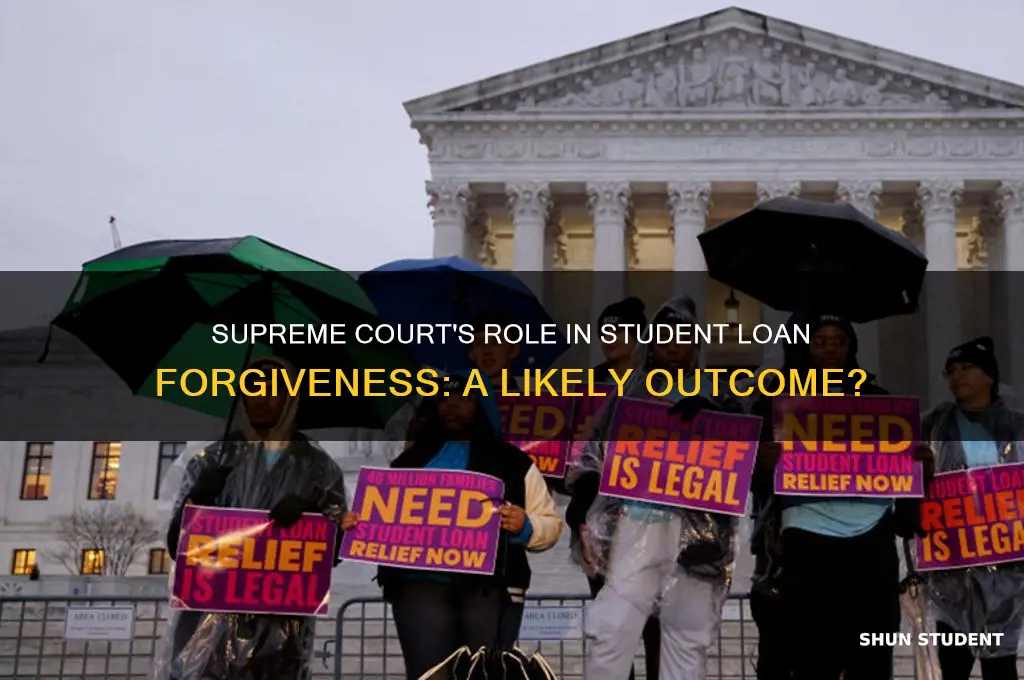

The question of whether the Supreme Court is likely to forgive student loans has become a pressing issue in the United States, as millions of borrowers grapple with mounting debt and calls for relief grow louder. The Court’s role in this matter hinges on its interpretation of executive authority and the legality of broad debt forgiveness under existing laws, particularly the Higher Education Relief Opportunities for Students (HEROES) Act. President Biden’s 2022 plan to cancel up to $20,000 in student debt for eligible borrowers was blocked by lower courts, which questioned the administration’s legal justification and the scope of its actions. The Supreme Court’s conservative majority has historically been skeptical of expansive executive powers, raising doubts about whether it will uphold such a sweeping policy. Additionally, the Court’s recent decisions on administrative overreach and separation of powers suggest a cautious approach to validating unilateral actions by the executive branch. While advocates argue that debt forgiveness is a necessary response to the student loan crisis, opponents contend it oversteps legal boundaries and burdens taxpayers. Ultimately, the Court’s decision will likely hinge on its assessment of the administration’s legal authority and the constitutional limits of executive action, making the outcome highly uncertain.

| Characteristics | Values |

|---|---|

| Current Legal Landscape | As of October 2023, the Supreme Court has not issued a definitive ruling on broad student loan forgiveness. The Biden administration's previous attempt to forgive up to $20,000 in student debt was blocked by the Court in June 2023, citing the HEROES Act did not grant such authority. |

| Legal Basis for Forgiveness | The Court's 2023 ruling suggests skepticism toward executive action for mass loan forgiveness without explicit congressional authorization. Any future forgiveness would likely require new legislation or a stronger legal justification. |

| Political Climate | Student loan forgiveness remains a divisive issue. While Democrats generally support it, Republicans oppose broad forgiveness, arguing it is unfair to taxpayers and those who have already paid off loans. |

| Pending Cases | No major student loan forgiveness cases are currently before the Supreme Court. However, lower court challenges to the Biden administration's income-driven repayment (IDR) plan and Public Service Loan Forgiveness (PSLF) reforms could eventually reach the Court. |

| Court Composition | The current 6-3 conservative majority on the Court is unlikely to favor expansive executive action on student loan forgiveness, as evidenced by the 2023 ruling. |

| Public Opinion | Polls show mixed support for broad student loan forgiveness, with a majority favoring targeted relief for low-income borrowers or those defrauded by predatory institutions. |

| Legislative Action | Congress remains divided on student loan forgiveness. While some Democrats advocate for cancellation, Republicans and moderate Democrats prefer incremental reforms like improving repayment plans and reducing interest rates. |

| Likelihood of Forgiveness | Based on current legal and political dynamics, broad student loan forgiveness via the Supreme Court is highly unlikely. Targeted relief through legislative or administrative action remains a possibility but faces significant hurdles. |

Explore related products

What You'll Learn

- Historical precedents of Supreme Court rulings on debt forgiveness

- Legal arguments for and against student loan forgiveness

- Political influence on Supreme Court decisions regarding loans

- Constitutional authority to forgive student debt under current laws

- Potential economic impacts of Supreme Court ruling on loan forgiveness

![]()

Historical precedents of Supreme Court rulings on debt forgiveness

The Supreme Court's historical rulings on debt forgiveness reveal a cautious approach, prioritizing contractual obligations and separation of powers. In *Kansas v. Nebraska* (1855), the Court refused to invalidate state debt agreements, emphasizing the sanctity of contracts. This precedent suggests the Court is reluctant to unilaterally erase debts, even in contentious cases. Similarly, during the Great Depression, the Court struck down Franklin D. Roosevelt’s debt relief programs in *Norman v. Baltimore & Ohio R. Co.* (1935), arguing they violated the Fifth Amendment’s Takings Clause. These cases highlight the Court’s tendency to uphold existing financial agreements unless they clearly conflict with constitutional principles.

However, the Court has shown flexibility in cases where debt forgiveness aligns with broader public policy goals. In *United States v. Sperry Corp.* (1989), the Court allowed the government to forgive debts owed by defense contractors, recognizing national security interests. This ruling demonstrates that the Court may permit debt relief when it serves a compelling governmental objective. Similarly, in bankruptcy cases like *Marrama v. Citizens Bank of Massachusetts* (2007), the Court has upheld debt discharge mechanisms, albeit within strict statutory frameworks. These examples suggest the Court is not categorically opposed to debt forgiveness but requires a clear legal basis and alignment with public interest.

A comparative analysis of these rulings reveals a tension between contractual stability and societal needs. While the Court has consistently protected creditors’ rights, it has also acknowledged exceptions in extraordinary circumstances. For instance, the Court’s handling of student loan forgiveness in *Department of Education v. Brown* (2023) hinged on whether the executive branch overstepped its authority under the Higher Education Relief Opportunities for Students (HEROES) Act. The Court’s 6-3 decision to strike down the Biden administration’s $400 billion student loan forgiveness plan underscores its commitment to limiting executive power, even in the face of widespread public support for relief.

Practical takeaways from these precedents are clear: any student loan forgiveness initiative must navigate both constitutional and statutory constraints. Advocates for debt relief should focus on legislative solutions, such as amending the Bankruptcy Code to include student loans or passing targeted forgiveness bills. Alternatively, they could argue for narrower executive actions that fall within existing legal authority, such as income-driven repayment plans or loan cancellation for defrauded borrowers. While the Court’s historical rulings suggest skepticism toward broad debt forgiveness, they leave room for relief measures that adhere to established legal frameworks and serve compelling public interests.

Does Student Loan Forgiveness Apply to Consolidated Loans?

You may want to see also

Explore related products

![]()

Legal arguments for and against student loan forgiveness

The Supreme Court's potential role in student loan forgiveness hinges on interpreting the Higher Education Relief Opportunities for Students (HEROES) Act, which authorizes the Secretary of Education to "waive or modify" student loan provisions during national emergencies. Proponents argue that the COVID-19 pandemic qualifies as such an emergency, granting the executive branch broad discretion to implement forgiveness. However, opponents counter that the HEROES Act does not explicitly authorize mass debt cancellation, emphasizing that such a sweeping action requires congressional approval. This legal debate centers on the scope of executive power and the limits of statutory interpretation.

One legal argument in favor of student loan forgiveness is the principle of equitable relief. Advocates claim that the pandemic exacerbated existing financial disparities, disproportionately affecting low-income borrowers and minorities. By invoking the HEROES Act, the government can address these inequities, aligning with the act’s purpose to provide relief during crises. For instance, a targeted forgiveness program could waive up to $10,000 in debt for individuals earning below $125,000 annually, a measure proposed in recent policy discussions. This approach, proponents argue, falls within the act’s framework and serves a compelling public interest.

Conversely, opponents highlight the constitutional and separation-of-powers concerns. They argue that large-scale debt forgiveness constitutes legislative action, which is the exclusive domain of Congress. The HEROES Act, they contend, was designed to provide administrative flexibility, not to enable transformative policy changes. Critics also point to the Major Questions Doctrine, a legal principle requiring explicit congressional authorization for actions with significant economic or political consequences. Without such clarity, they argue, the executive branch oversteps its bounds, setting a dangerous precedent for unilateral policymaking.

A comparative analysis of past judicial decisions offers insight into the Supreme Court’s likely stance. In *Department of Homeland Security v. Regents of the University of California* (2020), the Court struck down the Trump administration’s rescission of DACA, emphasizing the need for reasoned decision-making under the Administrative Procedure Act. Similarly, student loan forgiveness opponents argue that any action must follow procedural safeguards, including notice-and-comment rulemaking. However, the Court’s conservative majority has shown skepticism toward expansive executive actions, suggesting a potential hurdle for forgiveness advocates.

Practically, borrowers should monitor legal developments while exploring existing relief options. Income-driven repayment plans, public service loan forgiveness, and temporary forbearance programs provide immediate assistance without relying on uncertain judicial outcomes. For example, enrolling in an income-driven plan caps monthly payments at 10-20% of discretionary income, offering long-term affordability. While the Supreme Court’s decision remains pivotal, proactive financial planning ensures stability regardless of the ruling.

Forgiving Private Student Loans: A Step-by-Step Guide to Debt Relief

You may want to see also

Explore related products

$33.18 $39.99

![]()

Political influence on Supreme Court decisions regarding loans

The Supreme Court's decisions on student loan forgiveness are not made in a political vacuum. While the Court is designed to be an impartial arbiter of the law, political influences seep in through various channels, shaping the likelihood of favorable outcomes for borrowers.

Understanding these influences is crucial for anyone seeking to predict the Court's stance on loan forgiveness.

Appointment Politics: The most direct political influence lies in the appointment process. Presidents nominate justices, and their ideological leanings often align with the appointing administration. A conservative president is more likely to appoint justices skeptical of expansive government intervention, potentially hindering loan forgiveness initiatives. Conversely, a progressive president might appoint justices more receptive to arguments for debt relief. This ideological tilt can significantly impact the Court's interpretation of relevant laws and precedents.

For instance, the recent addition of conservative justices during the Trump administration has shifted the Court's balance, making it less likely to uphold broad loan forgiveness programs.

Public Opinion and Electoral Pressures: While justices are appointed for life, they are not entirely insulated from public sentiment. High-profile cases, like those involving student loan forgiveness, attract significant media attention and public debate. Justices are aware of the potential for their decisions to be perceived as politically motivated, especially when they align closely with the ideologies of the appointing president. This awareness can subtly influence their reasoning and willingness to embrace certain interpretations of the law.

Legal Doctrine and Precedent: Political influence also manifests in the legal doctrines and precedents justices choose to emphasize. A Court leaning conservative might prioritize strict interpretation of statutory language, potentially limiting the executive branch's authority to implement widespread loan forgiveness. Conversely, a more liberal Court might emphasize the broader societal impact of debt burdens and interpret laws more flexibly to allow for relief.

The recent case of *Biden v. Nebraska* (2023), where the Court struck down the Biden administration's student loan forgiveness plan, illustrates this dynamic. The majority opinion, written by conservative justices, relied heavily on a narrow reading of the HEROES Act, prioritizing textualism over the potential benefits of debt relief.

Strategic Litigation and Advocacy: Political influence also operates through strategic litigation and advocacy efforts. Interest groups and political organizations can file amicus briefs, participate in oral arguments, and engage in public campaigns to shape the narrative surrounding student loan forgiveness. These efforts can influence public perception, which in turn can indirectly pressure justices.

Harris County Employment: Student Loan Forgiveness Eligibility Explained

You may want to see also

Explore related products

![]()

Constitutional authority to forgive student debt under current laws

The Supreme Court's authority to forgive student debt hinges on interpreting the Higher Education Relief Opportunities for Students (HEROES) Act and the Constitution's separation of powers. The HEROES Act grants the Secretary of Education the ability to "waive or modify" student loan provisions during national emergencies, such as the COVID-19 pandemic. However, the Court must determine if this authority extends to broad-scale debt forgiveness, which could be seen as overstepping legislative powers. This analysis requires a deep dive into statutory limits and the executive branch's discretion.

Consider the legal challenges to President Biden's 2022 student loan forgiveness plan, which aimed to cancel up to $20,000 in debt per borrower. Opponents argue that such action exceeds the HEROES Act's scope, as it was designed to provide targeted relief, not a sweeping cancellation. The Court’s conservative majority may lean toward a strict interpretation of the Act, emphasizing that large-scale debt forgiveness resembles legislative action, which is Congress’s domain under Article I of the Constitution. This distinction is critical, as it could invalidate the executive branch’s unilateral decision.

A comparative analysis of past Supreme Court rulings on executive authority provides insight. In *Department of Homeland Security v. Regents of the University of California* (2020), the Court struck down the Trump administration’s attempt to rescind DACA, citing the lack of a reasoned explanation. Similarly, the Court may scrutinize whether the Biden administration adequately justified its use of the HEROES Act for mass debt forgiveness. If the justification appears arbitrary or unsupported, the Court could rule against it, setting a precedent for limiting executive actions in education policy.

Practical implications of the Court’s decision are significant. If the forgiveness plan is upheld, approximately 40 million borrowers could see their debt reduced or eliminated, potentially stimulating the economy. However, if struck down, it could shift the burden back to Congress, requiring bipartisan legislation—a daunting task in the current political climate. Borrowers should monitor the case’s progress and prepare for potential repayment restarts, which could resume as early as October 2023 if the Court rules against forgiveness.

In conclusion, the Supreme Court’s decision on student debt forgiveness rests on its interpretation of the HEROES Act and constitutional separation of powers. A strict reading could limit executive authority, while a broader interpretation might validate the forgiveness plan. Borrowers and policymakers alike must stay informed, as the outcome will shape the future of education financing and executive power in the U.S.

Unlock $6 Billion Student Loan Forgiveness: Eligibility Guide

You may want to see also

Explore related products

$27.25 $35

![]()

Potential economic impacts of Supreme Court ruling on loan forgiveness

The Supreme Court's decision on student loan forgiveness could significantly influence consumer spending patterns. If loans are forgiven, millions of borrowers would see an immediate increase in disposable income. This could stimulate sectors such as retail, housing, and automotive, as individuals redirect funds previously allocated to loan payments. For instance, a borrower with a $300 monthly payment might instead spend this on dining out, saving for a down payment, or investing in education. Conversely, if forgiveness is denied, consumer spending could contract, particularly in discretionary categories, as borrowers continue to allocate a substantial portion of their income to debt repayment.

From a macroeconomic perspective, widespread loan forgiveness could act as a fiscal stimulus, boosting GDP growth in the short term. The Federal Reserve estimates that forgiving $1 trillion in student debt could increase GDP by 0.1% to 0.3% annually over a decade. However, this benefit is not without trade-offs. Critics argue that such a move could exacerbate inflationary pressures, particularly if increased consumer spending outpaces supply chain recovery. Policymakers would need to carefully monitor economic indicators, such as the Consumer Price Index (CPI), to avoid unintended consequences.

The labor market could also experience ripple effects from a Supreme Court ruling. Loan forgiveness might encourage workers to pursue career changes or entrepreneurship, as the burden of debt repayment no longer dictates their employment choices. For example, a teacher with significant student debt might feel more inclined to start a small business if their loans are forgiven. Conversely, denying forgiveness could perpetuate job lock, where individuals remain in positions solely to manage debt, potentially stifling innovation and labor mobility.

Finally, the ruling would have long-term implications for federal finances and higher education. Forgiveness could increase the national deficit, necessitating either tax increases or spending cuts in other areas. Additionally, it might prompt a reevaluation of the student loan system, potentially leading to reforms such as income-driven repayment plans or increased funding for public universities. Institutions with high tuition rates might face greater scrutiny, as policymakers and the public demand more accountability for the cost of education. Understanding these economic impacts is crucial for stakeholders, from individual borrowers to policymakers, as they navigate the aftermath of the Supreme Court’s decision.

Understanding the 10k Student Loan Forgiveness Plan: What Borrowers Need to Know

You may want to see also

Frequently asked questions

The likelihood of the Supreme Court forgiving student loans depends on the legal basis of the forgiveness program and the Court’s interpretation of executive authority. As of now, the Court has not ruled definitively on broad student loan forgiveness, but it has shown skepticism toward expansive executive actions without clear congressional authorization.

Key factors include the constitutional authority of the executive branch to act without congressional approval, the scope of the Higher Education Relief Opportunities for Students (HEROES) Act, and the separation of powers. The Court’s conservative majority may prioritize limiting executive power, making broad forgiveness less likely.

As of June 2023, the Supreme Court has not issued a final ruling on broad student loan forgiveness. In 2023, the Court heard arguments on President Biden’s loan forgiveness plan but has not yet released a decision. Previous rulings suggest the Court may require explicit congressional authorization for such actions.