Subsidized student loans, a form of federal financial aid designed to assist students with demonstrated financial need, often come with the added benefit of government-paid interest while the borrower is in school, during grace periods, and in certain deferment periods. A common question among borrowers is whether these loans are eligible for forgiveness. While subsidized loans themselves are not automatically forgiven, they can qualify for various loan forgiveness programs, such as Public Service Loan Forgiveness (PSLF) or income-driven repayment (IDR) plans, which can discharge remaining balances after a set number of qualifying payments. Understanding the eligibility criteria and requirements for these programs is crucial for borrowers seeking to manage or eliminate their student debt effectively.

| Characteristics | Values |

|---|---|

| Loan Type | Subsidized Direct Loans (undergraduate only) |

| Forgiveness Eligibility | Not automatically forgiven; must qualify through specific programs |

| Income-Driven Repayment (IDR) Forgiveness | Remaining balance forgiven after 20-25 years of qualifying payments |

| Public Service Loan Forgiveness (PSLF) | Forgiveness after 10 years of qualifying payments and employment |

| Teacher Loan Forgiveness | Up to $17,500 forgiveness for eligible teachers in low-income schools |

| Disability Discharge | Full forgiveness if borrower has a permanent disability |

| Death Discharge | Loans forgiven upon borrower's death |

| Closed School Discharge | Forgiveness if school closes while enrolled or shortly after withdrawal |

| Bankruptcy Discharge | Extremely rare, but possible under undue hardship |

| Interest Subsidy During Forgiveness | Government pays interest during in-school, grace, and deferment periods |

| Tax Treatment of Forgiven Amounts | Generally tax-free under current law (exceptions may apply) |

| Eligibility for Other Forgiveness Programs | Can qualify for programs like Perkins Loan Cancellation |

| Repayment Plans | Eligible for all federal repayment plans, including IDR |

| Borrower Defense to Repayment | Forgiveness if school misled borrower (case-by-case basis) |

| Automatic Forgiveness | No automatic forgiveness; requires application and eligibility |

| Loan Consolidation Impact | Consolidation may reset IDR payment counts but retains subsidized status |

Explore related products

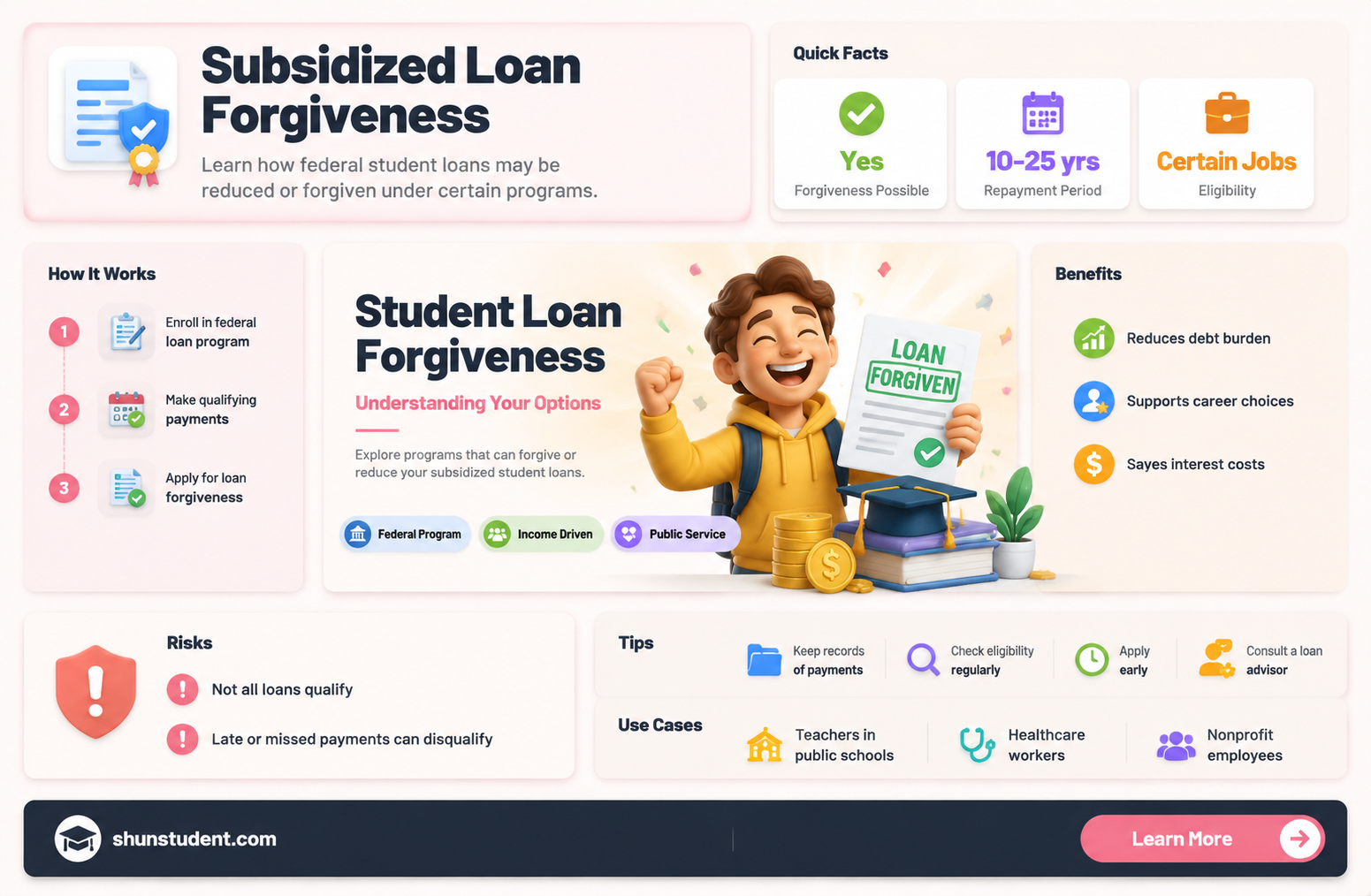

What You'll Learn

- Income-Driven Repayment Forgiveness: Loans forgiven after 20-25 years of payments under income-driven plans

- Public Service Loan Forgiveness (PSLF): Forgiveness after 10 years of payments in public service jobs

- Teacher Loan Forgiveness: Up to $17,500 forgiven for teachers in low-income schools

- Disability Discharge: Loans forgiven if borrower becomes totally and permanently disabled

- Closed School Discharge: Forgiveness if school closes while enrolled or shortly after

![]()

Income-Driven Repayment Forgiveness: Loans forgiven after 20-25 years of payments under income-driven plans

Subsidized student loans, unlike their unsubsidized counterparts, do not accrue interest while the borrower is in school, but they are not automatically forgiven. However, borrowers with subsidized loans can still benefit from Income-Driven Repayment (IDR) Forgiveness, a program designed to provide relief after 20 to 25 years of qualifying payments. This option is particularly valuable for those with lower incomes or high debt-to-income ratios, as it caps monthly payments at a manageable percentage of discretionary income. For instance, under the Revised Pay As You Earn (REPAYE) plan, payments are set at 10% of discretionary income, making long-term repayment more feasible.

To qualify for IDR Forgiveness, borrowers must first enroll in an income-driven repayment plan, such as Income-Based Repayment (IBR), Pay As You Earn (PAYE), or REPAYE. Each plan has specific eligibility criteria, but all require annual recertification of income and family size. For example, IBR is available to borrowers with federal student loans taken out before or after July 1, 2014, but the payment cap and forgiveness timeline differ based on the loan’s disbursement date. Borrowers with newer loans pay 10% of discretionary income and receive forgiveness after 20 years, while those with older loans pay 15% and wait 25 years.

One critical aspect of IDR Forgiveness is the tax implications. As of current regulations, forgiven amounts are treated as taxable income, which can result in a significant tax bill. For example, if $50,000 is forgiven after 20 years, the borrower may owe taxes on that amount at their ordinary income tax rate. To mitigate this, borrowers should plan ahead by setting aside funds in a savings account or consulting a tax professional to explore strategies like the Public Service Loan Forgiveness (PSLF) program, which offers tax-free forgiveness after 10 years of qualifying payments for those in eligible public service jobs.

Practical tips for maximizing IDR Forgiveness include staying current on payments, recertifying income on time, and choosing the plan that best aligns with financial goals. For instance, borrowers expecting income growth may opt for the standard 10-year repayment plan to avoid prolonged debt, while those with stable, low incomes might benefit from REPAYE’s interest subsidies, which cover half of unpaid interest on subsidized loans for the first three years. Additionally, keeping detailed records of payments and correspondence with loan servicers is essential for resolving disputes and ensuring progress toward forgiveness.

In conclusion, while subsidized student loans are not automatically forgiven, IDR Forgiveness offers a pathway to debt relief for borrowers committed to long-term repayment. By understanding the nuances of each income-driven plan, planning for tax liabilities, and adopting strategic repayment habits, borrowers can navigate this complex system effectively. This approach not only alleviates financial stress but also empowers individuals to make informed decisions about their educational investments and future financial stability.

Disabled Veterans: Do They Qualify for Student Loan Forgiveness?

You may want to see also

Explore related products

![]()

Public Service Loan Forgiveness (PSLF): Forgiveness after 10 years of payments in public service jobs

For those burdened by student debt, the Public Service Loan Forgiveness (PSLF) program offers a beacon of hope. Established in 2007, PSLF promises to forgive the remaining balance on eligible federal student loans after 120 qualifying payments while working full-time for a qualifying public service employer. This translates to a potential path to debt freedom in just 10 years, a stark contrast to the standard 10-25 year repayment plans.

Unlike income-driven forgiveness programs that require 20-25 years of payments, PSLF's 10-year timeline is a significant advantage. However, it's crucial to understand the program's stringent eligibility requirements.

Qualifying Employment: Not all public service jobs qualify. Eligible employers include government organizations at any level (federal, state, local, or tribal), 501(c)(3) non-profit organizations, and some other types of non-profits that provide specific public services. Teaching, social work, healthcare, law enforcement, and military service are common examples of qualifying careers.

Loan Types: Only Direct Loans are eligible for PSLF. This includes Direct Subsidized and Unsubsidized Loans, Direct PLUS Loans, and Direct Consolidation Loans. If you have Federal Family Education Loans (FFEL) or Perkins Loans, you'll need to consolidate them into a Direct Consolidation Loan to qualify.

Payment Requirements: Payments must be made under a qualifying repayment plan, such as an income-driven plan (IDR). Each payment must be made on time and in full. Partial payments or payments made during periods of deferment or forbearance do not count towards the 120 required payments.

Certification and Tracking: It's essential to certify your employment annually with the U.S. Department of Education and your loan servicer. This ensures your payments are being tracked correctly and helps identify any potential issues early on.

Perseverance is Key: The PSLF application process can be complex and requires meticulous record-keeping. Don't be discouraged by the paperwork. Utilize resources like the Federal Student Aid website and consider seeking guidance from a student loan counselor.

While PSLF demands dedication and careful planning, the potential reward of debt forgiveness after 10 years makes it a compelling option for those committed to a career in public service.

Unlocking CSU Student Loan Forgiveness: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

Teacher Loan Forgiveness: Up to $17,500 forgiven for teachers in low-income schools

Teachers in low-income schools face unique challenges, from resource scarcity to larger class sizes, yet their role in shaping futures is undeniable. The Teacher Loan Forgiveness program acknowledges this by offering up to $17,500 in debt relief for eligible educators. To qualify, teachers must work full-time for five consecutive years in a low-income elementary or secondary school designated by the federal government. This program specifically targets subsidized Direct Loans and Subsidized Federal Stafford Loans, providing a lifeline for those burdened by student debt.

Consider this scenario: A math teacher with $25,000 in subsidized Direct Loans teaches for five years at a Title I school. After completing the required service, $17,500 of their debt is forgiven, reducing their balance to $7,500. This example highlights the program’s potential to significantly alleviate financial strain, allowing educators to focus on their students rather than their loans. However, it’s crucial to note that the forgiveness amount caps at $17,500, even if the total debt exceeds this figure.

To maximize this opportunity, teachers should verify their school’s eligibility annually through the Federal Student Aid website, as designations can change. Additionally, maintaining detailed records of employment and loan payments is essential for a smooth application process. While the program doesn’t cover private loans or unsubsidized federal loans, it remains a powerful tool for subsidized loan holders. Pairing this forgiveness with other programs, like Public Service Loan Forgiveness (PSLF), can further reduce debt for long-term educators.

Critics argue that the $17,500 cap falls short of addressing the full scope of teacher debt, especially for those with advanced degrees. However, the program’s value lies in its accessibility and focus on underserved communities. By incentivizing service in low-income schools, it bridges the gap between financial relief and societal need. Teachers considering this path should weigh the benefits against their career goals, ensuring the commitment aligns with their long-term plans.

In practice, securing Teacher Loan Forgiveness requires proactive steps. First, confirm your loans are eligible—only subsidized Direct and Stafford Loans qualify. Second, submit an Employment Certification Form annually to track progress toward the five-year requirement. Finally, apply for forgiveness after completing the service period using the Teacher Loan Forgiveness Application. While the process demands diligence, the reward—up to $17,500 in debt erased—is a testament to the program’s impact on both educators and the students they serve.

When Will Student Loan Forgiveness Begin? Timelines and Updates

You may want to see also

Explore related products

![]()

Disability Discharge: Loans forgiven if borrower becomes totally and permanently disabled

For borrowers facing total and permanent disability, the Disability Discharge program offers a critical lifeline by forgiving federal student loans, including subsidized ones. This provision acknowledges the financial strain disability can impose, providing relief to those who can no longer work. To qualify, borrowers must submit proof of their disability, which can include documentation from the Social Security Administration, a physician’s certification, or evidence of a disability-based veterans’ benefit. Once approved, the loans are discharged, freeing the borrower from repayment obligations. This process not only alleviates financial burden but also ensures dignity and stability for individuals navigating long-term health challenges.

The application process for Disability Discharge, while straightforward, requires careful attention to detail. Borrowers must complete an application form and include supporting documentation that meets specific criteria. For instance, physician certifications must confirm the borrower’s inability to engage in substantial gainful activity due to a physical or mental impairment expected to last continuously for at least 60 months or result in death. It’s crucial to retain copies of all submitted materials and follow up with the loan servicer to ensure the application is processed promptly. Borrowers should also be aware that discharged loans may be subject to a three-year post-discharge monitoring period, during which certain income and employment conditions must be met to avoid loan reinstatement.

One often-overlooked aspect of Disability Discharge is its tax implications. Prior to 2018, forgiven loans were considered taxable income, potentially saddling disabled borrowers with a significant tax liability. However, the Tax Cuts and Jobs Act of 2017 eliminated this burden for discharges due to disability through 2025, ensuring financial relief extends beyond loan forgiveness. Borrowers should consult a tax professional to understand their specific obligations, especially if their discharge occurs after 2025. This exemption underscores the program’s intent to provide comprehensive support, addressing both immediate and long-term financial concerns.

Comparatively, Disability Discharge stands out among loan forgiveness programs for its accessibility and scope. Unlike income-driven repayment plans or Public Service Loan Forgiveness, which require years of qualifying payments, Disability Discharge offers immediate relief upon approval. It also applies to all federal student loans, including subsidized, unsubsidized, and PLUS loans, making it a versatile option for a wide range of borrowers. However, it’s essential to distinguish this program from temporary disability forbearance, which only pauses payments and does not forgive debt. For those permanently unable to work, Disability Discharge remains the most effective solution, combining compassion with practical financial relief.

Finally, advocacy and awareness play a pivotal role in maximizing the impact of Disability Discharge. Many eligible borrowers remain unaware of this option, often due to complex eligibility criteria or lack of outreach. Organizations, educators, and policymakers can bridge this gap by disseminating clear, actionable information about the program. Encouraging borrowers to explore their eligibility and providing step-by-step guidance can transform lives, ensuring that disability does not equate to lifelong debt. By prioritizing accessibility and transparency, the Disability Discharge program can fulfill its promise of offering a fresh start to those facing insurmountable health and financial challenges.

Paid Off Student Loans? How to Still Qualify for Loan Forgiveness

You may want to see also

Explore related products

![]()

Closed School Discharge: Forgiveness if school closes while enrolled or shortly after

Imagine this: You’re enrolled in a program, working toward a degree, when suddenly your school shuts down. Your education is interrupted, your future uncertain, and your student loans still loom. This is where Closed School Discharge steps in—a federal provision designed to forgive subsidized and unsubsidized Direct Loans, Federal Family Education Loans (FFEL), and Perkins Loans if your school closes while you’re enrolled or shortly after you withdraw. It’s a lifeline for borrowers caught in the fallout of institutional collapse, but it’s not automatic. You must apply, and eligibility hinges on specific timing and circumstances.

To qualify, you must have been enrolled at the time of closure or withdrawn no more than 120 days prior (for loans issued before July 1, 2020) or 180 days prior (for loans issued after that date). If you transferred credits to another school through a teach-out agreement, you’re likely ineligible unless you decline the teach-out. For example, if your school closed on June 1, 2023, and you withdrew on February 1, 2023, you’d qualify under the 180-day rule. However, if you completed a teach-out program, forgiveness is off the table unless you explicitly opted out.

Applying for Closed School Discharge involves submitting a request to your loan servicer, often with proof of enrollment dates. The process can be bureaucratic, so keep detailed records of your attendance and withdrawal dates. If approved, not only are your loans forgiven, but any amounts already paid are refunded. However, beware: discharged loans may be considered taxable income, so consult a tax professional to plan accordingly.

Compared to other forgiveness programs, Closed School Discharge is more straightforward but narrower in scope. It doesn’t require a career in public service or years of payments like Public Service Loan Forgiveness (PSLF) or income-driven repayment plans. Instead, it’s a targeted solution for a specific crisis. For instance, students affected by the abrupt closures of for-profit chains like ITT Tech or Corinthian Colleges have benefited from this discharge, regaining financial stability after losing their educational pathway.

In practice, this discharge is a critical safety net, but it’s reactive, not preventive. Borrowers should stay informed about their school’s financial health and understand their rights if closure occurs. While it won’t erase the disruption to your education, Closed School Discharge can lift the burden of debt, allowing you to refocus on rebuilding your academic and financial future.

Biden's Student Loan Forgiveness: Step-by-Step Application Guide for Borrowers

You may want to see also

Frequently asked questions

Yes, subsidized student loans are eligible for certain forgiveness programs, such as Public Service Loan Forgiveness (PSLF) and income-driven repayment (IDR) plans, depending on the borrower's circumstances and the specific program requirements.

No, subsidized student loans do not automatically qualify for forgiveness after a set period. Borrowers must meet specific criteria, such as working in public service or making qualifying payments under an IDR plan, to be eligible for forgiveness.

Yes, subsidized student loans can be forgiven through programs like Teacher Loan Forgiveness or PSLF if you work in eligible professions and meet the program’s requirements, such as completing a certain number of years of service in a designated field.