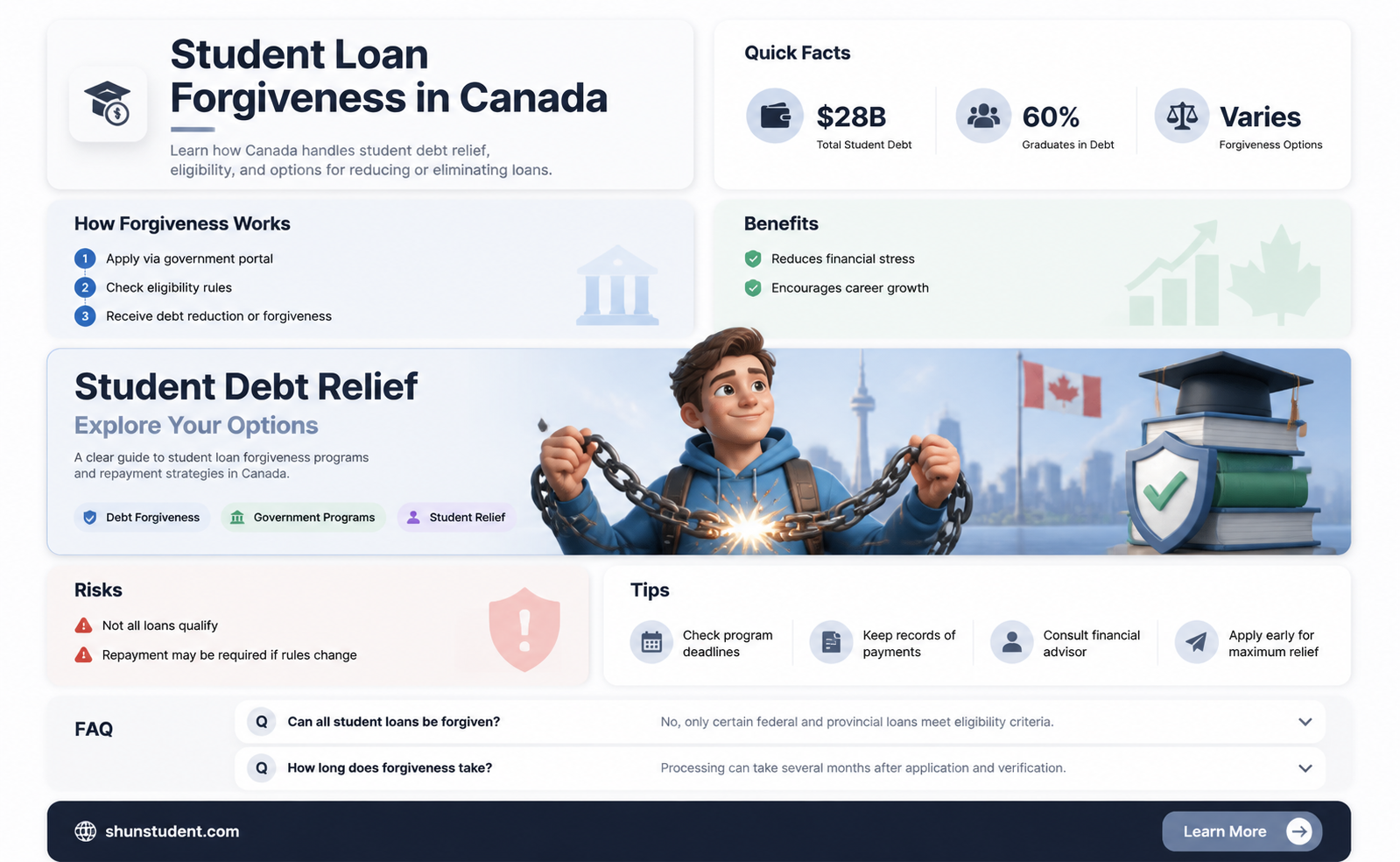

In Canada, student loan forgiveness programs exist to alleviate the financial burden on eligible borrowers, particularly those in specific professions or facing significant economic hardship. The primary initiatives include the Canada Student Loan Forgiveness Program for Family Doctors, Nurses, and Nurse Practitioners, which offers forgiveness of up to $8,000 annually for a maximum of five years for those working in underserved rural or remote communities. Additionally, the Canada Student Loan Forgiveness for Borrowers with Permanent Disabilities provides full loan forgiveness for individuals facing permanent disabilities. While these programs offer targeted relief, widespread or automatic forgiveness for all student loans is not available in Canada. Borrowers struggling with repayment can explore options like the Repayment Assistance Plan (RAP), which adjusts payments based on income and family size, but does not eliminate debt entirely. Understanding these programs is crucial for Canadian students and graduates seeking financial relief from their student loans.

| Characteristics | Values |

|---|---|

| Federal Student Loan Forgiveness | Canada offers the Canada Student Loan Forgiveness Program for family doctors, nurses, and other eligible professionals working in underserved areas. Up to $8,000 per year for family doctors and $4,000 per year for nurses/nurse practitioners, up to a maximum of $40,000 and $20,000, respectively. |

| Provincial Loan Forgiveness | Some provinces (e.g., Ontario, Saskatchewan) offer loan forgiveness programs for specific professions like healthcare workers, teachers, or veterinarians working in rural/remote areas. |

| Repayment Assistance Plan (RAP) | Not loan forgiveness but provides financial assistance to reduce or eliminate monthly payments based on income and family size. Available for federal and some provincial loans. |

| Disability Forgiveness | Permanent disability discharge is available for Canada Student Loans and Canada Apprentice Loans. Requires medical certification. |

| Death of Borrower | Canada Student Loans and Canada Apprentice Loans are discharged upon the borrower's death. |

| Bankruptcy Discharge | Student loans are not automatically discharged through bankruptcy. Must wait 7 years after ceasing studies (or 5 years with undue hardship proof). |

| Loan Cancellation for Default | No forgiveness for default; instead, collection agencies pursue repayment, and credit scores are negatively impacted. |

| Public Service Loan Forgiveness | No federal program similar to the U.S. PSLF. Provincial programs may offer limited forgiveness for public service roles. |

| Maximum Forgiveness Amount | Varies by program (e.g., $40,000 for family doctors, $20,000 for nurses under federal program). |

| Eligibility Criteria | Depends on profession, location of work, income, and loan type (federal/provincial). |

| Application Process | Requires submission of proof (e.g., employment contracts, income verification, medical certification). |

| Tax Implications | Loan forgiveness may be considered taxable income in some cases (consult a tax professional). |

| Private Student Loans | No forgiveness programs; terms depend on lender agreements. |

Explore related products

$8.99 $19.95

$8.34 $17.99

What You'll Learn

- Federal Loan Forgiveness Programs: Details on Canada’s federal student loan forgiveness initiatives for eligible borrowers

- Provincial Forgiveness Options: Provincial-specific programs offering student loan forgiveness in Canada

- Repayment Assistance Plan (RAP): How RAP helps reduce or eliminate student loan payments based on income

- Loan Forgiveness for Professionals: Forgiveness programs for doctors, nurses, teachers, and other professionals in Canada

- Bankruptcy and Student Loans: Conditions under which student loans can be discharged through bankruptcy in Canada

![]()

Federal Loan Forgiveness Programs: Details on Canada’s federal student loan forgiveness initiatives for eligible borrowers

Canada’s federal government offers several loan forgiveness programs designed to alleviate the financial burden on eligible student loan borrowers. One of the most prominent initiatives is the Canada Student Loan Forgiveness for Family Doctors and Nurses, which targets healthcare professionals working in underserved rural or remote communities. Under this program, family doctors can receive up to $8,000 per year for a maximum of five years, totaling $40,000 in loan forgiveness. Nurses, including nurse practitioners, are eligible for up to $4,000 annually for a maximum of five years, totaling $20,000. To qualify, borrowers must commit to working full-time in designated communities for a specified period, ensuring access to healthcare in areas where it’s most needed.

Another key program is the Canada Student Loan Forgiveness for Borrowers with Permanent Disabilities. This initiative provides full loan forgiveness for eligible borrowers who have a permanent disability and are experiencing financial hardship. Applicants must meet specific criteria, including having a significant permanent disability as defined by the Canada Student Financial Assistance Program (CSFAP) and demonstrating ongoing financial need. The program aims to remove financial barriers for individuals facing long-term challenges, allowing them to focus on their well-being and career development without the burden of student debt.

For those pursuing careers in public service, the Public Service Loan Forgiveness Program offers partial relief after a decade of qualifying payments. Borrowers must work full-time for a federal, provincial, territorial, or Indigenous government, or a qualifying non-profit organization, while making consistent payments under the National Student Loan Service Centre’s repayment assistance plan. After 120 qualifying monthly payments (10 years), the remaining balance of the federal portion of the loan is forgiven. This program incentivizes public service careers while providing a pathway to financial freedom for dedicated professionals.

It’s crucial for borrowers to understand the eligibility criteria and application processes for these programs. For instance, the Repayment Assistance Plan (RAP) is not a forgiveness program but a complementary initiative that can reduce monthly payments based on income and family size. Borrowers enrolled in RAP may eventually qualify for loan forgiveness if they continue to meet eligibility requirements for a specified period, typically 10 years for those with permanent disabilities or 15 years for others. Practical tips include keeping detailed records of employment and payments, staying informed about program updates, and consulting with financial aid advisors to maximize benefits.

In summary, Canada’s federal loan forgiveness programs are tailored to support borrowers in specific professions and circumstances, from healthcare workers in remote areas to individuals with permanent disabilities and public service employees. By understanding the nuances of each program and taking proactive steps to meet eligibility requirements, borrowers can significantly reduce or eliminate their student debt, paving the way for greater financial stability and career fulfillment.

Healthcare Heroes: Your Guide to Student Loan Forgiveness Applications

You may want to see also

Explore related products

![]()

Provincial Forgiveness Options: Provincial-specific programs offering student loan forgiveness in Canada

In Canada, provincial governments play a pivotal role in offering student loan forgiveness programs tailored to local needs and economies. These initiatives are designed to alleviate financial burdens for graduates who commit to specific careers or regions, fostering economic growth and addressing workforce shortages. Unlike federal programs, provincial options often target niche areas, such as healthcare, education, or rural development, making them a critical resource for eligible borrowers. Understanding these programs requires a closer look at their eligibility criteria, application processes, and long-term benefits.

Take Ontario’s Ontario Student Loan Forgiveness for Doctors and Nurses as an example. This program forgives up to $8,000 annually for physicians and nurse practitioners working in underserved communities, with a maximum of $40,000 over five years. To qualify, applicants must commit to full-time practice in designated areas, such as northern or rural regions, where healthcare access is limited. The program not only reduces debt but also strengthens local healthcare systems. Applicants must submit proof of employment and residency, with approvals processed annually. This targeted approach highlights how provinces align forgiveness with regional priorities.

In contrast, Newfoundland and Labrador’s Public Service Forgiveness Program takes a broader approach, offering up to $12,000 in loan forgiveness for graduates working in the public sector. Eligible roles include teaching, social work, and government administration, with a focus on retaining talent within the province. Participants must commit to at least two years of full-time employment and submit annual progress reports. While less specialized than Ontario’s program, it underscores the province’s commitment to public service and economic stability. Such programs demonstrate how provinces adapt forgiveness to their unique demographic and economic challenges.

For those in Saskatchewan, the Graduate Retention Program provides a tax credit of up to $20,000 over seven years for graduates who remain in the province post-graduation. Unlike direct loan forgiveness, this program reduces taxable income, effectively lowering the financial burden on graduates. Eligibility requires continuous residency and filing annual tax returns. This incentive-based model encourages long-term settlement, addressing population decline in rural areas. While not a direct loan forgiveness program, it offers significant financial relief and aligns with Saskatchewan’s broader economic goals.

When navigating provincial forgiveness options, borrowers should prioritize research and planning. Each program has distinct eligibility requirements, application deadlines, and documentation needs. For instance, British Columbia’s BC Loan Forgiveness for Family Doctors requires a minimum five-year commitment, while Manitoba’s Manitoba Graduate Skills Tax Rebate focuses on recent graduates in high-demand fields. Prospective applicants should consult provincial websites, track deadlines, and maintain detailed records of employment and residency. By leveraging these programs strategically, graduates can reduce debt while contributing to their communities, creating a win-win scenario for both individuals and provinces.

Can Student Loan Forgiveness Be Blocked? Legal Hurdles Explained

You may want to see also

Explore related products

![]()

Repayment Assistance Plan (RAP): How RAP helps reduce or eliminate student loan payments based on income

In Canada, the Repayment Assistance Plan (RAP) is a lifeline for graduates struggling to manage their student loan payments. This program is not about forgiving loans outright but rather adjusting payments to align with the borrower’s income, ensuring that repayment remains manageable. RAP is particularly crucial for recent graduates entering the workforce with entry-level salaries or those facing unemployment, as it prevents default and financial strain. By recalculating monthly payments based on income and family size, RAP offers a practical solution to the challenge of student debt.

To qualify for RAP, borrowers must demonstrate financial need by submitting an application and providing proof of income. The program is available to both federal and provincial loan holders, though the specifics may vary by province. Once approved, payments are reduced to a level proportional to the borrower’s income. For example, if a graduate earns below the threshold set by the program, their monthly payment could drop to zero temporarily. This income-driven approach ensures that repayment doesn’t become a burden, especially during the early years of a career.

One of the most compelling aspects of RAP is its flexibility. The program reassesses eligibility every six months, adjusting payments as income changes. This dynamic model means that as a borrower’s earnings increase, so do their payments—but only to a degree that remains affordable. For instance, a graduate earning $30,000 annually might pay $100 monthly, while someone earning $50,000 could pay $300. This scalability ensures that the program remains fair and sustainable for both borrowers and lenders.

While RAP doesn’t forgive student loans entirely, it effectively eliminates payments for those with very low incomes. After a certain period—typically 15 years for those outside of Quebec and 10 years in Quebec—any remaining balance is forgiven if the borrower has consistently qualified for RAP. This feature acts as a safety net, preventing lifelong debt for those who face prolonged financial hardship. However, it’s important to note that forgiven amounts may be considered taxable income, so borrowers should plan accordingly.

Practical tips for maximizing RAP benefits include keeping income records up-to-date, applying promptly if financial difficulties arise, and exploring additional provincial assistance programs. Borrowers should also avoid missing payments, as this can disqualify them from the program. By leveraging RAP effectively, graduates can focus on building their careers without the looming stress of unmanageable student debt. This program underscores Canada’s commitment to making education accessible and its aftermath bearable.

Congress Children's Student Loan Forgiveness: Fact or Fiction?

You may want to see also

Explore related products

![]()

Loan Forgiveness for Professionals: Forgiveness programs for doctors, nurses, teachers, and other professionals in Canada

Canada recognizes the critical role that professionals like doctors, nurses, and teachers play in society, and it offers targeted loan forgiveness programs to alleviate their financial burden while encouraging service in underserved areas. For instance, the Canada Student Loan Forgiveness for Family Doctors program forgives up to $8,000 per year for a maximum of five years for physicians who work in underserved rural or remote communities. This program not only reduces debt but also addresses healthcare disparities by incentivizing doctors to practice where they’re needed most. Similarly, the Nursing Student Loan Forgiveness Program in Ontario offers up to $8,000 in forgiveness for nurses working in designated high-need areas, such as long-term care facilities or public health units. These programs are designed to be mutually beneficial: professionals gain financial relief, and communities gain access to essential services.

Teachers, too, have access to loan forgiveness programs, particularly in provinces with acute staffing shortages. For example, the British Columbia Teacher Loan Forgiveness Program provides up to $4,000 per year for a maximum of five years for teachers working in specified rural or remote schools. Eligibility often requires a commitment of at least three years, ensuring stability in these regions. It’s important to note that these programs typically require applicants to have Canada Student Loans, not provincial or private loans, and the forgiveness amounts are considered taxable income. Prospective applicants should carefully review the terms and conditions, as some programs require annual reapplication and proof of employment in eligible areas.

While these programs offer significant benefits, they are not without limitations. For instance, the Canada Student Loan Forgiveness for Family Doctors program excludes specialists, focusing solely on family physicians. Nurses must often work full-time in eligible positions to qualify, which may not align with everyone’s career goals. Teachers may find that eligible schools are limited to specific geographic areas, requiring relocation. Additionally, the forgiveness amounts, though substantial, may not fully cover the total debt of professionals with high loan balances. To maximize these opportunities, professionals should research provincial and territorial programs, as many offer additional incentives beyond federal initiatives.

A comparative analysis reveals that while these programs share a common goal, their structures differ significantly. For example, the federal program for family doctors is more generous in terms of maximum forgiveness ($40,000 over five years) compared to the nursing program in Ontario ($8,000 total). Teachers’ programs often prioritize geographic location over profession type, whereas healthcare programs may distinguish between roles (e.g., doctors vs. nurses). This diversity underscores the importance of aligning career choices with available programs. For instance, a nurse considering loan forgiveness might opt for a position in long-term care in Ontario, while a teacher might prioritize rural postings in British Columbia.

In conclusion, loan forgiveness programs for professionals in Canada are a strategic tool to address workforce shortages while providing financial relief. By understanding the specifics of each program—eligibility criteria, forgiveness amounts, and commitment requirements—professionals can make informed decisions that benefit both their careers and the communities they serve. Practical tips include starting the application process early, maintaining detailed employment records, and exploring complementary provincial programs. While these initiatives won’t erase all student debt, they represent a meaningful step toward financial stability for those dedicated to serving in high-need areas.

Can Student Loan Forgiveness Face Legal Challenges in Court?

You may want to see also

Explore related products

![]()

Bankruptcy and Student Loans: Conditions under which student loans can be discharged through bankruptcy in Canada

In Canada, discharging student loans through bankruptcy is not automatic and is subject to specific conditions outlined in the Bankruptcy and Insolvency Act. Unlike other unsecured debts, student loans are treated differently, reflecting their unique policy considerations. To qualify for discharge, the borrower must have ceased studies for a minimum period: seven years for federal student loans and five years for provincial loans in most cases. This waiting period underscores the government’s intent to balance financial relief with accountability.

The process begins with filing for bankruptcy, but the seven- or five-year rule is not the only hurdle. Borrowers may face a legal challenge known as an "opposition to discharge" from the loan provider. If the court sides with the lender, the debt remains. However, borrowers can apply for an earlier discharge by demonstrating financial hardship. This involves proving that repaying the loan would cause undue financial difficulty, a standard assessed through a separate court application. Success in this application requires thorough documentation of income, expenses, and attempts to repay the debt.

A lesser-known alternative to bankruptcy is a *consumer proposal*, a negotiated settlement with creditors facilitated by a Licensed Insolvent Trustee. While student loans are included, the same time restrictions apply. For instance, if a borrower ceased studies six years ago, a consumer proposal would not discharge the loan, but it could address other debts, providing partial relief. This option is particularly useful for those with mixed debt portfolios but does not bypass the waiting period for student loans.

Practical tips for navigating this process include maintaining detailed financial records and consulting a trustee early. Borrowers should also explore provincial repayment assistance programs before considering bankruptcy, as these may offer immediate relief without long-term credit consequences. For those nearing the seven- or five-year mark, timing the bankruptcy filing strategically can maximize the chances of discharge. Ultimately, while bankruptcy can discharge student loans, it is a complex and conditional process requiring careful planning and professional guidance.

PhD Loan Forgiveness: Strategies to Erase Your Student Debt

You may want to see also

Frequently asked questions

Canada does not have a blanket student loan forgiveness program, but certain programs like the Canada Student Loan Forgiveness Program for Family Doctors, Nurses, and Nurse Practitioners and the Repayment Assistance Plan (RAP) can help reduce or eliminate debt under specific conditions.

Eligibility varies by program. For example, the Canada Student Loan Forgiveness Program is for healthcare professionals working in underserved areas, while RAP is available to borrowers with low income or high debt levels. Permanent disability or death of the borrower may also lead to loan forgiveness.

Student loans are not automatically forgiven after a set period. However, if you consistently qualify for RAP and make no payments due to low income, your loan may be discharged after 15 years (for loans issued before August 1, 2016) or 10 years (for loans issued after that date).