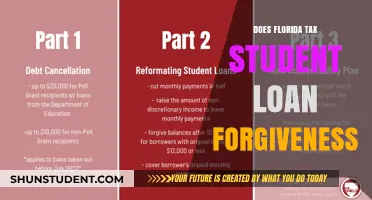

Georgia's tax treatment of student loan forgiveness is a critical concern for borrowers in the state, as it directly impacts the financial benefits of debt relief programs. While the federal government typically considers forgiven student loans as taxable income, Georgia's approach aligns with federal tax laws, meaning that forgiven amounts may be subject to state income tax unless specific exemptions apply. However, under the American Rescue Plan Act of 2021, forgiven student loans are exempt from federal taxation through 2025, and Georgia follows this exemption, ensuring borrowers are not taxed at the state level during this period. Borrowers should remain vigilant for any changes in legislation that could affect this tax treatment in the future.

| Characteristics | Values |

|---|---|

| State | Georgia |

| Taxation of Student Loan Forgiveness | Yes |

| Tax Year | 2023 and later |

| Federal Tax Treatment | Tax-free under the American Rescue Plan Act (ARPA) through 2025 |

| Georgia's Stance | Georgia does not conform to the federal exclusion, thus considers forgiven student loans as taxable income |

| Applicable Loans | Federal and private student loans |

| Forgiveness Programs Affected | Public Service Loan Forgiveness (PSLF), Teacher Loan Forgiveness, Income-Driven Repayment (IDR) forgiveness, etc. |

| Potential Tax Liability | Varies based on the amount forgiven and the taxpayer's income bracket |

| State Legislation | No current legislation to exclude student loan forgiveness from state taxation |

| Advocacy Efforts | Ongoing efforts by advocacy groups to push for state-level exclusion |

| Last Updated | October 2023 |

Explore related products

What You'll Learn

![]()

Federal vs. State Tax Laws

The tax treatment of student loan forgiveness varies significantly between federal and state laws, creating a complex landscape for borrowers. Federally, the American Rescue Plan Act of 2021 exempts forgiven student loan debt from federal income tax through 2025, offering substantial relief to borrowers. However, this federal exemption does not automatically apply to state taxes, leaving the decision to individual states. Georgia, like many others, has its own tax code that may diverge from federal guidelines, potentially subjecting forgiven student loans to state taxation.

Georgia’s tax laws do not explicitly mirror the federal exemption for student loan forgiveness. While federal law provides a clear break, Georgia’s treatment of forgiven debt depends on how it aligns with federal taxable income. If forgiven student loans are excluded from federal taxable income, Georgia typically follows suit, as the state uses federal adjusted gross income (AGI) as the starting point for state tax calculations. However, this alignment is not guaranteed, especially if Georgia’s tax code has not been updated to reflect federal changes. Borrowers must verify current state regulations to avoid unexpected tax liabilities.

To navigate this discrepancy, borrowers should take proactive steps. First, consult IRS Publication 970 and Georgia’s Department of Revenue guidelines to understand the latest rules. Second, consider working with a tax professional who specializes in state and federal tax laws to ensure compliance. Third, keep detailed records of loan forgiveness documentation, as Georgia may require proof that the forgiven amount qualifies for exclusion under state law. Ignoring these steps could result in underpayment penalties or audits.

The contrast between federal and state tax laws highlights the importance of understanding jurisdictional differences. While federal exemptions offer broad relief, state taxes can erode those savings if not managed carefully. Georgia’s approach underscores the need for borrowers to stay informed and plan strategically. By leveraging federal protections and adhering to state-specific rules, borrowers can maximize their financial benefits and minimize tax burdens.

Federal Employees and Student Loan Forgiveness: What You Need to Know

You may want to see also

Explore related products

![]()

Georgia’s Tax Exemption Rules

Georgia's tax exemption rules for student loan forgiveness are a critical consideration for borrowers navigating the financial aftermath of debt relief. Unlike the federal government, which made student loan forgiveness tax-free through the American Rescue Plan Act of 2021, Georgia’s stance is less straightforward. The state conforms to the federal tax code in many areas but has not explicitly adopted the federal exclusion for forgiven student loans. This means borrowers in Georgia may face state tax liability on forgiven amounts, depending on the type of loan and forgiveness program. For instance, Public Service Loan Forgiveness (PSLF) recipients could owe Georgia state taxes on the forgiven balance, as the state has not carved out an exception for this program.

To mitigate potential tax burdens, Georgia residents should scrutinize the source of their loan forgiveness. Certain programs, like those tied to income-driven repayment plans, may trigger taxable income under state law. Borrowers can proactively consult a tax professional to explore strategies such as adjusting withholdings or setting aside funds to cover potential tax obligations. Additionally, tracking legislative updates is essential, as Georgia’s tax laws could evolve in response to federal changes or advocacy efforts.

A comparative analysis reveals disparities between Georgia and states like Pennsylvania or Virginia, which have explicitly aligned with federal tax-free treatment for student loan forgiveness. This highlights the importance of state-specific research for borrowers. For example, while federal forgiveness under the Biden administration’s initiatives remains tax-free nationwide, Georgia’s lack of conformity creates a unique financial planning challenge. Borrowers must account for this discrepancy when calculating their net financial benefit from loan forgiveness.

Practical tips for Georgia residents include monitoring annual tax forms for changes related to student loan forgiveness and leveraging available deductions or credits to offset potential liabilities. For instance, the Georgia Student Scholarship Credit allows taxpayers to claim credits for contributions to qualified scholarship-granting organizations, which could indirectly ease the tax burden. Additionally, borrowers nearing forgiveness should request a tax estimate from their loan servicer to prepare for any state tax implications. By staying informed and proactive, Georgia residents can navigate the intersection of student loan forgiveness and state taxation with greater clarity and confidence.

COVID Relief Bill: Does It Include Student Loan Forgiveness?

You may want to see also

Explore related products

![]()

PSLF Tax Treatment in Georgia

Georgia residents benefiting from the Public Service Loan Forgiveness (PSLF) program face a critical question: will their forgiven debt be taxed at the state level? Unlike the federal government, which excludes PSLF forgiveness from taxable income, Georgia historically treated such forgiveness as taxable. However, recent legislative changes have shifted this landscape. As of 2023, Georgia aligns with federal tax treatment for PSLF, meaning forgiven amounts are no longer considered taxable income for state purposes. This change reflects a growing trend among states to mirror federal tax exclusions for student loan forgiveness programs.

Understanding the mechanics of this tax treatment is essential for Georgia residents. PSLF forgives the remaining balance on eligible federal student loans after 120 qualifying payments while working full-time for a qualifying public service employer. Prior to 2023, Georgia’s tax code required recipients to report forgiven amounts as income, increasing their state tax liability. Now, borrowers can exclude up to $75,000 in forgiven debt from their Georgia taxable income, provided it qualifies under federal PSLF guidelines. This exclusion applies retroactively to forgiveness granted on or after January 1, 2021, allowing some borrowers to amend previous returns for potential refunds.

For those navigating this change, practical steps can maximize benefits. First, ensure your PSLF eligibility by submitting an Employment Certification Form annually and using the Department of Education’s PSLF Help Tool. Second, keep detailed records of loan payments and employer certifications, as these may be required for tax documentation. Third, consult a tax professional to confirm your eligibility for the state exclusion and to explore additional deductions or credits. For example, educators with forgiven loans may also qualify for Georgia’s Educator Expense Deduction, further reducing taxable income.

A comparative analysis highlights Georgia’s progressive stance relative to other states. While some states, like California and New York, have long aligned with federal PSLF tax treatment, others continue to tax forgiven amounts. Georgia’s recent shift not only eases financial burdens for public servants but also positions the state as more attractive for professionals in education, healthcare, and government sectors. This alignment with federal policy simplifies tax compliance and reduces confusion for borrowers, particularly those with multi-state tax obligations.

In conclusion, Georgia’s updated PSLF tax treatment marks a significant win for public service workers. By eliminating state taxes on forgiven student loans, the state acknowledges the value of public service and reduces financial barriers to career entry. Borrowers should stay informed about potential legislative changes and leverage available resources to optimize their tax outcomes. As student loan forgiveness programs evolve, Georgia’s approach serves as a model for balancing fiscal responsibility with support for essential public sector workers.

USPS Employees: Unlocking Student Loan Forgiveness Opportunities and Benefits

You may want to see also

Explore related products

![]()

State Conformity to Federal Codes

Georgia's approach to taxing student loan forgiveness hinges on its conformity to federal tax codes, a critical yet often overlooked aspect of state tax policy. When the federal government forgives student loans, it typically treats the forgiven amount as taxable income. However, recent federal legislation, such as the American Rescue Plan Act of 2021, has temporarily excluded forgiven student loans from taxable income through 2025. Georgia, like many states, conforms to federal tax laws, meaning it generally adopts federal definitions of taxable income. This conformity simplifies tax compliance for residents but also means that changes in federal tax treatment of student loan forgiveness directly impact Georgia taxpayers.

To understand the practical implications, consider a Georgia resident whose $50,000 student loan is forgiven under a federal program. Under federal law, this amount would not be taxed through 2025 due to the exclusion. Because Georgia conforms to federal tax codes, this forgiven amount would also be excluded from Georgia state income tax during the same period. However, if federal law changes after 2025 and begins taxing forgiven student loans again, Georgia taxpayers would likely face state tax liability unless the state legislature explicitly decouples from the federal change.

Decoupling from federal tax codes is a strategic option for states seeking to diverge from federal tax policy. For instance, if Georgia decided to decouple from the federal exclusion, forgiven student loans could become taxable at the state level even if they remain tax-free federally. This scenario would create additional complexity for taxpayers and potentially increase their state tax burden. However, decoupling could also allow Georgia to retain more tax revenue, which might be used to fund other state priorities, such as education or infrastructure.

For taxpayers, understanding Georgia’s conformity to federal codes is essential for accurate tax planning. If you anticipate student loan forgiveness, monitor both federal and state tax laws, especially as the 2025 expiration of the federal exclusion approaches. Consult a tax professional to assess your specific situation, particularly if you have forgiven loans exceeding $20,000, as higher amounts can significantly impact your tax liability. Additionally, stay informed about Georgia’s legislative actions regarding tax conformity, as changes could occur in response to federal updates or state fiscal needs.

In conclusion, Georgia’s conformity to federal tax codes plays a pivotal role in determining whether forgiven student loans are taxed at the state level. While current federal exclusions provide temporary relief, taxpayers must remain vigilant about potential changes. By understanding the interplay between federal and state tax laws, Georgia residents can better navigate their tax obligations and plan for future financial scenarios.

Student Loan Forgiveness: How Close Are We to Relief?

You may want to see also

Explore related products

$32.98 $44.99

![H&R Block Tax Software Deluxe + State 2025 Win/Mac [PC/Mac Online Code]](https://m.media-amazon.com/images/I/611uM-FzipL._AC_UY218_.jpg)

![TurboTax Desktop Deluxe 2025, Federal & State Tax Return [PC/Mac Download]](https://m.media-amazon.com/images/I/71uOJaU7UvL._AC_UY218_.jpg)

![]()

Impact of Loan Discharge Types

Student loan forgiveness programs offer a lifeline to borrowers, but the tax implications vary widely depending on the type of discharge. In Georgia, understanding these differences is crucial for financial planning. For instance, Public Service Loan Forgiveness (PSLF) is generally tax-free at the federal level, but Georgia’s stance on this remains a critical consideration for residents. Conversely, income-driven repayment (IDR) forgiveness after 20 or 25 years of payments is federally taxable, and Georgia’s treatment of this income could significantly impact the borrower’s tax liability. This distinction highlights the need to scrutinize discharge types before assuming tax-free relief.

Consider disability discharge, another common form of loan forgiveness. Federally, this discharge is tax-exempt, but Georgia’s alignment with federal rules isn’t automatic. Borrowers must verify whether the state mirrors federal tax treatment or imposes additional obligations. Similarly, death discharge—where loans are forgiven upon the borrower’s death—is federally tax-free, but Georgia’s handling of this scenario requires clarification. These nuances underscore the importance of consulting a tax professional to avoid unexpected liabilities.

Bankruptcy discharge, though rare for student loans, presents a unique case. If successful, the forgiven amount is federally taxable, and Georgia’s tax code would likely follow suit. However, the complexity of qualifying for bankruptcy discharge often outweighs the tax consequences. Borrowers should weigh the long-term financial impact, including potential credit damage, against the immediate tax burden. This discharge type serves as a reminder that not all forgiveness programs offer equal benefits.

Practical steps can mitigate the tax impact of certain discharge types. For federally taxable forgiveness, such as IDR, Georgia residents can explore state-specific deductions or credits to offset the burden. Additionally, timing plays a role; borrowers nearing the end of an IDR plan might delay forgiveness until a year with lower income to reduce the tax bracket. Proactive planning, such as setting aside funds for anticipated tax liabilities, can prevent financial strain.

In conclusion, the impact of loan discharge types on Georgia residents extends beyond the forgiveness itself. Each program carries distinct tax implications, requiring careful analysis to maximize benefits. By understanding these differences and taking strategic steps, borrowers can navigate the complexities of student loan forgiveness with greater financial clarity.

Police Departments and Student Loan Forgiveness: What You Need to Know

You may want to see also

Frequently asked questions

Yes, Georgia currently taxes student loan forgiveness as income, as it follows federal tax guidelines.

As of now, there are no specific exceptions in Georgia law for taxing forgiven student loans, though federal exceptions may apply.

Georgia treats federally forgiven student loans, including those under PSLF, as taxable income unless federal law excludes them.

Georgia has not explicitly adopted the federal exclusion for student loan forgiveness under the American Rescue Plan, so it may still be taxed.

No, Georgia does not allow a deduction for taxes paid on forgiven student loans, as it aligns with federal taxable income calculations.

![H&R Block Tax Software Premium 2025 Win/Mac [PC/Mac Online Code]](https://m.media-amazon.com/images/I/51dMIAMHkkL._AC_UY218_.jpg)

![H&R Block Tax Software Deluxe 2025 Win/Mac [PC/Mac Online Code]](https://m.media-amazon.com/images/I/51Mlng5FWYL._AC_UY218_.jpg)

![TurboTax Desktop Premier 2025, Federal & State Tax Return [PC/Mac Download]](https://m.media-amazon.com/images/I/71RgxnEm-tL._AC_UY218_.jpg)

![TurboTax Desktop Deluxe 2025, Federal Tax Return [PC/Mac Download]](https://m.media-amazon.com/images/I/71zRbfw0RdL._AC_UY218_.jpg)

![TurboTax Desktop Home & Business 2025, Federal & State Tax Return [PC/Mac Download]](https://m.media-amazon.com/images/I/71KOcfYElCL._AC_UY218_.jpg)

![H&R Block Tax Software Premium & Business 2025 Win [PC Online code]](https://m.media-amazon.com/images/I/618kxmZlTGL._AC_UY218_.jpg)

![TurboTax Desktop Business 2025, Federal Tax Return [PC Download]](https://m.media-amazon.com/images/I/71UL+5xLOeL._AC_UY218_.jpg)

![(Old Version) H&R Block Tax Software Deluxe + State 2024 with Refund Bonus Offer (Amazon Exclusive) Win/Mac [PC/Mac Online Code]](https://m.media-amazon.com/images/I/51+fonAXhPL._AC_UY218_.jpg)

![[OLD VERSION] TurboTax Deluxe 2024 Tax Software, Federal & State Tax Return [PC/MAC Download]](https://m.media-amazon.com/images/I/71UbHaUeeUL._AC_UY218_.jpg)