Navigating the timeline for hearing about student loan forgiveness can be a source of anxiety for many borrowers. The duration varies significantly depending on the specific forgiveness program, such as Public Service Loan Forgiveness (PSLF), Teacher Loan Forgiveness, or income-driven repayment plans. Generally, processing times range from several weeks to several months, with some cases taking up to a year or more, especially if additional documentation or reviews are required. Factors like the complexity of the application, the volume of submissions, and the efficiency of the loan servicer also play a role. Staying informed, submitting accurate paperwork, and maintaining regular communication with your loan servicer can help expedite the process and provide clarity on when you might receive a decision.

| Characteristics | Values |

|---|---|

| Processing Time for Applications | 4-6 weeks for initial review; up to 6 months for final decision (varies). |

| Factors Affecting Timeline | Application completeness, loan type, and program-specific requirements. |

| Public Service Loan Forgiveness (PSLF) | 2-3 months for Employer Certification Form (ECF) processing. |

| Income-Driven Repayment (IDR) Forgiveness | 3-6 months after submitting IDR plan application. |

| Notification Method | Email or mail from the loan servicer or Department of Education. |

| Current Backlog Impact | Delays possible due to high application volume (as of 2023). |

| Appeal Process Time | Additional 2-3 months if application is denied and appealed. |

| Updates on Application Status | Check online account or contact loan servicer for updates. |

| One-Time Account Adjustment | Processing time varies; updates expected through 2024. |

| Fraud or Error Resolution | May extend timeline by several months. |

Explore related products

What You'll Learn

![]()

Application Processing Time

The timeline for hearing back about student loan forgiveness applications can feel like a black hole, with borrowers often left in the dark about when to expect a decision. Understanding the application processing time is crucial for managing expectations and planning finances. While the exact duration varies depending on the forgiveness program and individual circumstances, there are some general patterns to be aware of.

Factors Influencing Processing Time:

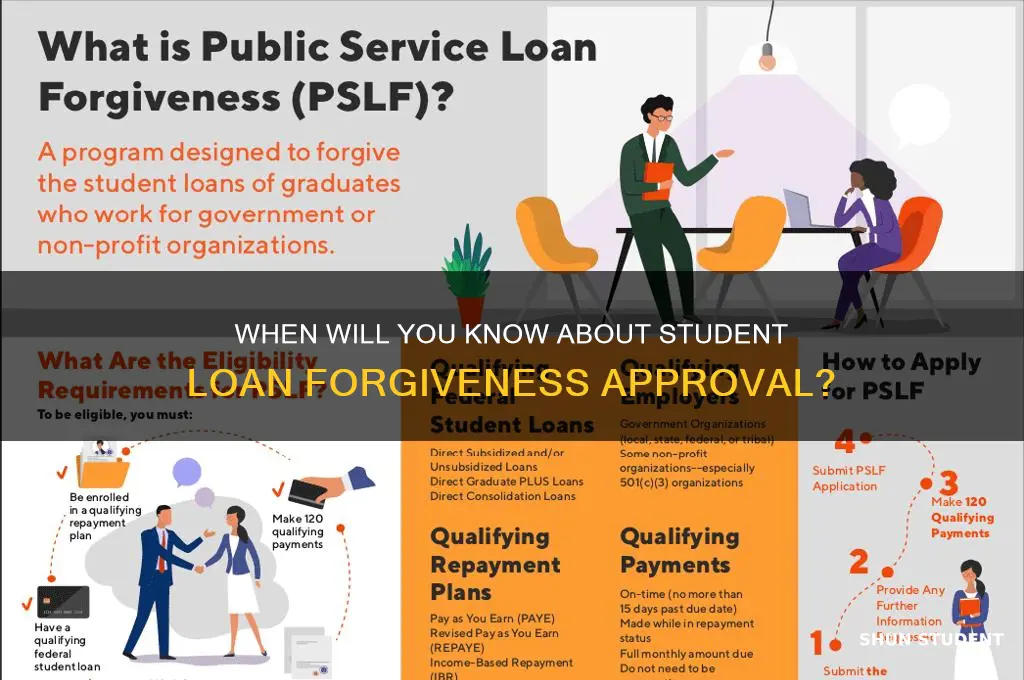

Several factors contribute to the time it takes for student loan forgiveness applications to be processed. Firstly, the type of forgiveness program plays a significant role. For instance, the Public Service Loan Forgiveness (PSLF) program, which requires 120 qualifying payments, typically takes 2-3 months for initial review and up to 3-6 months for final approval after submission. In contrast, income-driven repayment (IDR) plan forgiveness, which can take 20-25 years of payments, may have a more extended processing period due to the need for annual recertification of income and family size.

Tips for Expediting the Process:

To minimize delays, borrowers should ensure their applications are complete and accurate. This includes providing all necessary documentation, such as employment certification forms for PSLF or tax returns for IDR plans. Submitting applications online, if available, can also speed up processing times compared to mailing physical documents. Additionally, staying proactive by regularly checking the status of the application and responding promptly to any requests for further information can help keep the process moving forward.

Comparative Analysis of Processing Times:

A comparative analysis of different student loan forgiveness programs reveals varying processing times. For example, the Teacher Loan Forgiveness program, which offers up to $17,500 in forgiveness for eligible teachers, typically takes 4-6 weeks for processing. In contrast, the Perkins Loan Cancellation program, which provides forgiveness for specific professions like teachers, nurses, and law enforcement officers, can take up to 12 weeks. Understanding these differences can help borrowers set realistic expectations and plan accordingly.

Practical Advice for Borrowers:

To navigate the application processing time effectively, borrowers should create a timeline for their forgiveness application, including key milestones and deadlines. This can help them stay organized and ensure they meet all requirements. Additionally, keeping detailed records of all communications with loan servicers and submitting applications well in advance of any deadlines can provide a buffer in case of unexpected delays. By being proactive and informed, borrowers can minimize the stress and uncertainty associated with waiting for a decision on their student loan forgiveness application.

Student Loan Forgiveness After Death: A Guide for Borrowers

You may want to see also

Explore related products

![]()

Eligibility Review Duration

The eligibility review duration for student loan forgiveness varies widely, influenced by factors such as the type of forgiveness program, the volume of applications, and the complexity of individual cases. For instance, Public Service Loan Forgiveness (PSLF) reviews can take anywhere from 2 to 4 months, but this timeline extends significantly if additional documentation is required or if there are discrepancies in employment certification. Understanding these variables is crucial for borrowers to manage expectations and plan accordingly.

Analyzing the process reveals that the initial review often focuses on verifying employment and payment history. Borrowers can expedite this stage by ensuring their Federal Student Aid (FSA) account is up to date and submitting all required forms accurately. For income-driven repayment (IDR) forgiveness, the review may take longer, up to 6 months or more, due to the need to confirm payment counts and income eligibility over an extended period. Proactive borrowers should track their qualifying payments and retain records to streamline the review.

A comparative look at different programs highlights disparities in review times. Teacher Loan Forgiveness, for example, typically takes 3 to 6 months, but this assumes all teaching credentials and school eligibility are clearly documented. In contrast, Borrower Defense to Repayment (BDR) claims can take over a year due to the legal and investigative nature of the process. Borrowers in this category should prepare for a lengthy wait and stay informed about updates from the Department of Education.

To navigate this process effectively, borrowers should adopt a strategic approach. First, identify the specific forgiveness program and its unique requirements. Second, gather and organize all necessary documentation beforehand. Third, submit applications during periods of lower volume, if possible, to avoid delays. Finally, maintain regular communication with loan servicers and monitor the status of the review through the FSA website. These steps can mitigate frustration and increase the likelihood of a timely resolution.

In conclusion, the eligibility review duration for student loan forgiveness is not one-size-fits-all. By understanding program-specific timelines, preparing thoroughly, and staying proactive, borrowers can better manage the waiting period and increase their chances of a successful outcome. Patience and persistence are key, as the process often requires time and attention to detail.

Student Loan Forgiveness Phone Number: Your Guide to Debt Relief

You may want to see also

Explore related products

![]()

Approval Notification Timeline

The timeline for receiving approval notification for student loan forgiveness varies significantly depending on the program and the borrower’s circumstances. For instance, under the Public Service Loan Forgiveness (PSLF) program, borrowers typically hear back within 2-3 months after submitting their application, provided all documentation is complete and accurate. However, during periods of high application volume, such as after policy changes or waivers, processing times can extend to 6 months or more. Understanding these variables is crucial for managing expectations and planning finances effectively.

For income-driven repayment (IDR) forgiveness, the timeline is less predictable. Borrowers may not receive a formal notification until they reach their repayment term, which ranges from 20 to 25 years, depending on the plan. Interim updates are rare, and borrowers must track their qualifying payments independently. A practical tip: use the Federal Student Aid website to monitor payment counts annually, as errors in tracking can delay forgiveness. This proactive approach ensures you’re on track and allows time to dispute discrepancies.

Comparatively, borrowers under the one-time Student Loan Forgiveness initiative tied to the 2022 Biden administration’s debt relief plan faced unique challenges. Notifications were sent in waves, with some receiving approval within weeks and others waiting months due to legal holds and processing backlogs. This example highlights the importance of staying informed via official channels, such as the Department of Education’s website, and avoiding reliance on third-party sources that may spread misinformation.

To expedite the approval process, borrowers should prioritize accuracy and completeness when submitting applications. For PSLF, ensure your employer certification form is correctly filled out and submitted annually. For IDR, verify your income information promptly during recertification periods. A cautionary note: missing deadlines or submitting incomplete forms can reset the clock, significantly delaying notification. By treating each step with care, borrowers can minimize wait times and increase the likelihood of a swift approval.

Finally, while waiting for notification, borrowers should continue making payments if required, as forgiveness is not guaranteed until officially approved. For those in financial hardship, exploring options like forbearance or deferment can provide temporary relief. The key takeaway is that understanding the approval notification timeline empowers borrowers to navigate the process with confidence, reducing stress and ensuring a smoother path to debt relief.

How to Apply for Obama Student Loan Forgiveness Program: A Guide

You may want to see also

Explore related products

![]()

Common Delays Explained

The student loan forgiveness process is notorious for its unpredictability, often leaving borrowers in a state of limbo. One of the most common delays occurs during the verification of employment and income, a critical step for programs like Public Service Loan Forgiveness (PSLF). Borrowers must submit an Employment Certification Form (ECF) annually or when switching jobs, but processing times can stretch from 6 to 12 weeks. Missing signatures, incorrect employer information, or outdated forms frequently trigger rejections, forcing borrowers to resubmit and restart the clock. Pro tip: Double-check every field and use the latest form version available on the Federal Student Aid website.

Another bottleneck arises from backlogs at loan servicers, particularly during periods of policy changes or high application volumes. For instance, the 2022 limited PSLF waiver led to a surge in applications, overwhelming servicers like MOHELA, the designated PSLF processor. Borrowers reported wait times exceeding 90 days for simple inquiries, let alone forgiveness reviews. To mitigate this, track your application status through your servicer’s portal and follow up every 30 days. If progress stalls, escalate the issue to the Federal Student Aid Ombudsman for expedited resolution.

Documentation errors are a silent killer of timely forgiveness approvals. Programs like Income-Driven Repayment (IDR) forgiveness require proof of qualifying payments, but borrowers often submit incomplete or inconsistent records. For example, payments made under the wrong plan or during periods of deferment/forbearment may not count. Keep a personal log of all payments and cross-reference it with your servicer’s records annually. If discrepancies arise, request a payment history statement and dispute inaccuracies immediately.

Lastly, legislative and policy changes can introduce unforeseen delays. The Biden administration’s one-time student debt relief plan, for instance, faced legal challenges that paused processing for months. Similarly, updates to IDR or PSLF rules may require servicers to recalibrate their systems, slowing reviews. Stay informed by subscribing to updates from the Department of Education and advocacy groups like the Student Borrower Protection Center. While you can’t control policy shifts, being proactive ensures you’re prepared to act when changes occur.

In summary, delays in student loan forgiveness stem from verifiable steps, systemic backlogs, borrower errors, and external policy shifts. By understanding these pain points and taking targeted actions—such as meticulous form completion, persistent follow-ups, and proactive documentation—borrowers can navigate the process more effectively. Patience is key, but so is staying informed and engaged.

Virginia's Tax Treatment of Student Loan Forgiveness: What You Need to Know

You may want to see also

Explore related products

![]()

Checking Application Status Tips

After submitting your student loan forgiveness application, the waiting game begins, and the timeline for a decision can vary widely. While some applicants hear back within a few months, others may wait up to a year or more, depending on the program and the volume of applications being processed. This uncertainty can be frustrating, but understanding how to effectively check your application status can provide clarity and reduce anxiety.

Step-by-Step Guide to Checking Your Status

First, log into the official portal where you submitted your application, such as the Federal Student Aid website or the platform specific to your forgiveness program. Look for a "Check Application Status" or "Dashboard" section. If your program requires paper submissions, note the confirmation number or receipt date provided after submission. For federal programs like Public Service Loan Forgiveness (PSLF), use the PSLF Help Tool to track progress. If you’re unsure where to look, contact your loan servicer directly for guidance. Keep a record of all login credentials and submission details to streamline future checks.

Cautions to Avoid Frustration

Avoid the temptation to check your status daily, as updates may only occur monthly or quarterly. Over-checking can lead to unnecessary stress and confusion. Additionally, be wary of third-party services claiming to expedite status updates—these are often scams. Stick to official channels and verify any communication received to ensure it’s legitimate. If you notice discrepancies or errors in your status, address them promptly with your servicer to prevent delays.

Analyzing Delays and What They Mean

Delays in status updates often stem from high application volumes, incomplete submissions, or verification issues. For instance, PSLF applications can take 90 days or more for initial processing. If your status remains unchanged for an extended period, it may indicate a problem with your application, such as missing documentation or eligibility issues. In such cases, proactive communication with your servicer is key. They can provide insights into the holdup and guide you on resolving it.

Practical Tips for Staying Informed

Set a monthly reminder to check your status, ensuring you stay informed without obsessing. Keep a log of each check, noting any changes or updates, as this can help identify patterns or issues. If you’re nearing the expected decision timeline and still haven’t heard back, reach out to your servicer for an update. Finally, stay informed about program changes or extensions that could impact your application. For example, temporary waivers or policy updates might affect processing times or eligibility criteria.

By following these tips, you can navigate the waiting period with greater confidence and control, turning a potentially stressful experience into a manageable process.

Is Your Student Loan Forgiven? How to Check and Confirm

You may want to see also

Frequently asked questions

Processing times vary, but it generally takes 8–12 weeks to receive a decision after submitting a complete application.

Delays can occur due to high application volumes, incomplete documentation, or the complexity of the forgiveness program.

You can check the status by logging into your loan servicer’s website or contacting them directly for updates.

Yes, programs like Public Service Loan Forgiveness (PSLF) or income-driven repayment plans may have different processing times based on their requirements.

Follow up with your loan servicer to ensure your application is complete and inquire about any potential delays.