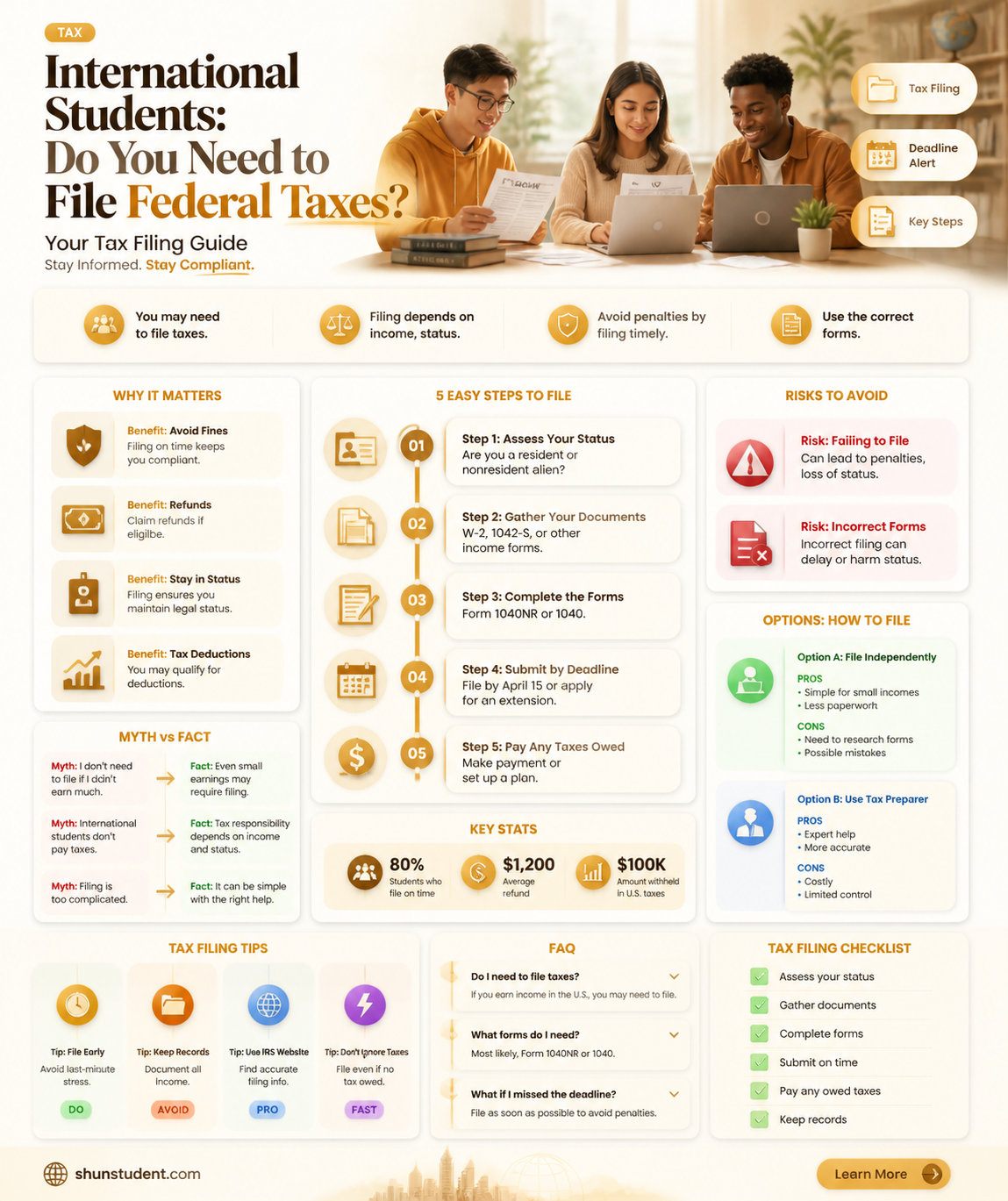

International students in the US are required to file a federal tax return each year they are in the country. This applies to students on F-1, J-1, F-2, and J-2 visas, who are considered nonresident aliens by the IRS and are therefore exempt from paying Social Security and Medicare taxes. However, they must file Form 8843, which is a statement that informs the IRS of how long they have been in the US. Additionally, students with F-1 visas who earn income through OPT (Optional Practical Training) are required to pay federal and state income taxes.

| Characteristics | Values |

|---|---|

| Who must file taxes? | All international students and their spouses and dependents, regardless of income, must complete Form 8843. |

| Who is exempt from paying taxes? | Students in the USA on F-1 visas are NOT required to pay employment taxes (i.e. Social Security and Medicare, also known as FICA). |

| Who is required to pay taxes? | F-1 visa holders pay federal and state income taxes, and J-1 visa holders pay taxes just like U.S. citizens. |

| What if you have no income? | International students who were in the United States for any length of time during 2023 and did not earn income must file the Non-Employed 8843 Form. |

| What if you have income from foreign sources only? | If you have income only from foreign sources, you may not be required to file taxes. |

| What if you have income from interest on a U.S. bank account? | If you have income from interest on a U.S. bank account, you may not be required to file taxes. |

| What if you have a tax-free scholarship? | If you have a tax-free scholarship, you may not be required to file taxes. |

| What if you have income from tax-free investments? | If you have income from certain types of tax-free investments, you may not be required to file taxes. |

| What if you have a taxable scholarship or fellowship? | If you have a taxable scholarship or fellowship, you must file taxes. |

| What if you have income from stock options, lottery or gambling winnings, or other types of non-wage income? | If you have income from any of these sources, you must file taxes. |

| What is the deadline for filing taxes? | The deadline for filing taxes is usually April 15 (or the following Monday if it falls on a weekend). |

| What happens if you don't file taxes? | If you don't file taxes, you may encounter complications when applying for U.S. visas or Green Cards in the future. |

| What is the process for filing taxes? | The process for filing taxes can be complicated, and it is recommended to contact your school's international student center or consult a professional tax advisor for help. |

Explore related products

What You'll Learn

![]()

F-1 visa students: federal and state taxes

International students in the US on an F-1 visa are generally considered nonresident aliens for tax purposes for the first five calendar years of their stay. During this time, they are exempt from paying Social Security and Medicare taxes. After five years, F-1 visa students usually become resident tax filers.

As a nonresident alien, you will need to file Form 1040-NR (federal tax return) to assess your federal income and taxes. Even if you don't earn money during your time in the US, you will still need to file Form 8843 with the IRS by the deadline. If you had no US income and are only filing IRS Form 8843, the deadline is 15 June 2025. The deadline for all F-1 students to file their tax documents is 15 April 2025.

In addition to federal taxes, you may also be required to file a state tax return, depending on the state. Most US states collect state income tax in addition to federal income tax, so international students may have to file a state tax return and pay state income tax even when no federal return is due. Nine states don't have any tax-filing requirements.

If you earn an income from Optional Practical Training (OPT), a program that allows international students to work in the US after graduation, you will be required to pay tax. International students must also fill in a W-4 tax form with their new employer when they start work.

Opening an Australian Bank Account as an International Student

You may want to see also

Explore related products

$32.62 $283.95

$123.99 $283.95

![]()

Exemptions: tax treaties

International students in the US on an F-1 visa are typically considered nonresident aliens for tax purposes for the first five calendar years of their stay. During this time, they may be eligible for tax exemptions under an income tax treaty. The US has income tax treaties with 65 countries, and these treaties can often reduce or eliminate US tax on various types of income, such as pensions, interest, dividends, royalties, and capital gains.

If an international student's country of residence has signed a tax treaty with the US, they may be partially or completely exempt from certain taxes. For example, a tax treaty may provide for a lesser rate of taxation on capital gains. Additionally, a special rule under the US-India Income Tax Treaty allows Indian students and business apprentices to claim the standard deduction if they do not claim itemized deductions.

It is important to note that even if income is not taxable due to a tax treaty, it must still be reported on a US income tax return. This is done by filing Form 1040-NR (federal tax return) to assess federal income and taxes. Additionally, international students must file Form 8843 with the IRS, even if they did not earn any income during their time in the US. This form is due by April 15, 2025, and there may be penalties for missing this deadline, including potential complications for future US visa or Green Card applications.

To accurately determine their federal tax filing status and any applicable exemptions, international students should refer to the IRS website or consult with a tax professional.

International Students: Post-Graduation Stay Options in the US

You may want to see also

Explore related products

![]()

Non-taxable income

International students in the US on F-1 visas are typically considered nonresident aliens for tax purposes. This means that they are only taxed on US-source income.

Nonresident alien students and scholars are not required to file taxes if their income comes only from the following sources:

- US savings and loan institutions

- US credit unions

- US insurance companies

- Investments that generate portfolio interest

- Tax-free scholarships or fellowship grants

Even if nonresident alien students and scholars do not earn money during their time in the US, they are still required to file Form 8843 with the IRS. This form is due by April 15 for the previous tax year. If you had no US income and are only filing Form 8843, the deadline is June 15.

Additionally, F-1 students are exempt from social security and Medicare taxes. However, if they violate their nonimmigrant status and earn self-employment income, this income will be subject to US income tax.

It is important to note that tax requirements may vary depending on the state, as some states do not have any tax-filing requirements, while others may require the filing of a state tax return in addition to a federal return.

International Students: Who Are They?

You may want to see also

Explore related products

![]()

Deadlines

International students in the US are required to file a tax return each year they are in the country. The deadline for filing federal tax returns is April 15 or the following Monday if the 15th falls on a weekend. For the 2024 tax year, this deadline is Monday, April 14, 2025.

The deadline for filing state tax returns varies by state. For example, in Connecticut, the deadline for filing a state tax return is in April of the following year. In Indiana, the state tax forms are available online, but no specific deadline is mentioned.

If you are unable to file your federal income tax return by the deadline, you may be able to get an automatic six-month extension. However, missing the deadline may lead to fines and penalties and could jeopardize your chances of securing a US visa or Green Card in the future.

It is important to note that the deadline for Form 8843 is different if you did not earn any income in the US. In that case, the deadline is June 15, 2025. Form 8843 is a statement required by the US government for certain nonresident aliens who are in the US on F-1, J-1, F-2, or J-2 visas. It is informational and lets the IRS know how long you've been in the country.

Understanding Your Status: Am I an International Student?

You may want to see also

Explore related products

![]()

State taxes

International students in the US on F-1 visas are considered nonresident aliens for tax purposes for the first five calendar years of their stay. However, some can be considered 'residents' or 'resident aliens' for tax purposes if they pass the substantial presence test. As a nonresident alien, you will need to file Form 1040-NR (federal tax return) to assess your federal income and taxes. Even if you don’t earn money during your time in the US, you will still need to file Form 8843 with the IRS by the deadline.

Now, let's focus on state taxes. In addition to federal taxes, most states in the US will collect state income tax. Tax rates and deductions will differ for each state, so the amount you will pay will depend on where you live and study. Because of this, international students may have to file a state tax return and pay state income tax even when no federal return is due.

Nine states don't have any tax-filing requirements. These are:

International Students in the USA: Can They Get Aid?

You may want to see also

Frequently asked questions

Yes, all international students are required to file federal taxes. However, the process varies depending on the type of visa and income.

F-1 visa holders are considered nonresident aliens and are exempt from paying Social Security and Medicare taxes. They need to file Form 1040-NR (federal tax return) and Form 8843 with the IRS. Even if they didn't earn any income, they must submit Form 8843 by the deadline.

International students earning income in the US must file federal and state tax returns. They may need to complete Form 1040NR or 1040NR-EZ, and they are responsible for paying federal and state income taxes. Additionally, they should fill out a W-4 tax form with their employer when starting work.