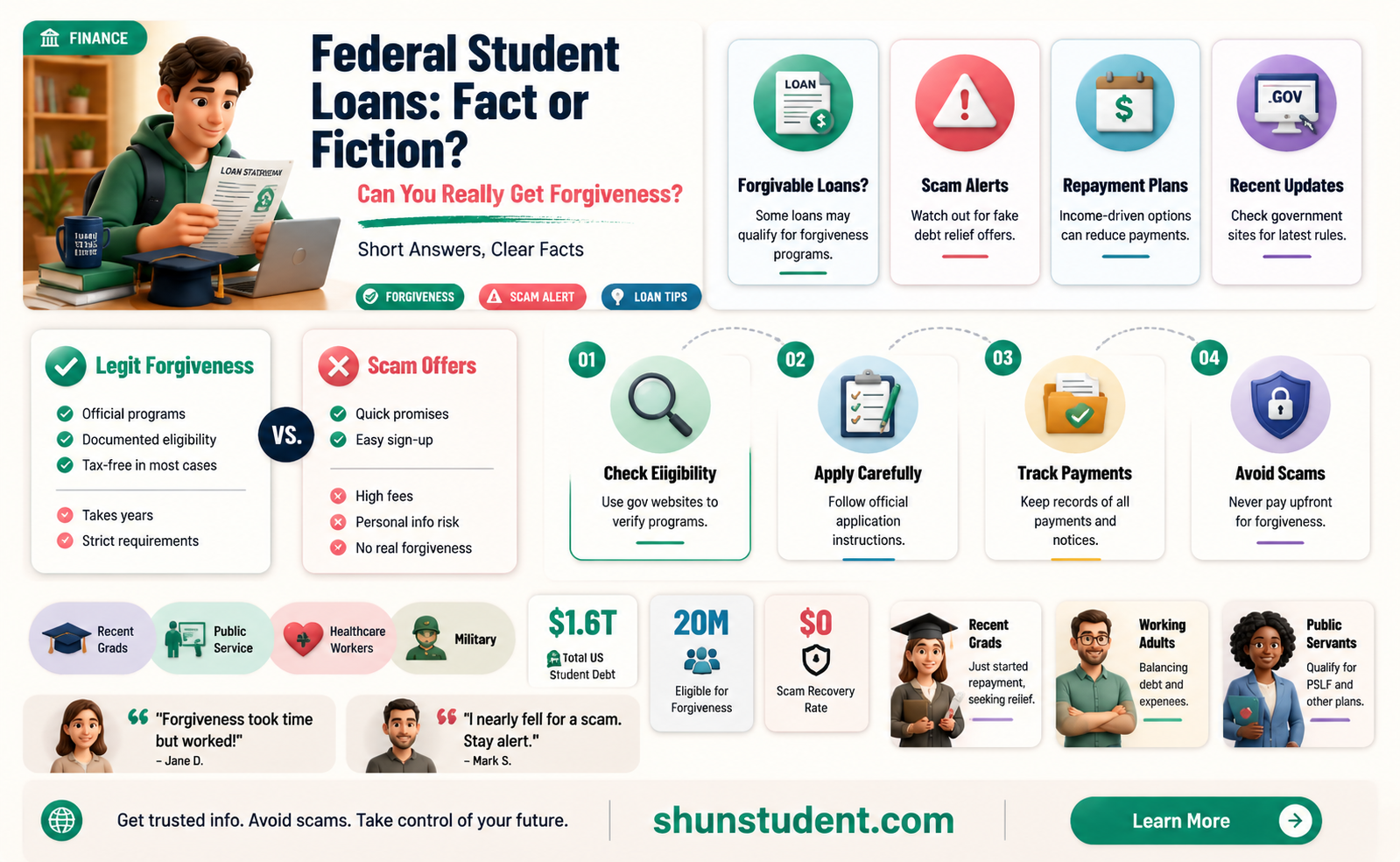

Federal student loan forgiveness is a legitimate program designed to help borrowers manage their debt under specific conditions, but it’s often surrounded by misinformation and scams. Genuine forgiveness options, such as Public Service Loan Forgiveness (PSLF) and income-driven repayment plans, exist for those who meet eligibility criteria, such as working in public service or making consistent payments based on income. However, scammers exploit confusion around these programs by promising immediate debt relief or charging fees for services borrowers can access for free. To avoid scams, borrowers should verify information through official government websites, such as the U.S. Department of Education, and never share personal details with unverified sources. Understanding the difference between legitimate forgiveness programs and fraudulent schemes is crucial for protecting financial well-being.

| Characteristics | Values |

|---|---|

| Are Federal Student Loans Forgivable? | Yes, under specific programs and conditions. |

| Common Forgiveness Programs | Public Service Loan Forgiveness (PSLF), Teacher Loan Forgiveness, Income-Driven Repayment (IDR) Forgiveness. |

| Eligibility Requirements | Varies by program (e.g., 10 years of qualifying payments for PSLF, 5 years of teaching in low-income schools for Teacher Loan Forgiveness). |

| Scam Risks | Scammers may charge fees for "loan forgiveness" services or request personal information. |

| Official Resources | U.S. Department of Education, Federal Student Aid website (studentaid.gov). |

| Red Flags for Scams | Requests for upfront payment, promises of immediate forgiveness, unsolicited calls or emails. |

| Cost for Legitimate Forgiveness | Free to apply through official government channels. |

| Timeframe for Forgiveness | Typically 10–25 years, depending on the program and repayment plan. |

| Tax Implications | Some forgiven amounts may be taxable, depending on the program. |

| Impact on Credit Score | Forgiveness does not negatively impact credit score if done legitimately. |

| Recent Updates (as of 2023) | Temporary changes to PSLF and IDR forgiveness due to COVID-19 relief measures. |

Explore related products

What You'll Learn

- Eligibility Criteria: Income-driven plans, public service, disability, school closure, or death may qualify

- Loan Forgiveness Programs: Public Service Loan Forgiveness (PSLF), Teacher Loan Forgiveness, and more

- Scam Warning Signs: Upfront fees, guaranteed forgiveness, or fake government affiliations are red flags

- Repayment Plans: Income-driven plans can lead to forgiveness after 20-25 years of payments

- Debt Relief Updates: Federal policies and temporary waivers may expand forgiveness opportunities

![]()

Eligibility Criteria: Income-driven plans, public service, disability, school closure, or death may qualify

Federal student loan forgiveness isn’t a scam, but it’s also not a free-for-all. Specific eligibility criteria determine who qualifies, and understanding these pathways is crucial for borrowers seeking relief. Among the most common routes are income-driven repayment plans, public service, disability, school closure, and death. Each of these categories has distinct requirements, and navigating them requires attention to detail and proactive planning.

Income-driven repayment plans are designed for borrowers whose federal student loan payments are disproportionately high compared to their income. These plans, such as Pay As You Earn (PAYE) or Revised Pay As You Earn (REPAYE), cap monthly payments at a percentage of discretionary income—typically 10-20%. After 20-25 years of consistent payments, the remaining balance may be forgiven. For example, a borrower earning $40,000 annually with $60,000 in loans might pay as little as $200 monthly under REPAYE, with forgiveness possible after 20 years. However, forgiven amounts may be taxed as income, so borrowers should consult a tax professional to plan accordingly.

Public service workers—those employed full-time by government or qualifying nonprofit organizations—may qualify for Public Service Loan Forgiveness (PSLF) after 10 years of eligible payments. Teachers, nurses, and government employees often fall into this category. A critical requirement is making 120 qualifying payments while working full-time in public service. For instance, a social worker earning $50,000 annually could have their remaining balance forgiven after a decade of service, provided they’ve adhered to the program’s strict guidelines. Caution: Only Direct Loans qualify, and payments must be made under an income-driven plan.

Disability discharge offers relief for borrowers with permanent disabilities, but the process is rigorous. Applicants must provide documentation from the Social Security Administration, a physician, or the Department of Veterans Affairs. For example, a veteran with a service-related disability could qualify for discharge, eliminating their loan obligation entirely. Importantly, recipients of disability discharge may be subject to a three-year monitoring period during which their income and employment are reviewed.

School closure and death are less common but equally valid pathways. If a borrower’s school closes while they’re enrolled or shortly after withdrawal, they may qualify for a discharge. For instance, students of a for-profit college that abruptly shut down could have their loans forgiven. In the case of death, federal student loans are discharged upon verification of the borrower’s passing, relieving their estate or cosigner of liability. Documentation, such as a death certificate, is required for processing.

Understanding these eligibility criteria empowers borrowers to take actionable steps toward loan forgiveness. Whether through income-driven plans, public service, disability, school closure, or death, each pathway demands specific documentation and adherence to rules. By researching and applying for the appropriate program, borrowers can transform overwhelming debt into manageable—or even forgivable—obligations.

When Will Student Loan Forgiveness Apply? Updates and Timeline

You may want to see also

Explore related products

![]()

Loan Forgiveness Programs: Public Service Loan Forgiveness (PSLF), Teacher Loan Forgiveness, and more

Federal student loans can indeed be forgiven through legitimate programs, but navigating these options requires precision and awareness. Among the most prominent are the Public Service Loan Forgiveness (PSLF) program and Teacher Loan Forgiveness, each designed to reward specific career paths with debt relief. PSLF, for instance, forgives the remaining balance on Direct Loans after 120 qualifying payments for those employed full-time in public service, such as government or nonprofit organizations. Teacher Loan Forgiveness, on the other hand, offers up to $17,500 in forgiveness for educators who teach full-time for five consecutive years in low-income schools. These programs are not scams but require strict adherence to eligibility criteria and documentation.

To qualify for PSLF, borrowers must consolidate their loans into a Direct Consolidation Loan if necessary and enroll in an income-driven repayment plan. This ensures monthly payments are capped at a manageable percentage of income, typically 10-20% of discretionary earnings. Teachers seeking forgiveness must submit an application after completing their five-year service and provide certification from their school’s chief administrative officer. Both programs demand meticulous record-keeping, as missed payments or incorrect paperwork can disqualify applicants. For example, PSLF requires proof of employment certification annually or whenever switching employers to avoid complications later.

Beyond PSLF and Teacher Loan Forgiveness, other programs cater to specific professions or circumstances. The Nurse Corps Loan Forgiveness program forgives up to 85% of nursing education loans for registered nurses working in underserved areas. Similarly, the Perkins Loan Cancellation and Discharge program offers forgiveness for teachers, nurses, firefighters, and others in public service roles, with cancellation increasing incrementally over five years. These programs highlight the government’s commitment to supporting essential services while alleviating student debt burdens. However, borrowers must proactively research and apply for these opportunities, as forgiveness is not automatic.

A critical caution is the proliferation of scams targeting borrowers seeking loan forgiveness. Fraudulent companies often promise immediate relief or charge fees for services that are otherwise free, such as enrolling in income-driven repayment plans. Legitimate programs, including PSLF and Teacher Loan Forgiveness, are administered through the U.S. Department of Education and require no upfront payment. Borrowers should verify program details on official government websites and avoid third-party services that guarantee forgiveness in exchange for payment. Staying informed and vigilant is key to distinguishing between genuine opportunities and deceptive schemes.

In conclusion, federal student loan forgiveness is a real and achievable goal for those in qualifying professions, but it demands diligence and adherence to program rules. Whether pursuing PSLF, Teacher Loan Forgiveness, or other specialized programs, borrowers must understand eligibility requirements, maintain accurate records, and avoid scams. By leveraging these opportunities, individuals can significantly reduce their debt burden while contributing to vital public service roles. The key takeaway is that forgiveness is not a scam but a structured benefit for those who meet specific criteria and follow the process carefully.

Mastering Income Calculation for Student Loan Forgiveness Success

You may want to see also

Explore related products

![]()

Scam Warning Signs: Upfront fees, guaranteed forgiveness, or fake government affiliations are red flags

Federal student loan forgiveness is a real possibility, but scammers exploit confusion around the process to prey on vulnerable borrowers. One of the most glaring red flags is the demand for upfront fees. Legitimate loan servicers and government programs never require payment before processing your application. If a company insists on a fee to "unlock" forgiveness or "expedite" your case, it’s a scam. These fees often range from $200 to $1,000, with some scammers even pushing for recurring monthly payments. Remember: you should never pay for assistance with federal student loan programs. The U.S. Department of Education provides free resources and support through its official website and loan servicers.

Another warning sign is the promise of guaranteed forgiveness. No company or individual can guarantee that your loans will be forgiven, as eligibility depends on specific criteria like your repayment plan, employment, and loan type. Scammers use this tactic to create a false sense of urgency, pressuring borrowers into handing over personal information or money. For instance, they might claim, "We’ve partnered with the government to forgive 100% of your debt!" In reality, programs like Public Service Loan Forgiveness (PSLF) or income-driven repayment plans have strict requirements that must be met over time. If it sounds too good to be true, it probably is.

Fake government affiliations are a third major red flag. Scammers often impersonate official agencies or use names that sound similar to legitimate organizations, like "Federal Student Loan Assistance" or "Department of Education Services." They may even use official-looking logos or websites to appear credible. To avoid falling for this, always verify the company’s legitimacy by checking the Federal Student Aid website or contacting your loan servicer directly. A simple rule: if you didn’t initiate contact with the organization, be skeptical.

To protect yourself, follow these practical steps: first, research any company claiming to help with loan forgiveness. Check reviews, look for complaints with the Better Business Bureau, and verify their contact information. Second, never share personal information like your FSA ID or Social Security number with unverified sources. Third, use official channels for loan forgiveness applications, such as the studentaid.gov website. Finally, report suspicious activity to the Federal Trade Commission (FTC) or your state’s attorney general. By staying vigilant and informed, you can avoid scams and navigate the loan forgiveness process safely.

Does Deferment Impact Student Loan Forgiveness Eligibility and Timeline?

You may want to see also

Explore related products

![]()

Repayment Plans: Income-driven plans can lead to forgiveness after 20-25 years of payments

Federal student loan borrowers often face a mountain of debt, but income-driven repayment (IDR) plans offer a structured path toward potential forgiveness. These plans, which include options like Pay As You Earn (PAYE), Revised Pay As You Earn (REPAYE), Income-Based Repayment (IBR), and Income-Contingent Repayment (ICR), adjust monthly payments based on income and family size. The key benefit? After 20 to 25 years of consistent payments, the remaining balance is forgiven. For instance, REPAYE forgives loans after 20 years for undergraduate loans and 25 years for graduate loans, while IBR offers forgiveness after 20 or 25 years depending on when the loan was taken out. This isn’t a scam—it’s a government-backed program designed to provide relief for borrowers with limited income relative to their debt.

To qualify for forgiveness through an IDR plan, borrowers must make timely payments each month, typically defined as payments received within 15 days of the due date. Missing payments or switching to a non-IDR plan can reset the forgiveness clock. For example, if a borrower makes 10 years of qualifying payments and then switches to a standard repayment plan, those 10 years no longer count toward the 20- or 25-year forgiveness timeline. Additionally, borrowers must recertify their income and family size annually to remain on an IDR plan. Failure to recertify can result in a return to the standard repayment plan, which does not offer forgiveness.

One critical aspect often overlooked is the tax implications of loan forgiveness. Under current law, forgiven amounts are treated as taxable income, which could result in a significant tax bill. For example, if $50,000 is forgiven after 25 years, the borrower may owe taxes on that amount in the year of forgiveness. However, the American Rescue Plan Act of 2021 temporarily exempts student loan forgiveness from taxation through 2025, providing a window of relief. Borrowers should consult a tax professional to plan for potential tax liabilities beyond this period.

Choosing the right IDR plan requires careful consideration of individual circumstances. For instance, REPAYE caps monthly payments at 10% of discretionary income and offers interest subsidies for the first three years, making it attractive for borrowers with high debt-to-income ratios. In contrast, IBR limits payments to 10% or 15% of discretionary income depending on when the loan was taken out, but it may result in higher total payments over time. Borrowers should use the Federal Student Aid Loan Simulator to compare plans and estimate long-term costs, including potential forgiveness amounts.

While IDR plans offer a legitimate path to forgiveness, they aren’t a one-size-fits-all solution. Borrowers with high incomes or those expecting significant salary increases may find that standard repayment plans or refinancing with private lenders offer better terms. Additionally, public service workers can pursue Public Service Loan Forgiveness (PSLF), which forgives loans after 10 years of qualifying payments and employment. For others, IDR plans provide a lifeline, balancing manageable monthly payments with the promise of eventual forgiveness. The key is to stay informed, make consistent payments, and leverage available resources to navigate the complexities of federal student loan repayment.

Struggling with Student Debt? Why Loan Forgiveness Isn't Always an Option

You may want to see also

Explore related products

![]()

Debt Relief Updates: Federal policies and temporary waivers may expand forgiveness opportunities

Federal student loan forgiveness isn’t a myth, but it’s also not a free-for-all. Recent updates to federal policies and temporary waivers have expanded opportunities for borrowers to shed their debt, though navigating these changes requires attention to detail. For instance, the Public Service Loan Forgiveness (PSLF) program, which forgives remaining balances after 120 qualifying payments for public servants, has been temporarily revised to count previously ineligible payments. This means teachers, nurses, and nonprofit workers who were previously denied forgiveness may now qualify—but only if they act before the waiver expires in October 2023.

To take advantage of these updates, borrowers must follow specific steps. First, consolidate any Federal Family Education Loans (FFEL) or Perkins Loans into a Direct Consolidation Loan, as only Direct Loans are eligible for most forgiveness programs. Second, submit a PSLF form to ensure all payments are counted correctly, even those made under different repayment plans. Third, monitor the Federal Student Aid website for updates, as new policies or extensions may emerge. Ignoring these steps could mean missing out on thousands in debt relief.

Critics argue these temporary waivers create confusion, but proponents counter that they address long-standing administrative failures. For example, the waiver allows payments made under graduated or extended repayment plans to qualify for PSLF, correcting years of misguidance from loan servicers. Similarly, the limited-time waiver for income-driven repayment (IDR) forgiveness counts time spent in any repayment status toward the 20- or 25-year forgiveness threshold, potentially erasing debt for borrowers who’ve been in repayment for decades.

Practical tips for maximizing these opportunities include keeping detailed records of all payments and employment certifications. Borrowers should also consider switching to an IDR plan if they haven’t already, as these plans cap monthly payments at a percentage of discretionary income and offer forgiveness after 20–25 years. While these updates aren’t a scam, they are time-sensitive and require proactive steps. Borrowers who fail to act before deadlines risk losing access to these expanded forgiveness opportunities, leaving them back where they started.

Supreme Court's Decision on Student Loan Forgiveness: What Happened?

You may want to see also

Frequently asked questions

Yes, federal student loans can be forgiven under specific programs like Public Service Loan Forgiveness (PSLF), Teacher Loan Forgiveness, or income-driven repayment (IDR) plans after a certain number of qualifying payments.

Qualification depends on the program. For example, PSLF requires 10 years of qualifying payments while working full-time for a government or nonprofit organization. IDR plans forgive remaining balances after 20–25 years of payments.

No, federal student loan forgiveness is legitimate, but beware of scams. The government does not charge fees for forgiveness applications, so avoid companies promising forgiveness for a fee.

No, private student loans are not eligible for federal forgiveness programs. Private lenders may offer their own relief options, but they are rare and not guaranteed.