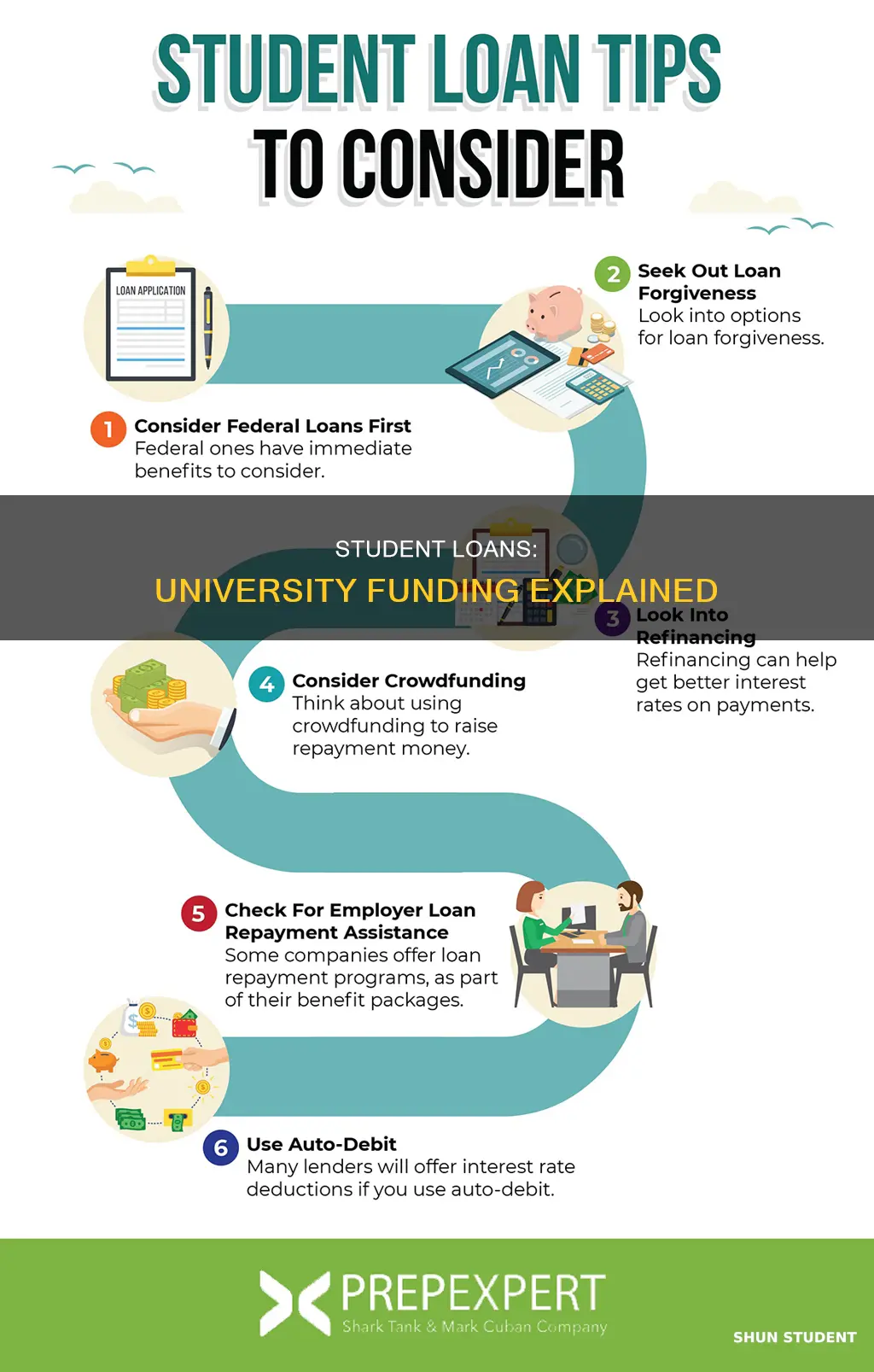

There are a variety of ways that students can receive loans for university, with options varying depending on location. In the United States, federal student loans are offered by the government, and are generally the most affordable option. Private student loans are also available, but these accrue interest immediately and are therefore likely to be more expensive. Some colleges offer their own loans, and scholarships and grants are also available. International students are eligible for most scholarships and aid, and may also qualify for state funding.

| Characteristics | Values |

|---|---|

| Type of loan | Federal or private |

| Federal loan eligibility | Determined by filing the FAFSA |

| Federal loan advantages | Less expensive, more borrower protections, possibility of loan forgiveness |

| Private loan providers | Banks or finance companies |

| Private loan advantages | No origination fees, lower interest rates than certain federal loans |

| Institutional loans | Offered by colleges and universities using funds from their resources, alumni, corporations, foundations, donors, and loan repayments |

| Institutional loan eligibility | Determined by each college, may be available regardless of federal financial aid eligibility |

| International students | Eligible for scholarships and aid from colleges, may qualify for state funding, eligible for private loans with a US-based co-signer |

| Interest rates | Lower for borrowers who bank with the lender, higher for private loans |

| Income share agreements | Alternative to traditional loans, borrower repays a percentage of their salary to the institution |

Explore related products

What You'll Learn

![]()

Federal student loans

There are a few different types of federal student loans available:

- Federal Direct Subsidized Loans: These are need-based loans for undergraduate students. The amount that can be borrowed is determined by the total cost of college and the family's ability to pay, as determined by the Free Application for Federal Student Aid (FAFSA). One of the benefits of subsidized loans is that the government pays the interest on the loan while the student is still enrolled in school.

- Federal Direct Unsubsidized Loans: These loans are available to undergraduate and graduate students and are not based on financial need. While a FAFSA application is required, the amount that can be borrowed is determined by the cost of attendance and other financial aid received. Interest is charged during all periods and may be capitalized, which can increase the total loan cost.

- Direct PLUS Loans: These are unsubsidized loans for parents of dependent students and graduate/professional students. PLUS loans can help pay for education expenses up to the cost of attendance after other financial aid is exhausted. Eligibility is not based on financial need but a credit check is required, and borrowers with an adverse credit history must meet additional requirements. Interest is charged during all periods and may be capitalized, which can increase the total loan cost.

Jewish Student Population at University of Richmond

You may want to see also

Explore related products

![]()

Private student loans

There are several private loan options available, and students must research which option is best for them. It is important to understand the annual and cumulative loan limits, interest rates, fees, and loan terms. Private loans may be available to students regardless of their federal financial aid eligibility.

Some private colleges offer interest-free loans to students from specific geographic regions. These loans are often subsidized by the college and can be repaid over a longer period, sometimes up to 10 years. Repayment may also be deferred during periods of graduate study or post-graduate employment.

When applying for a private student loan, a student's creditworthiness is evaluated, along with the credit of any cosigners. A cosigner with good credit may increase the chances of loan approval and may help secure a better interest rate.

There are a variety of private lenders offering student loans, such as Sallie Mae, Citizens Student Loan, and College Ave Student Loans. These lenders provide different repayment options and may cover up to 100% of school-certified costs. It is recommended to compare multiple lenders and their loan options to find the best fit.

Enrolment Figures for Fisk University: An Overview

You may want to see also

Explore related products

![]()

Direct loans

In the United States, there are two types of lenders providing international student loans: banks and lending companies. Borrowing from a bank offers the convenience of having your banking and student loans in one place. Non-bank lenders may offer international students more flexibility.

Federal Direct Loans are low-interest loans from the US Department of Education for students enrolled at least half-time and are administered by universities like Catholic University. There are two types of Federal Direct Loans: subsidized and unsubsidized. The primary difference between the two loans is the point at which interest begins to accrue. Interest on subsidized loans is paid by the federal government while the student is enrolled. Interest on unsubsidized loans begins to accrue at the time of disbursement. The federal government sets limits on the amount of money a student can borrow.

Many colleges and universities offer their own loans to help students and families pay for college. Institutional loan funds typically come from the college's resources, alumni, corporations, foundations, donors and repayments from prior college loan borrowers. For example, several private colleges in Southern California offer interest-free loans to high school graduates from a specific geographic region of the state. Recipients of such funds are determined by each college campus and are given up to 10 years to repay the amount borrowed.

To receive federal student loans, all borrowers should complete an Annual Student Loan Acknowledgment at studentaid.gov. This will become an annual requirement. It is recommended that you complete an Annual Student Loan Acknowledgment each year you accept a new federal student loan. Your Federal Direct Loan will not disburse to your student account unless you complete all the steps.

University of New Hampshire: Student Population Insights

You may want to see also

Explore related products

![]()

Institutional loans

Universities and colleges can provide financial aid to students in the form of institutional loans. These are a type of private student loan distributed by the college or school the student is enrolled in. Institutional loans are non-federal financial aid and do not have the same benefits as federal student loans. They are serviced by the school or a third-party lender and are only offered to enrolled students.

However, institutional loans do not qualify for federal loan benefits, so borrowers cannot get their loans forgiven or choose an income-driven repayment plan. They may also require a credit check, which could be challenging for some students. It is important to understand the repayment details and terms provided by your school before taking out an institutional loan.

Students can also explore other options for financial aid, such as scholarships, grants, fellowships, and work-study programs. Additionally, some employers offer tuition assistance programs or student loan repayment benefits. Prioritizing these options can help minimize the amount borrowed and the overall debt post-graduation.

Fresno State University: Enrollment Figures and Trends

You may want to see also

Explore related products

![]()

Scholarships and grants

Scholarships, grants, and student loans are the three most common types of financial aid for students. Scholarships and grants are similar in that they are both gifts that do not need to be repaid, whereas student loans are borrowed money that must be repaid over time.

Scholarships are usually merit-based awards offered for academic achievements, athletic or other abilities, or excellence in a specific field. Many scholarship programs have specific qualifications that students must meet, including standards based on academic performance, talents, and academic or social merit. Some scholarships are also need-based or criteria-specific, meaning they are awarded to students from specific countries or cultural backgrounds, or restricted to a particular discipline. Many scholarships come with specific conditions, such as maintaining a certain GPA or committing to continue studying in a particular field.

Grants are typically need-based awards provided by governments, universities, colleges, or non-profits to students in financial need or those belonging to specific backgrounds. Grants can also be project-based, provided for a particular academic project or research. Students who receive grants may be required to fulfil certain obligations, such as submitting periodic research progress reports. Like scholarships, grants are non-repayable funds, but they are limited in funding, so it is important to apply early to increase the chances of receiving a grant.

Funding University as a Mature Student

You may want to see also

Frequently asked questions

There are federal loans and private student loans. Federal loans are either subsidised (the government pays the interest) or unsubsidised. Private student loans are offered by banks or finance companies.

Federal loans are less expensive and usually come with more borrower protections. There is also the possibility that some of the loans can be forgiven, meaning you don't have to repay them if you work in certain professions.

Federal loan eligibility is determined by filing the FAFSA.

An income share agreement is an alternative to a traditional loan. The borrower agrees to pay a percentage of their salary to the educational institution after graduation.

Many colleges and universities offer their own loans to help students and families pay for college. Institutional loan funds typically come from the college's resources, alumni, corporations, foundations, donors and repayments from prior college loan borrowers.