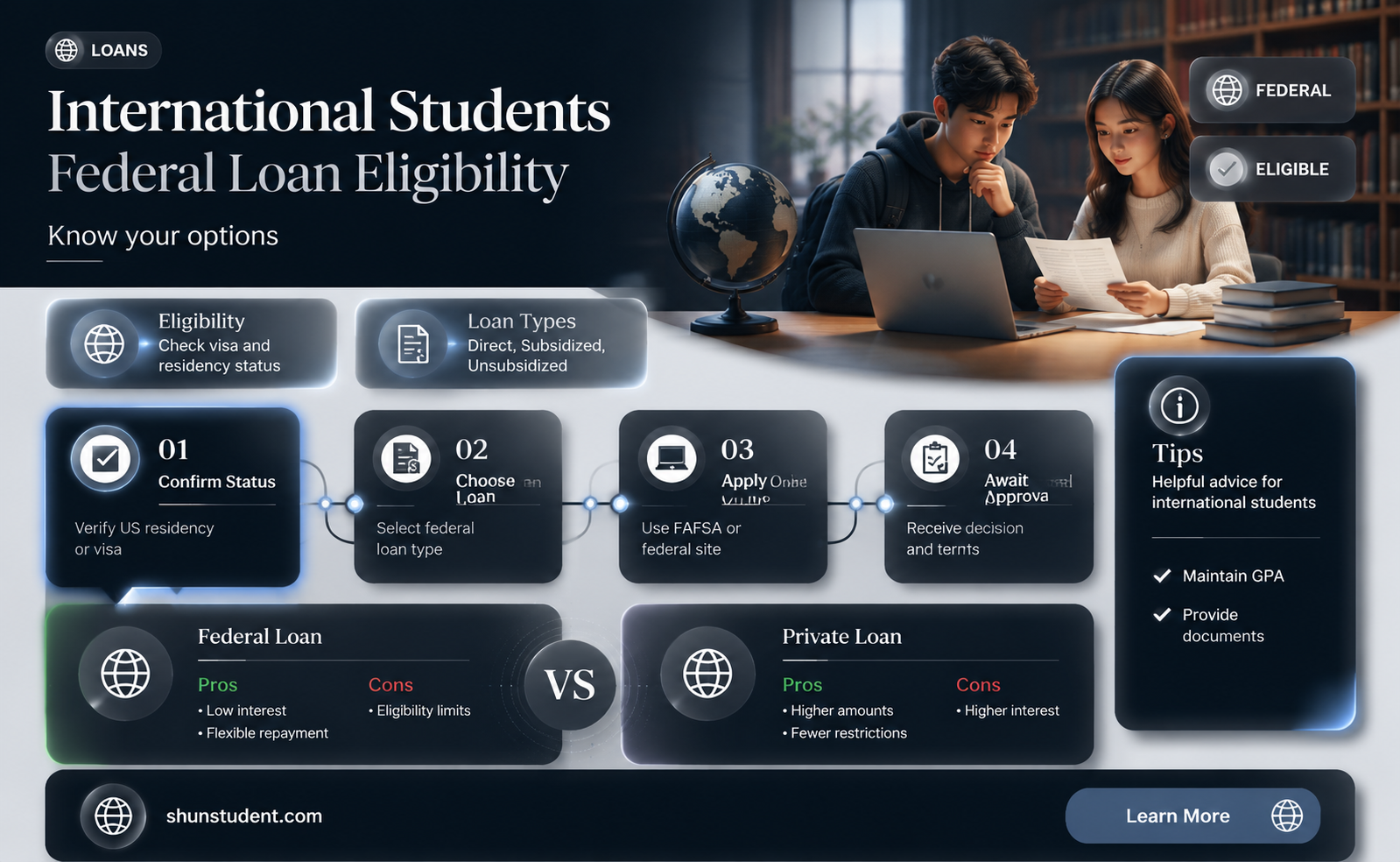

International students studying in the United States often face additional costs, such as visa application fees and international airfare, on top of the usual expenses like tuition, housing, and books. While international students are not eligible for federal student loans or state aid, there are other financial aid options available to them. These include private student loans, grants, scholarships, and merit-based aid. Many private student loans require a cosigner, typically a US citizen with good credit, and have variable interest rates calculated based on an index and other factors determined by the lender.

| Characteristics | Values |

|---|---|

| Federal student loans availability | Not available to international students |

| Federal financial aid | Not available to international students |

| FAFSA | Not available to international students |

| Private student loans | Available to international students |

| International student loans | Available to international students |

| MPOWER Financing | Available to international students |

| No-cosigner loans | Available to international students |

| Variable rate loans | Available to international students |

| Repayment period | 10-25 years |

| Repayment plan options | Full Deferral, Interest Only |

Explore related products

What You'll Learn

![]()

International students and federal student loans

International students studying in the United States cannot access federal student loans or federal financial aid. To qualify for federal student loans, you must be a US citizen, permanent resident, or eligible noncitizen. However, international students can explore other options to fund their education.

Private Student Loans

International students can apply for private student loans, which are specifically designed for those studying in the US. These loans can cover the full cost of attendance, including tuition, living expenses, and other fees. Private lenders often require a cosigner who is a US citizen or permanent resident with good credit. However, some lenders, such as MPOWER Financing, offer loans without a cosigner, with reasonable interest rates and flexible repayment plans.

Scholarships and Grants

International students may qualify for institutional scholarships and grants, as well as merit-based aid offered by their college or university. For example, Howard University offers Freshman Scholarships for international students in their first year. Additionally, students can explore external scholarships and grants, such as those offered by organisations or private foundations.

Work-Study Programs

Although international students generally cannot work while studying in the US, some universities offer work-study programs as part of their financial aid packages. These programs allow students to work on campus to help cover their educational expenses.

Other Options

International students can also consider other sources of funding, such as family funds or personal savings. Additionally, some colleges and universities may have their own financial aid applications specifically for international students, such as the International Student Application for Financial Assistance (ISAFA). It is important to carefully research and evaluate the costs of studying in the US and explore all available options to secure the necessary financial aid.

Studying Abroad: Are Americans International Students in Europe?

You may want to see also

Explore related products

![]()

Private student loans for international students

International students are not eligible for federal student loans in the US. However, they can apply for private student loans. Private student loans are available to international students to help cover costs while studying at college in the US. These costs can include tuition, books, transportation, and living expenses.

International students can use loan comparison tools to find eligible loan options and choose the one that best suits their needs. After selecting their citizenship and school, a list of lenders that will work for them will be provided. The loan comparison tool will also help them understand the different terms and conditions offered by each lender.

International students usually need a cosigner with a good credit score because they do not have a credit history in the US. The cosigner can be a parent or any other person who can legally sign loan papers or documentation to help the student obtain a loan.

The interest rate on variable rate loans is calculated based on an "index" plus a margin that will add an additional percentage depending on the cosigner's creditworthiness or other factors decided by the lender. The two most common indexes used for international student loans are the Prime Rate and the Secured Overnight Financing Rate (SOFR). SOFR is determined by the federal funds rate set by the US Federal Reserve, which is the rate at which banks lend to each other.

Repayment terms depend on the lender and loan option chosen. This is an important feature of a loan since most international students cannot work while studying in the US. Therefore, it is crucial to consider how much the monthly payments will be, when payments will begin, and how long repayment can be deferred. The repayment period typically ranges from 10 to 25 years.

Before taking out a private student loan, international students should explore other financial aid options. They can start by researching funding opportunities from their country's embassy or governmental educational office to see if there are applicable scholarships. They can also use the US Department of Labor's scholarship search engine to identify scholarships, fellowships, grants, and financial aid awards. Additionally, they should check with their college to see if they offer financial aid for international students and consider finding an advising center to help navigate the financial aid process.

The Wealth of Chinese International Students

You may want to see also

Explore related products

![]()

Interest rates and repayment plans

International students are not eligible for federal student loans from the US government. However, they can apply for international student loans from private lenders. The interest rates and repayment plans for these loans can vary depending on the lender and loan option chosen.

When taking out a private loan, international students often need a co-signer who is a US citizen or permanent resident with good credit. The interest rate on the loan is calculated based on a benchmark rate, such as the Prime Rate or the Secured Overnight Financing Rate (SOFR), plus an additional percentage determined by the creditworthiness of the borrower or co-signer. The SOFR is based on transactions in the Treasury repurchase market, where banks and investors lend and borrow funds overnight. It is considered more reliable and accurate than the previous benchmark, LIBOR, as it does not rely on estimates or surveys.

Repayment terms for international student loans can range from 10 to 25 years, with the larger the loan, the longer the repayment period. There are typically a few standard repayment plan options available, including full deferral and interest-only plans. With full deferral, students can defer payments until six months after graduation, for a maximum of four years. Under an interest-only plan, students make interest payments while in school and then defer repayment of the principal until 45 days after graduation or when they drop below full-time status.

It is important for international students to carefully evaluate the cost of studying in the US and consider all available options for financing their education, including scholarships, financial aid from the school, and family funds, before taking on private loans.

Free Community College for International Students in San Francisco?

You may want to see also

Explore related products

![]()

Scholarships, grants, and institutional loans

International students are not eligible for federal student loans or federal financial aid. However, they can apply for scholarships, grants, and institutional loans.

Scholarships

There are several scholarships available for international students, which are often merit-based and highly competitive. Scholarships are usually awarded based on special skills, talents, or abilities. For example, scholarships may be based on TOEFL scores, academic records, artistic ability, musical ability, or athletic ability.

Some specific scholarships for international students include:

- The Aga Khan Foundation International Scholarship, which provides scholarships to students from select developing countries with no other source of financial help for graduate studies.

- The American Association of University Women offers fellowships for non-American women pursuing a Master's or doctorate in the USA, with priority given to those committed to the advancement of women and girls.

- The Civil Society Leadership Awards offer full scholarships for Master's students from specific countries dedicated to fostering social change.

- The Joint Japan/World Bank Graduate Scholarship Program provides comprehensive financial coverage, including tuition, a monthly stipend, airfare, health insurance, and travel allowance, to students from developing countries applying for a development-related Master's program.

- MPOWER Financing offers scholarships for international and DACA students through its Global Citizen Scholarship Program.

- The P.E.O. International Peace Scholarship awards scholarships to women from other countries earning graduate degrees in the USA.

Grants

Grants are another option for international students seeking financial assistance. Grants are typically need-based, and some grants are specifically for international students. International students can find grants through online databases such as IEFA and International Student, which offer comprehensive listings of grants and scholarships for international students.

Institutional Loans

Institutional loans are also an option for international students. These loans are offered by the university or college and are usually reserved for graduate studies in the form of assistantships and fellowships. Private student loans are also available to international students, but it is important to carefully research and compare the rates and terms offered by various lenders.

Additionally, international students can take out private loans from a variety of organizations and institutions, although many financial aid experts advise against taking on too much debt. These loans often require a cosigner, who guarantees repayment if the student is unable to pay back the loan. The repayment period for international student loans typically ranges from 10 to 25 years, and students should carefully consider the monthly payments and when repayment will begin.

International Students: Higher Acceptance Rates?

You may want to see also

Explore related products

![]()

Work visas and work-study programs

International students are not eligible for federal student loans or federal financial aid in the US. However, they can apply for private student loans, which are available to non-US citizens studying in the country. International students can also avail of merit-based aid, scholarships, and work-study programs to help fund their education.

Work Visas

The US offers several types of visas for international students, the most common being the F-1 and M-1 visas. F-1 visas are for full-time international students pursuing academic studies, while M-1 visas are for those in vocational or non-academic programs. F-1 visa holders may not work off-campus during their first academic year but may accept on-campus employment. After the first year, F-1 students may engage in three types of off-campus employment: Curricular Practical Training (CPT), Optional Practical Training (OPT), and the Science, Technology, Engineering, and Mathematics (STEM) OPT Extension. CPT and OPT allow international students to gain work experience during and after their studies.

The J-1 exchange visitor visa is another option for international students. This visa is for those participating in work-and-study-based exchange programs, such as visiting scholars, camp counselors, au pairs, and research assistants. J-1 visa holders must contact their responsible officer to determine their eligibility for work outside their program of study.

Work-Study Programs

Work-study programs provide part-time employment opportunities for students to help fund their education. While international students are generally not eligible for federal work-study programs, they may be able to participate in institutional work-study programs offered by their college or university. These programs typically involve on-campus jobs that are often related to a student's course of study.

It is important to note that work opportunities for international students in the US may be limited, and there are specific requirements and restrictions that must be followed. International students should carefully review the guidelines for their visa type and consult with their school's international office to understand their options for working and studying in the US.

International Students: Your Path to Canadian PR

You may want to see also

Frequently asked questions

No, international students cannot qualify for federal student loans or state aid. However, they can apply for international student loans, which are private loans.

International student loans require a cosigner who is a permanent US resident with good credit. The cosigner is often a close friend or relative who can assist in getting credit. The loan can be used for education-related expenses such as tuition, books, fees, insurance, and room and board.

The interest rate for international student loans is calculated based on an "index" plus a margin that depends on the creditworthiness of the cosigner. The two most common indexes used are the Prime Rate and the Secured Overnight Financing Rate (SOFR).

Repayment terms depend on the lender and loan option chosen. Since most international students cannot work while studying in the US, it is important to consider how much the monthly payments will be and when payments will begin. The repayment period typically ranges from 10-25 years, with various repayment plan options available.