Navigating the complexities of student debt is a pressing concern for many, as the duration of repayment can vary significantly based on factors such as loan type, interest rates, repayment plans, and individual financial circumstances. For instance, federal student loans often offer flexible repayment options like income-driven plans, which can extend the repayment period to 20–25 years, while standard plans typically span 10 years. Private loans, on the other hand, may have shorter or longer terms depending on the lender’s terms. Additionally, strategies like refinancing, making extra payments, or pursuing loan forgiveness programs can shorten the time spent in debt. Understanding these variables and creating a tailored financial plan is crucial for managing student debt effectively and minimizing its long-term impact.

Explore related products

What You'll Learn

- Understanding Loan Terms: Repayment periods, interest rates, and loan types impact debt duration

- Income-Driven Repayment Plans: Lower payments based on income extend repayment time

- Debt Forgiveness Programs: Public Service Loan Forgiveness or other programs can eliminate debt

- Extra Payments Strategy: Paying more than the minimum reduces interest and time

- Refinancing Options: Lower interest rates through refinancing can shorten repayment timelines

![]()

Understanding Loan Terms: Repayment periods, interest rates, and loan types impact debt duration

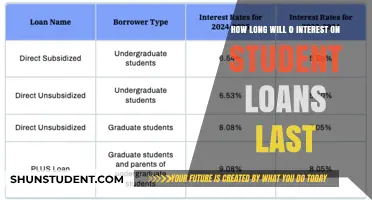

Repayment periods, interest rates, and loan types form the backbone of your student debt timeline. A standard federal student loan offers a 10-year repayment window, but this is far from a one-size-fits-all scenario. Income-driven repayment plans, for instance, stretch this timeline to 20-25 years, tying monthly payments to your earnings. While this lowers immediate financial strain, it prolongs the debt and often results in paying more in interest over time. Private loans, on the other hand, vary widely—some offer 5-year terms, while others extend up to 20 years. Understanding these differences is crucial, as the repayment period directly dictates how long you’ll be in debt.

Interest rates are the silent architects of your debt duration. Federal loans for undergraduates currently hover around 5.5%, while graduate and private loans can climb to 7% or higher. A seemingly small difference of 1-2% can add thousands to your total repayment amount. For example, a $30,000 loan at 5% interest paid over 10 years totals $34,780, whereas the same loan at 7% balloons to $38,290. Compounding interest means the longer you take to repay, the more it costs. Prioritizing high-interest loans first can shorten your debt timeline significantly.

Loan types dictate not only repayment terms but also flexibility and benefits. Federal loans come with perks like income-driven plans, deferment, and forgiveness programs, which can extend repayment but offer safety nets. Private loans often lack these protections but may offer lower rates for borrowers with excellent credit. For instance, a borrower with a 750 credit score might secure a 4% private loan, repaying it faster than a federal loan at 5.5%. However, private loans rarely allow forbearance or forgiveness, making them riskier if financial hardship arises.

To minimize debt duration, consider these practical steps: First, calculate your total monthly payment across all loans and explore refinancing options for private loans if your credit score has improved. Second, allocate extra funds to high-interest loans while maintaining minimum payments on others. Third, investigate loan forgiveness programs like Public Service Loan Forgiveness (PSLF) if you work in qualifying sectors. Finally, avoid extending repayment periods unless absolutely necessary, as it increases total interest paid. By strategically navigating repayment periods, interest rates, and loan types, you can take control of your student debt timeline.

Will Nevada Tax Student Loan Forgiveness? What Borrowers Need to Know

You may want to see also

Explore related products

![]()

Income-Driven Repayment Plans: Lower payments based on income extend repayment time

Income-driven repayment (IDR) plans are a lifeline for borrowers struggling with federal student loan payments, but they come with a trade-off: lower monthly payments in exchange for a longer repayment period. These plans, which include options like Pay As You Earn (PAYE), Revised Pay As You Earn (REPAYE), Income-Based Repayment (IBR), and Income-Contingent Repayment (ICR), cap your monthly payment at a percentage of your discretionary income, typically 10-20%. For example, a single borrower earning $40,000 annually with $50,000 in loans might see payments drop from $500 to $200 per month under REPAYE. While this provides immediate relief, the extended repayment term—often 20 to 25 years—means you’ll be in debt longer, potentially paying more in interest over time.

Consider the math: a borrower with $30,000 in loans at 5% interest on the Standard 10-Year Plan would pay $318 monthly and $10,164 in total interest. Under REPAYE, the same borrower might pay $150 monthly but stretch repayment to 25 years, accruing $22,500 in interest. The longer timeline can feel daunting, but IDR plans offer a safety net: any remaining balance after the repayment period is forgiven, though you may owe taxes on the forgiven amount. This makes IDR particularly appealing for borrowers with low incomes or high debt-to-income ratios, such as teachers, social workers, or recent graduates in entry-level positions.

Choosing an IDR plan requires careful consideration of your financial goals. If your income is expected to rise significantly in the future, the extended repayment period may outweigh the benefits of lower payments. However, for those in public service or with incomes unlikely to grow substantially, IDR can provide stability and the possibility of loan forgiveness. For instance, borrowers pursuing Public Service Loan Forgiveness (PSLF) often pair it with an IDR plan to minimize payments while working toward forgiveness after 10 years.

Practical tips for navigating IDR include annually recertifying your income to ensure accurate payments and exploring options like REPAYE, which offers interest subsidies to prevent negative amortization. Additionally, keep detailed records of payments, as administrative errors in IDR programs are common. While IDR plans extend your time in debt, they can be a strategic tool for managing student loans without sacrificing financial stability. The key is to weigh the immediate relief against the long-term commitment and align your choice with your career and financial trajectory.

Can Sallie Mae Student Loans Be Forgiven? Exploring Options and Eligibility

You may want to see also

Explore related products

![]()

Debt Forgiveness Programs: Public Service Loan Forgiveness or other programs can eliminate debt

Student debt can feel like a life sentence, but it doesn't have to be. Debt forgiveness programs offer a glimmer of hope, potentially shaving years or even decades off your repayment timeline.

Public Service Loan Forgiveness (PSLF) stands out as a beacon for those committed to serving the greater good. This federal program wipes away remaining loan balances after 120 qualifying payments (10 years) for borrowers working full-time in eligible public service jobs. Think teachers, nurses, social workers, and government employees. The key lies in meticulous record-keeping: ensure your employer qualifies, submit employment certification forms annually, and stay enrolled in an income-driven repayment plan.

While PSLF offers a clear path, it's not the only route. Income-Driven Repayment (IDR) plans, coupled with forgiveness after 20-25 years of payments, provide a safety net for borrowers in various careers. These plans cap monthly payments based on income and family size, making them manageable for those with lower salaries. After the designated repayment period, any remaining balance is forgiven, though borrowers may face tax implications on the forgiven amount.

State-based forgiveness programs and employer-sponsored repayment assistance add further layers of opportunity. Many states offer loan forgiveness for professionals in high-demand fields like healthcare, education, and law, often tied to service commitments in underserved areas. Simultaneously, an increasing number of employers recognize the burden of student debt and offer repayment assistance as a benefit, chipping away at balances over time.

Navigating these programs requires diligence and research. Eligibility criteria, application processes, and potential tax consequences vary widely. Utilize resources like the Federal Student Aid website, state education agencies, and employer benefits portals to explore your options. Remember, debt forgiveness isn't a guarantee, but with careful planning and strategic choices, you can significantly shorten your journey to financial freedom.

Military Reserves and Student Loan Forgiveness: What You Need to Know

You may want to see also

Explore related products

![]()

Extra Payments Strategy: Paying more than the minimum reduces interest and time

Making only the minimum payment on your student loans is a slow, costly path to freedom. Each month, a significant portion of that payment goes toward interest, barely chipping away at the principal balance. This cycle can trap you in debt for decades, delaying major life milestones like buying a home or saving for retirement.

Enter the extra payments strategy: a deliberate approach to accelerate debt repayment. By allocating additional funds beyond the minimum, you directly target the principal, shrinking the overall balance faster. This reduces the total interest accrued over time, saving you money and shortening your loan term.

Imagine two borrowers, both with $30,000 in student loans at 6% interest. Borrower A pays the minimum monthly payment of $300. Borrower B pays an extra $100 each month. Borrower A will be in debt for 10 years, paying a total of $37,676. Borrower B, however, will be debt-free in just over 7 years, paying a total of $34,264. That's a savings of nearly $3,500 and over 3 years of debt-free living.

Implementing this strategy requires discipline and planning. Start by assessing your budget to determine how much extra you can realistically afford each month. Even small increments, like $50 or $100, can make a difference. Consider automating these extra payments to ensure consistency. If you receive bonuses, tax refunds, or other windfalls, allocate a portion or all of it toward your loans.

It's crucial to confirm with your loan servicer that extra payments are applied to the principal, not future payments. Some servicers may automatically apply extra funds to the next month's payment unless instructed otherwise. Additionally, focus on high-interest loans first if you have multiple loans. This maximizes the impact of your extra payments by reducing the most costly debt fastest.

The extra payments strategy isn't a quick fix, but it's a powerful tool for taking control of your student debt. By committing to paying more than the minimum, you'll not only save money on interest but also reclaim years of your financial life. It's an investment in your future, one that pays dividends in both dollars and peace of mind.

Forgiving Student Loans: A Path to Economic Growth and Equality

You may want to see also

Explore related products

![]()

Refinancing Options: Lower interest rates through refinancing can shorten repayment timelines

Student debt repayment timelines often stretch over a decade or more, but refinancing can be a powerful tool to accelerate your journey to debt freedom. By securing a lower interest rate, you can significantly reduce the total amount you pay over the life of your loan and potentially shorten your repayment period.

Imagine this: you have a $30,000 loan at a 7% interest rate with a 10-year repayment term. Your monthly payment would be around $340, and you'd end up paying over $40,000 in total. Now, let's say you refinance to a 5% interest rate. Your monthly payment drops to roughly $315, and your total repayment amount shrinks to around $37,800. That's a savings of over $2,000 and potentially a shorter repayment timeline if you continue paying the original higher amount.

Refinancing isn't a one-size-fits-all solution. To qualify, you'll typically need a good credit score (generally 650 or higher), a steady income, and a low debt-to-income ratio. Shop around for lenders who specialize in student loan refinancing, comparing interest rates, repayment terms, and any fees associated with the process. Remember, refinancing federal loans means giving up certain borrower protections, like income-driven repayment plans and loan forgiveness options. Weigh the benefits of lower interest rates against the potential loss of these safeguards.

Consider this scenario: Sarah, a recent graduate with $45,000 in federal loans at a 6.8% interest rate, was facing a 10-year repayment plan. By refinancing to a private loan with a 4.5% interest rate and maintaining her original monthly payment, she shaved two years off her repayment timeline and saved thousands in interest.

Refinancing can be a strategic move to shorten your student debt journey, but it requires careful consideration. Assess your financial situation, compare offers diligently, and understand the trade-offs involved. With the right approach, refinancing can be a powerful tool to achieve financial freedom faster.

Volunteers Needed: Mentoring Students for a Brighter Future

You may want to see also

Frequently asked questions

The average time to pay off student debt ranges from 10 to 30 years, depending on the loan type, repayment plan, and amount borrowed.

Yes, you can shorten the repayment period by making extra payments, refinancing for a lower interest rate, or choosing an accelerated repayment plan.

Yes, income-driven repayment plans often extend the repayment term (up to 20–25 years) but can lower monthly payments and offer loan forgiveness after the term ends.

Refinancing can shorten or extend your repayment term depending on the new loan terms you choose, such as a lower interest rate or a shorter repayment period.

Loan forgiveness programs, like Public Service Loan Forgiveness (PSLF), can eliminate debt after 10–25 years of qualifying payments, but eligibility requirements must be met.