Many parents who have taken out loans to support their children's education often wonder if there are any student loan forgiveness options available to them. While most forgiveness programs are designed for the students themselves, parents who borrowed through federal programs like Parent PLUS loans may have limited options. These can include income-contingent repayment (ICR) plans, which can lead to loan forgiveness after 25 years of qualifying payments, or public service loan forgiveness (PSLF) if the parent works in an eligible public service job. However, it’s crucial for parents to explore these options carefully, as eligibility requirements can be strict, and forgiveness may come with tax implications. Understanding these programs can help parents manage their financial burden more effectively.

Explore related products

What You'll Learn

![]()

Federal Parent PLUS Loan Forgiveness Programs

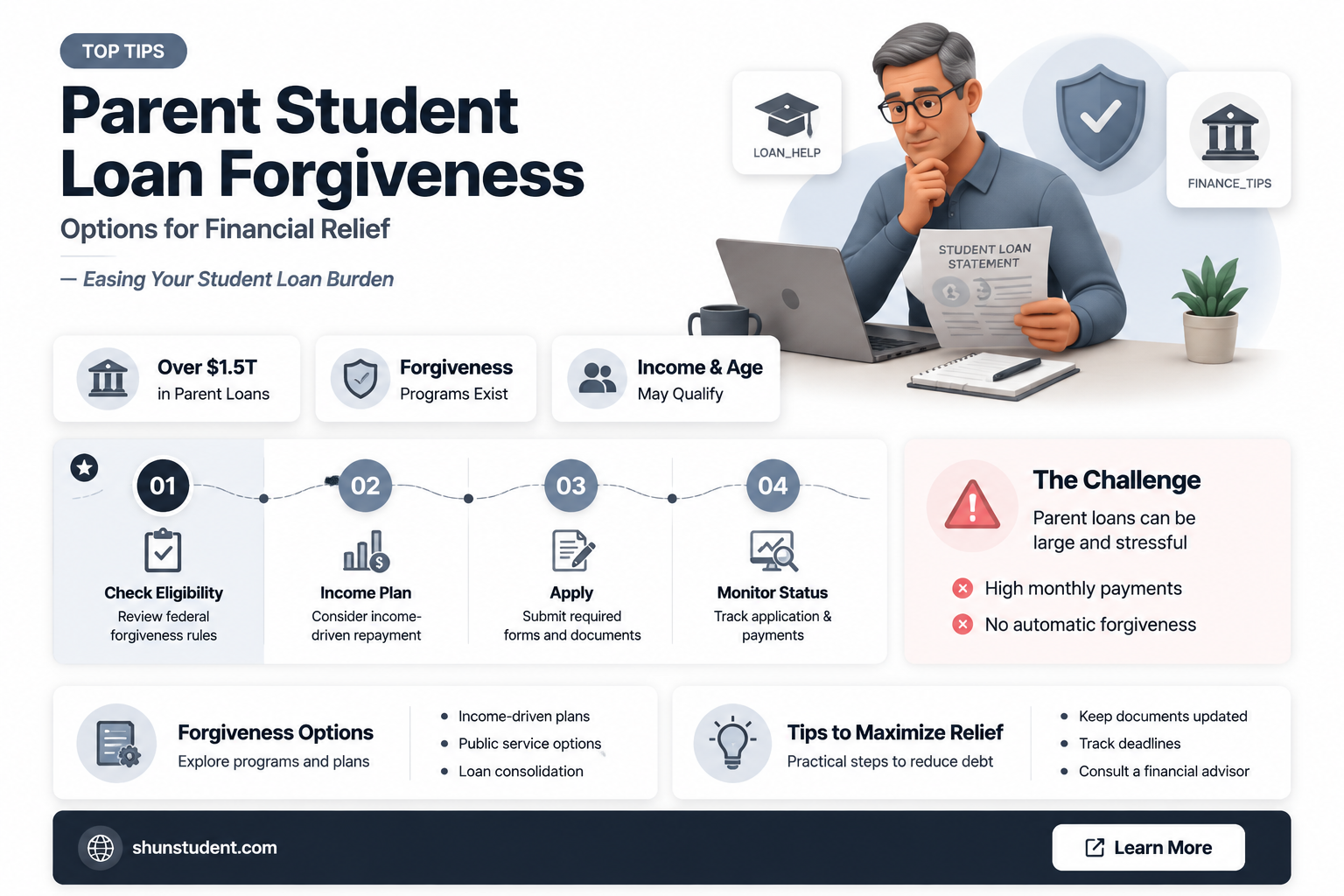

Parents who took out Federal Parent PLUS Loans to support their child's education often find themselves seeking relief from the burden of repayment. While Parent PLUS Loans are not eligible for many of the forgiveness programs available to students, there are still pathways to debt relief that parents can explore. One of the most viable options is consolidating Parent PLUS Loans into a Direct Consolidation Loan, which opens the door to income-driven repayment (IDR) plans. These plans, such as Income-Contingent Repayment (ICR), can lower monthly payments based on income and family size, and after 25 years of qualifying payments, any remaining balance may be forgiven.

To qualify for ICR, parents must first consolidate their Parent PLUS Loans into a Direct Consolidation Loan through the federal government. This process is straightforward and can be completed online via the Federal Student Aid website. Once consolidated, parents can apply for ICR, which calculates payments as 20% of their discretionary income or the amount they would pay on a fixed payment plan over 12 years, adjusted for income, whichever is less. It’s crucial to recertify income and family size annually to ensure payments remain affordable and to maintain eligibility for forgiveness after 25 years.

Another option for Parent PLUS Loan forgiveness is through Public Service Loan Forgiveness (PSLF), but with a significant caveat. Parents themselves cannot qualify for PSLF unless they work full-time for a qualifying employer, such as a government or nonprofit organization. However, if the student for whom the loan was taken out later consolidates the Parent PLUS Loan into their own Direct Consolidation Loan and pursues PSLF, the parent’s loan could be forgiven after 10 years of qualifying payments. This strategy requires careful coordination between parent and child and is less common but worth considering for families in public service.

For parents nearing retirement, understanding the interplay between Parent PLUS Loans and Social Security benefits is essential. If payments are not maintained, loans can go into default, potentially leading to wage garnishment or Social Security offsets. However, under ICR, payments are capped based on income, reducing the risk of default. Parents should also be aware that forgiven amounts under ICR may be considered taxable income, though current tax laws provide temporary relief through 2025, exempting forgiven student loan balances from taxation.

In summary, while Parent PLUS Loans are not eligible for many forgiveness programs, strategic use of consolidation and income-driven repayment plans can provide a path to relief. Parents should act proactively by consolidating loans, enrolling in ICR, and staying informed about tax implications. For those in public service or with children pursuing PSLF, exploring indirect forgiveness options may also yield results. Navigating these programs requires diligence, but the potential for reduced payments or eventual forgiveness makes the effort worthwhile.

Disability Student Loan Forgiveness: A Step-by-Step Application Guide

You may want to see also

Explore related products

![]()

Income-Driven Repayment Plans for Parents

Parents who have taken out federal student loans to support their child's education often face the challenge of managing repayment while balancing other financial responsibilities. Income-Driven Repayment (IDR) plans offer a viable solution by adjusting monthly payments based on income and family size, potentially leading to loan forgiveness after a set period. These plans are particularly beneficial for parents with limited income or those seeking long-term financial stability.

Understanding the Mechanics of IDR Plans

IDR plans calculate monthly payments as a percentage of discretionary income, typically 10-20%, depending on the specific plan. For parents, this means payments are tailored to their current financial situation, not the total loan balance. For example, if a parent earns $50,000 annually and has a family of four, their discretionary income is adjusted downward, resulting in lower monthly payments. This flexibility is crucial for parents juggling mortgage payments, childcare costs, and other expenses.

Eligibility and Application Process

To qualify for an IDR plan, parents must have eligible federal loans, such as Direct Loans or Federal Family Education Loans (FFEL) consolidated into a Direct Consolidation Loan. The application process involves submitting income documentation and family size details through the Federal Student Aid website. Parents should carefully review the four IDR options—Income-Based Repayment (IBR), Pay As You Earn (PAYE), Revised Pay As You Earn (REPAYE), and Income-Contingent Repayment (ICR)—to determine which best aligns with their financial goals.

Long-Term Benefits and Forgiveness

One of the most appealing aspects of IDR plans for parents is the potential for loan forgiveness. After 20-25 years of qualifying payments, any remaining balance is forgiven, though this may be considered taxable income. For instance, a parent on the REPAYE plan could see forgiveness after 20 years if all loans were for undergraduate study. However, parents must remain diligent in recertifying their income and family size annually to avoid payment increases or loss of benefits.

Practical Tips for Maximizing IDR Benefits

Parents can optimize their IDR experience by keeping detailed records of income and family size changes, as these factors directly impact payment amounts. Additionally, exploring Public Service Loan Forgiveness (PSLF) in conjunction with IDR can expedite forgiveness for parents working in eligible public service roles. Regularly reviewing loan servicer communications and staying informed about policy changes can also help parents navigate the complexities of these plans effectively.

In summary, Income-Driven Repayment plans provide parents with a manageable path to student loan repayment, offering both immediate relief and long-term forgiveness opportunities. By understanding the mechanics, eligibility criteria, and practical strategies, parents can make informed decisions to alleviate financial stress and secure a stable future.

Obama's Student Loan Forgiveness for Disabled Veterans: Fact or Fiction?

You may want to see also

Explore related products

![]()

Public Service Loan Forgiveness Eligibility

Parents burdened with federal student loans taken out for their children’s education often overlook the Public Service Loan Forgiveness (PSLF) program as a viable option. This program, designed to reward borrowers who commit to public service careers, can also benefit parents who work in qualifying sectors. To be eligible, the borrower—not the child—must be employed full-time by a government or nonprofit organization. This means a parent working as a teacher, nurse, or social worker, for example, could qualify, even if the loans were taken out under the Parent PLUS Loan program. The key is the parent’s employment, not the purpose of the loan.

Qualifying for PSLF requires more than just public service employment. Borrowers must make 120 eligible payments while working full-time for a qualifying employer. These payments must be made under an income-driven repayment plan, which adjusts monthly payments based on income and family size. For parents, this can be particularly advantageous, as income-driven plans often result in lower monthly payments compared to standard plans. Additionally, payments must be made on time and in full to count toward the 120 required. Tracking these payments is crucial, as errors in payment counts are common and can delay forgiveness.

One critical but often misunderstood aspect of PSLF eligibility is the type of loan required. Parent PLUS Loans, which many parents use to fund their children’s education, are eligible for PSLF but must be consolidated into a Direct Consolidation Loan to qualify. This step is non-negotiable, as only Direct Loans are eligible for the program. Consolidation can also simplify repayment by combining multiple loans into one, making it easier to manage. However, parents must be cautious: consolidating resets the payment count, meaning previous payments no longer count toward the 120 required for forgiveness.

For parents considering PSLF, proactive planning is essential. Start by confirming employer eligibility using the PSLF Help Tool provided by the U.S. Department of Education. Next, switch to an income-driven repayment plan if not already enrolled. Submit the Employment Certification Form annually to ensure payments are tracked correctly. Finally, stay informed about program updates, as PSLF has undergone significant changes in recent years, including temporary waivers that may benefit older borrowers. While the process is detailed, the potential to eliminate thousands of dollars in debt makes PSLF a worthwhile pursuit for eligible parents.

Is $10,000 Student Loan Forgiveness a Realistic Possibility?

You may want to see also

Explore related products

![]()

State-Based Forgiveness Options for Parents

While federal student loan forgiveness programs often dominate the conversation, parents burdened by student loan debt shouldn't overlook the potential relief offered by state-based initiatives. These programs, though less publicized, can provide targeted assistance based on residency, occupation, and financial need.

Understanding the landscape of state-based forgiveness requires a proactive approach. Researching your specific state's Department of Education website is crucial. Many states offer loan repayment assistance programs (LRAPs) designed to attract and retain professionals in high-demand fields like healthcare, education, and public service. For instance, the California State Loan Repayment Program provides up to $50,000 in loan repayment for eligible healthcare professionals serving in underserved areas.

Eligibility criteria for state-based forgiveness programs vary widely. Some programs target recent graduates, while others cater to experienced professionals. Income thresholds, service commitments, and specific loan types are common factors considered. For example, the New York State Young Farmers Loan Forgiveness Incentive Program offers up to $10,000 annually for five years to eligible farmers under 62 years old.

Beyond profession-specific programs, some states offer broader initiatives. Minnesota's Office of Higher Education administers the Loan Forgiveness for Public Service Employees program, providing up to $6,000 annually for qualifying individuals working in government, non-profit, or public service sectors.

Is Public Student Loan Forgiveness Worth It? Pros, Cons, and Eligibility

You may want to see also

Explore related products

![]()

Loan Discharge Due to Disability or Death

In the realm of student loan forgiveness, one critical yet often overlooked option is the discharge of loans due to disability or death. This provision offers a lifeline to parents who have taken on the burden of their child’s education through Parent PLUS loans or other federal student loans. If the student or the parent borrower becomes permanently disabled or passes away, the loan may be discharged entirely, relieving the family of this financial obligation. This option is not just a legal technicality but a compassionate measure designed to prevent undue hardship during already challenging times.

To qualify for a disability discharge, the borrower must provide documentation proving a total and permanent disability. This typically involves a physician’s certification or evidence of eligibility for Social Security Disability Insurance (SSDI). For Parent PLUS loans, if the parent borrower dies, the loan is automatically discharged, regardless of the student’s financial situation. Similarly, if the student for whom the loan was taken passes away, the loan is forgiven. This process requires submitting a death certificate to the loan servicer, but it can significantly ease the financial strain on grieving families.

While the discharge process may seem straightforward, it’s essential to navigate it carefully. For disability discharges, borrowers must avoid defaulting on their loans during the application period, as this can complicate the process. Additionally, some disability discharges may have tax implications, as the forgiven amount could be considered taxable income, though exceptions apply under the American Rescue Plan Act through 2025. Parents should consult a tax professional to understand their specific situation.

Comparatively, this forgiveness option stands out for its accessibility and immediacy. Unlike income-driven repayment plans or public service loan forgiveness, which require years of qualifying payments, disability or death discharges provide immediate relief. However, it’s a last-resort measure tied to unfortunate circumstances, not a proactive strategy for loan management. Parents should explore other forgiveness options first but keep this provision in mind as a safety net.

In practice, parents should proactively inform themselves about this option and keep necessary documentation organized. For instance, if a parent or student has a chronic illness, it’s wise to familiarize oneself with the disability discharge process in advance. Similarly, ensuring that loan servicers have updated contact information can expedite the discharge process in the event of a borrower’s death. While no one plans for tragedy, being informed can make a significant difference in managing the financial aftermath.

Are Argosy Student Loans Forgiven? Understanding Your Options and Relief

You may want to see also

Frequently asked questions

Yes, parents who took out Federal Direct PLUS Loans may qualify for Public Service Loan Forgiveness (PSLF) if they work full-time for a qualifying employer, such as a government or nonprofit organization, and make 120 eligible payments.

Yes, parents with Federal Direct PLUS Loans can consolidate them into a Direct Consolidation Loan and then enroll in an income-driven repayment plan. After 20–25 years of qualifying payments, the remaining balance may be forgiven, though taxes may apply on the forgiven amount.

Yes, parents with federal student loans, including PLUS Loans, may qualify for Total and Permanent Disability (TPD) Discharge if they meet the eligibility criteria, which includes providing documentation of their disability.

Yes, if a parent took out a Federal Direct PLUS Loan for their child and the child passes away, the parent may qualify for loan discharge through the death discharge program.

Some states offer loan repayment assistance programs (LRAPs) for parents or borrowers who meet specific criteria, such as working in certain professions (e.g., healthcare, education) or living in designated areas. Check your state’s higher education agency for available options.