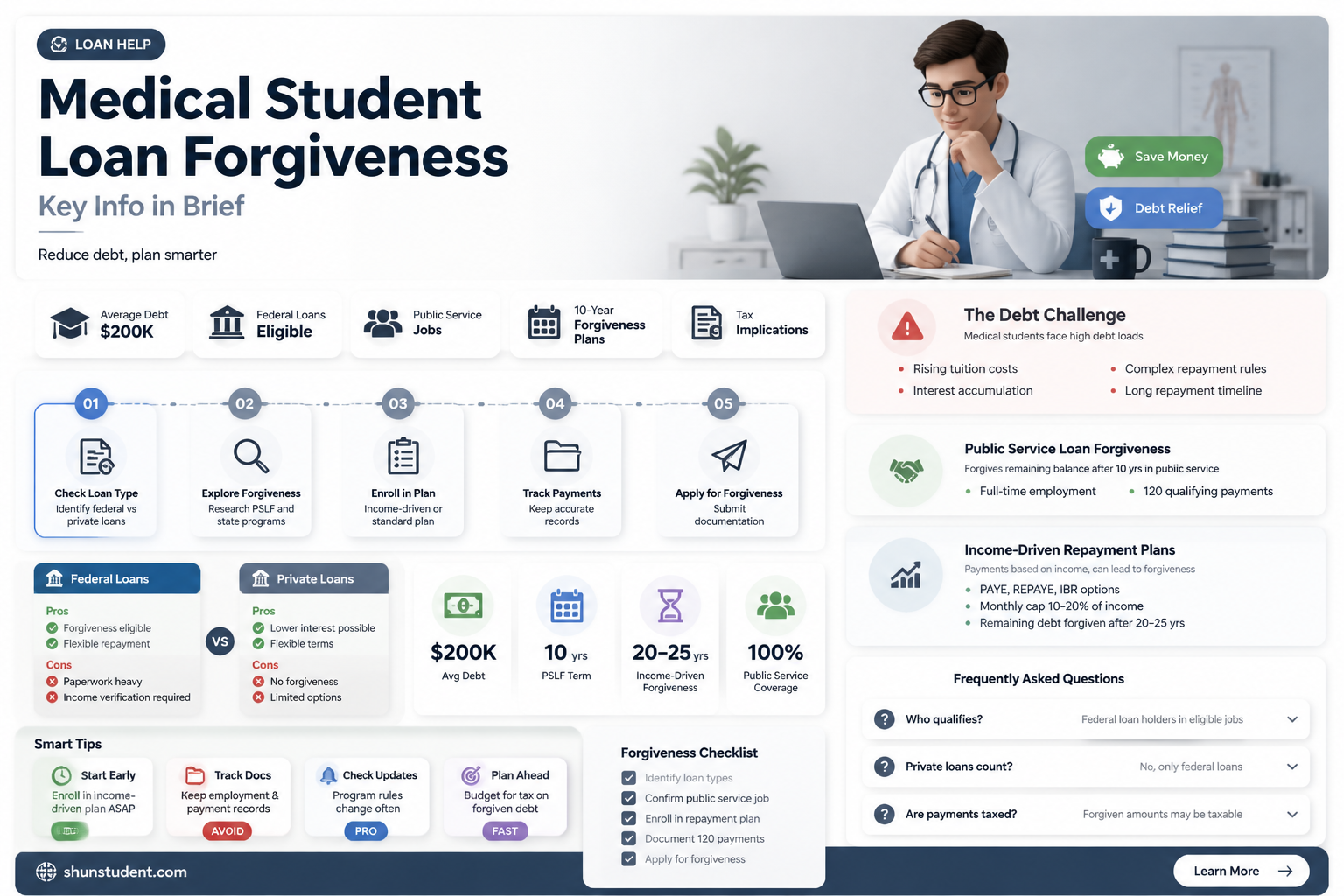

Medical student loans are a significant financial burden for many aspiring healthcare professionals, often totaling hundreds of thousands of dollars by graduation. As a result, the question of whether these loans can be forgiven has become a critical concern for medical students and graduates alike. Loan forgiveness programs, such as the Public Service Loan Forgiveness (PSLF) program and income-driven repayment plans, offer potential avenues for relief, but eligibility requirements and application processes can be complex. Additionally, specialized programs like the National Health Service Corps (NHSC) Loan Repayment Program provide forgiveness in exchange for service in underserved areas. Understanding these options is essential for medical students seeking to manage their debt effectively and pursue their careers without overwhelming financial strain.

| Characteristics | Values |

|---|---|

| Public Service Loan Forgiveness (PSLF) | Forgiveness after 120 qualifying payments (10 years) while working full-time for a qualifying employer (e.g., government, non-profit, 501(c)(3) organizations). |

| Income-Driven Repayment (IDR) Forgiveness | Forgiveness after 20-25 years of payments, depending on the plan (e.g., PAYE, REPAYE, IBR, ICR). Remaining balance is forgiven but may be taxed as income. |

| National Health Service Corps (NHSC) Loan Repayment Program | Up to $50,000 in loan repayment for 2 years of service in a Health Professional Shortage Area (HPSA). |

| State Loan Repayment Programs (SLRP) | Varies by state; offers loan repayment assistance for medical professionals serving in underserved areas. |

| Military Loan Repayment Programs | Up to $40,000 in loan repayment for physicians serving in the military (e.g., Army, Navy, Air Force). |

| Taxability of Forgiven Amounts | PSLF forgiveness is tax-free; IDR forgiveness may be taxed as income unless legislation changes. |

| Eligibility for Federal vs. Private Loans | Forgiveness programs typically apply only to federal student loans (e.g., Direct Loans); private loans are generally not eligible. |

| Residency and Fellowship Considerations | Payments made during residency/fellowship may qualify for PSLF or IDR forgiveness if enrolled in an eligible repayment plan. |

| Recent Legislative Changes | Updates like the Fresh Start Initiative (2023) and IDR Account Adjustment may accelerate forgiveness timelines for some borrowers. |

| Specialty-Specific Programs | Some specialties (e.g., primary care, psychiatry) may have additional loan forgiveness opportunities through NHSC or state programs. |

| Private Loan Forgiveness | Limited options; some employers or states may offer repayment assistance, but no federal forgiveness programs exist. |

Explore related products

$26.87 $29.99

What You'll Learn

![]()

Public Service Loan Forgiveness (PSLF) for medical students

Medical students often graduate with substantial debt, averaging over $200,000 in loans. Public Service Loan Forgiveness (PSLF) offers a lifeline, but it’s not automatic. To qualify, borrowers must make 120 eligible payments while working full-time for a qualifying employer, such as a government or nonprofit organization. For medical students, this often means committing to public health, academic medicine, or underserved communities. The program forgives the remaining balance after meeting these requirements, tax-free. However, navigating PSLF requires meticulous planning and adherence to specific rules, making it both a promising opportunity and a complex process.

Qualifying for PSLF begins with choosing the right repayment plan. Medical students should enroll in an income-driven repayment (IDR) plan, such as PAYE or REPAYE, which caps monthly payments at a percentage of discretionary income. These plans lower monthly costs and ensure eligibility for PSLF. For instance, a resident physician earning $60,000 annually with $250,000 in loans might pay as little as $200–$300 per month under an IDR plan, compared to $2,500 under a standard 10-year plan. This not only makes payments manageable but also maximizes the amount forgiven after 120 payments.

One common pitfall is assuming all public service jobs qualify. Employers must be designated as tax-exempt under Section 501(c)(3) of the Internal Revenue Code or be a government organization. For medical students, this includes hospitals with nonprofit status, community health centers, and academic institutions. Private practice, even in underserved areas, typically does not qualify unless it’s structured as a nonprofit. Borrowers should use the PSLF Help Tool to verify their employer’s eligibility and submit an Employment Certification Form annually to track progress.

PSLF is particularly advantageous for medical students pursuing lower-paying specialties or those committed to public service. For example, a pediatrician working in a rural health clinic or a primary care physician in a federally qualified health center can benefit significantly. However, the program demands long-term commitment. Leaving public service before completing 120 payments means losing eligibility for forgiveness. Borrowers must weigh their career goals against the program’s requirements, ensuring their passion aligns with PSLF’s constraints.

Finally, recent updates to PSLF have made it more accessible. The Limited PSLF Waiver, introduced in 2021, allowed borrowers to receive credit for past payments made under any repayment plan or loan type, provided they worked for a qualifying employer. While this waiver expired in October 2022, its impact remains, as many borrowers saw significant progress toward forgiveness. Moving forward, medical students should stay informed about policy changes and proactively manage their loans to maximize PSLF benefits. With careful planning, PSLF can transform overwhelming debt into a manageable path toward financial freedom.

VA Disability Benefits: Student Loan Deferment Options for 50% Rating

You may want to see also

Explore related products

$9.99 $14.99

$17.83 $14.95

![]()

Income-Driven Repayment (IDR) forgiveness options

Medical students often graduate with substantial debt, and the burden of repaying these loans can be overwhelming. Income-Driven Repayment (IDR) plans offer a lifeline by capping monthly payments at a percentage of discretionary income, typically 10-20%. However, the real game-changer is the potential for loan forgiveness after 20-25 years of consistent payments. This makes IDR plans a strategic choice for medical professionals, especially those pursuing public service or working in lower-paying specialties.

To qualify for IDR forgiveness, borrowers must first enroll in an eligible plan, such as Revised Pay As You Earn (REPAYE), Pay As You Earn (PAYE), Income-Based Repayment (IBR), or Income-Contingent Repayment (ICR). Each plan has unique eligibility criteria and payment caps, so it’s crucial to choose the one that aligns with your financial situation. For instance, REPAYE is ideal for those with high debt relative to income, while IBR may suit borrowers with older loans. Tracking payments meticulously is essential, as forgiveness hinges on meeting the required number of qualifying payments, typically 240-300.

One critical aspect often overlooked is the tax implications of IDR forgiveness. When loans are forgiven, the IRS may consider the forgiven amount as taxable income, potentially resulting in a substantial tax bill. However, under the American Rescue Plan Act of 2021, forgiven student loan balances through 2025 are tax-free. Borrowers should plan ahead for potential changes in tax laws beyond this period and consult a financial advisor to mitigate future liabilities.

For medical professionals in public service, combining IDR with the Public Service Loan Forgiveness (PSLF) program can accelerate debt relief. PSLF offers forgiveness after 120 qualifying payments, significantly shorter than the 20-25 years required for standard IDR forgiveness. To maximize benefits, ensure your employer qualifies as a public service organization and submit employment certification forms regularly. This dual approach can provide a faster path to financial freedom while serving underserved communities.

Finally, staying proactive is key to navigating IDR forgiveness successfully. Regularly recertify your income and family size annually to maintain accurate payment amounts. Monitor policy changes, as federal student loan programs are subject to legislative updates. Tools like the Federal Student Aid website and loan servicer portals can help track progress and ensure compliance. With careful planning and persistence, IDR forgiveness can transform overwhelming debt into a manageable, and ultimately forgivable, financial obligation.

Unlock Student Loan Forgiveness: 10,000 Debt-Free Strategies Revealed

You may want to see also

Explore related products

![]()

National Health Service Corps (NHSC) loan repayment

Medical school graduates often face staggering debt, with average student loans exceeding $200,000. The National Health Service Corps (NHSC) Loan Repayment Program offers a compelling solution, providing substantial financial relief in exchange for service in underserved communities. This program stands out for its clear structure and significant benefits, making it a strategic option for debt-burdened physicians.

To qualify, licensed primary care medical, dental, or mental/behavioral health clinicians must commit to serving at least two years in a Health Professional Shortage Area (HPSA). The NHSC calculates repayment amounts based on the HPSA score and the clinician’s full-time status. For instance, a full-time physician serving in a high-need HPSA could receive up to $50,000 for a two-year commitment, with an additional $25,000 for each subsequent year. Part-time clinicians receive prorated amounts, ensuring flexibility for varying career paths.

One of the program’s strengths lies in its inclusivity. Unlike some loan forgiveness programs, the NHSC accepts both federal and commercial loans, broadening its appeal. However, clinicians must ensure their practice site is NHSC-approved and maintain full licensure throughout their service term. Partial fulfillment of the commitment results in prorated repayment, while failure to complete the term requires repayment of the awarded amount, underscoring the importance of careful planning.

A comparative analysis reveals the NHSC’s advantages over other programs. For example, Public Service Loan Forgiveness (PSLF) requires 10 years of qualifying payments, whereas the NHSC offers faster relief. Additionally, the NHSC’s focus on underserved areas aligns with both career development and societal impact, providing clinicians with valuable experience while addressing critical healthcare disparities.

In conclusion, the NHSC Loan Repayment Program is a strategic, impactful option for medical professionals seeking debt relief. By committing to serve in underserved communities, clinicians can significantly reduce their financial burden while contributing to public health. Prospective applicants should carefully review eligibility criteria, calculate potential benefits, and align their career goals with the program’s mission to maximize this opportunity.

Do Student Loan Forgiveness Programs Call You? Beware of Scams

You may want to see also

Explore related products

![]()

State-specific loan forgiveness programs for doctors

Medical student loan debt often exceeds $200,000, making repayment a significant burden for new physicians. While federal programs like Public Service Loan Forgiveness (PSLF) exist, state-specific loan forgiveness programs offer targeted relief for doctors willing to serve in underserved areas or high-need specialties. These programs vary widely in eligibility, benefits, and obligations, requiring careful consideration to maximize their impact.

California’s Steven M. Thompson Loan Forgiveness Program, for instance, provides up to $105,000 over three years for primary care physicians practicing in federally designated Health Professional Shortage Areas (HPSAs). Applicants must commit to full-time service and demonstrate financial need. In contrast, New York’s Doctors Across New York program offers up to $20,000 annually for up to five years for physicians practicing in underserved communities, with no income restrictions. These examples highlight how state programs tailor incentives to address local healthcare gaps.

Not all programs are created equal, and understanding their nuances is critical. Texas’ Physician Education Loan Repayment Program requires a two-year commitment in a HPSA but caps forgiveness at $60,000 total. Meanwhile, Ohio’s Primary Care Workforce Grant targets family medicine, internal medicine, and pediatrics, offering $25,000 annually for four years. Some states, like Minnesota, prioritize rural areas, while others, like Massachusetts, focus on specialties like psychiatry or obstetrics. Prospective applicants should research their state’s program specifics, including application deadlines, service requirements, and funding availability.

A comparative analysis reveals that state programs often complement federal options like PSLF. For example, a physician in Illinois could combine the Health Professional Loan Repayment Program (up to $50,000 annually) with PSLF for dual benefits. However, state programs typically require shorter service commitments (2–4 years) compared to PSLF’s 10-year requirement. This makes them ideal for early-career physicians seeking immediate relief. Caution is advised, though: some states tax forgiven amounts, and breaking a service contract can result in repayment penalties.

To navigate these programs effectively, doctors should take practical steps. First, identify HPSAs or underserved areas in their state using the Health Resources & Services Administration’s (HRSA) database. Second, compare state program benefits against federal options using tools like the American Medical Association’s Loan Forgiveness Navigator. Third, consult a financial advisor to understand tax implications and long-term financial impacts. By strategically leveraging state-specific programs, physicians can alleviate debt while addressing critical healthcare needs in their communities.

Congressional Children and Student Loan Forgiveness: Fact or Fiction?

You may want to see also

![]()

Military service loan repayment programs for physicians

Physicians burdened by medical school debt have a unique opportunity to alleviate their financial strain through military service loan repayment programs. These programs, offered by all branches of the U.S. military, provide substantial financial incentives in exchange for a commitment to serve as a military physician. The specifics vary by branch, but the core concept remains consistent: a significant portion of your medical school loans can be forgiven in return for a defined period of active duty service.

For example, the Army's Health Professions Scholarship Program (HPSP) offers up to $250,000 in loan repayment for medical students who commit to four years of active duty service. This translates to a potential savings of tens of thousands of dollars in interest alone, making it a compelling option for those seeking both financial relief and a meaningful career path.

Beyond the financial benefits, military service offers physicians a unique professional experience. You'll have the opportunity to practice medicine in diverse settings, from stateside bases to overseas deployments, often with access to cutting-edge medical technology and specialized training. The military also fosters a strong sense of camaraderie and purpose, allowing you to serve your country while honing your medical skills.

However, it's crucial to carefully consider the commitment involved. Military service entails a structured lifestyle, potential deployments to challenging environments, and adherence to military regulations. Thoroughly research the specific requirements and obligations of each program before making a decision.

Ultimately, military service loan repayment programs present a viable pathway for physicians to address their student loan debt while contributing to a greater cause. By weighing the financial incentives against the demands of military service, you can determine if this path aligns with your personal and professional goals. Remember, these programs offer not just debt relief, but a chance to serve your country and gain invaluable experience in a unique medical environment.

Devry Student Loan Forgiveness: What Borrowers Need to Know Now

You may want to see also

Frequently asked questions

No, not all medical student loans are eligible for forgiveness. Eligibility depends on factors such as the type of loan (federal vs. private), repayment plan, and participation in specific forgiveness programs like Public Service Loan Forgiveness (PSLF) or income-driven repayment plans.

PSLF forgives the remaining balance of federal Direct Loans after 120 qualifying payments (10 years) while working full-time for a qualifying employer, such as a government or nonprofit organization. Medical students often qualify through residencies or careers in public service.

Private medical student loans are not eligible for federal forgiveness programs like PSLF. However, some private lenders offer limited forgiveness options, and borrowers may explore state-based loan repayment assistance programs (LRAPs) or employer-based repayment benefits.