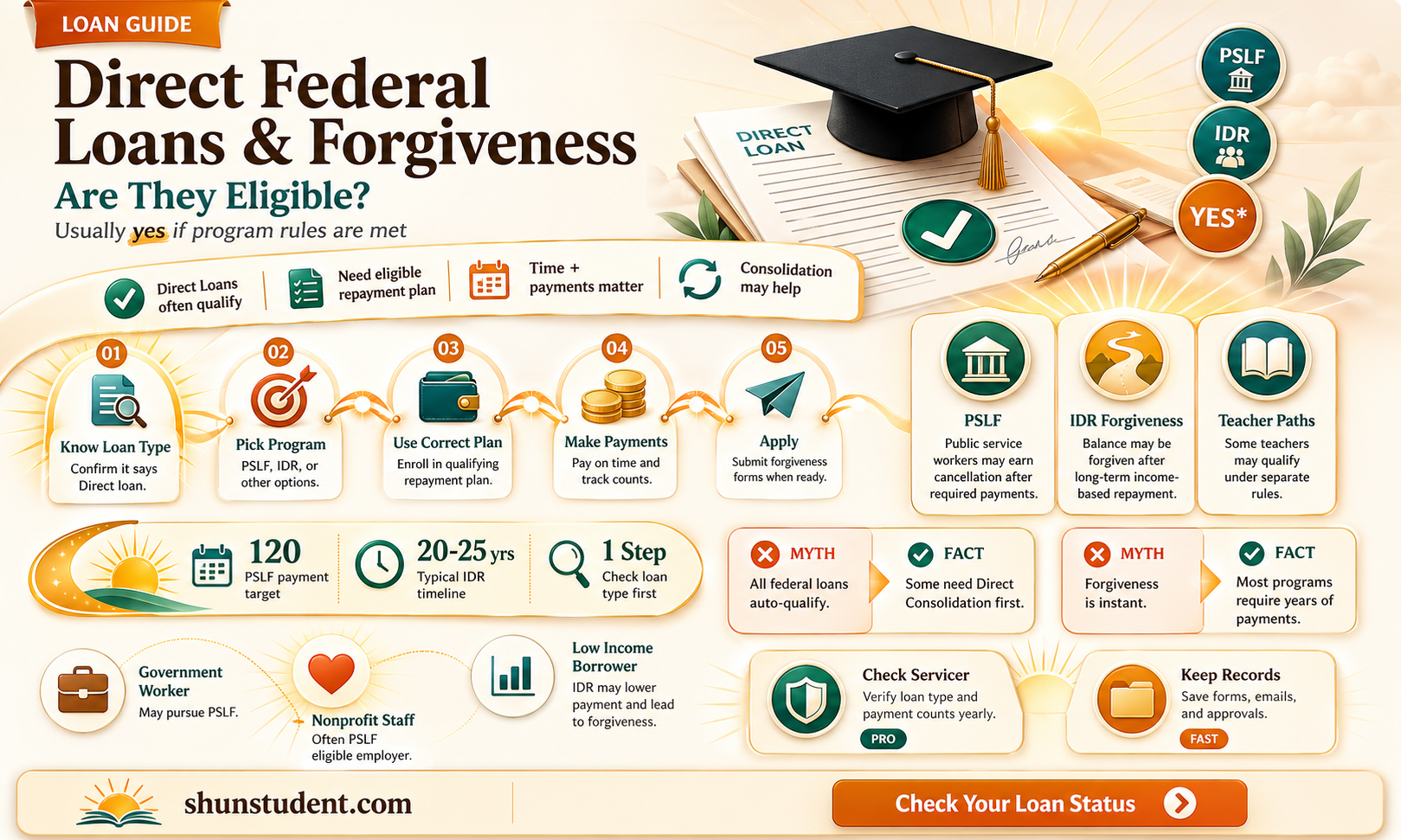

Direct federal loans, also known as Direct Subsidized Loans, Direct Unsubsidized Loans, and Direct PLUS Loans, are eligible for various student loan forgiveness programs offered by the federal government. These programs, such as Public Service Loan Forgiveness (PSLF), Teacher Loan Forgiveness, and income-driven repayment (IDR) plan forgiveness, provide opportunities for borrowers to have a portion or all of their remaining loan balance forgiven after meeting specific requirements. To qualify for forgiveness, borrowers must typically make a certain number of qualifying payments, work in a qualifying public service job, or meet income-driven repayment plan criteria. Understanding the eligibility requirements and application processes for these programs is crucial for borrowers seeking to take advantage of student loan forgiveness options for their direct federal loans.

| Characteristics | Values |

|---|---|

| Eligibility for Forgiveness | Yes, Direct Federal Loans are eligible for student loan forgiveness. |

| Types of Forgiveness Programs | Public Service Loan Forgiveness (PSLF), Teacher Loan Forgiveness, Income-Driven Repayment (IDR) Forgiveness, etc. |

| Requirements for PSLF | 120 qualifying payments while working full-time for a qualifying employer (government or non-profit). |

| Requirements for Teacher Loan Forgiveness | Teaching full-time for 5 consecutive years in a low-income school or educational service agency. |

| IDR Forgiveness | Forgiveness after 20-25 years of qualifying payments under an income-driven repayment plan (e.g., REPAYE, PAYE, IBR, ICR). |

| Loan Types Covered | Direct Subsidized Loans, Direct Unsubsidized Loans, Direct PLUS Loans (for graduates and parents), Direct Consolidation Loans. |

| Non-Eligible Loans | Federal Family Education Loan (FFEL) Program loans and Perkins Loans (unless consolidated into a Direct Consolidation Loan). |

| Tax Implications | Forgiveness under PSLF is tax-free; IDR forgiveness may be taxable (check current tax laws). |

| Application Process | Submit an Employment Certification Form for PSLF annually or when changing employers; apply for forgiveness after meeting program requirements. |

| Recent Updates | Temporary PSLF waiver (ended Oct. 31, 2022) allowed past payments to count, even if not under a qualifying plan. |

| Current Status | Active and available for eligible borrowers with Direct Federal Loans. |

Explore related products

What You'll Learn

![]()

Income-Driven Repayment Plans

Direct federal loans, including those under the William D. Ford Federal Direct Loan Program, are eligible for student loan forgiveness through Income-Driven Repayment (IDR) plans. These plans adjust monthly payments based on income and family size, offering a lifeline to borrowers struggling with high debt-to-income ratios. After 20 or 25 years of qualifying payments, depending on the plan, any remaining balance is forgiven, though borrowers may owe taxes on the forgiven amount. This structure makes IDR plans a critical tool for long-term debt management, particularly for those in low-income professions or with substantial loan balances.

Among the four IDR plans—Revised Pay As You Earn (REPAYE), Pay As You Earn (PAYE), Income-Based Repayment (IBR), and Income-Contingent Repayment (ICR)—each calculates payments differently. For instance, REPAYE caps payments at 10% of discretionary income and is available to all Direct Loan borrowers, while PAYE limits payments to 10% but requires borrowers to have been new borrowers as of October 1, 2007, and have received a disbursement on or after October 1, 2011. IBR offers 10% or 15% caps depending on when the borrower took out their first loan, and ICR sets payments at 20% of discretionary income or the amount of a fixed 12-year repayment plan, whichever is less. Choosing the right plan requires careful consideration of income, loan type, and long-term financial goals.

A common misconception is that IDR plans are only for those in dire financial straits. While they are invaluable for low-income earners, they can also benefit middle-income borrowers with high loan balances. For example, a borrower earning $60,000 annually with $100,000 in loans might see monthly payments drop from $1,000 under the Standard Repayment Plan to $300 under REPAYE. This reduction not only eases monthly financial pressure but also allows borrowers to allocate funds to other priorities, such as saving for retirement or paying off higher-interest debt.

However, IDR plans are not without drawbacks. The extended repayment period means borrowers pay more in interest over time, and forgiven amounts are typically taxable as income, though temporary tax relief is available under the American Rescue Plan Act through 2025. Additionally, borrowers must recertify their income and family size annually, a step that, if missed, can lead to payment increases or capitalization of unpaid interest. To navigate these complexities, borrowers should use tools like the Federal Student Aid Loan Simulator to estimate payments and forgiveness timelines under different plans.

In practice, maximizing the benefits of IDR plans requires proactive management. Borrowers should monitor their income and adjust their plan as needed, especially during periods of unemployment or reduced earnings. For instance, if a borrower loses their job, they can report their income as zero, potentially reducing payments to $0 without penalty. Similarly, those expecting income growth might opt for a plan with a shorter forgiveness timeline, like PAYE, to minimize long-term costs. By understanding the nuances of IDR plans and staying engaged with their repayment strategy, borrowers can turn a daunting debt into a manageable financial commitment.

Student Loan Forgiveness: Potential Impacts on Stock Market Trends

You may want to see also

Explore related products

![]()

Public Service Loan Forgiveness (PSLF)

Direct federal loans are indeed eligible for student loan forgiveness, and one of the most prominent programs offering this benefit is the Public Service Loan Forgiveness (PSLF) program. Established in 2007, PSLF is designed to encourage individuals to pursue careers in public service by forgiving the remaining balance of their federal student loans after they have made 120 qualifying payments while working full-time for a qualifying employer. This program stands out because it offers tax-free forgiveness, unlike some other forgiveness programs that may treat forgiven amounts as taxable income.

To qualify for PSLF, borrowers must have Direct Loans, which are the most common type of federal student loans. Other types of federal loans, such as Federal Family Education Loans (FFEL) or Perkins Loans, must be consolidated into a Direct Consolidation Loan to be eligible. Borrowers must also be employed full-time by a U.S. federal, state, local, or tribal government or not-for-profit organization. Part-time jobs can be combined to meet the full-time requirement, but each employer must qualify separately. It’s crucial to submit the Employment Certification Form (ECF) periodically to ensure payments are tracking correctly toward forgiveness.

One of the most common pitfalls borrowers face with PSLF is misunderstanding the requirements for qualifying payments. Payments must be made under an income-driven repayment (IDR) plan, such as Income-Based Repayment (IBR) or Pay As You Earn (PAYE), to count toward the 120-payment threshold. Payments made under the Standard Repayment Plan, for example, do not qualify unless the payment amount is at least as much as it would be under an IDR plan. Additionally, payments must be made on time and in full to count. Borrowers should regularly review their payment history and employer certifications to avoid surprises.

PSLF is particularly beneficial for borrowers with high loan balances who commit to a career in public service. For example, a borrower with $100,000 in Direct Loans under the IBR plan might pay around $200–$300 per month, depending on their income. After 10 years of qualifying payments, the remaining balance—potentially $80,000 or more—is forgiven tax-free. This makes PSLF a powerful tool for reducing long-term financial burden, especially for those in lower-paying public service roles. However, it requires careful planning and adherence to the program’s strict guidelines.

To maximize the benefits of PSLF, borrowers should take proactive steps. First, consolidate any non-Direct Loans into a Direct Consolidation Loan immediately. Second, enroll in an IDR plan to ensure payments qualify. Third, submit the ECF annually or whenever changing employers to confirm eligibility. Finally, keep detailed records of all payments and certifications. While the PSLF process can be complex, its potential for significant loan forgiveness makes it a worthwhile pursuit for eligible borrowers.

Track Your Student Loan Forgiveness Application Status: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

Teacher Loan Forgiveness Program

Direct federal loans, specifically Direct Subsidized and Unsubsidized Loans, are eligible for the Teacher Loan Forgiveness Program, a targeted initiative designed to alleviate student debt for educators in low-income schools. This program offers a clear pathway for teachers to reduce their loan burden, but eligibility hinges on specific criteria. To qualify, teachers must work full-time for five consecutive academic years in a designated low-income school or educational service agency. The school’s eligibility is determined by its listing in the Annual Directory of Designated Low-Income Schools for Teacher Cancellation Benefits, updated annually by the U.S. Department of Education. This requirement ensures the program’s benefits are directed toward areas with the greatest need.

The forgiveness amounts under this program are tiered based on the teacher’s subject area and qualifications. Educators in mathematics, science, or special education can receive up to $17,500 in loan forgiveness, while those in other fields are eligible for up to $5,000. These amounts are not insignificant, particularly for early-career teachers facing substantial loan balances. However, it’s crucial to note that only Direct Loans are eligible; Federal Family Education Loans (FFEL) or Perkins Loans do not qualify unless consolidated into a Direct Consolidation Loan. Teachers should verify their loan type and consider consolidation if necessary to access this benefit.

Applying for the Teacher Loan Forgiveness Program involves submitting a completed Teacher Loan Forgiveness Application to the loan servicer after the five-year teaching commitment. The application requires certification from the school’s chief administrative officer, confirming the teacher’s employment and the school’s low-income status. Teachers should keep detailed records of their employment and loan information to streamline the process. It’s also advisable to submit the application promptly after completing the five-year requirement to avoid delays in receiving forgiveness.

While the Teacher Loan Forgiveness Program offers substantial relief, it’s not a one-size-fits-all solution. Teachers pursuing this option should also explore additional forgiveness programs, such as Public Service Loan Forgiveness (PSLF), which requires 10 years of qualifying payments but can forgive the remaining balance. Comparing these programs can help educators maximize their debt relief. For instance, a teacher with high loan balances might benefit more from PSLF, while those with smaller debts may find the Teacher Loan Forgiveness Program more advantageous. Strategic planning and understanding the nuances of each program are key to making informed decisions.

Finally, teachers should be aware of potential pitfalls. For example, switching schools mid-commitment could disrupt eligibility if the new school is not designated as low-income. Additionally, part-time teaching or gaps in employment may invalidate the consecutive years requirement. Staying informed about program updates and maintaining consistent employment in eligible schools are essential for success. By carefully navigating these details, teachers can leverage the Teacher Loan Forgiveness Program to significantly reduce their financial burden while contributing to underserved communities.

Protect Your Student Loan Forgiveness: Strategies to Avoid Taxable Income

You may want to see also

Explore related products

![]()

Disability Discharge Eligibility

Direct federal loans can be discharged due to total and permanent disability, offering a lifeline to borrowers facing significant health challenges. This provision, known as Disability Discharge, is a critical component of student loan forgiveness programs, designed to alleviate financial burdens for those who cannot work due to a disability. To qualify, borrowers must meet specific criteria, which include providing documentation of their disability from a physician, the Department of Veterans Affairs, or the Social Security Administration. Understanding the eligibility requirements and application process is essential for borrowers seeking relief through this program.

Eligibility Criteria and Documentation

To be eligible for a Disability Discharge, borrowers must demonstrate that they are totally and permanently disabled. This means the individual is unable to engage in any substantial gainful activity due to a physical or mental impairment that has lasted or is expected to last for a continuous period of 60 months or more, or is expected to result in death. The documentation required varies depending on the source. For example, a physician’s certification must be provided on the U.S. Department of Education’s form, while Social Security Administration (SSA) notices of award for Social Security Disability Insurance (SSDI) or Supplemental Security Income (SSI) based on disability can also serve as proof. Veterans can submit documentation from the Department of Veterans Affairs showing a service-connected disability rating of 100 percent.

Application Process and Post-Discharge Monitoring

Applying for a Disability Discharge involves submitting the appropriate documentation to the loan servicer or the U.S. Department of Education. Once approved, the borrower’s federal student loans are discharged, and they are no longer required to make payments. However, there is a three-year post-discharge monitoring period during which the borrower must meet certain conditions to avoid reinstatement of the loans. These conditions include not earning income above the poverty guideline for a family of two in the borrower’s state and not receiving a new federal student loan or TEACH Grant. Failure to comply with these conditions can result in the reinstatement of the discharged loans.

Practical Tips for a Smooth Application

Navigating the Disability Discharge process can be complex, but several practical tips can help ensure a smoother experience. First, gather all necessary documentation before starting the application to avoid delays. If using a physician’s certification, ensure the doctor completes the form accurately and thoroughly. For SSA recipients, keep a copy of the notice of award readily available. Borrowers should also monitor their income during the post-discharge monitoring period to avoid inadvertently triggering loan reinstatement. Additionally, staying in contact with the loan servicer and keeping records of all communications can provide a safety net in case of disputes or errors.

Comparative Analysis with Other Forgiveness Programs

Compared to other student loan forgiveness programs, Disability Discharge stands out for its focus on borrowers with severe health conditions. While programs like Public Service Loan Forgiveness (PSLF) require a specific number of qualifying payments and employment in public service, Disability Discharge does not have such prerequisites. Similarly, income-driven repayment (IDR) plans offer forgiveness after 20–25 years of payments, but they do not address the immediate needs of borrowers who are unable to work due to disability. Disability Discharge provides immediate relief, making it a uniquely tailored solution for those facing total and permanent disability. However, the post-discharge monitoring period is a distinct feature that requires careful attention, unlike other programs that do not impose such conditions after forgiveness is granted.

COVID Relief Bill: Does It Include Student Loan Forgiveness?

You may want to see also

Explore related products

![]()

Closed School Discharge Rules

Direct Federal Loans, including Direct Subsidized, Unsubsidized, PLUS, and Consolidation Loans, are eligible for student loan forgiveness under specific circumstances, one of which is the Closed School Discharge program. This program offers a lifeline to borrowers whose educational institutions shut down before they could complete their programs. To qualify, borrowers must meet precise criteria, such as being enrolled or having withdrawn within a defined period before the school’s closure. Understanding these rules is crucial for those seeking relief from their federal student loan obligations.

The Closed School Discharge Rules outline a step-by-step process for borrowers to apply for loan forgiveness. First, confirm that your school closed while you were enrolled or shortly after you left. If you were on an approved leave of absence when the school closed, you may still qualify. Next, ensure you did not complete your program through a teach-out (a plan allowing students to finish their studies elsewhere) or transfer credits to another institution. Borrowers who meet these conditions can submit a discharge application to their loan servicer, providing documentation of their enrollment status at the time of closure.

One critical aspect of the Closed School Discharge Rules is the timeline for eligibility. If you withdrew from the school more than 120 days before its closure, you are generally ineligible for discharge. However, if you were enrolled or had withdrawn within 120 days of the closure, you may qualify. For example, if a student withdrew 90 days before the school closed, they could apply for discharge. Conversely, a student who left 150 days prior would not meet the criteria. This strict timeline underscores the importance of acting promptly when a school closes.

While the Closed School Discharge Rules offer a pathway to forgiveness, borrowers should be aware of potential pitfalls. For instance, if you received a refund of tuition or other credits after withdrawing, your discharge amount may be reduced accordingly. Additionally, loans in default may still qualify, but borrowers must navigate the discharge process carefully. It’s advisable to consult with your loan servicer or a financial advisor to ensure all requirements are met. Proper documentation, such as official transcripts or withdrawal notices, can strengthen your application and expedite the approval process.

In conclusion, the Closed School Discharge Rules provide a targeted solution for borrowers affected by school closures, but navigating the program requires attention to detail and adherence to specific guidelines. By understanding the eligibility criteria, timelines, and potential challenges, borrowers can maximize their chances of successfully discharging their Direct Federal Loans. This program not only offers financial relief but also underscores the government’s commitment to protecting students from unforeseen institutional failures.

Maryland's Tax Treatment of Student Loan Forgiveness: What You Need to Know

You may want to see also

Frequently asked questions

Not all direct federal loans are eligible for every forgiveness program. Eligibility depends on the specific program, such as Public Service Loan Forgiveness (PSLF) or income-driven repayment (IDR) plans. Generally, Direct Subsidized Loans, Direct Unsubsidized Loans, Direct PLUS Loans, and Direct Consolidation Loans are eligible, but Perkins Loans or FFEL Loans must be consolidated into a Direct Loan to qualify.

Yes, direct federal loans are eligible for PSLF if the borrower works full-time for a qualifying employer (e.g., government or nonprofit) and makes 120 qualifying payments under an eligible repayment plan. Other federal loans, like FFEL or Perkins Loans, must be consolidated into a Direct Loan to qualify for PSLF.

Yes, direct federal loans are eligible for forgiveness under IDR plans after 20–25 years of qualifying payments, depending on the plan. This includes Direct Subsidized, Unsubsidized, PLUS, and Consolidation Loans. However, Parent PLUS Loans must be consolidated and enrolled in an IDR plan to qualify for forgiveness.