University student loans are a way for students to borrow money to help pay for university or college tuition fees and living costs. Student loans can include a tuition fee loan and a maintenance loan. Tuition fee loans are paid directly to the course provider to cover the cost of tuition fees, while maintenance loans are paid to the student to help with living costs such as accommodation, food, and books. The amount of money a student can borrow depends on various factors, including their household income, where they study, and where they live. Students are usually required to repay their loans after they finish their studies and start earning above a certain income threshold. The repayment amount is based on the graduate's salary, with interest rates varying depending on the income level.

| Characteristics | Values |

|---|---|

| Who issues the loans? | Student Loans Company |

| Who are the loans for? | All full-time undergraduate students |

| What are the prerequisites? | Residency, UK national or settled status, living in the UK, Channel Islands, or Isle of Man for three years before the course begins |

| What is the maximum tuition fee loan amount? | £9,250 per year |

| What is the maximum maintenance loan amount? | £11,672 per year (for students living away from home in London) |

| When do repayments start? | The April after you finish your course and are earning over a certain amount |

| How much do you repay? | Depends on your salary, not the amount borrowed; repayments vary with your salary and stop if your income drops too low |

| What is the interest rate? | 4.3% for Student Loans on Plans 1, 4 and 5; 5.4% for the 2019/2020 academic year |

| Can you pay back early? | Yes, you can pay off the loan in a lump sum without any charges |

| What if you can't get a student loan? | You can rely on your salary, savings, family support, or other sources of finance to cover the costs |

| Are there alternatives to student loans? | Yes, scholarships, bursaries, and grants are available from universities, charities, businesses, etc. |

Explore related products

![]()

Tuition fee loans

The amount you can borrow as a tuition fee loan varies depending on your location. In England, you can borrow up to £9,250 per year, while in Wales, it is £9,000, and in Northern Ireland, it is £4,160. If you are studying in Scotland and are from Scotland or the EU, you do not have to pay tuition fees.

Repayments for tuition fee loans typically begin after you complete your course and are based on your income. You will only start making repayments once you are earning above a certain level, and the amount you pay back is a percentage of your income. The interest rate on tuition fee loans is also linked to your income, with a higher interest rate for those earning more. It's important to note that any loan not repaid after a certain period, typically 30 years, is usually wiped off.

Transferring to Seoul National University: Is It Possible?

You may want to see also

Explore related products

![]()

Maintenance loans

The amount of maintenance loan you can receive depends on several factors, including where you are living and your family's income. For instance, students living away from home in London receive more due to higher living costs. Similarly, students from lower-income backgrounds are generally eligible for more financial support. In England, 35% of the maintenance loan is means-tested, so those with higher family incomes may receive a smaller loan. The maximum maintenance loan amount for the 2019/2020 academic year was £8,944 for students living away from home outside of London and £11,672 for those living in London.

Like tuition fee loans, maintenance loans must be repaid after completing the course. However, repayments are income-dependent, and you will only start repaying your student loans once you earn above a certain threshold. In the UK, as of April 2019, repayments begin when income exceeds £25,725 per year, and the interest rate for student loans is currently 4.3% on Plans 1, 4, and 5.

Denver University's Student Population: A Comprehensive Overview

You may want to see also

Explore related products

![]()

Interest rates

Federal student loans have fixed interest rates, which means the rate remains constant for the loan's duration. The federal government sets these rates annually, based on the 10-year Treasury note rate. For instance, the federal student loan interest rate for undergraduates is 6.53% for the 2024-25 school year. Federal loans also have an interest cap, preventing rates from rising above a certain level.

Private student loans, on the other hand, may offer fixed or variable interest rates. Variable rates can change periodically, typically monthly, quarterly, or annually. Private lenders usually base their variable rates on a base rate and the SOFR rate set by banks. Fixed rates for private loans are often determined using a similar formula, but they can also be influenced by an applicant's credit score. Generally, higher credit scores lead to lower interest rates for private loans. The average private student loan interest rate falls between 4% and 16%.

It's worth noting that interest on student loans may start accruing immediately or after a grace period, depending on the loan type. Federal Direct subsidized loans, for example, do not accrue interest while the borrower is in school or during a six-month grace period after graduation. In contrast, private loans may start accruing interest as soon as the loan is disbursed.

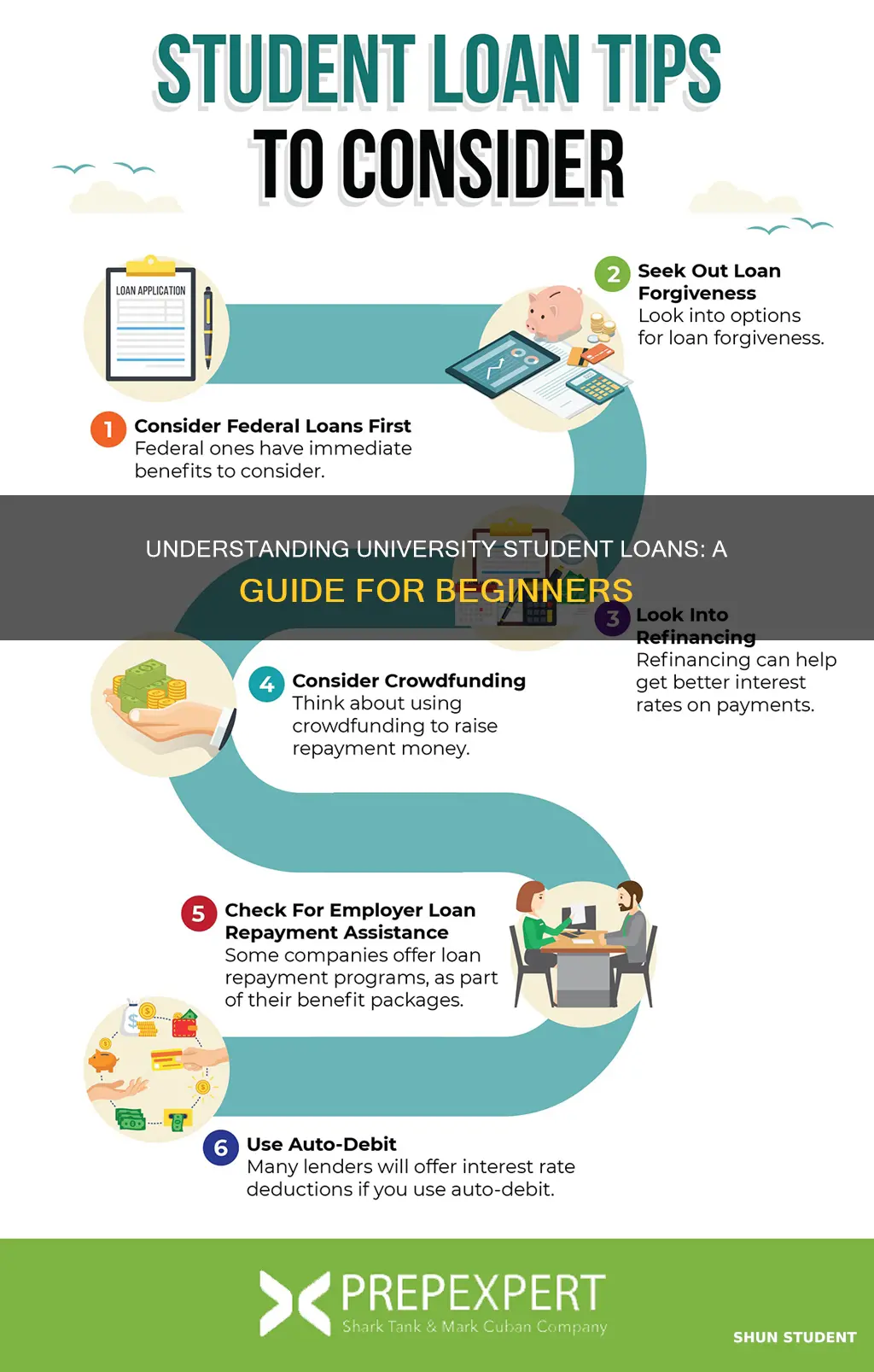

Borrowers can take steps to lower their student loan interest rates. One option is to sign up for automatic payments, which can reduce the rate by a small percentage for both federal and private loans. Additionally, borrowers can consider refinancing their loans with a new lender to obtain a lower interest rate, although this may result in losing certain benefits associated with federal loans. Improving one's credit score is another way to increase the chances of securing a lower interest rate, especially for private loans.

Lesley University: Need-Based Aid for International Students?

You may want to see also

Explore related products

![]()

Repayments

The interest rate on student loans is currently set at 4.3% for Plans 1, 4 and 5. Interest rates are updated annually in September, using the Retail Price Index (RPI) rate from March as a reference. For instance, the RPI rate in March 2019 was 2.4%, so the interest charged on student loans for the 2019/2020 academic year was 5.4%. While studying, or if earning below £21,000, the interest paid is the same as the RPI rate. The interest rate gradually increases once graduates begin to earn more. For every £1,000 earned over £21,000, the interest rate rises by 0.15%. Once a graduate is earning over £41,000, the interest rate is set at RPI plus 3%, which is the maximum rate.

Full Scholarship Students: Dormitory Fees at Sabancı University

You may want to see also

Explore related products

$16.53 $22.99

![]()

Alternative funding

There are a number of ways to fund your university education without taking out student loans.

Firstly, scholarships are a great alternative as they don't need to be repaid and there's no interest to worry about. Scholarships can be merit-based, need-based, recurring, or one-time awards. You can apply for as many scholarships as you want, and they can be found from a variety of sources, including federal and state governments, universities, private organizations, and local businesses.

Grants are another option for funding your education, and like scholarships, they typically don't need to be repaid. Grants are usually need-based and are offered by federal and state governments, universities, colleges, and some non-profit organizations. To qualify, you'll need to provide documentation of your financial need.

If you're studying part-time or full-time, you may be able to work for the university in exchange for a percentage-based tuition discount. This can help reduce your need for student loans and cover living expenses.

Additionally, you could consider taking up a part-time job to earn money for your education. This option provides more income-earning potential compared to working for the university, but be sure to balance your work and academic commitments to avoid feeling overwhelmed.

Finally, if you're seeking funding for postgraduate studies, you can register for the Alternative Guide to Postgraduate Funding, which offers a database of funding opportunities and guidance on grant applications. Charities, foundations, and trusts are also alternative funding sources for postgraduate research, offering studentships, scholarships, bursaries, and more.

Explore the Student Population at Texas A&M University

You may want to see also

Frequently asked questions

A student loan is a sum of money borrowed to pay for university or college tuition fees and living costs.

The amount you can borrow depends on your household income, where you live, and where you study. For example, in the 2019/2020 academic year, the maximum maintenance loan was £8,944 if you lived away from home and £7,529 if you lived at home.

You'll start repaying your student loan once you finish your course and are earning over a certain amount. In the UK, as of April 2019, you'll start repaying your loan if you earn more than £25,725 a year.

Your monthly repayments will depend on how much you earn, not how much you owe. The more you earn, the more interest you will pay.

Yes, you can pay your loan off in one lump sum if you want to. However, many experts recommend against this as the amount of interest you pay on a student loan is often less than the interest you can gain from a savings account.