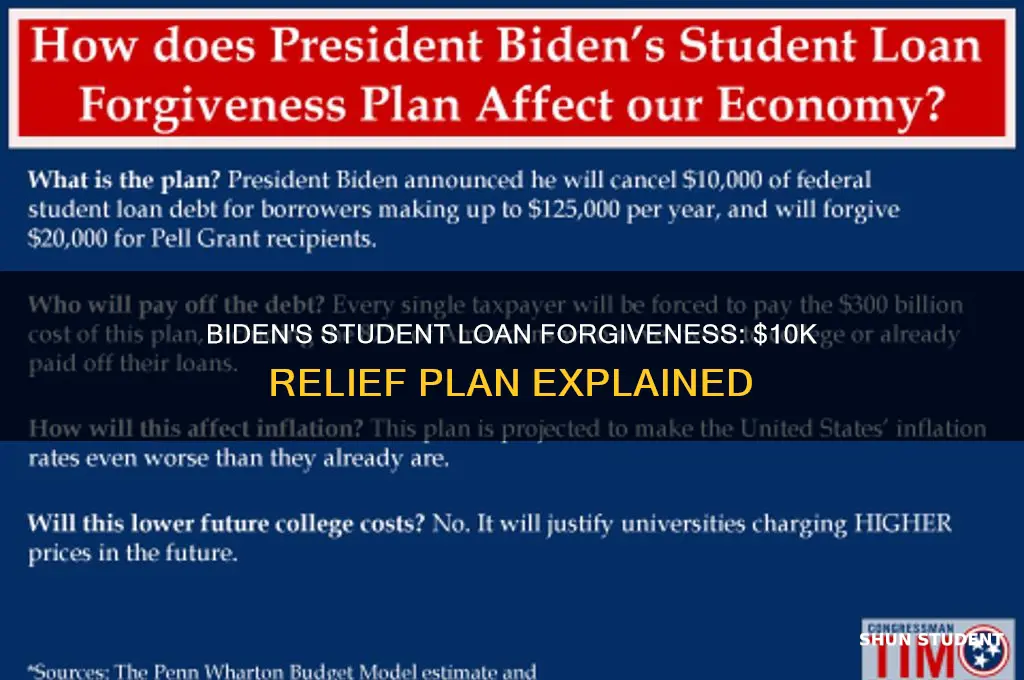

The topic of President Biden forgiving $10,000 in student loans has sparked widespread debate and discussion across the United States. As part of his campaign promises, Biden proposed targeted student loan forgiveness to alleviate the financial burden on millions of borrowers. While he has taken steps to address the issue, such as canceling debt for specific groups like defrauded students and those with disabilities, the broader $10,000 forgiveness plan remains a contentious issue. Advocates argue it would provide much-needed relief to struggling borrowers, while critics raise concerns about its cost, fairness, and potential impact on the economy. As of now, no final decision has been announced, leaving borrowers and policymakers eagerly awaiting further developments.

| Characteristics | Values |

|---|---|

| Loan Forgiveness Amount | Up to $10,000 for eligible borrowers |

| Additional Forgiveness for Pell Grant Recipients | Up to $20,000 for borrowers who received Pell Grants |

| Eligibility Income Limit | Annual income below $125,000 (individuals) or $250,000 (married couples) |

| Loan Types Covered | Federal student loans (Direct Loans, FFELP, Perkins Loans) |

| Private Loans Eligibility | Not eligible for forgiveness |

| Application Requirement | Borrowers may need to apply (details pending) |

| Implementation Status | Partially implemented; legal challenges have delayed full rollout |

| Current Legal Status | Facing lawsuits and Supreme Court challenges |

| Debt Cancellation Timeline | Originally planned for late 2022, now uncertain due to legal battles |

| Total Estimated Cost | Approximately $400 billion |

| Number of Borrowers Impacted | Over 40 million borrowers |

| Political Context | Key campaign promise by President Biden; opposed by Republican lawmakers |

| Alternative Relief Measures | Extended student loan payment pause until legal issues are resolved |

Explore related products

What You'll Learn

![]()

Eligibility criteria for loan forgiveness

As of the latest updates, President Biden's student loan forgiveness plan has been a subject of intense discussion and legal scrutiny. While the initial proposal aimed to forgive up to $10,000 in federal student loans for eligible borrowers, with an additional $10,000 for Pell Grant recipients, the implementation has faced significant challenges. Understanding the eligibility criteria is crucial for borrowers hoping to benefit from this relief. Here’s a detailed breakdown to guide you through the process.

Income Thresholds: Who Qualifies?

The eligibility criteria for Biden’s loan forgiveness plan are primarily income-driven. Single borrowers earning less than $125,000 annually or married couples filing jointly with incomes under $250,000 are eligible for the $10,000 forgiveness. Pell Grant recipients meeting these income thresholds can receive an additional $10,000, totaling $20,000 in relief. These income limits are based on either 2020 or 2021 tax returns, providing flexibility for borrowers whose financial situations may have changed. It’s essential to verify your income status using the correct tax year to ensure compliance with the criteria.

Loan Types and Disbursement Dates

Not all student loans qualify for forgiveness. Only federal student loans held by the Department of Education are eligible. This includes Direct Loans, Federal Family Education Loans (FFEL) held by the government, and Perkins Loans. Private loans and commercially held FFEL loans are excluded. Additionally, the loans must have been disbursed before July 1, 2022. Borrowers with loans taken out after this date are not eligible for forgiveness under this plan. Double-checking your loan type and disbursement date is a critical step in determining your eligibility.

Steps to Verify Eligibility

To confirm eligibility, borrowers should log into their Federal Student Aid account or contact their loan servicer. The Department of Education has also provided an online tool to help borrowers check their status. If your income falls within the thresholds and your loans meet the type and disbursement criteria, you’re likely eligible. However, if your income exceeds the limits, you may still qualify if you received a Pell Grant. Keep your tax documents handy, as they will be necessary for verification.

Cautions and Common Pitfalls

While the eligibility criteria seem straightforward, there are potential pitfalls. For instance, borrowers in default on their federal loans may face complications. Although defaulted loans are technically eligible, resolving the default status is often required before forgiveness can be applied. Additionally, borrowers with commercially held FFEL loans may mistakenly assume eligibility, only to find their loans excluded. Always verify your loan type and status to avoid disappointment. Lastly, beware of scams—official communications regarding loan forgiveness will come directly from the Department of Education or your loan servicer.

Understanding the eligibility criteria is the first step toward securing student loan forgiveness. By carefully reviewing your income, loan type, and disbursement date, you can determine whether you qualify. Stay informed about updates, as legal challenges and policy changes may impact the program’s implementation. Taking proactive steps now can help you navigate this complex process and potentially reduce your student loan burden significantly.

Unlocking Debt-Free Future: Guide to Federal Student Loan Forgiveness

You may want to see also

Explore related products

![]()

Impact on federal vs. private loans

The Biden administration's student loan forgiveness plan has sparked a critical distinction between federal and private loans, leaving many borrowers wondering where they stand. While the proposal aims to alleviate the burden of educational debt, its impact is not uniform across the lending landscape. Federal student loans, backed by the government, are the primary focus of this relief effort, with eligible borrowers potentially receiving up to $10,000 in forgiveness, or $20,000 for Pell Grant recipients. This targeted approach is a strategic move to address the growing crisis in federal student lending, which accounts for the majority of outstanding educational debt in the United States.

In contrast, private student loans, issued by banks, credit unions, and other financial institutions, are largely excluded from this forgiveness initiative. These loans, often characterized by higher interest rates and less flexible repayment options, will not receive direct relief under the current plan. Borrowers with private loans may feel a sense of disparity, as their financial obligations remain unchanged while their federal loan-holding counterparts experience significant debt reduction. This divide highlights the complex nature of the student lending system and the challenges in creating a one-size-fits-all solution.

The exclusion of private loans from forgiveness programs is not without reason. Federal loans are governed by a set of standardized rules and regulations, making them more amenable to large-scale policy changes. Private lenders, on the other hand, operate under diverse terms and conditions, making it difficult to implement a uniform forgiveness strategy. Moreover, private loans are not subsidized by the government, and lenders may be less inclined to offer relief without a clear financial incentive. As a result, borrowers with private student debt must explore alternative avenues for managing their loans, such as refinancing or negotiating with lenders for more favorable terms.

For those with a mix of federal and private loans, the impact of the forgiveness plan can be both a blessing and a logistical challenge. While the reduction in federal debt is a welcome relief, borrowers must carefully navigate their remaining private loan obligations. This may involve prioritizing high-interest private loans for repayment or seeking consolidation options to simplify their financial portfolio. Financial advisors recommend creating a comprehensive repayment strategy, taking into account the unique characteristics of each loan type, to maximize the benefits of the federal forgiveness program while minimizing the long-term costs of private debt.

In the broader context of student loan reform, the federal vs. private loan distinction underscores the need for a multifaceted approach. While the Biden administration's plan provides much-needed relief for federal borrowers, it also draws attention to the disparities in the lending system. Addressing these disparities may require future policy interventions, such as increased regulation of private lenders or the expansion of income-driven repayment plans to include private loans. As the debate over student debt forgiveness continues, borrowers must stay informed about their options, advocating for solutions that cater to the diverse needs of all loan holders.

Unlock Debt Freedom: Forgiving 100% of Your Student Loans

You may want to see also

Explore related products

![]()

Timeline for debt cancellation

The timeline for student debt cancellation under Biden’s plan has been a rollercoaster of legal battles and administrative hurdles. Initially announced in August 2022, the program aimed to forgive up to $10,000 in federal student loans for eligible borrowers, with an additional $10,000 for Pell Grant recipients. However, within weeks, lawsuits from Republican-led states and conservative groups halted implementation. By November 2022, the Supreme Court agreed to hear challenges to the program, effectively freezing it until a ruling was issued in June 2023. This delay left millions of borrowers in limbo, unsure of their financial futures.

Analyzing the timeline reveals a pattern of political and legal resistance. The Biden administration’s use of the HEROES Act of 2003 as the legal basis for debt cancellation was immediately contested. Critics argued it exceeded executive authority, while supporters claimed it was a necessary response to the economic fallout of the pandemic. The Supreme Court’s 6-3 decision in *Biden v. Nebraska* struck down the program, citing lack of congressional approval. This outcome underscores the fragility of executive actions in addressing systemic issues like student debt.

For borrowers, understanding the timeline is crucial for planning. From the initial announcement to the Supreme Court’s ruling, the process spanned nearly a year, during which payments and interest were paused. After the ruling, payments resumed in October 2023, with interest accruing again. Borrowers who had anticipated relief were forced to reevaluate their budgets. Practical tips include enrolling in income-driven repayment plans, exploring Public Service Loan Forgiveness, and staying informed about potential legislative solutions, such as the *Fresh Start* initiative proposed in 2024.

Comparatively, other debt relief programs, like the American Rescue Plan’s stimulus checks, faced fewer legal challenges and were implemented swiftly. Student debt cancellation, however, became a partisan battleground, highlighting the complexity of addressing long-term financial burdens through executive action. The timeline also exposes the need for bipartisan legislative solutions, as executive orders remain vulnerable to legal and political shifts.

Looking ahead, the timeline for debt cancellation remains uncertain. While the Biden administration has explored alternative pathways, such as targeted relief for specific groups, no large-scale program has been implemented. Borrowers should monitor updates from the Department of Education and consider refinancing private loans if eligible. The lesson from this timeline is clear: systemic change requires durable, bipartisan solutions, not temporary fixes.

Unlock NP Student Loan Forgiveness: Working in HPSA Areas Guide

You may want to see also

Explore related products

![]()

Tax implications of forgiveness

The Biden administration's proposal to forgive $10,000 in federal student loans per borrower has sparked debates about its economic impact, but one critical aspect often overlooked is the tax implications of such forgiveness. Under current tax laws, forgiven debt is generally treated as taxable income, which could result in unexpected tax bills for borrowers. For instance, if a borrower has $10,000 in student loans forgiven, the IRS may consider this amount as income, potentially pushing the borrower into a higher tax bracket. This raises the question: How can borrowers prepare for the tax consequences of loan forgiveness?

To mitigate the tax burden, borrowers should first understand the exceptions to the taxable income rule. The American Rescue Plan of 2021 temporarily exempts student loan forgiveness from federal taxation through 2025, provided the forgiveness occurs under specific programs, such as income-driven repayment plans or the Public Service Loan Forgiveness (PSLF) program. However, this exemption does not apply to all forgiveness scenarios, leaving some borrowers vulnerable. For example, if the $10,000 forgiveness is extended beyond 2025 or falls outside designated programs, it could become taxable. Borrowers should consult tax professionals to assess their individual situations and explore strategies like adjusting withholdings or making estimated tax payments to avoid penalties.

Another critical consideration is the interplay between federal and state tax laws. While federal tax exemptions may apply, many states treat forgiven student loans as taxable income, creating a patchwork of rules. For instance, states like California and New York have conformed to the federal exclusion, but others, such as Massachusetts and Virginia, have not. Borrowers must research their state’s tax laws or seek advice to determine their total tax liability. Ignoring state-level implications could lead to underpayment and additional financial strain.

Finally, proactive planning is essential for borrowers anticipating loan forgiveness. Those expecting a significant tax liability can set aside a portion of their savings to cover the bill or explore deductions and credits to offset the impact. For example, contributing to retirement accounts or claiming education-related tax credits can reduce taxable income. Additionally, borrowers should monitor legislative updates, as tax laws and forgiveness policies may evolve. Staying informed and prepared ensures that the relief of loan forgiveness isn’t overshadowed by unforeseen tax obligations.

Unlocking Debt Freedom: A Guide to Forgiving Federal Student Loans

You may want to see also

Explore related products

![]()

Public reaction and political debate

The announcement of President Biden's plan to forgive $10,000 in student loans per borrower sparked a firestorm of public reaction, with responses ranging from jubilant relief to outraged criticism. Social media platforms became battlegrounds, with hashtags like #CancelStudentDebt and #NoFreeRide trending as supporters and opponents clashed over the policy's fairness and economic implications. This immediate and intense response underscored the deeply personal and politically charged nature of student debt relief.

Analyzing the debate reveals a stark divide along generational and ideological lines. Younger Americans, particularly those burdened by six-figure debts, hailed the move as a lifeline, sharing stories of delayed homeownership, marriage, and family planning due to financial strain. In contrast, older generations, many of whom paid off their loans without assistance, criticized the plan as an unfair subsidy, arguing it penalizes fiscal responsibility. This generational rift highlights broader tensions over economic opportunity and intergenerational equity.

Politically, the debate has become a litmus test for party loyalty and policy priorities. Democrats framed the forgiveness as a progressive step toward addressing systemic inequality, while Republicans decried it as fiscally irresponsible and a misuse of taxpayer funds. Legal challenges further complicated the issue, with lawsuits questioning the administration’s authority to enact such broad relief without congressional approval. This partisan standoff reflects the difficulty of achieving consensus on a policy with such far-reaching consequences.

Practical considerations also shaped public opinion. Critics questioned the plan’s long-term impact on college tuition, suggesting that forgiveness could incentivize institutions to raise prices further. Proponents countered that relief would stimulate the economy by freeing up disposable income for millions of borrowers. These competing narratives illustrate the challenge of balancing immediate relief with sustainable solutions to the student debt crisis.

Ultimately, the public reaction and political debate over Biden’s $10,000 forgiveness plan reveal a society grappling with the complexities of economic fairness and policy trade-offs. While the initiative offers tangible relief to millions, it also exposes deeper divisions over who should bear the cost of education and how to address systemic inequalities. As the debate continues, it serves as a reminder that student debt is not just a financial issue but a reflection of broader societal values and priorities.

Student Loan Forgiveness After Death: What Happens to Debt?

You may want to see also

Frequently asked questions

No, President Biden’s student loan forgiveness plan targets specific borrowers. The $10,000 forgiveness applies to federal student loan borrowers earning less than $125,000 annually ($250,000 for married couples). Pell Grant recipients may qualify for up to $20,000 in forgiveness.

The timeline for forgiveness depends on legal challenges. As of now, the program is on hold due to court battles. Borrowers should monitor updates from the Department of Education for the latest information.

No, only federal student loans are eligible for the $10,000 forgiveness. Private loans are not included in President Biden’s plan.

The forgiven amount is not considered taxable income under the American Rescue Plan Act of 2021, which excludes student loan forgiveness from federal taxation through 2025. However, state tax laws may vary.

![The Debt [Blu-ray]](https://m.media-amazon.com/images/I/81CZAuyNzeL._AC_UL320_.jpg)