Many physician assistants (PAs) burdened by student loan debt often wonder if their loans can be forgiven after 10 years. The answer depends on the type of loans they have and their eligibility for specific forgiveness programs. Federal student loans, such as Direct Loans, may qualify for Public Service Loan Forgiveness (PSLF) after 120 qualifying payments (approximately 10 years) if the borrower works full-time for a qualifying employer, such as a government or non-profit organization. However, not all PAs meet these criteria, and private loans are generally not eligible for forgiveness programs. It’s crucial for PAs to research their loan types, explore repayment plans like income-driven repayment (IDR), and consult with a financial advisor or loan servicer to determine their best path to managing or potentially forgiving their student debt.

Explore related products

What You'll Learn

![]()

Public Service Loan Forgiveness (PSLF) Requirements

Physician assistants burdened by student loan debt often wonder if Public Service Loan Forgiveness (PSLF) can offer relief after 10 years. The answer hinges on meeting specific, stringent requirements. PSLF isn’t automatic; it’s a structured program demanding meticulous planning and adherence to its rules. To qualify, you must make 120 eligible payments while working full-time for a qualifying employer, typically a government or nonprofit organization. This means tracking every payment, employer, and loan type with precision.

First, ensure your loans are federal Direct Loans, as only this type qualifies for PSLF. If you have Federal Family Education Loans (FFEL) or Perkins Loans, consolidate them into a Direct Consolidation Loan to become eligible. Next, verify your employer’s eligibility using the PSLF Help Tool. Hospitals, clinics, and universities often qualify, but private practices rarely do unless they’re nonprofit. Your role as a physician assistant is irrelevant if your employer doesn’t meet PSLF criteria.

Your payment plan also matters. Payments must be made under an income-driven repayment (IDR) plan, such as PAYE, REPAYE, IBR, or ICR, to count toward PSLF. These plans cap monthly payments at a percentage of your discretionary income, making them manageable while working in public service. Standard 10-year repayment plans don’t align with PSLF’s structure, as the goal is forgiveness after 120 payments, not full repayment.

Documentation is your lifeline. Submit the Employment Certification Form (ECF) annually or whenever you change employers to confirm your eligibility. This creates a paper trail, ensuring each payment counts toward the 120 required. Waiting until year 10 to apply can lead to costly surprises if payments were misapplied or employers disqualified. Proactive tracking prevents disqualification due to technicalities.

Finally, beware of pitfalls. Payments made during residency or fellowship may not qualify if your employer wasn’t PSLF-approved. Partial payments, late payments, or those made during periods of deferment or forbearance don’t count. Stay vigilant, review your payment history annually, and consult the Department of Education or a loan specialist if unsure. PSLF offers a path to freedom from debt, but only for those who navigate its requirements with care.

Is Student Loan Forgiveness Real? Unraveling the Truth and Myths

You may want to see also

Explore related products

![]()

Income-Driven Repayment Plan Eligibility

Physician assistants burdened by student loan debt often wonder if income-driven repayment (IDR) plans can pave the way to forgiveness after 10 years. While these plans offer lower monthly payments tied to income and family size, eligibility hinges on a complex interplay of factors. Understanding these criteria is crucial for PAs seeking a manageable repayment path and potential forgiveness.

First, consider your loan type. Only federal Direct Loans qualify for IDR plans. If you have older FFEL or Perkins Loans, consolidation into a Direct Consolidation Loan is necessary. This step, while seemingly bureaucratic, unlocks access to IDR and its forgiveness potential.

Next, assess your income and family size. IDR plans calculate payments based on discretionary income, typically defined as the difference between your adjusted gross income and 150% of the poverty guideline for your family size. For a single PA earning $80,000 annually, discretionary income would be roughly $52,000 (assuming 150% of the poverty guideline is $28,000). This figure directly influences your monthly payment amount.

Larger families benefit from higher poverty guideline thresholds, resulting in lower discretionary income and, consequently, lower monthly payments. For instance, a PA with a spouse and two children earning $100,000 would have a significantly lower discretionary income compared to a single PA earning the same amount.

Finally, choose the IDR plan that best suits your financial situation. Options include Revised Pay As You Earn (REPAYE), Pay As You Earn (PAYE), Income-Based Repayment (IBR), and Income-Contingent Repayment (ICR). Each plan has specific eligibility requirements and payment calculations. REPAYE, for example, caps payments at 10% of discretionary income, while IBR offers a 10% or 15% cap depending on when the loan was first disbursed.

Remember, IDR plans are not a one-size-fits-all solution. Carefully evaluate your income, family size, and loan type to determine eligibility and choose the plan that minimizes your monthly burden while maximizing your chances of loan forgiveness after 20-25 years of consistent payments. Consulting with a qualified student loan advisor can provide personalized guidance tailored to your unique circumstances.

Student Loan Forgiveness After Death: A Guide for Borrowers

You may want to see also

Explore related products

![]()

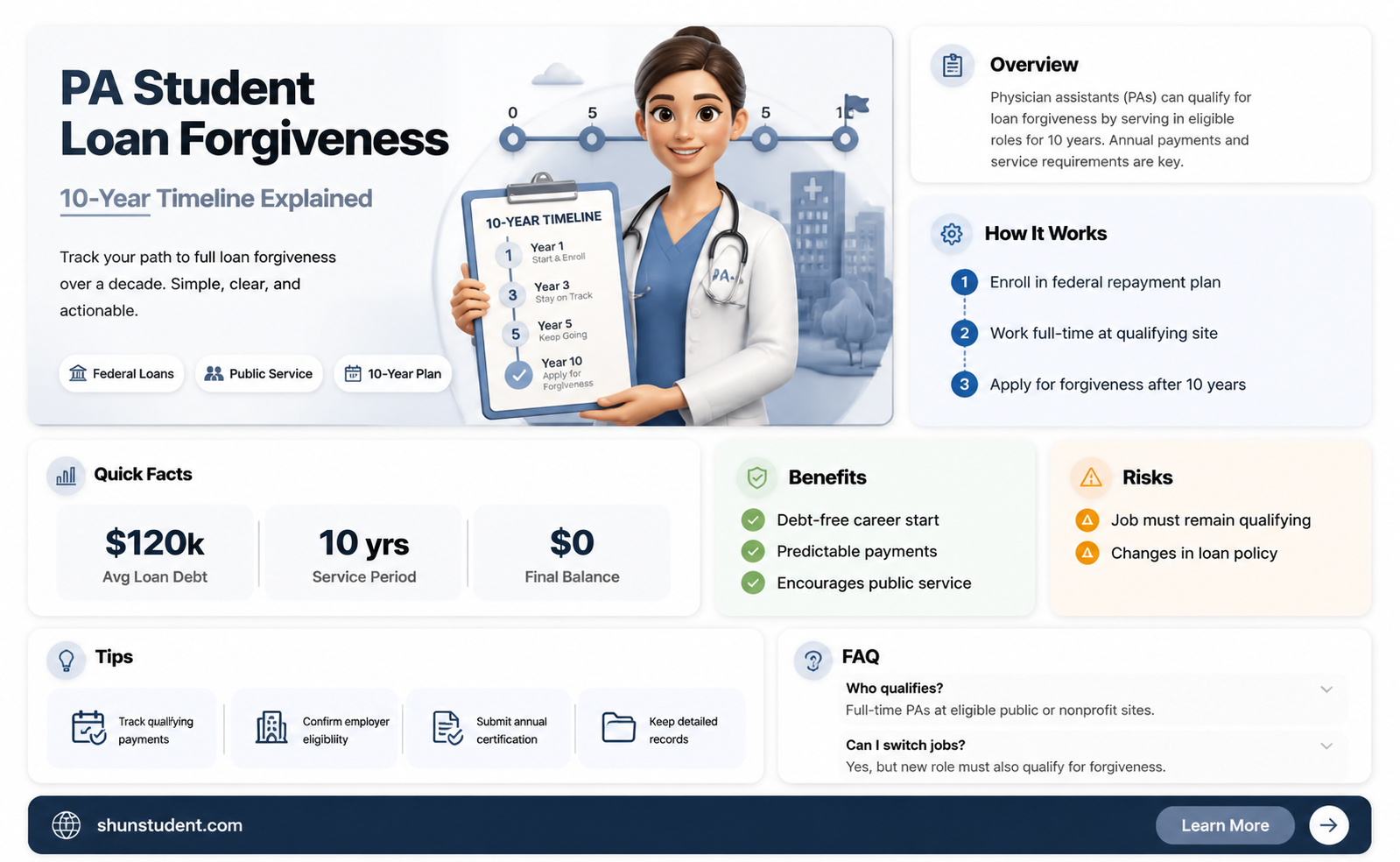

Loan Forgiveness for Physician Assistants

Physician assistants (PAs) often graduate with substantial student loan debt, averaging between $100,000 and $150,000. For many, the prospect of loan forgiveness after 10 years is a lifeline. The Public Service Loan Forgiveness (PSLF) program is the most accessible pathway for PAs, but it requires strategic planning. To qualify, PAs must work full-time for a qualifying employer—such as a government agency, nonprofit hospital, or 501(c)(3) organization—and make 120 eligible payments under an income-driven repayment plan. This means tracking employment certification annually and ensuring each payment counts toward the 10-year goal.

While PSLF is a federal program, state-specific loan forgiveness programs can also benefit PAs, particularly those working in underserved areas. For instance, the National Health Service Corps (NHSC) offers up to $50,000 in loan repayment for two years of service in a Health Professional Shortage Area (HPSA). PAs in primary care roles can leverage this program to significantly reduce their debt burden while serving communities in need. However, these programs often require a commitment to work in high-need specialties or locations, which may not align with every PA’s career goals.

A common misconception is that all PAs qualify for loan forgiveness after 10 years simply by working in healthcare. In reality, eligibility hinges on employment type, repayment plan, and consistent documentation. For example, working in a for-profit hospital or private practice typically disqualifies PAs from PSLF, even if they serve underserved populations. Additionally, switching repayment plans or missing payments can reset the 120-payment counter, delaying forgiveness. PAs must stay vigilant and proactive in managing their loans to avoid pitfalls.

For PAs considering loan forgiveness, the first step is to assess their employment eligibility and consolidate loans into a Direct Loan program, as only these loans qualify for PSLF. Next, enroll in an income-driven repayment plan, such as PAYE or REPAYE, to lower monthly payments and maximize forgiveness potential. Finally, submit an Employment Certification Form annually to ensure each year of service counts toward the 10-year requirement. While the process demands diligence, the reward of debt-free living makes it a worthwhile pursuit for many PAs.

Can Cosigners Benefit from Student Loan Forgiveness Programs?

You may want to see also

Explore related products

![]()

Qualifying Employment for PSLF

Physician assistants (PAs) burdened by student loans often eye the Public Service Loan Forgiveness (PSLF) program as a lifeline. However, qualifying employment is the linchpin of this 10-year forgiveness path. Not all jobs meet the PSLF criteria, and misunderstanding this can lead to years of ineligible payments. The program demands that you work full-time for a qualifying employer—typically a government organization, a 501(c)(3) nonprofit, or certain other nonprofit entities—while making 120 qualifying payments under an income-driven repayment plan.

To determine if your PA role qualifies, scrutinize your employer’s tax status. Hospitals, clinics, and healthcare organizations often fall under the 501(c)(3) umbrella, but not always. For instance, for-profit hospitals or private practices rarely qualify, even if they serve underserved populations. Use the IRS Tax Exempt Organization Search tool to verify your employer’s status. Additionally, if you work for a government agency, such as a VA hospital or a public health department, you’re likely in the clear. However, part-time work or employment with a contractor, even for a qualifying organization, may disqualify you.

Beyond employer eligibility, your job duties matter less than your employer’s status. Whether you’re in primary care, surgery, or emergency medicine, your role as a PA doesn’t inherently disqualify you—it’s the organization’s mission and tax classification that count. However, be cautious of hybrid roles. For example, if you split time between a qualifying nonprofit clinic and a for-profit entity, only hours worked for the nonprofit count toward PSLF. Track your hours meticulously to ensure compliance.

Practical steps to secure PSLF eligibility include submitting the Employment Certification Form (ECF) annually or whenever you change jobs. This form confirms your employer’s eligibility and tracks your qualifying payments. It’s a safeguard against administrative errors and provides a paper trail if disputes arise. Additionally, enroll in an income-driven repayment plan, such as PAYE or REPAYE, to lower monthly payments and ensure they qualify for PSLF. These plans cap payments at 10-15% of your discretionary income, making them manageable while you accrue qualifying payments.

Finally, beware of common pitfalls. Missing a single qualifying payment resets the 120-payment clock, so stay vigilant about deadlines and repayment plan renewals. Consolidating loans can also reset your progress, so time consolidations carefully. By understanding these nuances and taking proactive steps, PAs can navigate the PSLF program effectively, turning a decade of service into a debt-free future.

Is Biden's Student Loan Forgiveness Legal? Analyzing the Debate

You may want to see also

Explore related products

![]()

Tax Implications of Loan Forgiveness

Student loan forgiveness can feel like a financial lifeline, especially for physician assistants burdened by six-figure debt. But before you celebrate, understand this: forgiven debt often comes with a tax bill. The IRS considers forgiven debt as taxable income, meaning you'll owe taxes on the amount wiped away. This can be a nasty surprise if you're unprepared.

Let's break down the tax implications of loan forgiveness programs for physician assistants.

Public Service Loan Forgiveness (PSLF) stands out as a beacon of hope for many PAs. Work full-time for a qualifying employer (like a government agency or non-profit) for 10 years while making 120 qualifying payments, and your remaining federal student loan balance disappears. The good news? PSLF forgiveness is tax-free. This means the forgiven amount isn't considered taxable income, saving you a significant chunk of change.

However, not all forgiveness programs are created equal. Income-Driven Repayment (IDR) plans, while offering lower monthly payments based on your income, often result in forgiveness after 20-25 years. The catch? The forgiven amount is generally taxed as income. Imagine owing $100,000 after 25 years – that's a hefty tax bill unless you plan ahead.

So, how do you prepare for the tax implications of loan forgiveness? First, consult a tax professional. They can help you understand your specific situation and explore strategies to minimize your tax liability. Consider setting aside a portion of your income each year in a dedicated savings account earmarked for potential tax payments. This proactive approach prevents a financial scramble when tax season arrives.

Remember, knowledge is power. Understanding the tax implications of loan forgiveness empowers you to make informed decisions about your student loan repayment strategy. By planning ahead, you can ensure that loan forgiveness truly provides the financial relief you deserve.

Parent Income and Student Loan Forgiveness: What's the Connection?

You may want to see also

Frequently asked questions

No, not all physician assistant student loans are forgiven after 10 years. Only loans under specific repayment plans like Public Service Loan Forgiveness (PSLF) or income-driven repayment plans may qualify for forgiveness after 10–25 years, depending on the plan and eligibility criteria.

Yes, physician assistants can qualify for PSLF if they work full-time for a qualifying employer (e.g., government or nonprofit) and make 120 eligible payments (10 years’ worth) under a qualifying repayment plan.

No, income-driven repayment plans typically forgive remaining loans after 20–25 years, not 10. The 10-year forgiveness timeline specifically applies to PSLF for eligible borrowers.

No, loan forgiveness is not automatic. Borrowers must meet specific requirements, such as enrolling in a qualifying repayment plan, making eligible payments, and applying for forgiveness through the appropriate program (e.g., PSLF).

No, private student loans are not eligible for federal forgiveness programs like PSLF or income-driven repayment plans. Only federal student loans qualify for these forgiveness options.