Student loan forgiveness for Certified Clinical Medical Assistants (CCMA) is a topic of growing interest, particularly as healthcare professionals seek financial relief amidst rising educational debt. While there isn’t a specific forgiveness program exclusively for CCMAs, they may qualify for broader initiatives like Public Service Loan Forgiveness (PSLF) if they work for eligible employers, such as government or nonprofit healthcare organizations. Additionally, CCMAs could explore income-driven repayment plans or state-based loan repayment programs designed to assist healthcare workers in underserved areas. Understanding these options requires careful research and consultation with loan servicers to determine eligibility and maximize potential benefits.

| Characteristics | Values |

|---|---|

| Eligibility for Loan Forgiveness | CCMAs (Certified Clinical Medical Assistants) may qualify for student loan forgiveness through programs like Public Service Loan Forgiveness (PSLF) if they work full-time for a qualifying employer (e.g., government, non-profit, or certain healthcare organizations) for 10 years while making eligible payments. |

| Income-Driven Repayment Plans | CCMAs can enroll in income-driven repayment plans (e.g., IBR, PAYE, REPAYE) to lower monthly payments and potentially qualify for loan forgiveness after 20–25 years of payments, depending on the plan. |

| Employer-Based Forgiveness | Some healthcare employers offer student loan repayment assistance programs (LRAPs) for CCMAs, but this is not automatic and depends on the employer. |

| State-Specific Programs | Certain states offer loan repayment assistance programs for healthcare workers, including CCMAs, in underserved areas. Eligibility and benefits vary by state. |

| Federal Loan Requirement | Only federal student loans (e.g., Direct Loans) are eligible for forgiveness programs like PSLF or income-driven plans. Private loans are not eligible. |

| Tax Implications | Loan forgiveness through PSLF is tax-free, but forgiveness through income-driven plans may be taxable as income. |

| Certification Requirements | CCMAs must provide employment certification annually or when applying for PSLF to prove eligibility for forgiveness programs. |

| Partial Forgiveness | No partial forgiveness exists for CCMAs unless enrolled in an income-driven plan and making qualifying payments. |

| Private Loan Options | Private student loans for CCMAs do not qualify for federal forgiveness programs but may be refinanced for better terms. |

| Recent Updates (as of 2023) | No specific CCMAs-targeted forgiveness programs exist, but general federal programs like PSLF and IDR plans remain available. |

Explore related products

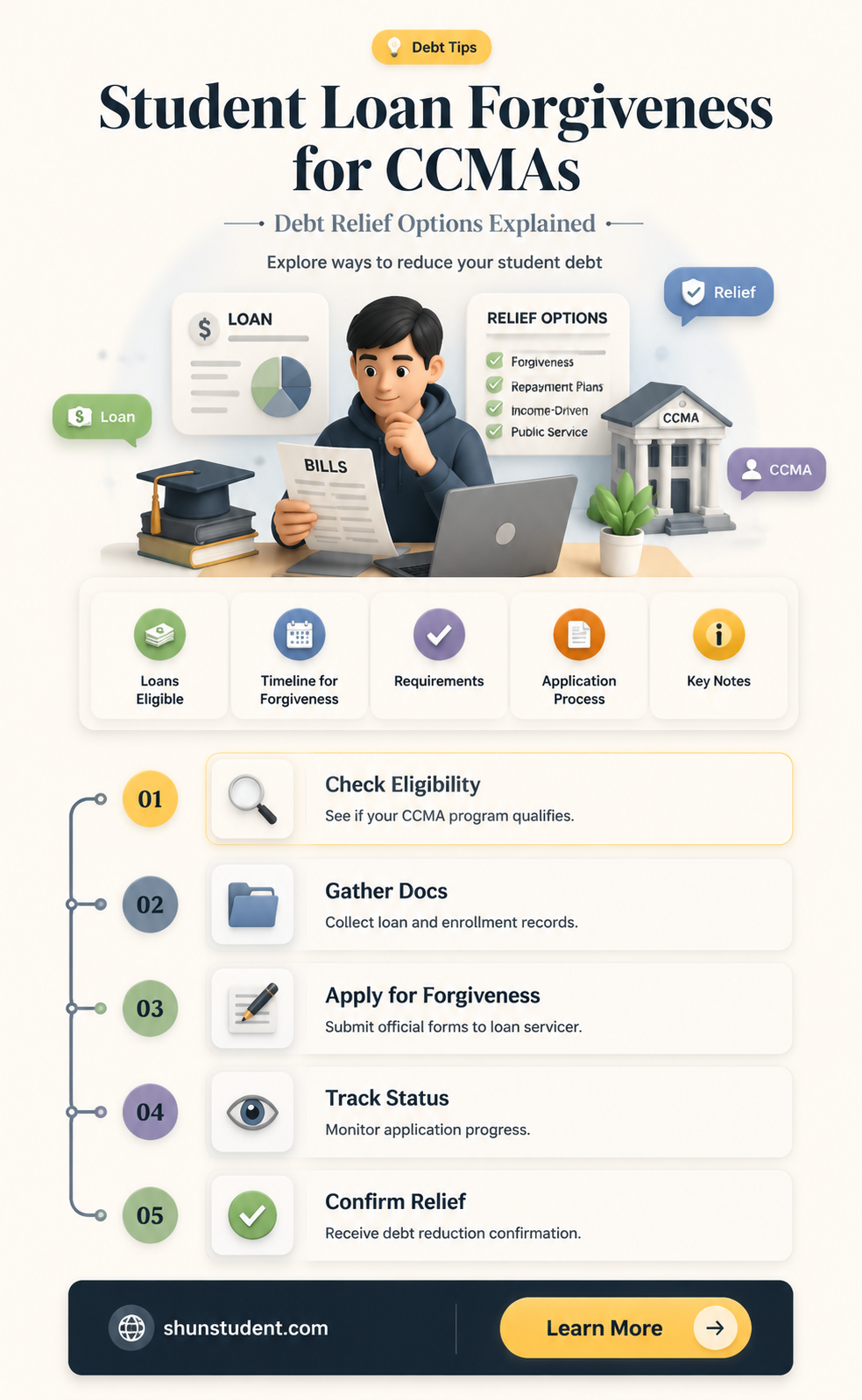

What You'll Learn

- Eligibility Criteria: Specific requirements for CCMAs to qualify for student loan forgiveness programs

- Public Service Loan Forgiveness (PSLF): How CCMAs can benefit from PSLF after 10 years of service

- Income-Driven Repayment Plans: Options for CCMAs to reduce payments and qualify for forgiveness

- Employer-Based Forgiveness: Programs offered by healthcare employers for CCMAs’ student loans

- State-Specific Forgiveness: Forgiveness opportunities for CCMAs in certain states or regions

![]()

Eligibility Criteria: Specific requirements for CCMAs to qualify for student loan forgiveness programs

Certified Clinical Medical Assistants (CCMAs) seeking student loan forgiveness must navigate a complex landscape of eligibility criteria tied to specific programs. The Public Service Loan Forgiveness (PSLF) program, for instance, requires CCMAs to work full-time for a qualifying employer—such as a government agency, 501(c)(3) nonprofit, or certain healthcare providers—and make 120 qualifying payments under an income-driven repayment plan. Full-time is defined as working at least 30 hours per week, a detail often overlooked by applicants. CCMAs in private practice or for-profit healthcare settings are typically ineligible unless their employer meets the nonprofit criteria.

Another pathway is the Income-Driven Repayment (IDR) Forgiveness, which forgives remaining loan balances after 20–25 years of qualifying payments. CCMAs must enroll in an IDR plan like Revised Pay As You Earn (REPAYE) or Income-Based Repayment (IBR), with monthly payments capped at 10–20% of discretionary income. For example, a CCMA earning $40,000 annually with a family size of two might pay as little as $200–$300 monthly under REPAYE. However, this option requires long-term commitment, and forgiven amounts may be taxed as income unless legislation changes.

Employer-based programs offer additional opportunities. Some healthcare employers, particularly in underserved areas, provide loan repayment assistance as part of their benefits package. For instance, the National Health Service Corps (NHSC) offers up to $50,000 in loan repayment for CCMAs committing to two years of service in a Health Professional Shortage Area (HPSA). CCMAs must verify their employer’s eligibility and submit proof of employment annually to maintain eligibility.

A lesser-known option is state-specific forgiveness programs, which vary widely. For example, California’s Bachelor of Science in Nursing Loan Repayment Program includes CCMAs working in critical shortage facilities, offering up to $10,000 annually for four years. Applicants must provide documentation of their CCMA certification, employment verification, and loan statements. Researching state programs through the American Medical Assistants Association (AMAA) or local healthcare boards can uncover hidden opportunities.

Finally, loan forgiveness for CCMAs in military service is an often-overlooked avenue. The Department of Defense’s Health Professions Loan Repayment Program (HPLRP) offers up to $40,000 in loan repayment for a three-year commitment. CCMAs serving in the Army, Navy, or Air Force must provide proof of certification and active duty status. This option combines loan relief with career advancement in military healthcare settings.

In summary, CCMAs must carefully assess their employment status, repayment plans, and available programs to maximize their chances of loan forgiveness. Each pathway has unique requirements, and combining multiple strategies—such as PSLF with employer assistance—can accelerate debt relief. Regularly reviewing eligibility criteria and maintaining meticulous documentation are essential for success.

Social Workers: Unlocking Student Loan Forgiveness Opportunities for Debt Relief

You may want to see also

Explore related products

![]()

Public Service Loan Forgiveness (PSLF): How CCMAs can benefit from PSLF after 10 years of service

Certified Case Managers (CCMs) often carry significant student loan debt, a burden that can hinder financial stability and career satisfaction. However, the Public Service Loan Forgiveness (PSLF) program offers a pathway to relief. By committing to 10 years of qualifying public service employment while making 120 eligible payments, CCMs can have their remaining federal student loan balance forgiven tax-free. This program is particularly advantageous for CCMs working in nonprofit hospitals, government agencies, or other qualifying organizations, as it directly aligns with their career paths.

CCMs seeking to leverage PSLF must first ensure their loans are eligible. Only Federal Direct Loans qualify, so those with Federal Family Education Loans (FFEL) or Perkins Loans must consolidate them into a Direct Consolidation Loan. Next, CCMs should submit the Employment Certification Form (ECF) annually or whenever they change employers to confirm their employment qualifies and their payments are on track. This proactive approach minimizes the risk of disqualification due to administrative errors or changes in employment status.

A critical aspect of PSLF is the requirement to make 120 qualifying payments under an income-driven repayment (IDR) plan. CCMs should enroll in an IDR plan like Revised Pay As You Earn (REPAYE) or Income-Based Repayment (IBR) to lower their monthly payments and ensure they count toward PSLF. These plans cap payments at a percentage of discretionary income, making them more manageable for CCMs, especially those in the early stages of their careers. By strategically combining PSLF with an IDR plan, CCMs can maximize their forgiveness potential while minimizing financial strain.

Despite its benefits, PSLF has a reputation for complexity and administrative challenges. CCMs must remain vigilant to avoid pitfalls such as missing payments, incorrect repayment plan enrollment, or employer disqualification. Regularly reviewing the PSLF Help Tool and consulting with a student loan advisor can provide clarity and peace of mind. Additionally, documenting all payments and employer certifications is essential to building a strong case for forgiveness. With careful planning and persistence, CCMs can turn PSLF into a powerful tool for achieving financial freedom.

Student Loan Forgiveness: How Banks Will Be Repaid Amid Debt Relief

You may want to see also

Explore related products

![NHA CCMA Study Cards 2025-2026: CCMA Exam Prep and Practice Test Questions [Full Color Cards]](https://m.media-amazon.com/images/I/61SwcsZ5qQL._AC_UY218_.jpg)

$40.28 $47.99

![NHA CCMA Study Guide 2025-2026 - 4 Full-Length Practice Tests, CCMA Exam Prep Book Secrets with Step-by-Step Video Tutorials: [3rd Edition]](https://m.media-amazon.com/images/I/71Kia-ICB2L._AC_UY218_.jpg)

![]()

Income-Driven Repayment Plans: Options for CCMAs to reduce payments and qualify for forgiveness

Certified Clinical Medical Assistants (CCMAs) often graduate with significant student loan debt, which can feel overwhelming, especially when starting out in a career with modest entry-level salaries. Income-Driven Repayment (IDR) plans offer a lifeline by capping monthly payments at a percentage of discretionary income, typically 10-20%, and forgiving remaining balances after 20-25 years of qualifying payments. For CCMAs, these plans can transform unmanageable debt into a sustainable financial commitment, aligning loan obligations with their earning potential.

Consider the Revised Pay As You Earn (REPAYE) plan, which limits payments to 10% of discretionary income and offers interest subsidies to prevent balance growth. For a CCMA earning $35,000 annually with $50,000 in loans, monthly payments could drop from $500 under the Standard plan to around $150 under REPAYE. Over time, this not only reduces financial strain but also sets the stage for loan forgiveness after 20 years. However, forgiven amounts may be taxed as income, so planning ahead is crucial.

Another option is the Pay As You Earn (PAYE) plan, which caps payments at 10% of discretionary income and forgives remaining balances after 20 years. To qualify, CCMAs must have taken out federal student loans after October 1, 2007, and demonstrate partial financial hardship. For example, a CCMA with $60,000 in debt and a $40,000 salary could see payments reduced from $600 to $200 monthly, making it easier to manage living expenses while working toward forgiveness.

While IDR plans offer relief, they require annual recertification of income and family size, which can be cumbersome. Missing deadlines may result in higher payments or capitalization of unpaid interest. CCMAs should also be aware that switching jobs or pursuing further education could impact eligibility and payment amounts. Proactive management, such as setting calendar reminders for recertification and exploring employer-based loan assistance programs, can maximize the benefits of these plans.

In conclusion, Income-Driven Repayment plans provide CCMAs with a strategic path to reduce monthly payments and qualify for loan forgiveness. By selecting the right plan, staying organized, and planning for potential tax implications, CCMAs can navigate their student debt with confidence, freeing up resources to invest in their careers and personal growth.

Unveiling the Lawmakers Who Opposed Student Loan Forgiveness: A Deep Dive

You may want to see also

Explore related products

![Medical Assistant Study Cards 2025-2026: All-in-One Prep for CMA, RMA, and CCMA Exams [Full Color Cards]](https://m.media-amazon.com/images/I/71arOdnzNeL._AC_UY218_.jpg)

![]()

Employer-Based Forgiveness: Programs offered by healthcare employers for CCMAs’ student loans

Certified Clinical Medical Assistants (CCMAs) often graduate with significant student loan debt, a burden that can hinder their financial stability and career advancement. However, a growing number of healthcare employers are stepping in to alleviate this pressure through employer-based forgiveness programs. These initiatives not only attract and retain skilled CCMAs but also foster loyalty and long-term commitment to the organization. By offering structured repayment assistance, employers are addressing a critical pain point for CCMAs while investing in their workforce’s future.

One prominent example of such programs is the loan repayment assistance program (LRAP), where employers agree to contribute a fixed amount toward an employee’s student loans over a specified period. For instance, a hospital might offer $2,000 annually for up to five years, totaling $10,000 in loan forgiveness. These programs often require CCMAs to commit to a minimum employment term, typically 2–3 years, ensuring stability for both parties. Some employers even tie repayment amounts to performance metrics, incentivizing employees to excel in their roles while receiving financial relief.

Another innovative approach is the tuition reimbursement model, where employers cover a portion of a CCMA’s education costs in exchange for continued service. While not strictly loan forgiveness, this strategy reduces the need for CCMAs to take out large loans in the first place. For example, a clinic might reimburse 50% of tuition costs for employees who complete their CCMA certification, provided they remain employed for at least two years post-graduation. This proactive approach not only eases financial strain but also encourages professional development within the organization.

When considering employer-based forgiveness programs, CCMAs should carefully review the terms and conditions. Some programs require employees to work in underserved areas or high-need specialties, such as geriatrics or urgent care. Others may have strict eligibility criteria, including minimum credit hours or GPA requirements. Prospective CCMAs should also inquire about tax implications, as some forgiveness benefits may be considered taxable income. Practical tips include negotiating loan repayment as part of a job offer and researching employers known for robust benefits packages, such as large hospital systems or federally qualified health centers (FQHCs).

In conclusion, employer-based forgiveness programs represent a win-win solution for CCMAs and healthcare organizations alike. By offering financial relief, employers not only attract top talent but also cultivate a motivated and stable workforce. For CCMAs, these programs provide a pathway to reduce debt while advancing their careers. As the demand for CCMAs continues to rise, such initiatives will likely become a standard component of competitive employment packages in the healthcare industry.

Harris County Employment: Student Loan Forgiveness Eligibility Explained

You may want to see also

Explore related products

![]()

State-Specific Forgiveness: Forgiveness opportunities for CCMAs in certain states or regions

Certified Clinical Medical Assistants (CCMAs) seeking student loan forgiveness may find that state-specific programs offer targeted relief, often tied to regional healthcare needs. For instance, New York’s Clinical Supervision Loan Forgiveness Program provides up to $20,000 in forgiveness for CCMAs working in underserved areas, with eligibility contingent on two years of full-time employment. Similarly, California’s CalHealthCares Loan Repayment Program offers up to $50,000 for CCMAs serving in federally designated Health Professional Shortage Areas (HPSAs). These programs underscore how states incentivize CCMAs to address local healthcare disparities, making geographic flexibility a strategic asset for loan forgiveness.

To maximize state-specific opportunities, CCMAs should first identify regions with critical healthcare shortages, as these areas often host the most generous programs. For example, Texas’ Rural Practitioner Tax Exemption forgives up to $10,000 annually for CCMAs working in rural counties, while Minnesota’s Rural Physician Loan Forgiveness Program extends benefits to allied health professionals, including CCMAs, with awards up to $30,000. A practical tip: use the Health Resources and Services Administration’s (HRSA) Finder Tool to locate HPSAs and corresponding state programs. Aligning employment with these areas not only accelerates forgiveness but also enhances career fulfillment by contributing to community health.

However, CCMAs must navigate program nuances to avoid pitfalls. Some states, like Florida, require a minimum commitment of three years for loan forgiveness, while others, such as Ohio, mandate participation in state-run healthcare initiatives. Additionally, income thresholds and repayment structures vary; for instance, Illinois’ Rural Health Loan Repayment Program caps annual forgiveness at $25,000 but excludes CCMAs earning above $100,000. A comparative analysis reveals that while state programs offer substantial relief, they demand careful planning and long-term commitment, making them best suited for CCMAs with clear career trajectories in underserved regions.

Persuasively, state-specific forgiveness programs not only alleviate financial burdens but also foster professional growth. CCMAs working in underserved areas gain hands-on experience, build diverse skill sets, and establish strong community ties. For example, Georgia’s Rural Hospital Tax Credit provides up to $40,000 in loan forgiveness for CCMAs in rural hospitals, while simultaneously offering mentorship and leadership opportunities. By leveraging these programs, CCMAs can transform student debt into a stepping stone for career advancement, proving that strategic geographic placement yields both financial and professional dividends.

Navigating Student Loan Forgiveness: How to Obtain Your Application Form

You may want to see also

Frequently asked questions

There is no specific student loan forgiveness program exclusively for CCMAs. However, CCMAs may qualify for general loan forgiveness programs like Public Service Loan Forgiveness (PSLF) if they work in eligible public service roles.

Yes, CCMAs can qualify for PSLF if they work full-time for a qualifying employer, such as a government or non-profit organization, and make 120 eligible payments under an income-driven repayment plan.

CCMAs working in healthcare may be eligible for programs like the Nurse Corps Loan Repayment Program or state-based loan repayment programs, depending on their employer and location.

Yes, CCMAs can enroll in income-driven repayment plans, which may forgive remaining loan balances after 20–25 years of qualifying payments, depending on the plan.