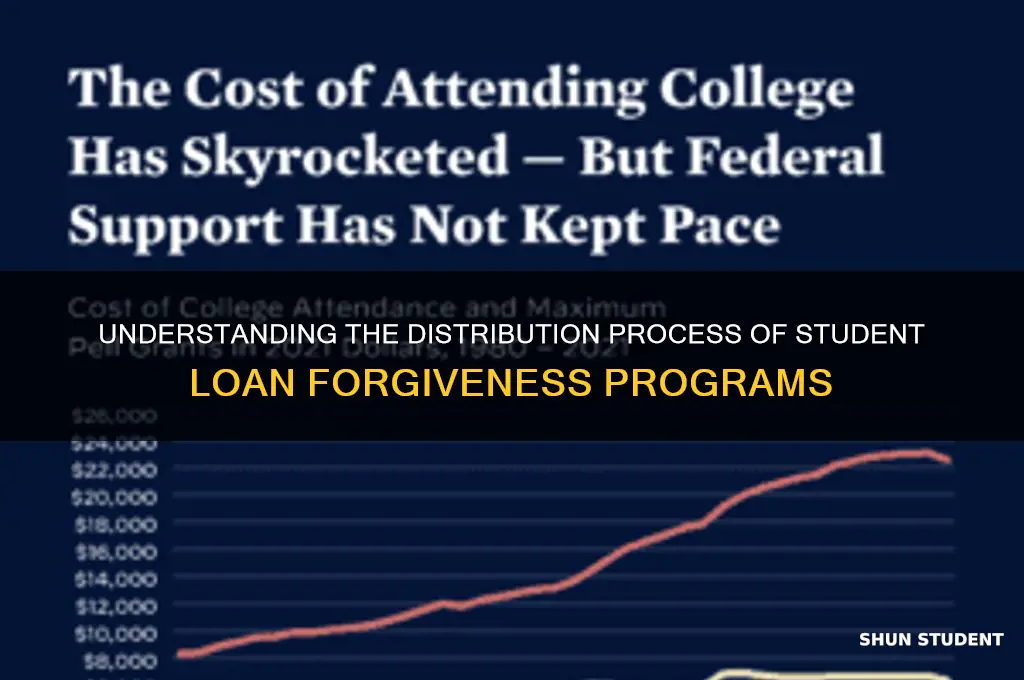

Student loan forgiveness has become a critical issue in recent years, with millions of borrowers seeking relief from mounting debt. The distribution of forgiveness programs varies widely, with initiatives like the Public Service Loan Forgiveness (PSLF) program and income-driven repayment plans offering pathways to debt cancellation after meeting specific criteria. Additionally, targeted relief efforts, such as those for defrauded students under the Borrower Defense to Repayment program, have provided immediate forgiveness to eligible individuals. However, the rollout of these programs has faced challenges, including administrative hurdles, confusion over eligibility, and uneven implementation, leaving many borrowers uncertain about their access to relief. As policymakers continue to debate broader forgiveness proposals, understanding how these programs are being distributed—and who benefits most—remains a pressing concern for borrowers and advocates alike.

| Characteristics | Values |

|---|---|

| Eligibility Criteria | Borrowers with federal student loans who meet income thresholds or work in public service. |

| Income-Driven Repayment (IDR) Forgiveness | Borrowers on IDR plans receive forgiveness after 20-25 years of qualifying payments. |

| Public Service Loan Forgiveness (PSLF) | Forgiveness after 10 years of qualifying payments for borrowers working full-time in public service. |

| One-Time Adjustment (2023) | Retroactive credit for IDR and PSLF, addressing past payment counting issues. |

| Loan Types Covered | Direct Loans, FFEL, and Perkins Loans (if consolidated into Direct Loans). |

| Income Thresholds | Single borrowers: $125,000; Married couples: $250,000 (based on 2020-2021 tax returns). |

| Amount Forgiven | Up to $20,000 for Pell Grant recipients; $10,000 for non-Pell Grant recipients. |

| Tax Implications | Forgiveness is tax-free at the federal level; state tax treatment varies. |

| Application Process | Automatic for most borrowers with up-to-date income information; others may need to apply. |

| Current Status (as of 2023) | Distribution paused due to legal challenges; pending Supreme Court decision. |

| Loan Servicers Involved | MOHELA (primary servicer for PSLF), other servicers for IDR adjustments. |

| Impact on Credit Score | Forgiveness does not negatively impact credit score. |

| Remaining Balance Treatment | Forgiven amount is removed from the loan balance; no further payments required. |

Explore related products

What You'll Learn

![]()

Eligibility criteria for loan forgiveness programs

Student loan forgiveness programs are not one-size-fits-all; they come with specific eligibility criteria that borrowers must meet to qualify. Understanding these requirements is crucial for anyone hoping to have their student debt forgiven. The criteria vary widely depending on the program, but common factors include the type of loan, employment sector, and repayment plan. For instance, the Public Service Loan Forgiveness (PSLF) program requires borrowers to work full-time in a qualifying public service job and make 120 eligible payments under an income-driven repayment plan. Conversely, the Teacher Loan Forgiveness program targets educators who teach full-time for five consecutive years in low-income schools. Each program’s criteria are designed to incentivize specific career paths or behaviors, making it essential for borrowers to align their circumstances with the program’s goals.

Analyzing the eligibility criteria reveals a strategic approach to debt relief. Programs like PSLF and income-driven repayment forgiveness (IDR) focus on long-term commitment, requiring 10 to 25 years of consistent payments. This structure ensures that only borrowers who demonstrate sustained financial responsibility benefit. On the other hand, programs like the National Health Service Corps Loan Repayment Program offer forgiveness in exchange for a shorter-term commitment, such as two years of service in a health professional shortage area. These differences highlight the importance of matching your career and financial situation to the program’s expectations. For example, a recent graduate with high debt might prioritize IDR forgiveness, while a mid-career professional could target PSLF.

A persuasive argument for borrowers is to proactively plan their careers and repayment strategies around these eligibility criteria. For instance, choosing an income-driven repayment plan early can lower monthly payments and set the stage for forgiveness after 20 or 25 years. Similarly, pursuing employment in public service or high-need fields like education or healthcare can open doors to specialized forgiveness programs. However, caution is necessary: not all loans qualify, and private loans are typically excluded. Borrowers must also maintain consistent payments and recertify income annually for IDR plans. Ignoring these details can disqualify even the most deserving candidates.

Comparatively, state-based loan forgiveness programs offer additional opportunities but with unique eligibility criteria. For example, California’s Teacher Loan Forgiveness Program requires teaching in a designated low-income school for five years, while New York’s Loan Forgiveness Program for Nurses mandates two years of service in underserved areas. These programs often complement federal options, providing a layered approach to debt relief. Borrowers should research state-specific programs to maximize their chances of forgiveness. Practical tips include keeping detailed records of employment and payments, staying informed about program updates, and consulting with loan servicers or financial advisors to ensure compliance with all requirements.

In conclusion, eligibility criteria for loan forgiveness programs are the gatekeepers to debt relief, designed to reward specific behaviors and careers. By understanding and strategically aligning with these criteria, borrowers can navigate the complex landscape of student loan forgiveness. Whether through federal programs, state initiatives, or a combination of both, careful planning and adherence to requirements are key to achieving financial freedom.

Does Student Loan Forgiveness Cover Refinanced Loans? Key Insights

You may want to see also

Explore related products

![]()

Income-driven repayment plan forgiveness timelines

Income-driven repayment (IDR) plans offer a lifeline to borrowers by capping monthly payments at a percentage of their discretionary income, but the real promise lies in the forgiveness timeline. After 20 or 25 years of consistent payments, depending on the plan, the remaining balance is forgiven. This isn’t a quick fix—it’s a long-term commitment. For instance, Revised Pay As You Earn (REPAYE) forgives after 20 years for undergraduate loans and 25 years for graduate loans, while Income-Based Repayment (IBR) typically requires 25 years. Understanding these timelines is critical, as they dictate how borrowers plan their financial futures.

Consider the mechanics: each payment under an IDR plan must be made on time and in full to count toward forgiveness. Missing payments resets the clock, so consistency is key. For example, a borrower on the Pay As You Earn (PAYE) plan who makes 120 qualifying payments over 10 years but then misses two payments will lose credit for those 120 payments and have to start over. Additionally, forgiven amounts may be taxed as income, though current policies like the American Rescue Plan Act of 2021 temporarily waive this tax through 2025. Borrowers should consult a tax professional to prepare for potential liabilities.

The choice of IDR plan significantly impacts the forgiveness timeline. For instance, a borrower with $50,000 in undergraduate loans earning $40,000 annually might pay 10% of their discretionary income under REPAYE, leading to forgiveness in 20 years. In contrast, the same borrower on IBR would pay 15% of discretionary income but face a 25-year timeline. Analyzing income, loan amount, and career trajectory can help borrowers select the plan that minimizes total repayment and aligns with their forgiveness goals.

Practical tips can streamline the journey. First, recertify income and family size annually to avoid payment increases or plan disqualification. Second, track payments meticulously—errors in counting qualifying payments are common. Third, explore Public Service Loan Forgiveness (PSLF) if eligible, as it offers forgiveness after 10 years of qualifying payments, potentially shaving 10–15 years off the IDR timeline. Finally, stay informed about policy changes, as federal regulations around student loan forgiveness evolve frequently.

In conclusion, income-driven repayment plan forgiveness timelines are a marathon, not a sprint. Borrowers must navigate plan specifics, maintain payment discipline, and strategize to minimize tax implications. While the path is long, the promise of debt relief makes it a viable option for many. By understanding the nuances and staying proactive, borrowers can turn this structured repayment system into a tool for financial freedom.

Is Your Student Debt Forgiven? Key Signs to Look For

You may want to see also

Explore related products

![]()

Public Service Loan Forgiveness (PSLF) requirements

The Public Service Loan Forgiveness (PSLF) program offers a lifeline to borrowers who dedicate their careers to public service, but its requirements are stringent and often misunderstood. To qualify, borrowers must make 120 eligible payments while working full-time for a qualifying employer. These payments must be made under an income-driven repayment plan, which adjusts monthly payments based on income and family size. For example, a teacher earning $45,000 annually with $100,000 in loans might pay as little as $150 per month under the Revised Pay As You Earn (REPAYE) plan, making it easier to meet the 120-payment threshold.

Qualifying employers include government organizations at any level, 501(c)(3) nonprofits, and some other types of nonprofits that provide public services. For instance, a social worker employed by a government-run mental health clinic or a lawyer working for a nonprofit legal aid organization would both meet the employer requirement. However, working for a for-profit company, even in a public service role, does not qualify. Borrowers must also be employed full-time, defined as either 30 hours per week or the employer’s definition of full-time, whichever is greater. Part-time workers, even in qualifying roles, are ineligible unless they meet the full-time criteria through multiple part-time jobs with qualifying employers.

One of the most common pitfalls borrowers face is misunderstanding which repayment plans qualify for PSLF. Only income-driven plans—such as Income-Based Repayment (IBR), Pay As You Earn (PAYE), and REPAYE—count toward the 120 payments. Standard or graduated repayment plans, while useful for other financial goals, do not qualify. Borrowers should submit an Employment Certification Form annually to ensure their payments and employer qualify, as this helps catch errors early. For example, a nurse who switches from a standard plan to REPAYE mid-career would only begin accruing eligible payments after the switch.

Persuasively, PSLF is one of the most generous forgiveness programs available, but its complexity demands proactive management. Borrowers should keep meticulous records of payments and employment, as well as stay informed about policy changes. For instance, the limited PSLF waiver in 2021-2022 temporarily allowed previously ineligible payments to count, benefiting thousands of borrowers. Such opportunities highlight the importance of staying engaged with the program’s updates. By meeting the requirements with precision, public servants can eliminate their student debt after a decade of dedicated service, transforming their financial futures.

Utah's Tax Rules on Student Loan Forgiveness: What You Need to Know

You may want to see also

Explore related products

![]()

One-time debt cancellation policies and limits

Student loan forgiveness programs often include one-time debt cancellation policies, which are designed to provide immediate relief to borrowers under specific circumstances. These policies typically target individuals who meet certain eligibility criteria, such as those who have worked in public service, experienced school misconduct, or faced financial hardship. For example, the Public Service Loan Forgiveness (PSLF) program offers tax-free cancellation of remaining loan balances after 120 qualifying payments for those employed full-time in eligible public service jobs. Similarly, the Borrower Defense to Repayment program discharges loans for students whose schools misled them or engaged in illegal practices, providing a one-time solution to their debt burden.

Analyzing these policies reveals both their strengths and limitations. One-time cancellations can significantly reduce financial stress for targeted groups, fostering economic stability and career mobility. However, they often exclude borrowers who do not meet narrow eligibility requirements, leaving many without relief. For instance, PSLF requires a decade of consistent payments and specific employment, which can be challenging to maintain. Additionally, these programs frequently face administrative hurdles, such as lengthy application processes and unclear guidelines, delaying or denying relief to eligible borrowers. Policymakers must balance the need for targeted assistance with the risk of creating inequities in debt relief distribution.

To maximize the impact of one-time cancellation policies, borrowers should take proactive steps to determine their eligibility and navigate the application process effectively. Start by reviewing the specific requirements for programs like PSLF or Borrower Defense, ensuring all necessary documentation is in order. For PSLF, use the Department of Education’s Employment Certification Form annually to track qualifying payments. If pursuing Borrower Defense, gather evidence of school misconduct, such as marketing materials or enrollment agreements. Additionally, stay informed about policy updates, as eligibility criteria and application procedures can change. For example, recent waivers for PSLF have temporarily relaxed certain rules, allowing more borrowers to qualify retroactively.

Comparing one-time cancellation policies to broader debt relief approaches highlights their role as a complementary tool rather than a comprehensive solution. While income-driven repayment plans offer long-term affordability, one-time cancellations provide immediate, transformative relief for specific borrowers. However, their limited scope underscores the need for systemic reforms, such as lowering interest rates or increasing grant-based aid. Advocates argue that combining targeted cancellations with broader policy changes could address both individual and systemic issues in student debt. For instance, pairing PSLF with expanded eligibility for public service roles could incentivize more borrowers to pursue careers in underserved areas.

In conclusion, one-time debt cancellation policies serve as a critical mechanism for providing targeted student loan relief, but their effectiveness depends on clear eligibility criteria, streamlined administration, and borrower awareness. By understanding these programs’ nuances and taking practical steps to qualify, individuals can maximize their chances of receiving forgiveness. However, policymakers must also address the limitations of these policies by integrating them into a broader strategy for tackling the student debt crisis. This dual approach ensures that both immediate needs and long-term challenges are met, creating a more equitable and sustainable system for borrowers.

Teacher Loan Forgiveness: What the Department of Education Offers

You may want to see also

Explore related products

![]()

State-specific loan forgiveness initiatives and distribution

In the patchwork of student loan forgiveness programs, state-specific initiatives stand out as tailored solutions addressing local workforce needs and economic priorities. Unlike federal programs, which cast a wide net, state programs often target specific professions, geographic areas, or industries critical to regional development. For instance, California’s Teacher Loan Forgiveness Program offers up to $20,000 to educators working in low-income schools, while New York’s Get on Your Feet Loan Forgiveness Program provides relief to recent graduates earning under $50,000 annually. These programs demonstrate how states leverage loan forgiveness to retain talent and address local shortages.

Consider the mechanics of distribution: state programs typically require applicants to commit to a specific service period, often ranging from 2 to 5 years. For example, Texas’ Rural Health Care Loan Repayment Program forgives up to $60,000 in loans for healthcare professionals serving in underserved areas for two years. Eligibility criteria are stringent, often requiring proof of employment, residency, or licensure within the state. Distribution is usually first-come, first-served or merit-based, with priority given to applicants in high-demand fields like education, healthcare, or law enforcement. Prospective applicants should research their state’s offerings early, as funding is limited and deadlines are firm.

A comparative analysis reveals disparities in state initiatives. Wealthier states like Massachusetts and Washington invest heavily in loan forgiveness, with programs like the Massachusetts Loan Repayment Program offering up to $50,000 for healthcare providers. In contrast, states with tighter budgets, such as Mississippi or West Virginia, offer smaller-scale programs with lower forgiveness caps. This gap underscores the need for federal-state collaboration to ensure equitable access to relief. States with robust programs often tie forgiveness to economic development goals, such as revitalizing rural areas or supporting STEM education, creating a win-win for borrowers and communities.

For borrowers navigating these programs, practical tips can streamline the process. First, verify eligibility by checking state-specific requirements, such as minimum service years or income thresholds. Second, gather documentation early, including employment contracts, tax returns, and loan statements. Third, apply promptly, as many programs have annual application windows and limited funding. Finally, explore stacking state and federal programs for maximum relief. For example, a teacher in Illinois could combine the state’s Loan Repayment Assistance Program with the federal Public Service Loan Forgiveness (PSLF) program to accelerate debt-free status.

In conclusion, state-specific loan forgiveness initiatives offer targeted relief but require proactive research and strategic planning. By aligning individual career goals with state priorities, borrowers can access substantial savings while contributing to local economies. As these programs evolve, staying informed and acting decisively will be key to maximizing their benefits.

Is Public Service Loan Forgiveness Still Available in 2023?

You may want to see also

Frequently asked questions

Eligibility varies by program. For example, the Public Service Loan Forgiveness (PSLF) program requires 10 years of qualifying payments while working full-time for a government or nonprofit employer. Other programs, like income-driven repayment plans, may offer forgiveness after 20-25 years of payments.

The Biden administration’s plan targets borrowers earning under $125,000 (individuals) or $250,000 (married couples). Eligible borrowers can receive up to $10,000 in forgiveness, with an additional $10,000 for Pell Grant recipients. Distribution is based on income and application approval.

Timing varies by program. For the Biden administration’s plan, forgiveness was initially expected within weeks of approval, but legal challenges have delayed the process. Other programs, like PSLF, process forgiveness after the borrower submits a complete application and meets all requirements.

Application processes differ by program. For the Biden administration’s plan, borrowers must complete an online application through the Department of Education’s website. For PSLF, borrowers must submit an Employment Certification Form annually and a final PSLF application after 120 qualifying payments.

Borrowers in default may still qualify for forgiveness, but they must first rehabilitate their loans or consolidate them into a new direct loan. Some programs, like the Fresh Start initiative, offer temporary relief for defaulted borrowers to help them regain eligibility for forgiveness.