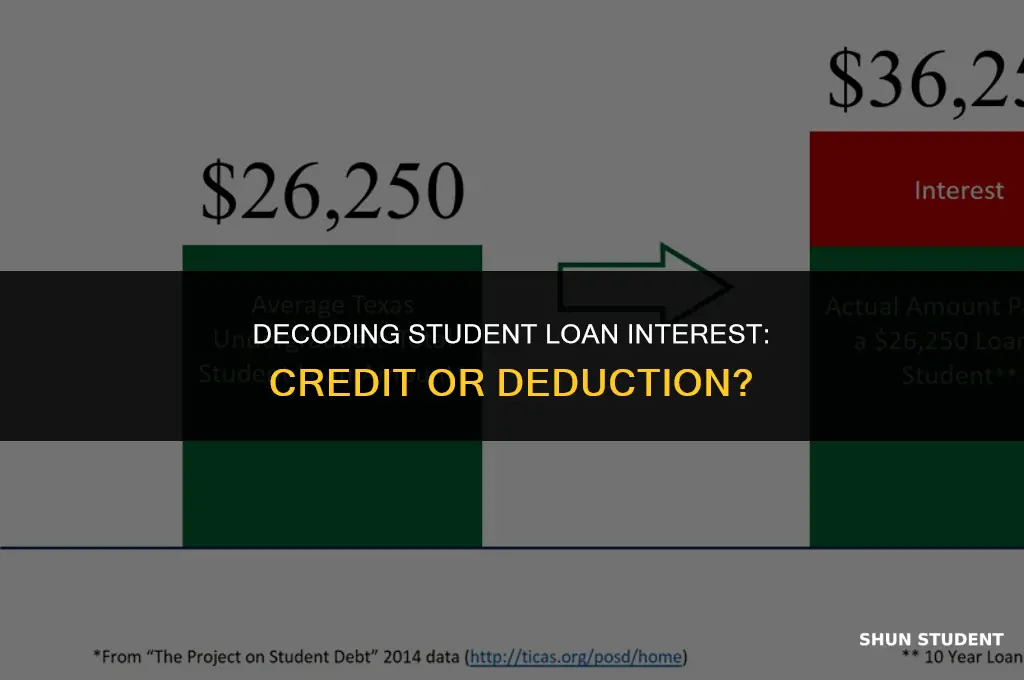

When it comes to student loans, understanding the tax implications is crucial. One common question borrowers face is whether the interest paid on student loans is considered a credit or a deduction. In the context of tax filing, a credit directly reduces the amount of tax owed, while a deduction reduces the taxable income. For student loan interest, the IRS allows borrowers to deduct up to $2,500 of interest paid annually, provided certain conditions are met. This deduction can help lower the taxable income, potentially resulting in a smaller tax bill. However, it's important to note that this deduction is subject to income limits and other restrictions, so not all borrowers may qualify.

| Characteristics | Values |

|---|---|

| Type of Expense | Interest on student loans |

| Tax Treatment | Deduction |

| Eligibility Criteria | Must have paid interest on a qualified student loan during the tax year |

| Maximum Deduction Amount | $2,500 per year |

| Income Limitations | Phase-out begins at $70,000 for single filers and $140,000 for joint filers |

| Documentation Required | Form 1098-E (Student Loan Interest Statement) |

| Impact on Tax Liability | Reduces taxable income, potentially lowering tax owed |

| Availability | Available for federal income tax returns |

| Retroactive Application | No, only applicable for the current tax year |

| Interaction with Other Tax Benefits | Can be used in conjunction with other education-related tax benefits |

| Filing Status Impact | Available for all filing statuses, but income limitations vary |

| Dependent Impact | If a parent pays the interest, they may be able to claim the deduction |

| Loan Type Eligibility | Eligible for federal and private student loans |

| Interest Payment Timing | Must have been paid during the tax year |

| Refinancing Impact | Refinancing a student loan may affect the interest deduction |

| Forgiveness Programs | Interest forgiven under certain programs may not be deductible |

Explore related products

What You'll Learn

- Understanding Student Loan Interest: Basics of how interest accrues on student loans and its impact on repayment

- Tax Implications: Exploring whether student loan interest is tax-deductible and how to claim it on tax returns

- Credit Score Effects: Analyzing how student loan interest payments influence credit scores and financial health

- Repayment Strategies: Tips and strategies for managing and repaying student loans efficiently to minimize interest costs

- Current Legislation and Changes: Updates on laws and policies affecting student loan interest rates and repayment options

![]()

Understanding Student Loan Interest: Basics of how interest accrues on student loans and its impact on repayment

Student loan interest accrues based on a percentage of the outstanding loan balance. This percentage, known as the interest rate, can be fixed or variable, depending on the type of loan. For federal student loans, the interest rate is set by Congress and remains fixed for the life of the loan. Private student loans, on the other hand, may have variable interest rates that can change over time based on market conditions.

Interest on student loans typically begins accruing as soon as the loan is disbursed. However, for subsidized federal student loans, the government pays the interest while the borrower is in school, during the grace period, and during any periods of deferment. For unsubsidized federal student loans and private student loans, the borrower is responsible for paying the interest that accrues during these periods.

The impact of interest on student loan repayment can be significant. Over time, interest can increase the total amount owed on the loan, making it more difficult to pay off. This is why it's important for borrowers to understand how interest accrues and to make payments on time to minimize the amount of interest that is added to their loan balance.

One strategy for managing student loan interest is to make payments while in school or during the grace period, even if they are not required. This can help reduce the amount of interest that accrues over time. Additionally, borrowers can consider refinancing their student loans to a lower interest rate, which can also help reduce the total amount owed.

In conclusion, understanding how interest accrues on student loans is crucial for managing repayment. By making timely payments and considering strategies to reduce interest, borrowers can take control of their student loan debt and work towards financial stability.

BCC Student Representation: Which Organization Advocates for Campus Interests?

You may want to see also

Explore related products

![]()

Tax Implications: Exploring whether student loan interest is tax-deductible and how to claim it on tax returns

The tax implications of student loan interest can be a significant concern for borrowers. In many countries, including the United States, student loan interest is tax-deductible, which can provide a valuable benefit when filing tax returns. To claim this deduction, borrowers must meet certain criteria and follow specific steps.

First, it's essential to determine if the student loan interest is eligible for deduction. In the U.S., for example, the interest must be paid on a qualified student loan, which is a loan taken out solely for the purpose of paying for higher education expenses. Additionally, the borrower must be the one who is legally responsible for repaying the loan, and the interest must be paid during the tax year for which the deduction is being claimed.

To claim the student loan interest deduction, borrowers must fill out the appropriate tax form, which in the U.S. is Form 1040. They will need to provide information about the loan, including the lender's name, the amount of interest paid, and the borrower's adjusted gross income. It's important to keep accurate records of student loan interest payments, as these will be needed to substantiate the deduction.

One common mistake borrowers make is to overlook the student loan interest deduction or to claim it incorrectly. To avoid this, it's crucial to carefully review the tax form instructions and to consult with a tax professional if necessary. Additionally, borrowers should be aware of any changes to tax laws that may affect the student loan interest deduction, as these can impact their tax liability.

In conclusion, the student loan interest deduction can provide a valuable tax benefit for borrowers who meet the eligibility criteria. By understanding the requirements and following the proper steps, borrowers can ensure that they take full advantage of this deduction and minimize their tax liability.

When Do Unsub Student Loans Begin Accruing Interest?

You may want to see also

Explore related products

$14.87 $15.95

![]()

Credit Score Effects: Analyzing how student loan interest payments influence credit scores and financial health

Student loan interest payments can have a significant impact on an individual's credit score and overall financial health. When borrowers make timely interest payments on their student loans, it demonstrates responsible credit behavior, which can positively influence their credit score. This is because credit scoring models, such as FICO and VantageScore, consider payment history as a critical factor in determining creditworthiness.

However, the relationship between student loan interest payments and credit scores is not straightforward. While on-time payments can boost credit scores, late or missed payments can have detrimental effects. A single late payment can result in a credit score drop, and multiple late payments can lead to a substantial decrease in creditworthiness. Furthermore, high student loan balances can contribute to a higher debt-to-income ratio, which can also negatively impact credit scores.

It's essential to note that interest payments on student loans are not tax-deductible, unlike mortgage interest payments. This means that borrowers cannot reduce their taxable income by deducting student loan interest payments, which can further strain their financial situation. Additionally, the interest rates on student loans can be relatively high, especially for private loans, which can lead to a significant increase in the total amount paid over the life of the loan.

To mitigate the negative effects of student loan interest payments on credit scores and financial health, borrowers can consider various strategies. One approach is to prioritize making on-time payments by setting up automatic payments or using a budgeting app to track due dates. Borrowers can also explore options for reducing their interest rates, such as refinancing with a private lender or consolidating federal loans to qualify for a lower interest rate.

In conclusion, student loan interest payments can have a profound impact on credit scores and financial well-being. By understanding the relationship between interest payments and credit scores, borrowers can take proactive steps to manage their student loan debt and maintain a healthy financial profile.

When Does Student Loan Interest End: A Complete Guide

You may want to see also

Explore related products

![]()

Repayment Strategies: Tips and strategies for managing and repaying student loans efficiently to minimize interest costs

One effective strategy for managing student loan debt is to prioritize high-interest loans for repayment first. This approach, known as the avalanche method, involves making minimum payments on all loans while directing any extra funds towards the loan with the highest interest rate. By tackling the most expensive debt first, borrowers can reduce the overall interest paid over the life of the loans.

Another strategy is to consolidate multiple student loans into a single loan with a lower interest rate. Loan consolidation can simplify repayment by combining several monthly payments into one, and it may also result in a lower monthly payment if the new loan has a longer repayment term. However, borrowers should be cautious about extending the repayment term too long, as this could lead to paying more interest over time.

Income-driven repayment plans are another option for managing student loan debt. These plans adjust the monthly payment amount based on the borrower's income and family size, making it more manageable for those with lower incomes. While these plans can provide temporary relief, borrowers should be aware that they may not cover the full interest accrued, potentially leading to a larger balance over time.

Refinancing student loans is another strategy to consider. By refinancing, borrowers can potentially secure a lower interest rate, which can save money on interest payments. However, refinancing federal student loans may result in the loss of certain benefits, such as income-driven repayment options and loan forgiveness programs. Borrowers should carefully weigh the pros and cons before deciding to refinance.

Lastly, borrowers should take advantage of any employer-sponsored repayment assistance programs. Some employers offer to match a portion of the employee's student loan payments, which can help accelerate debt repayment. Additionally, borrowers should explore tax deductions for student loan interest, which can provide some financial relief.

In conclusion, managing and repaying student loans efficiently requires a strategic approach. By prioritizing high-interest loans, consolidating debt, exploring income-driven repayment plans, considering refinancing, and taking advantage of employer-sponsored programs and tax deductions, borrowers can minimize interest costs and pay off their student loans more effectively.

Decline in Student Reading Interest: Causes and Solutions

You may want to see also

Explore related products

![]()

Current Legislation and Changes: Updates on laws and policies affecting student loan interest rates and repayment options

Recent legislative changes have significantly impacted student loan interest rates and repayment options. The Bipartisan Student Loan Relief Act of 2022, for instance, introduced a temporary reduction in interest rates for undergraduate loans, capping them at 3.73% for the 2022-2023 academic year. This reduction aims to alleviate the financial burden on students and recent graduates. Additionally, the Act expanded eligibility for income-driven repayment plans, allowing more borrowers to qualify for lower monthly payments based on their income and family size.

Another notable development is the extension of the Public Service Loan Forgiveness (PSLF) program. Initially set to expire in 2022, the program has been extended to 2023, providing additional opportunities for borrowers who work in public service sectors to have their loans forgiven after meeting specific repayment and employment criteria. This extension is particularly beneficial for those in lower-paying public service roles, such as teachers, nurses, and social workers.

Furthermore, the Department of Education has proposed new regulations aimed at simplifying the Free Application for Federal Student Aid (FAFSA) process. These changes, set to take effect in the 2024-2025 academic year, will reduce the number of questions on the FAFSA form and streamline the application process, making it easier for students and families to apply for federal student aid. This simplification is expected to increase access to financial aid for low-income students and reduce the administrative burden on families.

In addition to federal legislation, several states have also implemented their own student loan relief programs. For example, California recently introduced the California Student Loan Relief Act, which provides financial assistance to borrowers who have taken out private student loans. This state-level intervention highlights the growing recognition of the need for comprehensive student loan reform at both the federal and state levels.

Overall, these legislative and policy changes reflect a concerted effort to address the student loan crisis and provide relief to borrowers. By reducing interest rates, expanding repayment options, and simplifying the financial aid application process, these measures aim to make higher education more affordable and accessible for all students.

Decline in Teen Reading: Understanding the Shift Away from Books

You may want to see also

Frequently asked questions

Interest on student loans is generally considered a deduction. This means that you can subtract the interest you pay on your student loans from your taxable income, potentially lowering your tax bill.

To qualify for the student loan interest deduction, you must meet certain criteria. Typically, you must be legally obligated to repay the student loan, the loan must be used solely for qualified education expenses, and you must be enrolled at least half-time in a degree program.

The maximum amount of student loan interest you can deduct varies depending on the tax year and your income level. It's important to consult the latest tax guidelines or a tax professional to determine the exact limit for your specific situation.

Generally, only the person who is legally obligated to repay the student loan can claim the interest deduction. This means that if a parent or someone else took out the loan on your behalf, they would be the one eligible to claim the deduction, not you.