The U.S. Department of Education publishes cohort default rates based on the percentage of a school's borrowers who enter repayment on Direct Loan Program loans during a fiscal year (October 1 to September 30) and default before the end of the second following fiscal year. This data is available for all students as of September 30, 2021, including undergraduates, graduates, and those pursuing professional degrees or certificates. The three-year student loan default rate is the highest among people who attended private for-profit colleges. In 2022, the three-year student loan default rate was 2.3%, down from 10-11.5% between 2016 and 2020. The COVID-19 pandemic also contributed to a decrease in student loan default rates.

Explore related products

![Reducing student loan defaults : a plan for action. 1990 [Leather Bound]](https://m.media-amazon.com/images/I/61IX47b4r9L._AC_UY218_.jpg)

What You'll Learn

![]()

Loan default rates by race/ethnicity

Student loan default rates vary significantly by race and ethnicity, reflecting dramatic differences in financial health, habits, and resource availability across communities. While the amounts borrowed by students of different races are comparable, Black borrowers are more likely to default on their student loans than White borrowers.

According to a Richmond Fed Economic Brief, 30% of Black college graduates with federal student loans reported having defaulted at least once, compared to 10% of White graduates. Similarly, Pew Research found that 50% of Black borrowers and 40% of Hispanic or Latino borrowers have had a loan default, compared to less than a third (29%) of White borrowers.

Black borrowers face unique challenges due to student loan debt, with higher monthly payments and lower median annual incomes than their White counterparts. They are also more likely to be on income-based repayment plans and struggle financially, with a net worth that is $8,500 less than White peers. Four years after graduation, Black students owe an average of 188% more than what White students borrowed. Additionally, Black borrowers are more likely to experience multiple defaults, with 37% reporting three or more loan defaults.

Hispanic or Latino borrowers also face significant challenges, with the second-highest default rates after Black borrowers. They are more likely to experience multiple defaults, with 75% reporting having defaulted more than once. Lower monthly payments may contribute to this, as lower payments result in a higher ultimate cost due to interest rates.

These disparities in loan default rates are attributed to socioeconomic factors, financial circumstances, and workplace discrimination rather than individual characteristics. Addressing these racial inequities in student loan defaults is crucial for promoting financial equality and accessibility to education.

Attendee Numbers at the University of Washington, Seattle

You may want to see also

Explore related products

![]()

Loan default rates by college type

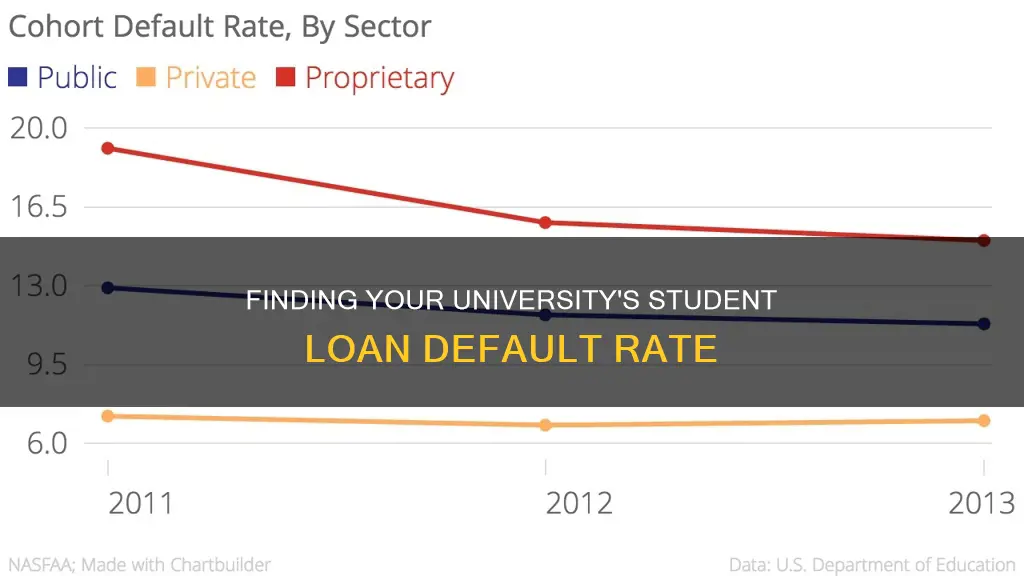

The likelihood of defaulting on student loans depends on various factors, including the type of college attended and whether the student completed their degree. The three-year student loan default rate is the highest among people who attended private for-profit colleges, and this has been the case for years. The current three-year default rate for private for-profit colleges is 1.7%, while it is 14.7% for students who attended a private for-profit college within three years of beginning repayment.

Private non-profit colleges have a lower default rate of 6.39% within three years of beginning repayment. However, students who attended private non-profit colleges for less than two years were the most likely to default on their loans within three years of beginning repayment.

Public institutions have a default rate of 9.30%, falling between the rates of private for-profit and private non-profit institutions.

Native American Colleges had the highest student loan default rate (19.73%), followed by HBCUs (16.65%), Ethnically Not Reported Colleges (9.18%), and Hispanic Colleges (8.68%). Four-year institutions at private, public, and for-profit institutions had the lowest collective student loan default rates.

Additionally, certain states tend to have higher student loan default rates. Mississippi had the highest rate (15.19%), followed by Oklahoma (15.15%), Louisiana (14.91%), New Mexico (13.66%), and West Virginia (12.96%). States in the Northeast and Midwest tend to have lower default rates, while Southern states tend to have higher rates.

Overall, the national student loan default rate dropped to 9.70%, down from 10.10% in the previous year.

Applying to Italian Universities: A Guide for International Students

You may want to see also

Explore related products

![]()

Loan default rates by degree type

The default rate is the percentage of outstanding loans that a lender writes off as unpaid after a prolonged period of missed payments. The default rate is an economic indicator. The likelihood of missing payments on student loans depends on various factors, including the school attended, race/ethnicity, income levels, and whether the degree was completed.

The three-year student loan default rate is the highest among people who attended private for-profit colleges. The default rate for borrowers who attended private nonprofit colleges is lower, at 1.7%. The default rate also tends to be lower for those who attended four-year programs and attained BA degrees, as opposed to dropouts.

In the last decade, the student loan default rate ranged from a high of 11.8% in 2012 to a low of 7.3% in 2018. The three-year student loan default rate in 2022 was 2.3%. The rate dropped to 0.0% in 2024 due to the COVID-19-related student loan forbearance.

At age 30, around 10% of bachelor's degree holders have defaulted on their student loans, while over 20% of associate degree holders have defaulted. Dropouts have higher default rates at every age than graduates, likely because graduates have better access to the labour market and can find better-paying jobs. However, among graduates, those with associate degrees default at higher rates than bachelor's degree holders.

Discover Grand Canyon University's On-Campus Student Population

You may want to see also

Explore related products

![]()

Loan default rates by state

The U.S. Department of Education releases official cohort default rates annually. The three-year cohort default rate is the percentage of a school's borrowers who enter repayment on specific federal loans during a particular federal fiscal year (FY) (October 1 to September 30) and default or meet other specified conditions before the end of the subsequent two fiscal years.

The three-year student loan default rate considers the percentage of student loan borrowers who enter federal student loan repayment during a federal fiscal year and default within the next two fiscal years. For instance, the 2024 student loan default rate refers to the rate between October 2020 and September 2023.

The three-year student loan default rate was 2.3% in 2022. From 2016 to 2020, student loan default rates ranged from 10% to 11.5%. The rate dropped to 0.0% in 2024 due to the COVID-19-related student loan forbearance. In the last decade, the highest rate was 11.8% in 2012, and the lowest was 7.3% in 2018.

The likelihood of missing student loan payments depends on factors such as the school attended, degree completion, race/ethnicity, and income levels. The three-year default rate is highest among borrowers from private for-profit colleges. For instance, 14.7% of borrowers from private for-profit colleges defaulted within three years of beginning repayment, compared to 6.39% from private non-profit colleges.

Additionally, 25% of borrowers in Texas defaulted within their first five years of repayment. Among recent graduates, 10.1% of Hispanic/Latino and 6.1% of White/Caucasian borrowers reported defaulting on their student loans.

Enrollments at Maryville University: A Comprehensive Overview

You may want to see also

Explore related products

![]()

Consequences of defaulting on a loan

Defaulting on a student loan can have serious financial and legal consequences, which can impact your future financial prospects and stability. Default occurs when an individual fails to make payments on their student loans or violates the terms of their payment agreement.

One of the key consequences of defaulting on a student loan is the negative impact on your credit score and credit history. Credit bureaus are notified of the default, which results in a negative credit report. This can make it challenging for borrowers to qualify for other forms of credit, such as credit cards, auto loans, or mortgages. It may even affect their ability to rent an apartment or secure employment, as landlords and employers may review credit histories.

Additionally, defaulted borrowers may face wage garnishment, where a portion of their earnings is withheld by their employer to repay the debt. This can be done through Administrative Wage Garnishment, where up to 15% of disposable income is deducted from paychecks. The Treasury Offset program is another method employed, where tax refunds and federal benefit payments are withheld and applied towards loan repayment.

Defaulted borrowers also lose eligibility for benefits such as deferment, forbearance, and the ability to choose repayment plans. They may also become ineligible for additional federal student aid unless satisfactory repayment arrangements are made.

The cost of collecting defaulted loans further exacerbates the financial burden. Collection charges, which can be as high as 30% of the loan amount, are added to the principal, interest, and late charges. This significantly slows down the borrower's progress in repaying the debt, extending the repayment period by several years.

It is crucial for individuals to understand the repercussions of defaulting on student loans and to proactively manage their loan repayment process. This includes borrowing responsibly, setting up budgets, and maintaining open communication with loan providers to avoid default and minimize financial strain.

Oral Roberts University: A Student-Centric Community

You may want to see also

Frequently asked questions

The U.S. Department of Education publishes cohort default rates based on the percentage of a school's borrowers who enter repayment on Direct Loan Program loans during a federal fiscal year (October 1 to September 30) and default before the end of the second following fiscal year. The data is available for download on the Federal Student Aid website.

The three-year student loan default rate has ranged from a high of 11.8% in 2012 to a low of 7.3% in 2018. In 2022, the three-year default rate was 2.3%. The rate dropped during the COVID-19 pandemic due to forbearance, with a rate of 0% in 2024.

The likelihood of defaulting on student loans depends on various factors, including the type of school attended (for-profit colleges have higher default rates), completion of the degree (dropouts default more), race/ethnicity, and income levels.