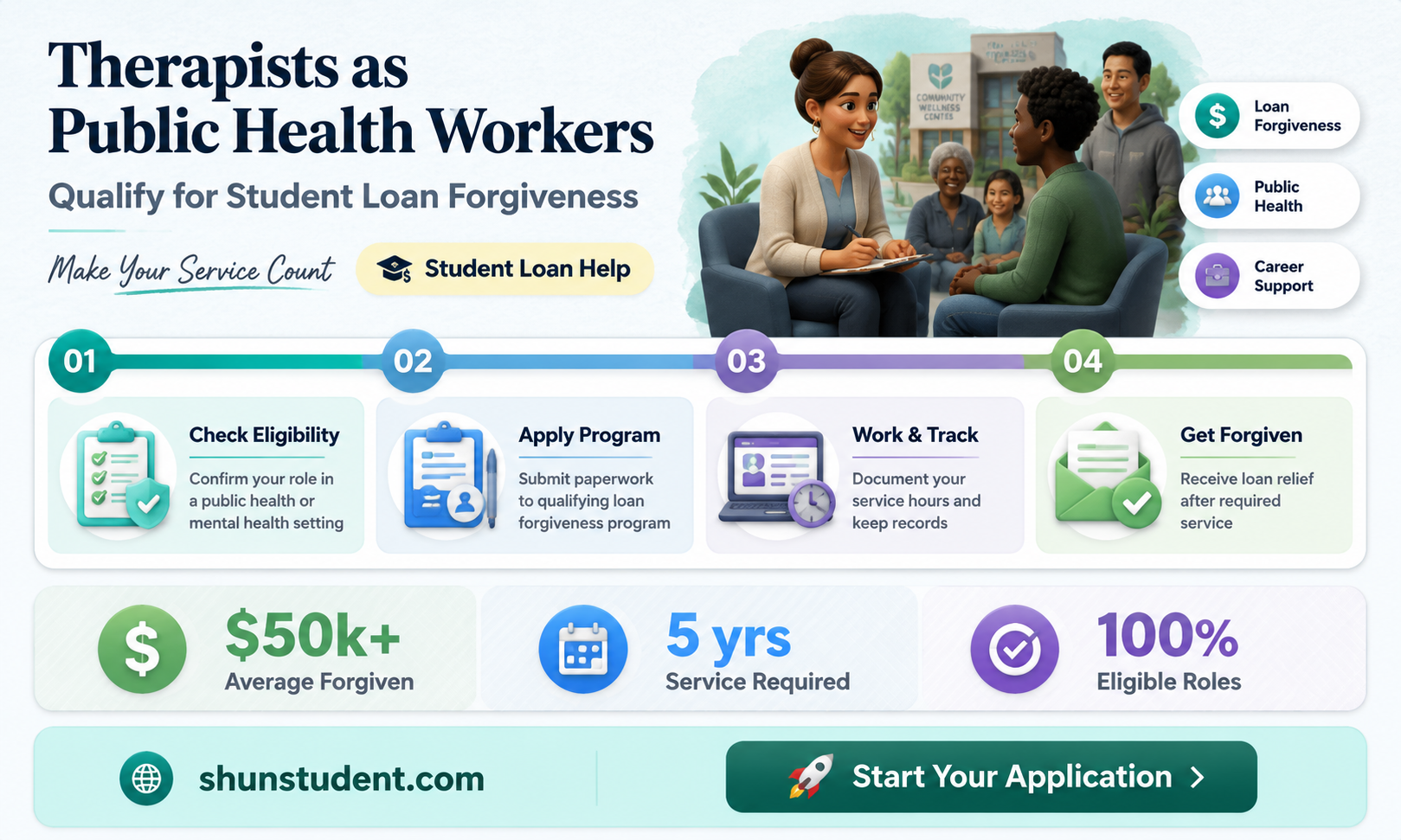

The question of whether therapists qualify for public health student loan forgiveness has gained significant attention as mental health professionals increasingly play a critical role in addressing public health crises. Therapists, including licensed clinical social workers, psychologists, and counselors, often work in underserved communities, schools, and public health settings, providing essential services that align with broader public health goals. Programs like the Public Service Loan Forgiveness (PSLF) and the National Health Service Corps (NHSC) Loan Repayment Program offer pathways for debt relief, but eligibility criteria and application processes can be complex. Understanding whether therapists meet the requirements for these programs is crucial, as it could alleviate financial burdens and encourage more professionals to pursue careers in public health-oriented roles, ultimately improving access to mental health care for those in need.

Explore related products

What You'll Learn

![]()

Eligibility criteria for therapists in public health roles

Therapists seeking student loan forgiveness through public health roles must first understand the eligibility criteria tied to such programs. The Public Service Loan Forgiveness (PSLF) program, for instance, requires applicants to work full-time for a qualifying employer, such as a government or non-profit organization, and make 120 eligible payments. Therapists employed in public health settings like community mental health centers, federally qualified health centers, or government-run clinics often meet these employer criteria. However, simply working in a public health role is not enough; the focus must be on the employer’s classification and the consistency of loan payments under an income-driven repayment plan.

To qualify, therapists must also hold a role that directly contributes to public health objectives. This includes positions in crisis intervention, substance abuse counseling, or mental health services for underserved populations. For example, a therapist working in a rural health clinic addressing opioid addiction would align with public health priorities. Documentation is critical—applicants must submit an Employment Certification Form periodically and keep records of their payments to ensure they remain on track for forgiveness. Missteps in paperwork or payment eligibility can derail the process, making meticulous record-keeping essential.

A comparative analysis of eligibility criteria reveals that therapists in public health roles have an advantage over those in private practice. While private practitioners may struggle to meet the employer requirement, public health therapists often work for government or non-profit entities, which are explicitly eligible under PSLF. Additionally, therapists in public health may qualify for other loan forgiveness programs, such as the National Health Service Corps (NHSC) Loan Repayment Program, which offers up to $50,000 in loan repayment for a two-year commitment in a Health Professional Shortage Area (HPSA). This program requires therapists to provide mental or behavioral health services in underserved communities, further aligning with public health goals.

Persuasively, therapists should consider the long-term benefits of pursuing public health roles for loan forgiveness. While the initial salary in public health may be lower than private practice, the potential for significant loan forgiveness can offset this disparity. For instance, a therapist earning $60,000 annually in a public health role could save over $100,000 in student loans through PSLF or NHSC programs. This financial relief allows therapists to focus on their mission without the burden of debt, fostering greater job satisfaction and long-term career sustainability in public health.

Instructively, therapists should take proactive steps to ensure eligibility. First, verify employer eligibility using the PSLF Help Tool. Second, enroll in an income-driven repayment plan to lower monthly payments and ensure they qualify. Third, submit the Employment Certification Form annually to track progress. Finally, stay informed about program updates, as changes to PSLF or other forgiveness programs can impact eligibility. By following these steps, therapists in public health roles can maximize their chances of achieving student loan forgiveness while making a meaningful impact on community health.

Retirement and Student Loans: Are Debts Forgiven When You Retire?

You may want to see also

Explore related products

![]()

Types of student loan forgiveness programs available

Therapists seeking student loan forgiveness have several pathways to explore, each tailored to different professional contexts and commitments. One prominent option is the Public Service Loan Forgiveness (PSLF) program, which forgives the remaining balance on Direct Loans after 120 qualifying payments. Therapists working full-time for government, non-profit, or certain public health organizations qualify, provided they meet repayment plan and employment certification requirements. This program is particularly advantageous for those in public health roles, as it rewards long-term commitment to underserved communities.

Another avenue is the National Health Service Corps (NHSC) Loan Repayment Program, designed for therapists working in Health Professional Shortage Areas (HPSAs). Participants can receive up to $50,000 in loan repayment for a two-year commitment, with the possibility of additional funding for extended service. This program is ideal for therapists in rural or urban underserved areas, where mental health services are critically needed. Eligibility hinges on licensure and full-time employment in an NHSC-approved site.

For therapists in academic or research roles, the Federal Perkins Loan Cancellation program offers partial to full forgiveness for those teaching in low-income schools or serving in specific public health capacities. Up to 100% of Perkins Loans can be forgiven over five years, with 15% canceled annually. While this program is less common since Perkins Loans are no longer issued, existing borrowers can still benefit if they meet the criteria.

Lastly, state-specific loan repayment programs provide additional opportunities. For instance, the California State Loan Repayment Program (SLRP) offers up to $50,000 for therapists working in federally designated shortage areas. Similar programs exist in other states, often requiring a two-year commitment. Therapists should research their state’s offerings, as these programs frequently complement federal initiatives, maximizing forgiveness potential.

In summary, therapists have multiple forgiveness options, from federal programs like PSLF and NHSC to state-specific initiatives. Each requires careful planning, documentation, and adherence to eligibility criteria. By aligning their career path with these programs, therapists can significantly reduce their student loan burden while serving communities in need.

Unlock $6 Billion Student Loan Forgiveness: Eligibility Guide

You may want to see also

Explore related products

![]()

Required employment settings for loan forgiveness

Therapists seeking student loan forgiveness through public health programs must navigate specific employment requirements, which often dictate where and how they practice. These settings are not arbitrary; they are strategically aligned with areas of greatest need, ensuring that mental health services reach underserved populations. For instance, the National Health Service Corps (NHSC) Loan Repayment Program requires therapists to work in Health Professional Shortage Areas (HPSAs), which are federally designated regions with insufficient healthcare providers. Similarly, the Public Service Loan Forgiveness (PSLF) program mandates employment in government or non-profit organizations, though not all non-profits qualify—only those with a 501(c)(3) designation or certain government-affiliated entities. Understanding these nuances is critical, as the wrong employment setting can disqualify an applicant from forgiveness programs.

To qualify for loan forgiveness, therapists must commit to full-time employment in approved settings, though some programs allow part-time work with prorated benefits. For example, the NHSC program defines full-time as a minimum of 32 hours per week, while PSLF requires 30 hours per week. Employment in schools, community health centers, or federally qualified health centers (FQHCs) often meets these criteria, provided the facility is located in a designated shortage area or serves a predominantly low-income population. Therapists should verify their employer’s eligibility using the NHSC’s Find a Health Center tool or the PSLF Employer Eligibility Form. Caution is advised when considering private practice, as it rarely qualifies unless it operates as a non-profit in a shortage area and meets strict regulatory standards.

A comparative analysis of employment settings reveals that rural and urban underserved areas offer the most opportunities for loan forgiveness. Rural HPSAs, for instance, often have higher repayment amounts due to the critical need for mental health services. Urban settings, while more populated, may also qualify if they serve low-income or marginalized communities. Therapists should weigh the financial benefits against the challenges of working in these areas, such as limited resources or higher caseloads. For example, a therapist working in a rural HPSA might receive up to $50,000 in loan repayment for a two-year commitment, compared to $30,000 in an urban setting. However, rural positions may require additional training in telehealth or crisis intervention to address unique community needs.

Practical steps for therapists include researching eligible employers early in their job search and confirming their status with the relevant forgiveness program. Networking with professionals in qualifying settings can provide insights into the day-to-day realities of these roles. Therapists should also document their employment meticulously, as PSLF requires 120 qualifying payments and proof of eligible employment. For NHSC participants, maintaining licensure and fulfilling service obligations without gaps is essential to avoid repayment penalties. Finally, therapists should explore state-specific loan repayment programs, which may offer additional opportunities in approved settings, such as working with veterans or in opioid treatment programs.

In conclusion, the required employment settings for loan forgiveness demand careful consideration and strategic planning. Therapists must align their career goals with the needs of underserved populations, ensuring their practice location and employer meet program criteria. By choosing settings like HPSAs, FQHCs, or eligible non-profits, therapists can not only alleviate their student debt but also make a meaningful impact on public health. The key lies in thorough research, proactive verification, and a commitment to serving communities where mental health resources are most needed.

Student Loan Pause: Does It Accelerate Your Path to Forgiveness?

You may want to see also

Explore related products

![]()

Documentation and application process details

Therapists seeking public health-related student loan forgiveness must navigate a meticulous documentation and application process, where precision and completeness are paramount. The Public Service Loan Forgiveness (PSLF) program, for instance, requires applicants to submit an Employment Certification Form (ECF) annually or when changing employers. This form verifies that the therapist’s employer qualifies as a public health entity, such as a government agency, 501(c)(3) nonprofit, or certain other organizations providing public health services. Missing even one ECF submission can reset the 120 qualifying payment count, delaying forgiveness. Additionally, therapists must ensure their loans are in a qualifying repayment plan, such as Income-Driven Repayment (IDR), and make all payments on time.

The application process for PSLF culminates in the submission of the PSLF Application for Forgiveness after 120 qualifying payments. This form requires detailed documentation, including payment histories and previous ECFs. Therapists should also prepare for potential audits by retaining all records, including pay stubs, tax forms, and employer verification letters. For those in the National Health Service Corps (NHSC) Loan Repayment Program, the process involves submitting a separate application, which includes proof of licensure, employment contracts, and service commitment details. Both programs demand strict adherence to deadlines, with NHSC applications typically due in the spring for funding cycles beginning in the fall.

A comparative analysis reveals that while PSLF requires 120 payments over 10 years, NHSC offers up to $50,000 in loan repayment for a two-year commitment in a Health Professional Shortage Area (HPSA). Therapists must weigh the long-term commitment of PSLF against the immediate financial relief of NHSC. For example, a therapist working in a rural clinic might qualify for both programs but may prioritize NHSC for quicker debt reduction. However, NHSC’s competitive nature means not all applicants are accepted, making PSLF a more reliable but slower option.

Persuasively, therapists should proactively organize their documentation to avoid common pitfalls. Creating a digital folder for all loan-related documents, setting calendar reminders for ECF submissions, and consulting with a loan servicer annually can streamline the process. For instance, using a spreadsheet to track payments and employer certifications ensures nothing is overlooked. Therapists should also consider consulting with a financial advisor or student loan specialist to optimize their repayment strategy. By treating the application process as a long-term project rather than a last-minute task, therapists can maximize their chances of securing forgiveness.

In conclusion, the documentation and application process for public health-related student loan forgiveness demands diligence, organization, and strategic planning. Therapists must understand the specific requirements of programs like PSLF and NHSC, maintain meticulous records, and adhere to deadlines. By approaching this process systematically, therapists can navigate the complexities of loan forgiveness and achieve financial relief while serving in critical public health roles.

Unraveling the Truth About Student Loan Forgiveness: Fact or Fiction?

You may want to see also

Explore related products

![]()

Impact of part-time vs. full-time work on forgiveness

The choice between part-time and full-time work significantly affects therapists’ eligibility and timeline for student loan forgiveness under public health programs. Full-time employment, typically defined as 30+ hours per week, accelerates forgiveness by meeting program requirements faster. For instance, the Public Service Loan Forgiveness (PSLF) program mandates 120 qualifying payments, which full-time workers can achieve in 10 years. Part-time workers, however, may extend this timeline proportionally, as each payment period corresponds to a month of qualifying employment, regardless of hours worked.

Consider the practical implications: a therapist working 20 hours per week at a nonprofit clinic will still qualify for PSLF but will need to ensure consistent payments and employment verification. Part-time workers must meticulously track their hours and payments, as partial schedules can complicate documentation. For example, a therapist working 24 hours per week at a federally qualified health center (FQHC) remains eligible for both PSLF and National Health Service Corps (NHSC) loan repayment assistance, but their forgiveness timeline aligns with their employment duration, not their peers’.

From a strategic perspective, part-time work offers flexibility but demands careful planning. Therapists in this position should prioritize maximizing their income-driven repayment (IDR) plan contributions to minimize interest capitalization. For instance, a part-time therapist earning $40,000 annually might opt for Pay As You Earn (PAYE) to cap monthly payments at 10% of discretionary income, ensuring affordability while progressing toward forgiveness. Conversely, full-time workers benefit from higher earnings, which can be allocated toward additional payments to shorten the forgiveness timeline.

A comparative analysis reveals trade-offs: full-time work expedites forgiveness but may limit work-life balance, while part-time work extends the process but offers flexibility. Therapists must weigh their financial goals, career stage, and personal priorities. For example, a mid-career therapist with significant debt might opt for full-time work at a public health agency to maximize PSLF benefits, while a new parent might choose part-time employment at a school-based clinic to balance family responsibilities.

Ultimately, the impact of part-time versus full-time work on loan forgiveness hinges on individual circumstances and program specifics. Therapists should consult resources like the Federal Student Aid website or a financial advisor to tailor their strategy. Whether full-time or part-time, consistent employment in qualifying public health roles remains the cornerstone of securing forgiveness. Practical tips include maintaining detailed employment records, enrolling in IDR plans, and annually certifying employment for PSLF to stay on track.

Volunteering with BSA: Can It Help Forgive Your Student Loans?

You may want to see also

Frequently asked questions

Yes, therapists can qualify for PSLF if they work full-time for a qualifying employer, such as a government or non-profit organization, and make 120 eligible payments under an income-driven repayment plan.

Therapists such as licensed clinical social workers, psychologists, marriage and family therapists, and mental health counselors may qualify if they work in designated public health or non-profit settings, such as community health centers or government agencies.

Generally, private practice therapists do not qualify for PSLF unless they work for a qualifying employer. However, they may explore other forgiveness programs or repayment options based on their specific circumstances.

Therapists can use the Federal Student Aid Employer Qualification Form to confirm if their employer meets PSLF requirements. Submitting this form to the U.S. Department of Education ensures eligibility for the program.