loan forgiveness programs. Independent students may have different financial aid options but are not inherently more eligible for forgiveness. |

| Parental Involvement | Parental income and information are required for dependent students on the FAFSA but do not affect loan forgiveness eligibility directly. |

| Program-Specific Requirements | Eligibility for loan forgiveness programs depends on the program's criteria, not dependency status. Dependent students must meet the same requirements as independent students. |

Explore related products

What You'll Learn

![]()

Income-Driven Repayment Plans for Dependent Students

Dependent students navigating the complexities of student loan repayment often find solace in income-driven repayment (IDR) plans, which adjust monthly payments based on earnings and family size. These plans are particularly beneficial for those with lower incomes or high debt-to-income ratios, offering a lifeline to avoid default. For dependent students, whose financial information includes parental data on the Free Application for Federal Student Aid (FAFSA), IDR plans consider both the student’s and parent’s income, potentially lowering payments if the combined household income is modest. This approach ensures repayment remains manageable, even for those still establishing financial independence.

One critical aspect of IDR plans is their eligibility criteria. Dependent students must have federal Direct Loans, as these are the only loans qualifying for such plans. Perkins Loans or private loans are ineligible, underscoring the importance of understanding loan types. Additionally, IDR plans require annual recertification of income and family size, a step dependent students cannot overlook. Failure to recertify can result in a return to the standard repayment plan, often with significantly higher monthly payments. Staying proactive in this process is key to maintaining affordability.

A lesser-known advantage of IDR plans is their pathway to loan forgiveness. After 20–25 years of qualifying payments, any remaining balance is forgiven, though this may be taxed as income. For dependent students, this timeline aligns with the early stages of their careers, providing long-term financial relief. However, the forgiven amount could result in a substantial tax bill, so planning ahead—such as setting aside funds annually—is advisable. This feature makes IDR plans not just a temporary solution but a strategic tool for debt management.

Practical tips for dependent students include consolidating multiple federal loans into a Direct Consolidation Loan if necessary, as this simplifies enrollment in IDR plans. Additionally, tracking payments meticulously is crucial, as administrative errors can occur. Utilizing tools like the National Student Loan Data System (NSLDS) to monitor progress ensures accuracy. Finally, dependent students should communicate openly with parents about their repayment strategy, as parental support—whether financial or advisory—can significantly ease the burden. With careful planning, IDR plans offer a realistic path to financial stability.

Peace Corps Service: A Path to Student Loan Forgiveness?

You may want to see also

Explore related products

![]()

Public Service Loan Forgiveness Eligibility Criteria

Dependent students seeking loan forgiveness often wonder if their status affects eligibility, especially under programs like Public Service Loan Forgiveness (PSLF). The good news is that dependency status itself does not disqualify borrowers from PSLF. Instead, eligibility hinges on specific criteria tied to employment, loan type, and repayment plan. For instance, borrowers must work full-time for a qualifying public service employer, such as a government organization or 501(c)(3) nonprofit, and make 120 qualifying payments while enrolled in an income-driven repayment plan. Dependency status, which primarily impacts financial aid eligibility, is irrelevant here. The focus is on the borrower’s employment and repayment history, not their familial or financial dependency.

To qualify for PSLF, borrowers must have Federal Direct Loans, as other loan types like Federal Family Education Loans (FFEL) or Perkins Loans are ineligible unless consolidated into a Direct Loan. This is a critical step for many, as consolidation can make previously ineligible loans qualify for forgiveness. For dependent students who took out loans with their parents, such as Parent PLUS Loans, only the student’s own Direct Loans are eligible for PSLF. Parents’ loans cannot be forgiven under this program, even if the student is still dependent. This distinction underscores the importance of understanding which loans are held by the borrower and how they can be managed to meet PSLF requirements.

Qualifying payments for PSLF must be made under an income-driven repayment plan, such as Income-Based Repayment (IBR), Pay As You Earn (PAYE), or Revised Pay As You Earn (REPAYE). These plans cap monthly payments at a percentage of the borrower’s discretionary income, typically 10-20%, making them more manageable for those in lower-paying public service roles. Dependent students transitioning into the workforce can benefit from these plans, as they align with potentially lower starting salaries. However, it’s crucial to recertify income and family size annually to ensure payments remain qualifying. Failure to do so can disrupt progress toward forgiveness.

A common misconception is that part-time work or volunteer service counts toward PSLF. In reality, borrowers must work at least 30 hours per week for a qualifying employer, or meet their employer’s definition of full-time if it’s less than 30 hours. For dependent students who may be balancing work and family obligations, this requirement can be challenging but is non-negotiable. Additionally, periods of unemployment, leaves of absence, or underemployment do not count toward the 120 qualifying payments. Borrowers must maintain consistent, full-time employment in public service to stay on track.

Finally, tracking progress and submitting the PSLF Employment Certification Form regularly is essential. This form verifies employment with a qualifying employer and ensures payments are counted toward forgiveness. Dependent students who transition from school to work should submit this form annually or when changing employers to avoid discrepancies. The PSLF Help Tool, available through the U.S. Department of Education, can assist borrowers in determining employer eligibility and managing their repayment journey. By staying organized and informed, dependent students can navigate PSLF eligibility effectively, regardless of their dependency status.

Bernie's Plan to Erase Student Debt: A Path to Forgiveness

You may want to see also

Explore related products

![]()

Parent PLUS Loans and Forgiveness Options

Parent PLUS Loans, designed for parents borrowing on behalf of their dependent undergraduate students, carry unique challenges and opportunities when it comes to forgiveness. Unlike federal student loans held by students themselves, Parent PLUS Loans are not eligible for income-driven repayment (IDR) plans unless consolidated into a Direct Consolidation Loan and then enrolled in the Income-Contingent Repayment (ICR) plan. This consolidation step is critical, as it unlocks the possibility of loan forgiveness after 25 years of qualifying payments under ICR. However, parents must carefully weigh the trade-offs, as consolidation may reset the payment clock and affect interest accrual.

For parents seeking forgiveness through Public Service Loan Forgiveness (PSLF), the path is similarly narrow but viable. Parent PLUS Loans can qualify for PSLF if consolidated into a Direct Consolidation Loan and if the borrower works full-time for a qualifying employer, such as a government or nonprofit organization. The catch? Payments must be made under an IDR plan, specifically ICR, for 10 consecutive years. This option demands meticulous planning, as PSLF requires strict adherence to eligibility criteria, including timely certification of employment and consistent qualifying payments.

Another lesser-known forgiveness avenue for Parent PLUS Loans is through the Total and Permanent Disability (TPD) discharge program. If the parent borrower or the dependent student becomes permanently disabled, the loans may be forgiven entirely. Documentation from a physician or the Social Security Administration is required, and the process involves a three-year monitoring period during which the borrower’s income and disability status are reviewed. While this option is situational, it provides a critical safety net for families facing severe hardship.

Practical tips for parents navigating Parent PLUS Loan forgiveness include staying informed about policy changes, as federal loan programs frequently evolve. For instance, limited-time waivers, like those introduced during the COVID-19 pandemic, can retroactively count previously ineligible payments toward forgiveness programs. Additionally, parents should consult a financial advisor or loan specialist to tailor a strategy that aligns with their long-term financial goals. Finally, maintaining detailed records of payments, employment, and consolidation steps is essential to streamline the forgiveness application process.

In conclusion, while Parent PLUS Loans present limited forgiveness options, strategic actions like consolidation, enrollment in ICR, and pursuit of PSLF or TPD discharge can provide pathways to relief. Parents must proactively navigate these options, balancing immediate financial pressures with long-term repayment strategies. With careful planning and awareness of program nuances, forgiveness for Parent PLUS Loans, though challenging, is not out of reach.

Can Student Loan Forgiveness Face Legal Challenges in Court?

You may want to see also

Explore related products

![]()

Dependent Student Loan Discharge Programs

Dependent students, typically those whose financial aid applications require parental information, often face unique challenges when navigating loan forgiveness options. While many forgiveness programs focus on borrower-specific criteria like income or profession, dependent students must also consider their familial financial ties. This complexity underscores the importance of understanding Dependent Student Loan Discharge Programs, which offer targeted relief under specific circumstances.

One critical program to explore is the Total and Permanent Disability (TPD) Discharge. If a dependent student becomes permanently disabled, they may qualify for loan discharge, regardless of their dependency status. The process requires documentation from a physician certifying the disability, and the borrower must meet income requirements to avoid tax liability on the discharged amount. For dependent students, this program provides a lifeline, though it’s essential to note that parental income does not factor into eligibility—only the borrower’s financial situation matters.

Another avenue is the Closed School Discharge, applicable if a student’s school closes while they are enrolled or shortly after withdrawal. Dependent students are eligible for this discharge just as independent students are, provided they meet the enrollment or withdrawal timeline criteria. For instance, if a student withdraws 120 days before the school closes, they qualify for full discharge. This program highlights how dependency status does not inherently limit access to certain forgiveness options.

A less-known but valuable program is the Borrower Defense to Repayment, which allows discharge if a school misled the student or violated state laws. Dependent students can pursue this option if their school engaged in fraudulent practices, such as falsifying job placement rates. The process requires submitting evidence of the school’s misconduct, and approval can lead to full discharge and potential reimbursement of payments made. This program underscores the importance of researching schools thoroughly, even for dependent students whose parents may play a role in decision-making.

While these programs offer relief, dependent students must navigate additional considerations. For example, if a parent co-signed a private loan, discharge programs typically do not apply, as private loans are not governed by federal regulations. Additionally, dependent students should monitor changes to federal policies, as new legislation could expand or modify eligibility criteria. Practical tips include keeping detailed records of school communications, staying informed about loan servicer updates, and consulting with a financial aid advisor to explore all available options. By understanding these programs, dependent students can take proactive steps toward managing their loan burden effectively.

Unlock Student Loan Forgiveness: Your Guide to $10,000 Relief

You may want to see also

Explore related products

![]()

Impact of Dependency Status on Forgiveness Eligibility

Dependency status significantly influences a student's eligibility for loan forgiveness programs, often determining whether they qualify for certain benefits or face additional hurdles. For instance, dependent students typically have their parents' income factored into their financial aid calculations, which can affect their eligibility for income-driven repayment plans—a common pathway to loan forgiveness. This means that even if a dependent student’s personal income is low, their parents’ financial situation could disqualify them from programs like Public Service Loan Forgiveness (PSLF) or income-driven forgiveness if the calculated payment is too high. Understanding this dynamic is crucial for borrowers navigating repayment options.

Consider the case of income-driven repayment plans, which cap monthly payments at a percentage of the borrower’s discretionary income. Dependent students may find themselves in a bind if their parents’ income inflates their expected family contribution (EFC), leading to higher calculated payments. For example, a dependent student whose parents earn $100,000 annually might be deemed ineligible for reduced payments under plans like Revised Pay As You Earn (REPAYE), even if they personally earn only $30,000 post-graduation. This highlights how dependency status can indirectly limit access to forgiveness programs tied to these plans.

To mitigate these challenges, dependent students should explore strategies to adjust their financial aid status. One practical tip is to appeal for a dependency override through the financial aid office, which can reclassify a student as independent if they can demonstrate extenuating circumstances, such as estrangement from parents or unusual financial hardship. Another approach is to pursue career paths that qualify for targeted forgiveness programs, like teaching in low-income schools or working in public service, which may offer forgiveness regardless of dependency status.

Comparatively, independent students often face fewer barriers to loan forgiveness due to their sole reliance on personal income for repayment calculations. This underscores the importance of understanding the long-term implications of dependency status early in the borrowing process. For dependent students, proactive planning—such as choosing federal loans over private ones, which rarely offer forgiveness options—can help maximize eligibility for future relief programs.

In conclusion, dependency status acts as a critical determinant in loan forgiveness eligibility, shaping access to income-driven plans and other relief programs. By recognizing its impact and taking strategic steps, dependent students can navigate these constraints more effectively. Whether through dependency overrides, career choices, or careful loan selection, informed decisions today can pave the way for financial relief tomorrow.

Student Loan Forgiveness: A Path to Equality or Deeper Divide?

You may want to see also

Frequently asked questions

Yes, dependent students may be eligible for loan forgiveness through programs like Public Service Loan Forgiveness (PSLF) or income-driven repayment (IDR) plans, provided they meet the program requirements.

Yes, dependent students’ eligibility for loan forgiveness is based on their own repayment plan and employment, not their parents’ income, once they begin repayment.

No, dependent students do not need to become independent to qualify for loan forgiveness. Eligibility is determined by the repayment plan and employment criteria, not dependency status.

Yes, dependent students have access to the same federal loan forgiveness programs as independent students, such as PSLF, IDR forgiveness, and temporary relief programs like those offered during the COVID-19 pandemic.