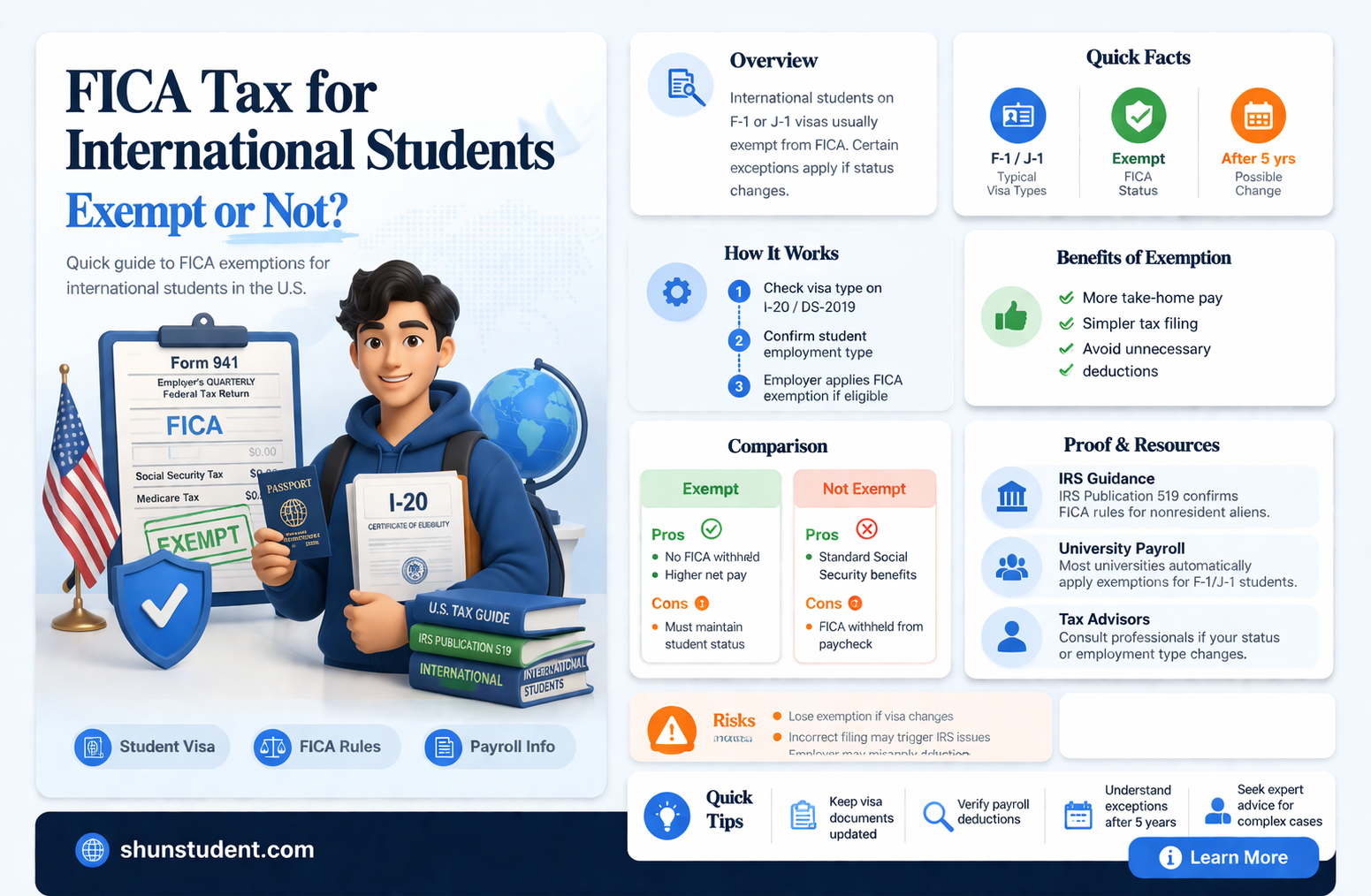

International students on specific visas are exempt from paying FICA taxes, which include Social Security and Medicare taxes, for a certain period. FICA exemptions are available to international students, scholars, professors, teachers, and researchers in the US on nonimmigrant visas such as F-1, J-1, M-1, or Q-1/Q-2, provided they are non-residents for tax purposes. However, this exemption does not apply to spouses and dependents, and the duration of the exemption varies based on visa type and other factors. Let's delve into the specifics of FICA exemptions for international students in the United States.

| Characteristics | Values |

|---|---|

| Who is exempt from FICA taxes? | International students, scholars, professors, teachers, trainees, researchers, physicians, au pairs, summer camp workers, and other non-student aliens |

| Visa status | F-1, J-1, M-1, Q-1/Q-2 nonimmigrant statuses |

| Time period | Exempt for the first 5 calendar years of physical presence in the US |

| Tax status | Nonresident aliens for tax purposes |

| Work type | Services must be allowed by U.S. Citizenship and Immigration Services (USCIS) |

| Work location | Employed by a school, college, or university where the student is pursuing a course of study |

| Other exemptions | J-1 Scholars, Teachers, Researchers, Trainees, and Physicians in J-1 status are exempt for the first 2 calendar years |

| Who is not exempt? | Spouses and dependents of alien students, scholars, trainees, teachers, or researchers in F-2, J-2, or M-2 status |

| Persons in H-1B, TN, O-1, or E-3 status |

Explore related products

![LLC Beginner's Guide [All-in-1]: Everything on How to Start, Run, and Grow Your First Company Without Prior Experience. Includes Essential Tax Hacks, Critical Legal Strategies, and Expert Insights](https://m.media-amazon.com/images/I/61SXdyvdqKL._AC_UY218_.jpg)

What You'll Learn

- International students with F-1 and J-1 visas are exempt from FICA taxes

- FICA exemption for students employed by their school, college, or university

- International students with M-1 or Q-1/Q-2 visas are exempt from FICA taxes

- FICA exemption does not apply to spouses and children of international students

- International students are exempt from FICA taxes for five calendar years

![]()

International students with F-1 and J-1 visas are exempt from FICA taxes

International students with F-1 and J-1 visas are indeed exempt from FICA taxes, which include Social Security and Medicare taxes. This exemption applies to international students, scholars, professors, teachers, trainees, researchers, physicians, au pairs, summer camp workers, and other non-student aliens. However, this exemption is contingent on their nonimmigrant status and the nature of their employment.

To be exempt from FICA taxes, individuals must be temporarily present in the United States with specific nonimmigrant visas, such as F-1, J-1, M-1, or Q-1/Q-2 visas. These visas indicate that the individuals are nonresident aliens for tax purposes. The exemption applies to wages earned by these individuals as long as their services are allowed by the U.S. Citizenship and Immigration Services (USCIS) and have not met the substantial presence criteria to be considered residents for tax purposes.

The exemption from FICA taxes for individuals on F-1 and J-1 visas typically lasts for a certain period. For J-1 scholars, teachers, researchers, and other non-students, the exemption is valid for the first two calendar years of their presence in the United States. After this period, they become residents for tax purposes and are subject to FICA withholding. On the other hand, international students on F-1 visas usually have a five-year exemption from FICA taxes, which includes any period of "practical training" or "optional practical training" allowed by the USCIS, as long as they maintain their nonresident status.

It is important to note that the FICA exemption does not apply to spouses and dependents of individuals with F-1, J-1, or other specified visas. These family members are subject to Medicare taxes on any wages they earn in the United States. Additionally, the exemption is only valid as long as the individual's employment aligns with the purpose for which the visa was issued. Changing to a non-exempt immigration status or obtaining a special protected status can also impact the exemption eligibility.

International Students: Medicare Eligibility Explained

You may want to see also

Explore related products

![]()

FICA exemption for students employed by their school, college, or university

FICA, or the Federal Insurance Contributions Act, imposes a tax on wages paid to employees. This tax is used to fund Social Security and Medicare. While FICA taxes generally apply to all employees, there are some exemptions, including for certain international students.

International students in F-1, J-1, M-1, Q-1, or Q-2 nonimmigrant status are exempt from FICA taxes for the first five calendar years of their physical presence in the United States. This exemption applies regardless of whether the student is employed on-campus or off-campus, as long as they are enrolled at least half-time and their employment is for the purpose of pursuing a course of study. After the five-year exemption period, international students are generally classified as residents for tax purposes and become subject to FICA withholding.

Additionally, students employed by a school, college, or university where they are enrolled and pursuing a course of study may be exempt from FICA taxes, regardless of their citizenship status. This exemption applies to both part-time and full-time students, as long as their relationship with the educational institution is predominantly educational rather than service-oriented. The educational institution must also meet certain requirements, such as providing formal instruction and maintaining a regular faculty, curriculum, and enrolled body of students.

It is important to note that the FICA exemption for students employed by their school, college, or university is not automatic, and students must meet certain criteria to qualify. Students should consult with their educational institution and tax advisors to determine their eligibility for any FICA exemptions.

In summary, international students may be exempt from FICA taxes under certain conditions, including their nonimmigrant status and employment by their school, college, or university. However, it is crucial to carefully evaluate the specific circumstances and seek professional guidance to determine the applicability of any exemptions.

Hiring International Students: US Companies Not Ready?

You may want to see also

Explore related products

![]()

International students with M-1 or Q-1/Q-2 visas are exempt from FICA taxes

International students on specific visas are exempt from paying FICA taxes, which include Social Security and Medicare taxes. International students, scholars, professors, teachers, trainees, researchers, physicians, au pairs, summer camp workers, and other non-student aliens are exempt from FICA taxes if they hold F-1, J-1, M-1, or Q-1/Q-2 nonimmigrant visas. This exemption is valid as long as they are classified as non-residents for tax purposes and their services are allowed by the U.S. Citizenship and Immigration Services (USCIS).

The exemption from FICA taxes for international students with M-1 or Q-1/Q-2 visas is time-bound. These students are generally exempt from FICA taxes for the first five calendar years of their physical presence in the United States. During this period, they are considered non-resident aliens for tax purposes. However, after this five-year period, they may be reclassified as resident aliens for tax purposes, making them subject to FICA tax withholding.

It is important to note that the exemption from FICA taxes for M-1 or Q-1/Q-2 visa holders does not apply to their spouses or dependents. Spouses and dependents in F-2, J-2, or M-2 status are considered liable for Medicare taxes on any wages they earn in the United States. Additionally, the FICA exemption is only valid as long as the services performed by the international students are closely connected to the purpose for which their visas were issued.

International students with M-1 or Q-1/Q-2 visas can benefit from the exemption from FICA taxes during their studies in the United States. However, they should be mindful of the time limitations and the conditions related to their visa status and purpose to ensure they remain eligible for the exemption. It is always advisable to seek official guidance from the IRS or immigration authorities to understand the specific requirements and any updates to the regulations.

International Students: Can They Study Law in the US?

You may want to see also

Explore related products

![]()

FICA exemption does not apply to spouses and children of international students

International students in F-1, J-1, M-1, Q-1, or Q-2 nonimmigrant status are exempt from FICA taxes for a certain period of time. FICA taxes, which include Social Security and Medicare taxes, generally apply to all wage income received in the US. However, international students who are employed by their school, college, or university and are enrolled at least half-time may qualify for the "'student FICA exemption.'" This exemption is valid during the school year, including the summer months when school is not in session if the student is engaged in "'practical training.'"

While international students may benefit from the FICA exemption under certain conditions, it is important to note that this exemption does not extend to their spouses and children. Spouses and children who hold F-2, J-2, M-2, or Q-3 nonimmigrant visas are not exempt from FICA taxes. They are generally considered liable for Social Security and Medicare taxes on any wages they earn in the US. This is because they have not entered the country for the primary purpose of education or training, which is a key criterion for the student FICA exemption.

The FICA exemption for international students also comes with several other limitations. Firstly, it only applies to on-campus employment that is closely connected to the purpose of their visa. Off-campus jobs or working for other employers do not qualify for the exemption. Additionally, international students who change to a different immigration status that is not exempt or who become resident aliens may lose their FICA exemption status.

It is worth mentioning that, in addition to international students, certain other categories of individuals may be exempt from FICA taxes. For example, J-1 scholars, teachers, researchers, and other non-students in J-1 status are considered nonresidents for tax purposes and are exempt from FICA taxes for their first two calendar years in the US. However, after this period, they will become residents for tax purposes and will be subject to FICA withholding.

In conclusion, while international students in specific nonimmigrant statuses may be exempt from FICA taxes under the "student FICA exemption," this exemption does not apply to their spouses and children holding F-2, J-2, M-2, or Q-3 nonimmigrant visas. These spouses and children are generally liable for Social Security and Medicare taxes on their US-sourced income. It is important for international students and their families to understand the tax implications of their visa statuses and seek appropriate guidance from relevant authorities or professionals.

USC Financial Aid: International Students' Options

You may want to see also

![]()

International students are exempt from FICA taxes for five calendar years

International students on specific visas are exempt from paying FICA taxes for a certain period. FICA, or the Federal Insurance Contributions Act, is a US federal employment tax imposed on both employees and employers to fund Social Security and Medicare programmes.

International students on F-1, J-1, M-1, or Q-1/Q-2 nonimmigrant visas are exempt from FICA taxes on their wages for five calendar years. This exemption also applies to any period in which the student is in "practical training" or "optional practical training" allowed by the US Citizenship and Immigration Services (USCIS), provided they are still classified as nonresident aliens for tax purposes.

The exemption does not apply to spouses and children of these visa holders, who are in F-2, J-2, M-2, or Q-3 nonimmigrant status. It also does not apply to students who change to an immigration status that is not exempt or to a special protected status. Additionally, students who become resident aliens for tax purposes are no longer exempt and are subject to FICA tax withholding.

It is important to note that the exemption only applies to international students who are employed by a school, college, or university where they are enrolled full-time and pursuing a course of study. An examination of the student's primary relationship with the educational institution will be conducted to determine if employment or education is predominant.

Entrance Exams: Cambridge's International Student Requirements

You may want to see also

Frequently asked questions

International students with F-1, J-1, M-1, or Q-1/Q-2 nonimmigrant statuses are exempt from FICA taxes on wages. However, this exemption does not apply if they change to an immigration status that is not exempt or if they become resident aliens.

FICA stands for Federal Insurance Contribution Act. FICA taxes include Social Security and Medicare taxes.

The FICA exemption typically lasts for the first 5 calendar years of physical presence in the United States for international students. After this period, they are generally classified as Resident Aliens for Tax Purposes and become subject to FICA taxes.