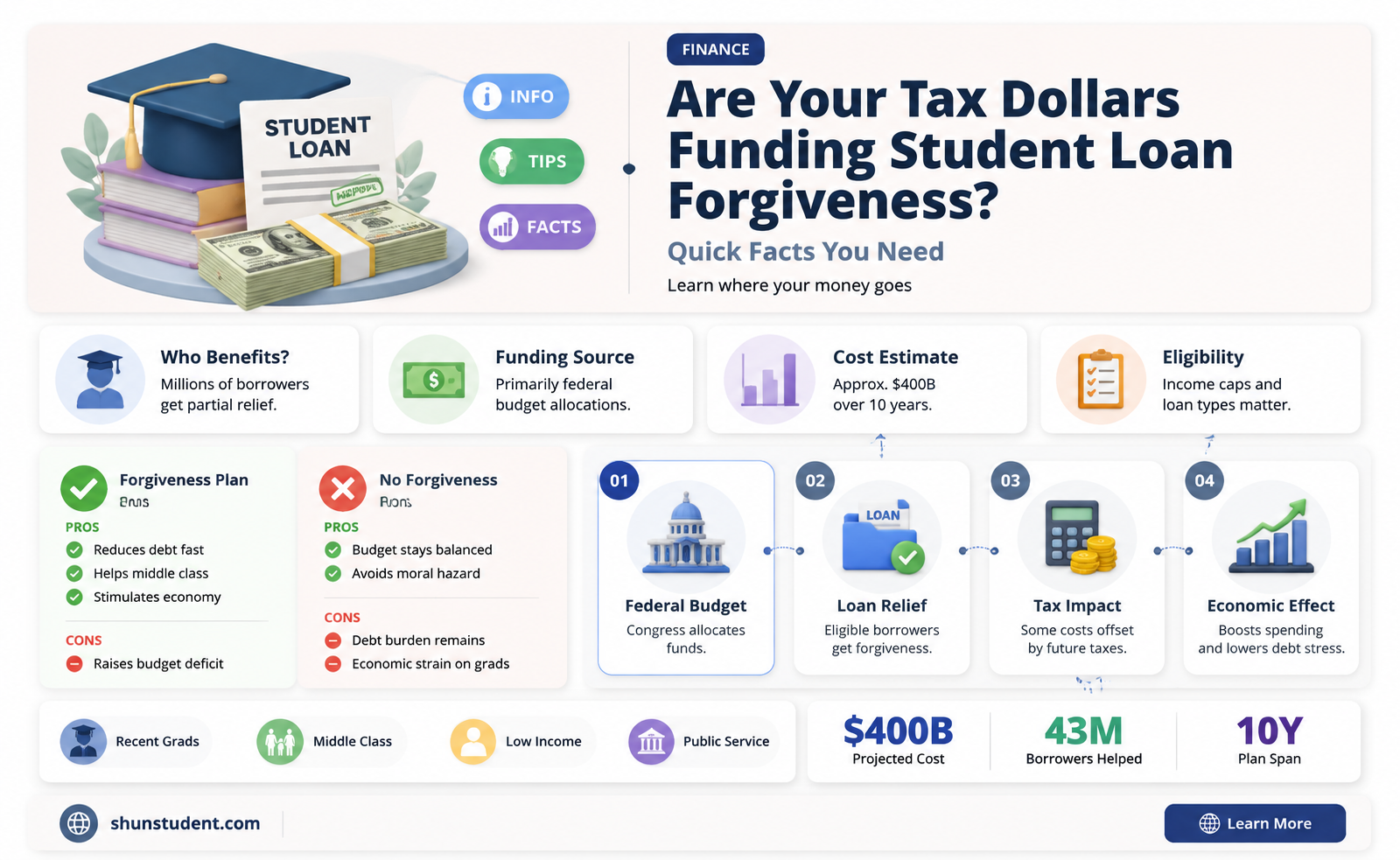

The topic of whether tax dollars are used for student loan forgiveness has sparked significant debate and discussion in recent years, as the burden of student debt continues to weigh heavily on millions of Americans. As the federal government explores various initiatives to alleviate this financial strain, questions arise regarding the source of funding for such programs. Proponents argue that utilizing tax dollars for student loan forgiveness can stimulate economic growth and provide much-needed relief to borrowers, while opponents raise concerns about the fairness and long-term implications of redistributing taxpayer funds in this manner. Understanding the relationship between tax dollars and student loan forgiveness is crucial for evaluating the feasibility and potential consequences of these policies, as well as for informing public discourse on this pressing issue.

| Characteristics | Values |

|---|---|

| Funding Source | Taxpayer dollars are used to fund student loan forgiveness programs, primarily through the federal budget. |

| Programs | Examples include Public Service Loan Forgiveness (PSLF), Income-Driven Repayment (IDR) forgiveness, and limited-time initiatives like the Biden administration's targeted forgiveness plans. |

| Eligibility | Eligibility varies by program; PSLF requires 10 years of qualifying payments and public service employment, while IDR forgiveness applies after 20-25 years of payments based on income. |

| Cost to Taxpayers | The cost varies; for instance, the Biden administration's 2022 forgiveness plan was estimated at $400 billion over 30 years, funded by taxpayers. |

| Controversy | Critics argue it unfairly burdens taxpayers, while supporters claim it addresses the student debt crisis and stimulates the economy. |

| Legal Challenges | Forgiveness programs have faced lawsuits, with some arguing they exceed executive authority or violate the Appropriations Clause of the Constitution. |

| Economic Impact | Forgiveness can boost disposable income, reduce defaults, and stimulate consumer spending, but long-term effects on federal spending are debated. |

| Political Divide | Student loan forgiveness is a partisan issue, with Democrats generally supporting it and Republicans often opposing it as fiscally irresponsible. |

| Recent Developments | As of 2023, the Supreme Court struck down Biden's broad forgiveness plan, limiting the use of taxpayer funds for such initiatives without congressional approval. |

Explore related products

What You'll Learn

![]()

Federal Budget Allocation for Loan Forgiveness

The federal budget is a complex tapestry of allocations, and student loan forgiveness has become a prominent thread in recent years. While the idea of forgiving student debt may seem like a direct use of tax dollars, the reality is more nuanced. The federal government has implemented various loan forgiveness programs, each with its own funding mechanisms and eligibility criteria. For instance, the Public Service Loan Forgiveness (PSLF) program, established in 2007, promises debt relief to borrowers who work in qualifying public service jobs and make 120 eligible payments. This program is funded through the Department of Education's budget, which is, in turn, financed by taxpayer dollars. However, it's essential to note that not all loan forgiveness initiatives are directly funded by the federal budget.

One illustrative example is the income-driven repayment (IDR) plans, which cap monthly payments based on a borrower's income and family size. After 20-25 years of qualifying payments, any remaining balance is forgiven. While these plans are administered by the federal government, the forgiven amounts are typically treated as taxable income, effectively shifting the financial burden from the government to the borrower. This approach raises questions about the true cost of loan forgiveness and its impact on the federal budget. To put this into perspective, consider that the average student loan debt for a 2020 graduate was $28,650. If a borrower enrolls in an IDR plan and has $20,000 forgiven after 20 years, they may face a substantial tax bill, potentially offsetting the perceived benefit of forgiveness.

A comparative analysis of federal budget allocation for loan forgiveness reveals a tension between direct and indirect funding models. Direct funding, as seen in the PSLF program, provides immediate relief to borrowers but requires significant upfront investment from the government. In contrast, indirect funding, such as the taxable forgiveness under IDR plans, defers the financial burden to a later date. Policymakers must carefully weigh these options, considering factors like program effectiveness, budgetary constraints, and the potential long-term consequences of each approach. For instance, a 2019 Government Accountability Office report found that the PSLF program had a lower-than-expected uptake, partly due to complex eligibility requirements. Simplifying these requirements could increase participation but would also require additional funding.

To navigate the complexities of federal budget allocation for loan forgiveness, it’s instructive to examine the role of legislative action. The CARES Act of 2020, for example, temporarily paused student loan payments and interest accrual, providing indirect relief to borrowers without directly forgiving debt. This measure, extended multiple times, highlights the government's ability to respond to crises through creative budgetary adjustments. Similarly, the proposed expansion of PSLF or the introduction of broad-based forgiveness plans would require explicit congressional approval and funding. Advocates for such measures argue that the economic benefits of reducing student debt, such as increased consumer spending and homeownership, justify the investment. Critics, however, caution about the potential for moral hazard and the regressive nature of forgiving debt for higher-income earners.

In practical terms, understanding federal budget allocation for loan forgiveness requires a focus on transparency and accountability. Borrowers should stay informed about existing programs and proposed changes, as these can significantly impact their financial planning. For example, using online tools like the Department of Education's Loan Simulator can help borrowers estimate their eligibility for forgiveness under different plans. Additionally, tracking legislative developments, such as the Biden administration's proposals for targeted debt cancellation, can provide insights into future budget priorities. Ultimately, while tax dollars do play a role in funding loan forgiveness, the specifics of how and when they are used vary widely, reflecting the intricate balance between fiscal responsibility and social equity.

Student Loan Forgiveness for Social Service Workers: A Path to Relief

You may want to see also

Explore related products

![]()

Impact on National Debt and Deficit

The debate over using tax dollars for student loan forgiveness often centers on its impact on the national debt and deficit. Proponents argue that canceling student debt stimulates the economy by freeing up disposable income, potentially increasing tax revenue over time. However, critics counter that such a policy immediately adds to the national debt, which stood at $31.46 trillion as of 2023, exacerbating long-term fiscal challenges. This tension highlights the need for a nuanced understanding of how loan forgiveness interacts with federal finances.

Consider the Biden administration’s 2022 proposal to forgive up to $20,000 in student debt per borrower, estimated to cost $400 billion over a decade. While this figure pales in comparison to the $7.2 trillion added to the national debt during the COVID-19 pandemic, it still represents a significant fiscal commitment. The Congressional Budget Office (CBO) projects that such spending would increase the deficit in the short term, as the government forgoes loan repayments without an immediate offsetting revenue source. For context, the federal deficit was $1.4 trillion in 2022, and adding hundreds of billions in debt forgiveness could delay efforts to stabilize this figure.

To mitigate these effects, policymakers could pair forgiveness with reforms to higher education funding, such as capping interest rates on future loans or increasing accountability for institutions with low graduation rates. For instance, if the government reduced the subsidy rate on federal student loans from 10.6% to 5%, it could save $10 billion annually, partially offsetting forgiveness costs. Additionally, targeting relief to low-income borrowers—who are more likely to default—could maximize economic benefits while minimizing fiscal strain. A 2021 study by the Roosevelt Institute found that canceling $50,000 in debt for borrowers earning under $100,000 annually would boost GDP by $86 billion to $108 billion per year, illustrating the potential for strategic forgiveness to yield returns.

Critics, however, warn that without structural changes, loan forgiveness could set a precedent for recurring bailouts, further straining the national debt. For example, if future administrations continue to cancel debt without addressing root causes like rising tuition costs, the CBO estimates that federal student loan holdings could double by 2051. This scenario underscores the importance of coupling forgiveness with measures to curb college costs, such as increasing Pell Grants or incentivizing states to reinvest in public higher education. By addressing both symptoms and causes, policymakers can balance relief with fiscal responsibility.

Ultimately, the impact of student loan forgiveness on the national debt and deficit depends on its design and accompanying reforms. While immediate costs are undeniable, strategic implementation could yield long-term economic benefits that partially offset fiscal burdens. For taxpayers and borrowers alike, the key lies in crafting a policy that prioritizes equity, sustainability, and accountability—ensuring that relief today does not become a liability tomorrow.

Does Student Loan Forgiveness Cover Principal or Interest?

You may want to see also

Explore related products

![]()

Eligibility Criteria for Tax-Funded Relief

Tax-funded student loan relief programs often hinge on stringent eligibility criteria to ensure funds are allocated fairly and efficiently. These criteria typically include income thresholds, loan type, and repayment status. For instance, the Public Service Loan Forgiveness (PSLF) program requires borrowers to work full-time in qualifying public service jobs and make 120 eligible payments. Similarly, income-driven repayment (IDR) plans cap monthly payments at a percentage of discretionary income, with remaining balances forgiven after 20–25 years. Understanding these requirements is crucial for borrowers seeking relief.

Analyzing the rationale behind eligibility criteria reveals a balance between fiscal responsibility and social equity. Income-based thresholds ensure that relief targets those most in need, while loan type restrictions (e.g., federal loans only) streamline administrative processes. For example, the recent one-time student debt relief plan proposed by the Biden administration limited eligibility to individuals earning under $125,000 annually (or $250,000 for married couples). Such criteria aim to prevent misuse of tax dollars while addressing systemic financial burdens.

A comparative look at international models highlights varying approaches to tax-funded relief. In countries like Germany, eligibility often ties to academic performance or field of study, whereas Canada’s Repayment Assistance Plan adjusts payments based on family size and income. These examples underscore the importance of tailoring criteria to national priorities. Borrowers should research their country’s specific guidelines to maximize eligibility and avoid pitfalls like missing deadlines or incomplete applications.

Persuasively, advocates argue that expanding eligibility criteria could stimulate economic growth by freeing borrowers from debt traps. Critics, however, caution against moral hazard and unsustainable fiscal strain. A middle ground might involve tiered relief, where partial forgiveness is granted based on income and repayment history. For instance, a borrower earning $50,000 annually might receive 50% forgiveness, while someone earning $30,000 could qualify for full relief. Such a model would balance compassion with accountability.

Practically, borrowers should take proactive steps to meet eligibility criteria. This includes consolidating private loans into federal programs, enrolling in IDR plans, and maintaining accurate employment records for programs like PSLF. Tools like the Federal Student Aid website offer calculators to estimate payments and forgiveness timelines. Additionally, staying informed about policy changes—such as temporary waivers for PSLF requirements—can unlock unexpected opportunities. By strategically navigating these criteria, borrowers can maximize their chances of securing tax-funded relief.

Unlock Student Loan Forgiveness: Low-Income Relief Guide

You may want to see also

Explore related products

![I Literally Want My Tax Dollars to Support | Bumper Sticker or Car Magnet | Protect Our Parks Funny Magnetic Bumper for Refrigerators Doors Trucks Cars [7.5x3.75]](https://m.media-amazon.com/images/I/71XFZdragNL._AC_UY218_.jpg)

![]()

Economic Benefits vs. Costs of Forgiveness

Student loan forgiveness programs, particularly those funded by tax dollars, spark intense debate over their economic implications. Proponents argue that forgiveness stimulates the economy by freeing up disposable income for borrowers, who are more likely to spend on goods, services, and investments like homes. For instance, a borrower relieved of $30,000 in debt might redirect $300 monthly payments toward consumer spending or savings, potentially boosting GDP by an estimated 0.1% to 0.3% annually, according to some economic models. This increased spending can create a ripple effect, generating jobs and tax revenue that partially offset the initial cost of forgiveness.

However, the economic benefits of forgiveness are not guaranteed and depend heavily on borrower behavior and broader economic conditions. Critics point out that not all forgiven debt translates into immediate spending; some borrowers may prioritize savings or debt repayment in other areas, muting the stimulative effect. Additionally, the long-term costs of forgiveness—often estimated in the hundreds of billions—could lead to higher taxes or reduced government spending in other critical areas like infrastructure or healthcare. This trade-off raises questions about the efficiency of using tax dollars for forgiveness versus investing in education affordability or workforce development programs.

A comparative analysis reveals that targeted forgiveness programs may yield better economic outcomes than broad-based relief. For example, forgiving loans for borrowers in low-income brackets or public service roles could maximize stimulative effects, as these individuals are more likely to spend additional income. In contrast, forgiving debt for high-earning professionals might have minimal economic impact, as they are less likely to change spending habits. Policymakers must weigh these nuances to design programs that balance costs and benefits effectively.

From a practical standpoint, implementing forgiveness requires careful consideration of funding mechanisms and potential unintended consequences. One approach is to phase in forgiveness gradually, allowing for real-time assessment of economic impacts and adjustments as needed. Another strategy is to pair forgiveness with reforms that address the root causes of student debt, such as capping interest rates or expanding income-driven repayment plans. By combining relief with systemic changes, policymakers can mitigate costs while fostering long-term economic stability.

Ultimately, the economic debate over student loan forgiveness hinges on a cost-benefit analysis that accounts for both immediate and long-term effects. While forgiveness has the potential to stimulate growth and improve financial well-being for millions, it is not a panacea. Success depends on thoughtful design, targeted implementation, and a commitment to addressing the underlying issues driving student debt. As tax dollars are finite, the challenge lies in maximizing their impact to benefit both borrowers and the broader economy.

Liberty Student Loan Forgiveness Scam: Uncovering the Truth Behind the Scheme

You may want to see also

Explore related products

![]()

Public Opinion on Using Tax Dollars for Relief

Public opinion on using tax dollars for student loan relief is deeply divided, reflecting broader ideological and generational tensions. Surveys consistently show that younger Americans, particularly those aged 18 to 34, overwhelmingly support such measures, with over 70% favoring forgiveness programs. This group often cites the crippling burden of student debt as a barrier to financial stability, homeownership, and family planning. In contrast, older generations, especially those over 55, are more skeptical, with only about 40% expressing approval. Their resistance often stems from concerns about fairness—why should taxpayers fund relief for individuals who voluntarily took on debt?—and worries about the program’s long-term economic impact.

To bridge this divide, policymakers must address the root causes of public skepticism. One effective strategy is to frame student loan relief not as a handout but as an investment in economic growth. For instance, studies suggest that debt forgiveness could stimulate consumer spending by freeing up billions of dollars annually, potentially boosting industries like housing and retail. Additionally, targeted relief programs—such as income-driven repayment plans or forgiveness for public service workers—can mitigate perceptions of unfairness by tying benefits to specific contributions or needs. Communicating these nuances is critical to shifting public opinion.

A comparative analysis of global approaches offers valuable insights. Countries like Germany and Norway, which provide tuition-free or heavily subsidized higher education, rarely face debates about loan forgiveness because the issue is largely moot. In the U.S., however, where student debt exceeds $1.7 trillion, the problem demands immediate attention. Borrowing elements from these systems—such as increasing public funding for colleges to reduce reliance on loans—could alleviate the need for large-scale forgiveness programs in the future. This approach, while requiring significant upfront investment, could reduce long-term costs and public resentment.

Practical steps for individuals navigating this debate include staying informed about proposed policies and their potential implications. For example, understanding the difference between broad forgiveness and means-tested relief can help voters advocate for solutions that align with their values. Advocacy groups and grassroots movements also play a crucial role in shaping public discourse. By amplifying personal stories of debt-burdened individuals, they humanize the issue and challenge stereotypes of borrowers as irresponsible. Ultimately, fostering a more nuanced conversation—one that acknowledges both the challenges of student debt and the complexities of funding relief—is key to building consensus.

Is OSLA Part of the Student Loan Forgiveness Program?

You may want to see also

Frequently asked questions

Yes, tax dollars are used to fund federal student loan forgiveness programs, such as Public Service Loan Forgiveness (PSLF) and income-driven repayment (IDR) forgiveness, as these programs are part of the federal budget.

Student loan forgiveness itself does not directly increase individual taxes, but the cost of forgiveness programs is part of the federal budget, which is funded by taxpayers collectively.

In some cases, forgiven student loans are treated as taxable income, depending on the program and circumstances. However, certain programs, like PSLF, are tax-free under current law.

State tax dollars do not directly fund federal student loan forgiveness programs, as these are primarily funded by the federal government. However, states may have their own loan forgiveness programs funded by state taxes.