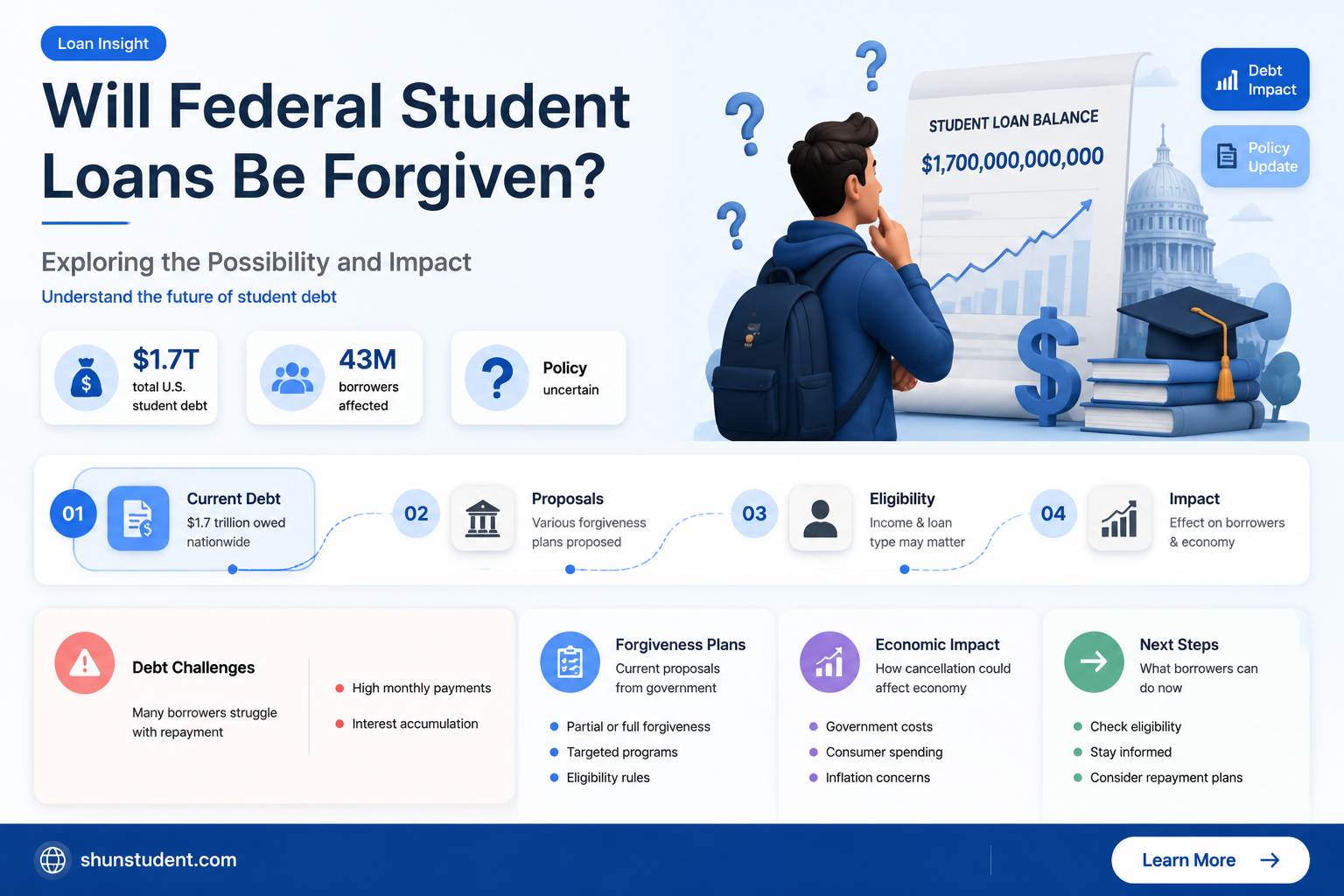

The question of whether the federal government will forgive student loans has become a pressing issue, sparking widespread debate and anticipation among millions of borrowers. With the burden of student debt reaching unprecedented levels, many are looking to policymakers for relief, especially in light of recent economic challenges and campaign promises. While there have been proposals and executive actions aimed at partial forgiveness or debt cancellation, the specifics remain uncertain, leaving borrowers in a state of limbo. Advocates argue that widespread forgiveness could stimulate the economy and alleviate financial strain, while critics raise concerns about fairness and long-term fiscal implications. As the discussion continues, the fate of federal student loan forgiveness remains a pivotal topic with far-reaching consequences for individuals and the nation as a whole.

| Characteristics | Values |

|---|---|

| Current Status | No widespread federal student loan forgiveness beyond existing programs. |

| Biden Administration Plan | One-time forgiveness of up to $20,000 (Pell Grant recipients) and $10,000 (others) blocked by Supreme Court in June 2023. |

| Supreme Court Ruling | Struck down Biden’s forgiveness plan as unconstitutional (June 2023). |

| Income-Driven Repayment (IDR) Reforms | New IDR plan (Saving on a Valuable Education, or SAVE) reduces payments and shortens forgiveness timelines. |

| Public Service Loan Forgiveness (PSLF) | Enhanced PSLF program continues, offering forgiveness after 10 years of qualifying payments. |

| Loan Payment Restart | Payments resumed in October 2023 after COVID-19 pause. |

| Pending Legislation | No active bills in Congress for broad forgiveness as of October 2023. |

| Debt Cancellation for Specific Groups | Targeted forgiveness for defrauded borrowers (e.g., ITT Tech, Corinthian Colleges) and disabled borrowers. |

| Interest Capitalization | Interest not capitalized during administrative forbearance periods. |

| Future Outlook | Unlikely for broad forgiveness without new legislation or executive action. |

Explore related products

What You'll Learn

![]()

Biden's loan forgiveness plan updates

As of the latest updates, President Biden's student loan forgiveness plan has been a subject of intense scrutiny and legal challenges. The initial proposal aimed to cancel up to $20,000 in federal student loan debt for Pell Grant recipients and up to $10,000 for other eligible borrowers, with an income cap of $125,000 for individuals and $250,000 for married couples. This plan was designed to provide relief to millions of Americans burdened by student debt, but its implementation has been far from straightforward.

Analytical Perspective: The Supreme Court’s June 2023 ruling struck down Biden’s original forgiveness plan, citing that the administration overstepped its authority under the HEROES Act. This decision halted progress and left borrowers in limbo. However, the Biden administration has since pivoted to pursuing debt cancellation through the Higher Education Act’s negotiated rulemaking process. This alternative route involves a longer, more complex procedure but could potentially withstand legal challenges. The Department of Education has been holding public hearings and gathering input to reshape the forgiveness criteria, focusing on targeted relief for specific groups, such as those with low balances or long-term repayment histories.

Instructive Approach: For borrowers awaiting updates, it’s crucial to stay informed through official channels like the Federal Student Aid website. While broad-scale forgiveness remains uncertain, other relief options are available. For instance, the Saving on a Valuable Education (SAVE) repayment plan, launched in 2023, caps monthly payments at a lower percentage of discretionary income and forgives remaining balances after 10 years for borrowers with original loan amounts of $12,000 or less. Additionally, public service loan forgiveness (PSLF) and income-driven repayment (IDR) programs offer pathways to debt cancellation for eligible borrowers.

Comparative Analysis: Biden’s plan contrasts sharply with previous administrations’ approaches. While Obama and Trump expanded income-driven repayment plans and temporary relief measures, Biden’s initiative sought to address systemic debt through direct cancellation. However, the legal and political hurdles highlight the challenges of implementing such sweeping reforms. Compared to other countries, such as Germany or Norway, where higher education is tuition-free or heavily subsidized, the U.S. system relies heavily on student loans, making forgiveness a contentious issue tied to broader debates about education funding and economic equity.

Descriptive Insight: The human impact of these updates cannot be overstated. For many borrowers, the promise of forgiveness represented a lifeline, offering the chance to buy homes, start families, or pursue careers without the crushing weight of debt. The uncertainty has caused widespread anxiety, with some pausing major life decisions until the situation clarifies. Advocacy groups continue to push for comprehensive solutions, while critics argue that forgiveness unfairly burdens taxpayers. As the Biden administration navigates this complex landscape, borrowers remain in a state of flux, balancing hope with pragmatism.

Practical Tips: While waiting for further developments, borrowers should take proactive steps to manage their debt. First, ensure your contact information is up to date with your loan servicer to receive important updates. Second, explore eligibility for existing forgiveness programs like PSLF or IDR. Third, consider refinancing private loans if interest rates are favorable, though this won’t affect federal loans. Finally, avoid scams by verifying all communications through official government websites. Staying informed and prepared will position you to act swiftly once new policies are finalized.

Church Employment and Student Loan Forgiveness: What You Need to Know

You may want to see also

Explore related products

![]()

Eligibility criteria for loan forgiveness

Federal student loan forgiveness isn’t automatic—it hinges on meeting strict eligibility criteria. The most prominent program, Public Service Loan Forgiveness (PSLF), requires 120 qualifying payments while working full-time for a government or nonprofit organization. Payments must be made under an income-driven repayment plan, and the loan type must be Direct. For example, a teacher working in a low-income school district could qualify after 10 years of consistent payments, but a private school teacher would not, as their employer doesn’t meet the nonprofit criteria.

Another pathway, income-driven repayment (IDR) forgiveness, applies after 20–25 years of payments, depending on the plan. Borrowers with lower incomes relative to their debt benefit most, as payments are capped at a percentage of discretionary income. For instance, someone earning $40,000 annually with $100,000 in loans might pay as little as $200 monthly under the Revised Pay As You Earn (REPAYE) plan, leading to forgiveness after 25 years. However, forgiven amounts may be taxed as income, so planning for this liability is crucial.

Temporary relief measures, like the COVID-19 payment pause, sometimes count toward forgiveness without requiring payments. For example, the pause from March 2020 to September 2023 was treated as qualifying payments for PSLF and IDR forgiveness. Borrowers should review their payment counts post-pause to ensure accuracy, as administrative errors are common.

Lastly, targeted forgiveness programs exist for specific professions or circumstances. For instance, the Teacher Loan Forgiveness program offers up to $17,500 for educators in low-income schools after five consecutive years. Similarly, the Nurse Corps Loan Repayment Program forgives 60% of loans for registered nurses working in underserved areas. These programs require separate applications and proof of eligibility, such as employment verification and certification.

Understanding these criteria is essential, as misinformation abounds. Borrowers should consult official resources like the Federal Student Aid website and document every payment and employer certification. While forgiveness is possible, it demands patience, precision, and proactive management of loan terms.

Discover Jobs That Qualify for Student Loan Forgiveness Programs

You may want to see also

Explore related products

![]()

Impact on borrowers' credit scores

Federal student loan forgiveness, if implemented, could significantly impact borrowers' credit scores, but the effects aren’t uniform. For borrowers in default or delinquency, forgiveness would remove a major negative mark from their credit reports, potentially boosting scores by 50 to 100 points within months. This is because defaulted loans weigh heavily on credit utilization and payment history, two factors that comprise 65% of a FICO score. However, borrowers with loans in good standing might see minimal changes, as their accounts reflect consistent, on-time payments—a positive behavior that forgiveness wouldn’t alter.

Consider the mechanics of credit reporting. When a loan is forgiven, it’s typically marked as "paid as agreed" or "settled," rather than "paid in full." While this is better than a default, it may not carry the same weight as a fully paid account. For instance, a borrower with a $30,000 loan in good standing might see their credit score dip slightly if the account closes, as it reduces their credit mix and average age of accounts. Conversely, a borrower with multiple late payments could see a dramatic improvement, as the removal of negative history outweighs the loss of a positive account.

A critical caution: forgiveness isn’t instantaneous. During the processing period, which could last 6 to 12 months, borrowers’ accounts may show as "in administrative review," creating uncertainty for lenders. This could temporarily lower creditworthiness, especially for those seeking mortgages or auto loans. To mitigate this, borrowers should monitor their credit reports via AnnualCreditReport.com and dispute inaccuracies promptly. Additionally, maintaining low credit card balances (below 30% of the limit) during this period can stabilize scores.

For younger borrowers (ages 22–30), forgiveness could free up income for credit-building activities, such as securing a credit card with a low limit and paying it off monthly. Older borrowers (ages 40–55) might prioritize refinancing high-interest debt, as their improved debt-to-income ratio post-forgiveness could qualify them for better terms. Practical tip: request a "goodwill adjustment" from creditors to remove minor delinquencies post-forgiveness, further enhancing your credit profile.

In summary, the impact of federal student loan forgiveness on credit scores depends on the borrower’s current standing. Defaulted borrowers stand to gain the most, while those in good standing should focus on preserving their credit mix and history. Proactive monitoring and strategic financial planning can maximize the benefits of forgiveness, turning it into a springboard for long-term credit health.

Obama Loan Forgiveness: Did Students Receive Reimbursement?

You may want to see also

Explore related products

![]()

Legal challenges to forgiveness programs

Legal challenges to federal student loan forgiveness programs have emerged as a significant hurdle, threatening to derail initiatives aimed at alleviating the $1.7 trillion debt burden carried by 43 million Americans. These challenges often center on questions of executive authority, statutory interpretation, and constitutional standing, creating a complex web of litigation that borrowers, policymakers, and advocates must navigate. For instance, the Biden administration’s 2022 plan to forgive up to $20,000 in student debt per borrower faced immediate lawsuits from Republican-led states and conservative groups, who argued the administration overstepped its authority under the Higher Education Relief Opportunities for Students (HEROES) Act. This act, designed to provide relief during national emergencies, became the legal cornerstone of the forgiveness plan—and its Achilles’ heel in court.

Analyzing the legal arguments reveals a clash between executive discretion and legislative intent. Opponents contend that the HEROES Act does not grant the Department of Education the power to cancel debt en masse, but rather to modify loan terms during emergencies. Proponents counter that the COVID-19 pandemic justified broad action to address financial hardship. The Supreme Court’s 2023 ruling in *Biden v. Nebraska* struck down the forgiveness plan, holding that the HEROES Act did not authorize such sweeping debt cancellation. This decision underscores the importance of statutory clarity and the limits of executive action, leaving future forgiveness efforts vulnerable to similar challenges unless Congress explicitly authorizes such programs.

For borrowers seeking relief, understanding these legal nuances is critical. While the Supreme Court’s ruling halted the Biden administration’s plan, other forgiveness programs, such as Public Service Loan Forgiveness (PSLF) and income-driven repayment (IDR) plans, remain intact. However, these programs are not immune to legal scrutiny. For example, PSLF has faced lawsuits over administrative errors and inconsistent eligibility determinations, highlighting the need for robust implementation and transparency. Borrowers should document their eligibility, track payments, and stay informed about program updates to protect themselves from potential legal pitfalls.

Comparatively, state-level forgiveness programs offer an alternative but come with their own legal risks. States like New York and California have launched initiatives to assist residents, but these programs could face preemption challenges if they conflict with federal law. Additionally, funding for such programs often relies on state budgets, which are subject to political and economic fluctuations. Borrowers considering state-based relief should research eligibility criteria, application deadlines, and the program’s legal standing to ensure they qualify and avoid unexpected setbacks.

In conclusion, legal challenges to federal student loan forgiveness programs demand a proactive approach from borrowers and policymakers alike. While the Supreme Court’s ruling closed one avenue of relief, it also highlighted the need for legislative solutions that withstand judicial scrutiny. Borrowers should explore existing programs, stay informed about legal developments, and advocate for comprehensive reforms. Policymakers, meanwhile, must craft forgiveness initiatives with clear statutory authority and robust administrative safeguards to minimize legal risks and maximize impact. The path to debt relief is fraught with legal obstacles, but with strategic action, meaningful progress remains possible.

Biden's Student Loan Forgiveness Plan: What Borrowers Need to Know

You may want to see also

Explore related products

![]()

Long-term effects on education costs

The prospect of federal student loan forgiveness has sparked debates about its long-term impact on education costs. While immediate relief for borrowers is a central focus, the ripple effects on tuition pricing, institutional behavior, and societal perceptions of higher education merit closer examination. Forgiving existing debt could inadvertently create a moral hazard, signaling to colleges and universities that unchecked tuition increases will eventually be subsidized by taxpayers. This dynamic risks perpetuating the very cycle of debt accumulation that forgiveness aims to address.

Consider the behavioral economics at play: if institutions anticipate future bailouts, they may feel less pressure to control costs or innovate in affordability. For instance, between 1980 and 2020, average tuition at public four-year colleges rose 211%, outpacing inflation by over 100%. Without structural reforms tied to forgiveness, such as caps on tuition increases or funding tied to graduation rates, this trend could accelerate. A comparative analysis of countries like Germany, where tuition is free or low-cost, reveals that direct investment in institutions—not debt forgiveness—is key to curbing long-term education costs.

From a policy standpoint, forgiveness without accountability measures risks shifting the financial burden from individual borrowers to taxpayers, while failing to address root causes. A more instructive approach would be to pair forgiveness with reforms like income-share agreements or increased funding for community colleges, which offer lower-cost pathways to degrees. For example, expanding Pell Grants or creating state-level tuition-free programs could reduce reliance on loans, thereby mitigating future debt accumulation. Such strategies address both immediate relief and systemic affordability.

The psychological and cultural impacts of widespread forgiveness also warrant attention. If students perceive higher education as a risk-free investment due to potential future bailouts, they may be less price-sensitive when choosing institutions. This could embolden colleges to further inflate costs, particularly in prestigious or high-demand fields. A persuasive argument here is that forgiveness must be coupled with transparency initiatives, such as requiring colleges to publish clear data on post-graduation earnings and debt-to-income ratios, empowering students to make cost-conscious decisions.

Ultimately, the long-term effects of federal student loan forgiveness on education costs hinge on whether it is implemented as a standalone measure or as part of a broader strategy to reform higher education financing. Without addressing the underlying drivers of tuition inflation, forgiveness risks becoming a temporary band-aid rather than a sustainable solution. Policymakers must balance relief for current borrowers with structural changes that incentivize affordability, ensuring that future generations are not saddled with the same burdens. The takeaway is clear: forgiveness alone is insufficient; it must be a catalyst for systemic change.

Illinois Tax Rules: Are Forgiven Student Loans Taxable?

You may want to see also

Frequently asked questions

As of now, there is no plan to forgive all federal student loans. However, targeted forgiveness programs exist for specific groups, such as public service workers or those with qualifying disabilities.

Future forgiveness depends on legislative and policy changes. Proposals for broader forgiveness are often debated, but nothing is guaranteed without congressional approval and presidential support.

Eligibility varies by program. Examples include Public Service Loan Forgiveness (PSLF), Teacher Loan Forgiveness, and Total and Permanent Disability Discharge. Borrowers must meet specific criteria to qualify.