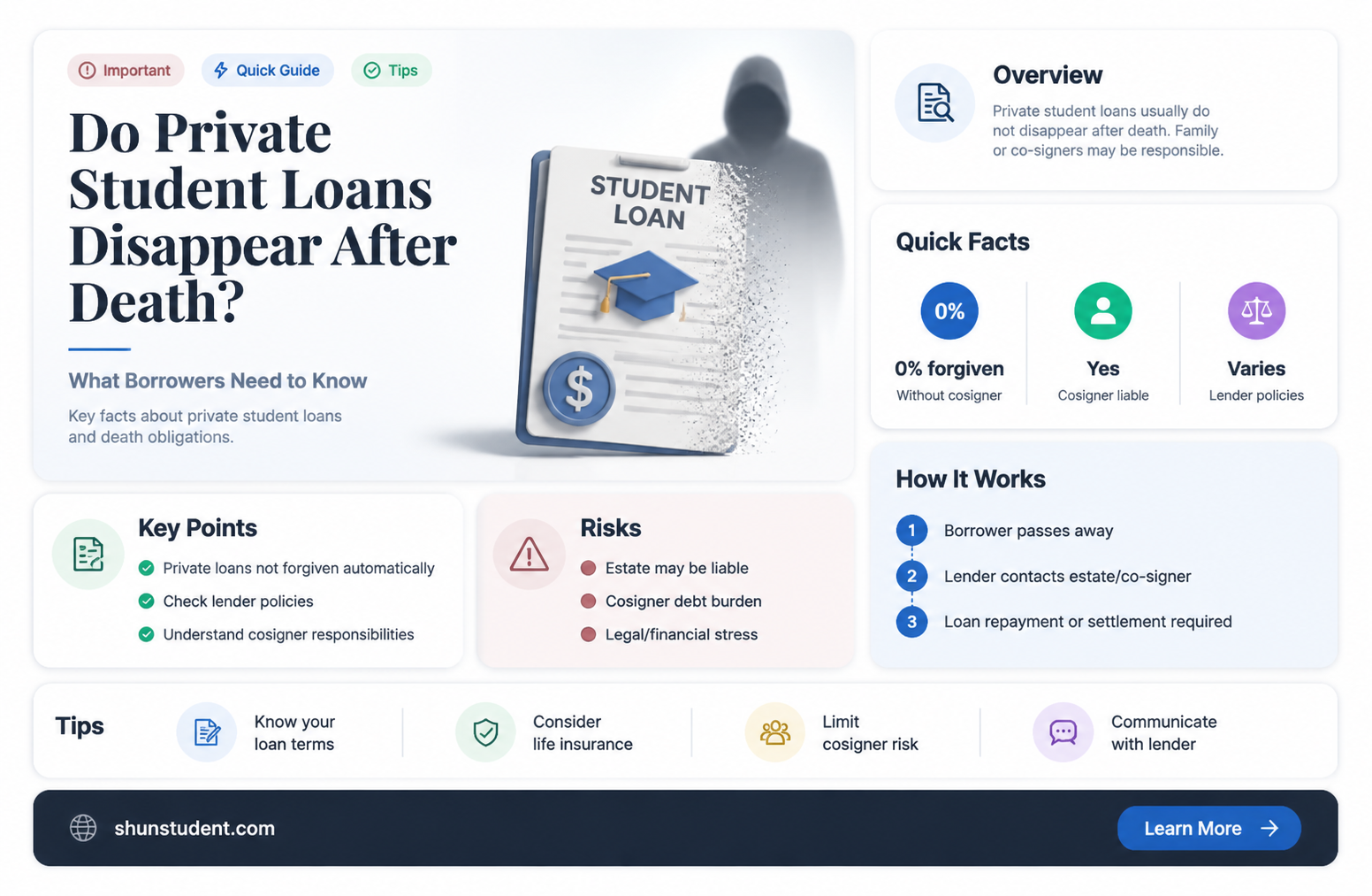

When considering private student loans, one critical question borrowers often ask is whether these loans are forgiven if the borrower dies. Unlike federal student loans, which typically offer loan discharge upon the borrower’s death, private student loans do not automatically qualify for forgiveness. Instead, the outcome depends on the lender’s policies and the terms outlined in the loan agreement. Some private lenders may forgive the debt, while others may require repayment from the borrower’s estate or cosigner, if applicable. It’s essential for borrowers to review their loan contracts carefully and consider options like life insurance to protect their loved ones from potential financial burden in the event of their passing.

| Characteristics | Values |

|---|---|

| Loan Forgiveness Upon Death | Most private student loans are not automatically forgiven upon death. |

| Co-signer Liability | Co-signers may still be responsible for repaying the loan if the borrower dies. |

| Lender Policies | Some lenders may offer death discharge policies, but this is rare. |

| State Laws | Certain states have laws preventing lenders from collecting from the borrower's estate if it has no assets. |

| Estate Responsibility | The borrower's estate may be responsible for repaying the loan, depending on state laws and lender policies. |

| Insurance Options | Some private loans offer optional life insurance to cover the debt in case of death. |

| Federal vs. Private Loans | Federal student loans are automatically discharged upon death, unlike most private loans. |

| Documentation Required | Lenders typically require a death certificate to process any discharge or forgiveness. |

| Impact on Credit | The loan may still affect the borrower's credit posthumously if not resolved. |

| Negotiation Possibility | Family members may negotiate with lenders for forgiveness, but success is not guaranteed. |

Explore related products

$8.99 $19.95

What You'll Learn

- Discharge Policies: Lenders' rules on loan forgiveness upon borrower's death vary widely

- Co-Signer Liability: Co-signers may still be responsible for repayment after death

- Proof Requirements: Death certificate and documentation needed to initiate forgiveness process

- Federal vs. Private: Federal loans forgiven; private loans depend on lender terms

- Estate Impact: Outstanding debt may be collected from borrower's estate if not forgiven

![]()

Discharge Policies: Lenders' rules on loan forgiveness upon borrower's death vary widely

Private student loan discharge policies upon a borrower's death are far from standardized, creating a complex landscape for borrowers and their families to navigate. While federal student loans are automatically discharged in the event of the borrower's death, private lenders operate under their own rules, which can vary dramatically. This lack of uniformity means that the fate of a private student loan after a borrower's passing depends heavily on the specific lender and the terms outlined in the loan agreement.

Understanding the Spectrum of Policies:

At one end of the spectrum, some private lenders offer compassionate discharge policies, forgiving the remaining loan balance upon the borrower's death. This approach provides much-needed relief to grieving families, ensuring they aren't burdened with debt during an already difficult time. For instance, lenders like Discover and Sallie Mae have publicly stated that they discharge private student loans if the borrower passes away.

Example: Discover Student Loans explicitly states on its website, "If the primary borrower dies, we will discharge the loan."

However, not all lenders are as forgiving. Some may require proof of death and extensive documentation, delaying the discharge process and adding stress for the borrower's loved ones. Others might only discharge a portion of the loan, leaving a significant financial burden. In the worst cases, some lenders may even demand repayment from the borrower's estate, potentially forcing the sale of assets to settle the debt.

Caution: Always carefully review the loan agreement's fine print regarding death discharge policies. Look for clauses related to "loan forgiveness upon death" or "death discharge."

Factors Influating Discharge Policies:

Several factors can influence a private lender's discharge policy. These include:

- Loan Type: Some lenders offer different discharge policies for undergraduate and graduate loans, or for loans with co-signers.

- State Laws: Certain states have enacted laws requiring private student loan discharge upon the borrower's death, regardless of the lender's policy.

- Loan Insurance: Some borrowers may have purchased loan insurance that covers the remaining balance in case of death.

Protecting Yourself and Your Loved Ones:

Given the variability in private student loan discharge policies, proactive measures are crucial.

Steps:

- Review Loan Agreements: Carefully examine the terms and conditions of your private student loans, specifically the section regarding death discharge.

- Consider Loan Insurance: If available, purchasing loan insurance can provide peace of mind, ensuring your debt won't burden your loved ones.

- Discuss with Lenders: If you're concerned about your lender's policy, contact them directly to inquire about their specific procedures and any options for loan discharge upon death.

- Seek Legal Advice: Consulting with an attorney specializing in student loan debt can provide valuable guidance and help you understand your rights and options.

The lack of standardized discharge policies for private student loans upon a borrower's death highlights the importance of thorough research and proactive planning. By understanding the varying lender policies, reviewing loan agreements carefully, and exploring protective measures, borrowers can minimize the financial burden on their loved ones during a difficult time. Remember, knowledge and preparation are key to navigating this complex landscape.

Can Chase Bank Forgive Your Student Loans? Exploring Options and Myths

You may want to see also

Explore related products

![]()

Co-Signer Liability: Co-signers may still be responsible for repayment after death

Private student loans often come with a hidden pitfall: co-signer liability that persists even after the borrower’s death. Unlike federal student loans, which typically offer loan discharge upon the borrower’s passing, many private lenders require co-signers to continue repaying the debt. This means that if you co-signed a student loan and the primary borrower dies, you could be legally obligated to settle the remaining balance. This harsh reality underscores the importance of understanding the terms of private loans before committing as a co-signer.

Consider the case of a parent who co-signs a private student loan for their child. If the child passes away unexpectedly, the parent may be blindsided by the lender’s demand for repayment. While some lenders offer death discharge policies, they are not universal, and the absence of such protections can leave co-signers in a financial bind. For instance, lenders like Sallie Mae and Discover have policies that forgive loans upon the borrower’s death, but others, such as Wells Fargo, do not. This inconsistency highlights the need for co-signers to scrutinize loan agreements for clauses related to death discharge.

To mitigate this risk, co-signers should take proactive steps. First, review the loan agreement carefully for language regarding death discharge. If the loan does not include this protection, consider refinancing with a lender that offers it. Second, explore life insurance options for the borrower, ensuring the policy covers the loan amount. This provides a financial safety net for co-signers in the event of the borrower’s death. Finally, if the borrower is in good financial standing, encourage them to remove the co-signer from the loan through a release process, which some lenders allow after a certain number of on-time payments.

The emotional toll of losing a loved one should not be compounded by unexpected financial burdens. Co-signers must be aware of their potential liability and take steps to protect themselves. While private student loans can be a necessary tool for funding education, their terms can be unforgiving. By staying informed and planning ahead, co-signers can minimize the risk of being held responsible for a debt that outlives the borrower. This awareness is not just a financial precaution—it’s a critical safeguard for peace of mind.

Is Nelnet Eligible for Student Loan Forgiveness? Key Details Explained

You may want to see also

Explore related products

![]()

Proof Requirements: Death certificate and documentation needed to initiate forgiveness process

Private student loan forgiveness upon death is not automatic, and the process requires specific documentation to initiate. The cornerstone of this process is the death certificate, a legal document issued by a government authority that declares the borrower’s passing. Without this, lenders have no verifiable proof to begin evaluating forgiveness requests. It’s not just any death certificate; it must be an official, certified copy, often obtained from the county or state vital records office where the death occurred. This document is non-negotiable—no exceptions, no substitutes.

Beyond the death certificate, lenders typically require additional documentation to confirm the borrower’s identity and the relationship of the person initiating the forgiveness request. For instance, the executor of the estate or a surviving family member may need to provide proof of their authority to act, such as letters of administration or a small estate affidavit. Some lenders also request a loan account statement to verify the borrower’s debt and ensure the request pertains to the correct account. These documents collectively establish legitimacy and prevent fraudulent claims, protecting both the lender and the borrower’s estate.

The process can be emotionally taxing for grieving families, so it’s crucial to approach it methodically. Start by contacting the lender directly to inquire about their specific requirements—these can vary widely. For example, some lenders may require a completed forgiveness application form, while others might accept a written request. Keep detailed records of all communications, including dates, names of representatives, and confirmation numbers. This documentation can be invaluable if disputes arise or if the process stalls.

One practical tip is to act promptly. While grief may delay administrative tasks, lenders often have time limits for submitting forgiveness requests. Waiting too long could complicate the process or even result in denial. Additionally, if the borrower had a co-signer, their role becomes critical. Co-signers are typically responsible for the debt unless the lender explicitly forgives it, so they should be involved in gathering and submitting the required documents. Clear communication between all parties ensures a smoother process and reduces the risk of misunderstandings.

In summary, initiating private student loan forgiveness after a borrower’s death hinges on providing the right documentation. The death certificate is the linchpin, but it’s just the beginning. Additional proof of authority, loan verification, and timely action are equally essential. By understanding these requirements and approaching the process systematically, families can navigate this challenging task with greater clarity and efficiency.

Navient Student Loan Forgiveness: Understanding Your Timeline for Debt Relief

You may want to see also

Explore related products

![]()

Federal vs. Private: Federal loans forgiven; private loans depend on lender terms

Federal student loans offer a clear path to forgiveness in the event of the borrower's death, providing a measure of financial relief to grieving families. This automatic discharge applies to Direct Loans, Federal Family Education Loans (FFEL), and Perkins Loans, ensuring that survivors are not burdened with the deceased's educational debt. The process typically requires submission of a death certificate to the loan servicer, after which the debt is canceled without further obligation. This policy reflects a broader federal commitment to protecting borrowers and their families from long-term financial hardship.

Private student loans, however, operate under a vastly different framework, with forgiveness upon death contingent on the lender's specific terms and conditions. Some private lenders, such as SoFi and CommonBond, include death discharge policies in their loan agreements, mirroring federal practices. Others may require proof of death and review the estate's assets before deciding whether to forgive the debt. Borrowers with private loans should carefully review their loan contracts or contact their lenders to understand their policies, as ignorance of these terms can lead to unexpected financial liabilities for cosigners or estates.

For those with private loans lacking death discharge provisions, the debt may fall to cosigners or be collected from the borrower's estate, potentially depleting assets intended for heirs. This underscores the importance of proactive planning, such as purchasing a life insurance policy to cover the loan balance or refinancing with a lender that offers more borrower-friendly terms. Additionally, borrowers can explore adding a cosigner release option if their financial situation improves, reducing the risk to others in the event of their death.

The contrast between federal and private loan forgiveness policies highlights the need for borrowers to make informed decisions when financing their education. Federal loans not only offer death discharge but also provide income-driven repayment plans and public service loan forgiveness, making them a safer choice for many. Private loans, while sometimes necessary for funding gaps, require careful scrutiny of lender policies and long-term financial planning to mitigate risks. Understanding these differences empowers borrowers to protect themselves and their loved ones from unforeseen financial consequences.

Nebraska's Tax Stance on Student Loan Forgiveness: What You Need to Know

You may want to see also

Explore related products

![]()

Estate Impact: Outstanding debt may be collected from borrower's estate if not forgiven

Upon death, private student loans typically aren’t automatically forgiven, unlike some federal loans. This means outstanding debt can linger, casting a shadow over the borrower’s estate. When a borrower passes away, creditors may file claims against the estate to recover unpaid balances. If the estate has sufficient assets—such as property, savings, or investments—these assets could be liquidated to settle the debt. For heirs or beneficiaries, this process can delay inheritance distribution and reduce the estate’s value, leaving less for loved ones.

Consider this scenario: A 30-year-old borrower with a $50,000 private student loan passes away. Their estate, valued at $100,000, includes a house, a car, and cash savings. The lender files a claim for the outstanding loan balance. If the estate’s executor doesn’t dispute the claim, the house might need to be sold, or savings depleted, to pay off the debt. This not only diminishes the estate’s value but also complicates the grieving process for the family.

To mitigate this risk, borrowers can take proactive steps. Purchasing a life insurance policy with a payout sufficient to cover the loan balance can ensure the debt is settled without burdening the estate. Another option is to refinance the loan with a cosigner who agrees to take responsibility in the event of death. Some lenders also offer loan forgiveness policies, though these are rare and often require specific conditions. Reviewing the loan agreement for death discharge clauses is essential, as terms vary widely among private lenders.

Executors of estates must act strategically when faced with private student loan claims. First, verify the debt’s validity by requesting documentation from the lender. If the estate lacks liquidity, negotiate a settlement for less than the full amount, especially if the lender is motivated to recover funds quickly. In some cases, filing a probate action to challenge the claim may be warranted, particularly if the loan terms are ambiguous or unfair. Consulting an estate attorney can provide clarity and protect the estate’s interests.

The estate impact of unpaid private student loans underscores the importance of planning ahead. For borrowers, understanding the potential consequences and taking preventive measures can safeguard their legacy. For executors and heirs, knowing how to navigate creditor claims can minimize financial loss and emotional stress. While private student loans don’t vanish upon death, their burden on an estate can be managed with foresight and informed action.

Does Student Loan Forgiveness Deliver on Its Promises? A Reality Check

You may want to see also

Frequently asked questions

It depends on the lender's policy. Some private lenders may forgive the loan upon the borrower's death, but many do not. It’s essential to review the loan agreement or contact the lender for specific details.

If there is no cosigner, the lender may attempt to collect the debt from the borrower’s estate. If the estate cannot cover the debt, the loan may remain unpaid, but it will not typically transfer to family members unless they cosigned.

Private student loans do not automatically include life insurance. However, some borrowers may choose to purchase life insurance to cover the debt in case of death.

Generally, family members are not responsible for private student loans unless they cosigned the loan. However, the lender may attempt to collect from the borrower’s estate.

There are no federal laws requiring private student loan forgiveness upon death. Forgiveness depends entirely on the lender’s policies and the terms of the loan agreement.