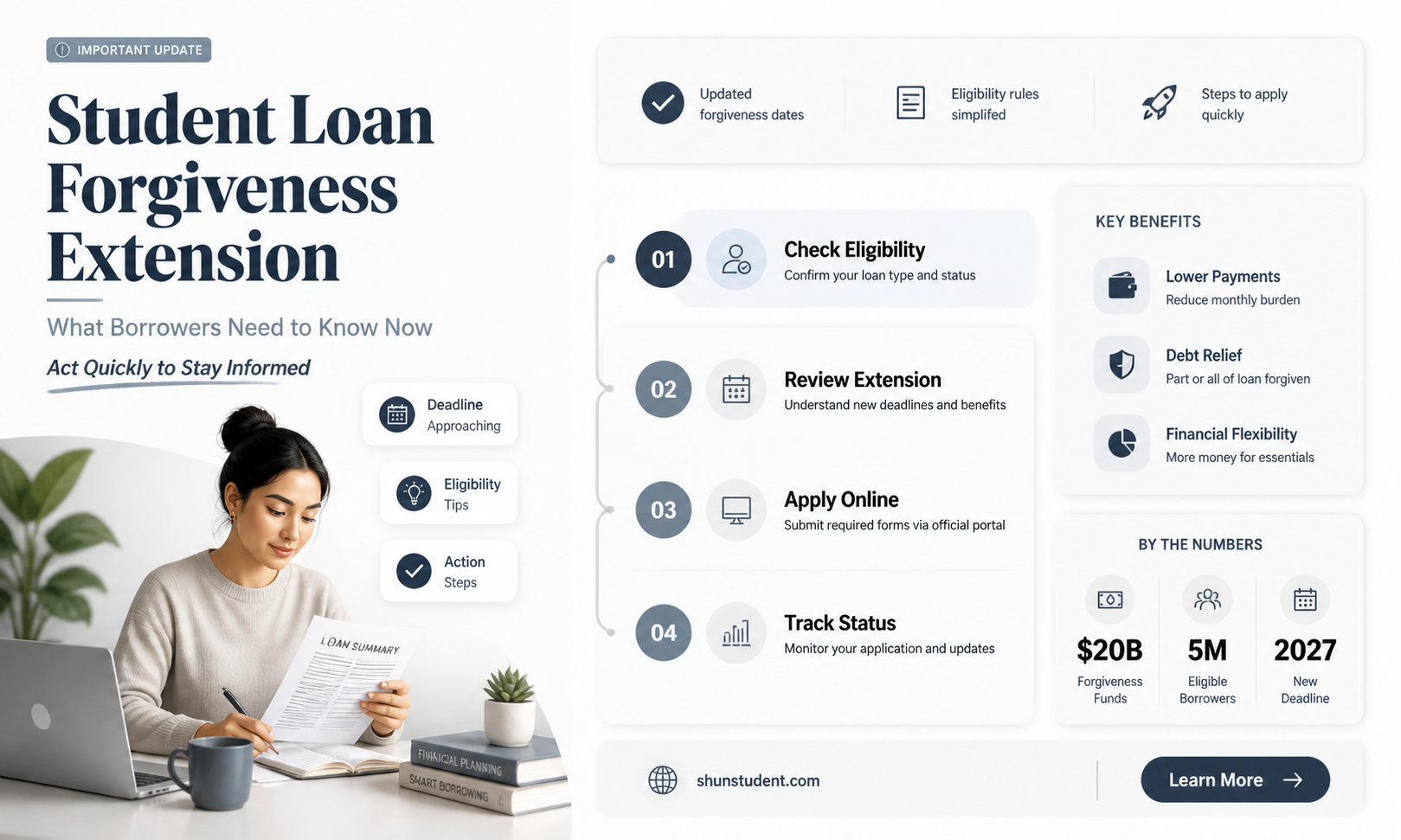

The topic of extending student loan forgiveness has become a focal point of national discussion, as millions of borrowers eagerly await updates on potential relief measures. With the current economic climate and the lingering effects of the pandemic, many are calling for further extensions or expansions of existing forgiveness programs to alleviate the financial burden on graduates. Policymakers and advocates are debating the feasibility and implications of such actions, weighing the benefits of debt relief against concerns about cost and fairness. As deadlines for repayment loom, borrowers are closely monitoring legislative developments and executive actions, hoping for clarity and support in managing their student loan obligations.

| Characteristics | Values |

|---|---|

| Current Status | No official extension announced as of October 2023. |

| Recent Updates | Supreme Court struck down Biden's one-time student loan forgiveness plan in June 2023. |

| Ongoing Relief Measures | Payment pause ended in October 2023; payments and interest resumed. |

| Income-Driven Repayment (IDR) Changes | New IDR plan (SAVE Plan) reduces monthly payments for eligible borrowers. |

| Public Service Loan Forgiveness (PSLF) | Temporary waiver expired Oct. 31, 2023; standard PSLF rules now apply. |

| Legislative Efforts | No active bills in Congress to extend broad forgiveness as of late 2023. |

| Department of Education Focus | Targeted relief for specific groups (e.g., defrauded students, disabled borrowers). |

| Next Steps for Borrowers | Enroll in SAVE Plan or explore existing forgiveness programs (PSLF, IDR). |

| Political Climate | Divided Congress makes broad forgiveness extension unlikely in near term. |

| Legal Challenges | Ongoing lawsuits may impact future forgiveness initiatives. |

Explore related products

What You'll Learn

- Eligibility Criteria Changes: Updates to who qualifies for extended student loan forgiveness programs

- Income-Driven Repayment Plans: Adjustments to repayment plans affecting forgiveness timelines

- Public Service Loan Forgiveness (PSLF): Enhancements or expansions to PSLF requirements

- One-Time Forgiveness Extensions: Potential additional one-time forgiveness opportunities for borrowers

- Legislative Updates: New bills or policies impacting student loan forgiveness extensions

![]()

Eligibility Criteria Changes: Updates to who qualifies for extended student loan forgiveness programs

Recent updates to student loan forgiveness programs have shifted the eligibility landscape, leaving many borrowers wondering if they still qualify. One of the most significant changes involves the expansion of income thresholds for Public Service Loan Forgiveness (PSLF). Previously, borrowers had to earn below a certain income cap to qualify, but new guidelines now consider a broader range of incomes, particularly for those in high-cost-of-living areas. This adjustment aims to include more public servants, such as teachers and nurses, who may have been excluded due to regional salary disparities.

Another critical update is the inclusion of additional loan types under the forgiveness umbrella. While earlier programs primarily targeted Direct Loans, recent changes now allow borrowers with Federal Family Education Loans (FFEL) and Perkins Loans to consolidate into Direct Consolidation Loans, making them eligible for forgiveness. This shift is particularly beneficial for older borrowers who may have taken out loans before the Direct Loan program became the standard. However, it’s essential to act promptly, as consolidation can reset the clock on qualifying payments, potentially delaying forgiveness.

For those in income-driven repayment (IDR) plans, the eligibility criteria have also been refined. The government now counts more types of financial hardship, such as medical expenses and childcare costs, when calculating discretionary income. This means borrowers with higher living expenses may qualify for lower monthly payments, accelerating their path to forgiveness. Additionally, the forgiveness timeline for some IDR plans has been shortened from 25 to 20 years, providing relief to long-term borrowers.

A notable cautionary point is the stricter verification process for employment certification. Borrowers seeking PSLF must now provide detailed documentation of their public service employment, including annual certifications. While this ensures program integrity, it places a greater burden on applicants to maintain accurate records. Practical tips include submitting employment certification forms annually and keeping a digital archive of all relevant documents to streamline the verification process.

In conclusion, the eligibility criteria changes reflect a more inclusive approach to student loan forgiveness, addressing long-standing gaps in the system. By expanding income thresholds, including more loan types, and refining IDR calculations, these updates aim to provide relief to a broader spectrum of borrowers. However, navigating these changes requires vigilance and proactive steps, such as consolidating loans and maintaining thorough documentation, to maximize the benefits of these extended programs.

Is Graduate Student Debt Forgiveness a Reality? Exploring Options and Myths

You may want to see also

Explore related products

![]()

Income-Driven Repayment Plans: Adjustments to repayment plans affecting forgiveness timelines

Income-driven repayment (IDR) plans have long been a lifeline for borrowers juggling student loan debt, but recent adjustments to these plans are reshaping forgiveness timelines in ways both subtle and significant. For instance, the Biden administration’s 2023 updates to IDR plans, such as the Saving on a Valuable Education (SAVE) Plan, lower monthly payments by capping them at a smaller percentage of discretionary income—5% for undergraduate loans, down from 10% under older plans. This reduction extends repayment periods but accelerates forgiveness for some borrowers, particularly those with lower incomes or higher debt balances. For example, a borrower with $40,000 in debt and an income of $40,000 could see forgiveness after 10 years under the SAVE Plan, compared to 20–25 years under previous IDR plans.

However, these adjustments aren’t without complexity. The new rules introduce a sliding scale for payment caps based on income and family size, requiring borrowers to recalculate their eligibility annually. For a single borrower earning $50,000, the monthly payment under the SAVE Plan would be roughly $125, compared to $250 under the Revised Pay As You Earn (REPAYE) Plan. While this eases immediate financial strain, it also means borrowers must stay vigilant about recertifying income and family size to avoid payment spikes or delays in forgiveness. Missteps here could reset the forgiveness clock, underscoring the need for proactive management.

Another critical change is the treatment of unpaid interest. Under the SAVE Plan, unpaid interest no longer capitalizes for borrowers making regular payments, preventing balances from ballooning over time. This is a game-changer for those with high-interest loans, as it keeps the principal amount stable and ensures that every payment brings them closer to forgiveness. For instance, a borrower with $60,000 in loans at 6% interest could save over $10,000 in capitalized interest over 10 years under the new rules. Yet, this benefit is contingent on consistent payments, making it essential for borrowers to budget carefully and avoid payment pauses or defaults.

Comparatively, these adjustments highlight a shift from broad-stroke forgiveness extensions to targeted relief for specific borrower profiles. While the changes benefit low-income earners and those with large debt-to-income ratios, they may offer less immediate relief for higher-earning borrowers or those nearing the end of their repayment terms. For example, a borrower with $80,000 in debt and a $70,000 income might still face a 20-year repayment timeline, albeit with lower monthly payments. This underscores the importance of evaluating individual circumstances before switching plans, as the “best” option depends on income trajectory, family size, and long-term financial goals.

In practice, borrowers should take three steps to maximize these adjustments: first, enroll in the SAVE Plan if eligible, as it offers the most generous terms; second, recertify income and family size annually to avoid payment increases; and third, monitor loan servicer communications for updates on forgiveness eligibility. Tools like the Federal Student Aid Loan Simulator can help model repayment scenarios under different plans. While the path to forgiveness is now clearer for many, it remains a marathon, not a sprint—one that requires patience, planning, and persistence.

Biden's Student Loan Forgiveness: Duration and Long-Term Implications Explained

You may want to see also

Explore related products

![]()

Public Service Loan Forgiveness (PSLF): Enhancements or expansions to PSLF requirements

The Public Service Loan Forgiveness (PSLF) program has undergone significant changes in recent years, with policymakers and advocates pushing for enhancements and expansions to make it more accessible and effective. One key area of focus is simplifying the often complex and confusing requirements, which have historically led to high denial rates. For instance, the U.S. Department of Education introduced the Limited PSLF (LPSLFWaiver) in 2021, allowing borrowers to receive credit for past payments made under any federal loan program or repayment plan, regardless of whether they met the original PSLF criteria. This temporary waiver, extended through October 31, 2023, has provided a lifeline for thousands of borrowers, but it also highlights the need for permanent reforms.

To further enhance PSLF, policymakers are considering expansions that would lower barriers to entry and increase eligibility. One proposal is to broaden the definition of "public service" to include a wider range of occupations, such as public health workers, first responders, and nonprofit employees in non-501(c)(3) organizations. Another suggestion is to reduce the required number of qualifying payments from 120 to 60 or 84 months, particularly for borrowers in high-need fields like education and healthcare. These changes would not only make PSLF more inclusive but also address workforce shortages in critical sectors.

Implementing these enhancements requires careful consideration of potential challenges. For example, expanding eligibility could strain the program’s budget, necessitating additional federal funding or creative financing solutions. Additionally, simplifying the application process, such as by integrating PSLF eligibility checks into existing loan servicer platforms, could reduce administrative burdens but would require significant technological upgrades. Borrowers should stay informed about these developments and take proactive steps, such as consolidating loans into the Direct Loan program and submitting the PSLF Help Tool form to ensure their payments count toward forgiveness.

A comparative analysis of PSLF with other loan forgiveness programs, like income-driven repayment (IDR) plans, reveals opportunities for synergy. While IDR plans offer forgiveness after 20–25 years of payments, PSLF provides relief in just 10 years for qualifying borrowers. By aligning PSLF with IDR timelines or allowing partial forgiveness after a certain number of payments, policymakers could create a more flexible and appealing system. For instance, a borrower working in public service could receive partial forgiveness after 5 years, encouraging long-term commitment while providing immediate financial relief.

Ultimately, the success of PSLF enhancements depends on clear communication and borrower engagement. The Department of Education should launch targeted outreach campaigns to inform eligible borrowers about changes and provide step-by-step guidance on applying. Practical tips, such as keeping detailed records of employment and payments, can help borrowers navigate the process. By addressing current limitations and expanding access, PSLF can fulfill its promise of supporting those who dedicate their careers to public service, easing the burden of student debt and fostering a more equitable society.

IRS and Student Loan Forgiveness: Navigating Income Tax Implications

You may want to see also

Explore related products

![]()

One-Time Forgiveness Extensions: Potential additional one-time forgiveness opportunities for borrowers

As of the latest updates, the Biden administration has been actively exploring avenues to provide further relief to student loan borrowers, particularly through one-time forgiveness extensions. These extensions are designed to address gaps in existing programs like Public Service Loan Forgiveness (PSLF) and income-driven repayment (IDR) plans, offering a lifeline to borrowers who may have fallen through the cracks. For instance, the limited PSLF waiver, which expired in October 2022, allowed borrowers to retroactively receive credit for past payments that previously didn’t qualify. This set a precedent for how one-time extensions can correct systemic issues and provide targeted relief.

To understand the potential for additional one-time forgiveness opportunities, consider the mechanics of such extensions. They typically involve temporary adjustments to eligibility criteria, allowing borrowers to consolidate loans, recalculate payment counts, or qualify for forgiveness under revised terms. For example, a hypothetical extension could allow borrowers with Federal Family Education Loans (FFEL) to consolidate into Direct Loans without losing progress toward forgiveness. This would require clear instructions from the Department of Education, including deadlines and eligibility requirements, to ensure borrowers can take advantage of the opportunity.

From a persuasive standpoint, one-time forgiveness extensions are not just about financial relief but also about restoring trust in the student loan system. Borrowers who have made payments for years, only to discover they don’t qualify for forgiveness due to technicalities, feel betrayed. Extensions like the PSLF waiver demonstrated that such measures can correct these injustices, providing a moral and practical justification for their continuation. Policymakers must weigh the cost of these extensions against the long-term benefits of a more equitable and functional loan system.

Comparatively, one-time extensions differ from broad-based forgiveness proposals in their targeted approach. While universal forgiveness would cancel debt for all borrowers up to a certain threshold, extensions focus on specific groups, such as those in public service or with older loan types. This precision makes extensions more politically feasible, as they address clear administrative failures rather than redistributing debt relief broadly. However, borrowers should remain cautious and proactive, as these opportunities are often time-sensitive and require specific actions, such as consolidating loans or submitting paperwork.

In conclusion, one-time forgiveness extensions represent a pragmatic solution to the student loan crisis, offering relief to borrowers who have been disadvantaged by bureaucratic complexities. By learning from past extensions like the PSLF waiver, policymakers can design future opportunities that are both impactful and administratively manageable. Borrowers should stay informed through official channels, such as the Department of Education’s website, and take immediate action when new extensions are announced. This approach ensures that relief reaches those who need it most, without the uncertainty of broader legislative changes.

Forgiven Student Loans: How to Verify Your Debt Relief Status

You may want to see also

Explore related products

$19.25 $22.99

![]()

Legislative Updates: New bills or policies impacting student loan forgiveness extensions

Recent legislative activity has introduced several bills aimed at extending or modifying student loan forgiveness programs, reflecting ongoing debates about the scope and sustainability of such initiatives. One notable proposal is the Student Loan Forgiveness for Frontline Heroes Act, which seeks to expand forgiveness eligibility to essential workers who served during the COVID-19 pandemic. This bill would provide up to $25,000 in loan forgiveness for eligible borrowers, including healthcare workers, teachers, and first responders. The rationale behind this legislation is to recognize the sacrifices made by these individuals while addressing the financial burden of student debt. However, critics argue that such targeted forgiveness could create inequities among borrowers and strain federal resources.

Another significant development is the Fresh Start Through Repayment Act, which proposes a one-time reset for borrowers in default, allowing them to re-enter repayment plans without penalties. While not a direct extension of forgiveness, this bill aims to provide relief to the 7.9 million borrowers currently in default, many of whom could qualify for forgiveness programs if their accounts were rehabilitated. This approach addresses a critical gap in existing policies, as defaulted borrowers often face barriers to accessing forgiveness options like Public Service Loan Forgiveness (PSLF). Advocates argue that this measure would improve financial stability for millions, while opponents question its long-term impact on loan repayment rates.

In contrast, the Responsible Education Assistance through Loan (REAL) Reforms Act takes a more restrictive approach, proposing to cap the amount of federal loans students can borrow based on their field of study and expected earnings. While not an extension of forgiveness, this bill indirectly impacts forgiveness programs by limiting the total debt eligible for relief. Proponents argue that this measure would curb rising tuition costs and reduce the need for widespread forgiveness, while critics warn it could disproportionately harm students pursuing careers in lower-paying fields like education or social work.

A comparative analysis of these bills reveals differing philosophies on how to address the student debt crisis. Targeted forgiveness programs like the Frontline Heroes Act emphasize recognition and relief for specific groups, while broader reforms like the Fresh Start Act focus on systemic barriers to repayment. Meanwhile, the REAL Reforms Act reflects a more conservative approach, prioritizing fiscal responsibility over expansive relief. Borrowers navigating these changes should monitor legislative progress and consult resources like the Federal Student Aid website to understand how new policies may affect their eligibility for forgiveness.

Practical tips for borrowers include staying informed about pending legislation, maintaining accurate records of employment and payments (especially for PSLF candidates), and exploring alternative repayment plans like income-driven options. Additionally, borrowers in default should act promptly to take advantage of programs like the Fresh Start initiative, as these opportunities may be time-sensitive. As the legislative landscape evolves, proactive engagement with available resources will be key to maximizing forgiveness benefits.

Biden Student Loan Forgiveness: Step-by-Step Application Guide for Borrowers

You may want to see also

Frequently asked questions

As of the latest updates, there are no widespread extensions to student loan forgiveness programs beyond what has already been announced. However, targeted relief for specific groups (e.g., public service workers or those defrauded by schools) may still be available.

The student loan payment pause has been extended multiple times, but there is no guarantee of further extensions. Borrowers should prepare to resume payments unless an official announcement is made.

While there are ongoing discussions about expanding eligibility, no new broad-scale expansions have been confirmed. Borrowers should stay informed through official channels for updates.

The one-time $10,000 to $20,000 forgiveness plan was blocked by the Supreme Court in 2023. As of now, there are no plans to reinstate it, but other targeted relief programs may still be available.