Understanding when student loan interest cuts out is crucial for borrowers looking to manage their debt effectively. Typically, interest accrual on student loans ceases under specific conditions, such as when the loan is fully paid off, during certain deferment periods, or when the borrower qualifies for loan forgiveness programs like Public Service Loan Forgiveness (PSLF). Additionally, some federal student loans offer interest-free periods during in-school enrollment or grace periods after graduation. Private loans, however, often have different terms, and interest may continue to accrue unless explicitly stated otherwise. Knowing these details can help borrowers strategize payments and minimize long-term costs.

| Characteristics | Values |

|---|---|

| Interest Accrual During Grace Period | Depends on loan type:

|

| Interest Accrual During Deferment |

|

| Interest Accrual During Forbearance | Interest accrues on all federal and private loans during forbearance. |

| Income-Driven Repayment Plans | Interest may be subsidized by the government, depending on the plan and income level. |

| Loan Forgiveness Programs | Interest may be forgiven under programs like Public Service Loan Forgiveness (PSLF) after meeting eligibility criteria. |

| Private Student Loans | Interest accrual policies vary by lender; no standard grace period or deferment rules. |

| Federal Student Loan Pause (COVID-19) | Interest was temporarily set to 0% from March 2020 to September 2023 under emergency relief measures. |

| Loan Payoff | Interest stops accruing once the loan is fully paid off. |

| Death or Disability Discharge | Interest stops accruing upon approval of discharge due to death or total and permanent disability. |

| Bankruptcy Discharge | Rarely discharges student loans, but if successful, interest stops accruing. |

Explore related products

What You'll Learn

- Income-Driven Repayment Plans: Interest forgiveness after 20-25 years of consistent payments under these plans

- Public Service Loan Forgiveness: Interest waived after 120 qualifying payments for eligible public service workers

- Loan Deferment Periods: Interest may stop accruing temporarily during approved deferment periods

- Subsidized vs. Unsubsidized Loans: Government pays interest on subsidized loans during school, grace, and deferment

- Loan Payoff Strategies: Paying more than minimum can reduce interest faster, cutting it out sooner

![]()

Income-Driven Repayment Plans: Interest forgiveness after 20-25 years of consistent payments under these plans

Income-Driven Repayment (IDR) plans are designed to make federal student loan payments more manageable by capping monthly payments at a percentage of the borrower’s discretionary income. One of the most significant benefits of these plans is the potential for interest forgiveness after 20-25 years of consistent payments, depending on the specific plan. This feature is particularly valuable for borrowers with high loan balances relative to their income, as it provides a pathway to loan forgiveness and prevents interest from indefinitely accruing. Under IDR plans, if a borrower makes all qualifying payments for the required period (20 or 25 years), any remaining loan balance, including unpaid interest, is forgiven. This means that even if interest continues to accrue and exceeds the borrower’s monthly payments, it will eventually be discharged, effectively "cutting out" the interest burden after the designated repayment period.

The four main IDR plans—Revised Pay As You Earn (REPAYE), Pay As You Earn (PAYE), Income-Based Repayment (IBR), and Income-Contingent Repayment (ICR)—each have different terms for interest forgiveness. For example, under REPAYE, any unpaid interest is forgiven annually if it exceeds the borrower’s monthly payment, but the 20- or 25-year forgiveness timeline still applies. For PAYE and IBR, interest forgiveness occurs after 20 years of payments, while ICR requires 25 years. It’s important to note that the forgiven amount may be considered taxable income, though current laws provide temporary tax-free treatment for forgiven balances through 2025. Borrowers should consult a tax professional to understand potential tax implications.

To qualify for interest forgiveness under IDR plans, borrowers must make consistent, on-time payments for the entire 20- or 25-year period. Payments made under other plans, such as the Standard Repayment Plan, do not count toward this timeline. Additionally, borrowers must recertify their income and family size annually to remain eligible for IDR plans. Missing recertification deadlines or failing to make payments on time can reset the forgiveness clock, delaying the point at which interest is forgiven. Staying in compliance with the plan’s requirements is crucial to maximizing this benefit.

Another critical aspect of IDR plans is how they handle interest accrual. If a borrower’s monthly payment is insufficient to cover the accruing interest, the unpaid interest may capitalize, adding to the loan’s principal balance. However, after 20 or 25 years of payments, any remaining balance, including capitalized interest, is forgiven. This makes IDR plans a powerful tool for borrowers struggling with high-interest rates, as it ensures that interest does not indefinitely compound and become unmanageable. Borrowers should carefully review their plan terms to understand how interest is treated and how it will be forgiven over time.

Finally, it’s essential for borrowers to choose the IDR plan that best aligns with their financial situation and goals. For instance, REPAYE may be more beneficial for borrowers with graduate school loans due to its interest subsidies, while PAYE or IBR might be better for those with lower incomes. Borrowers can use tools like the Federal Student Aid Loan Simulator to estimate their monthly payments and forgiveness timelines under different plans. By selecting the right plan and staying committed to the repayment terms, borrowers can effectively leverage the interest forgiveness feature of IDR plans to achieve long-term financial stability.

Discovering New Horizons: The Most Fascinating Aspect of Student Life

You may want to see also

Explore related products

![]()

Public Service Loan Forgiveness: Interest waived after 120 qualifying payments for eligible public service workers

The Public Service Loan Forgiveness (PSLF) program offers a unique opportunity for eligible public service workers to have their student loan interest waived after making 120 qualifying payments. This program is specifically designed to support individuals who dedicate their careers to public service, providing a pathway to financial relief and loan forgiveness. For those wondering when student loan interest cuts out, the PSLF program presents a clear and achievable goal. To qualify, borrowers must work full-time for a qualifying public service employer, such as government organizations, non-profit 501(c)(3) organizations, or other eligible entities. This program is particularly beneficial for individuals with substantial student loan debt who are committed to a career in public service.

To participate in the PSLF program and have interest waived after 120 qualifying payments, borrowers must first ensure their loans are eligible. Federal Direct Loans, including Direct Subsidized, Direct Unsubsidized, Direct PLUS, and Direct Consolidation Loans, are eligible for PSLF. Other federal loans, such as Federal Family Education Loans (FFEL) and Perkins Loans, may become eligible if consolidated into a Direct Consolidation Loan. It is crucial for borrowers to confirm their loan type and consider consolidation if necessary to qualify for PSLF. Additionally, borrowers must be enrolled in an income-driven repayment (IDR) plan to ensure their monthly payments are affordable and qualify for the program.

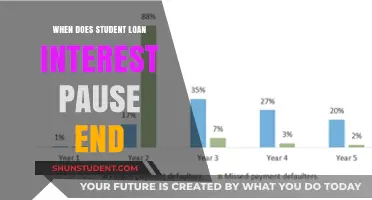

Making 120 qualifying payments is a key requirement for interest waiver and loan forgiveness under the PSLF program. These payments must be made on time, in full, and while working full-time for a qualifying public service employer. Borrowers should keep detailed records of their employment and payments, as they will need to submit an Employment Certification Form periodically and a PSLF application after completing the 120 payments. It is essential to note that only payments made after October 1, 2007, count toward the 120 required payments, and periods of economic hardship deferment or forbearance do not qualify. Staying organized and maintaining consistent payments are critical to successfully reaching the interest waiver milestone.

One of the most significant advantages of the PSLF program is that any remaining loan balance is forgiven tax-free after the 120 qualifying payments. Unlike other loan forgiveness programs, PSLF does not require borrowers to pay taxes on the forgiven amount, providing substantial financial relief. This feature makes PSLF particularly attractive for public service workers with high loan balances. However, borrowers must remain vigilant and ensure they meet all program requirements, as failing to do so could result in disqualification. Regularly reviewing the PSLF guidelines and staying in contact with loan servicers can help borrowers navigate the program successfully.

For eligible public service workers, the PSLF program offers a clear path to waiving student loan interest and achieving loan forgiveness. By committing to 120 qualifying payments while working in public service, borrowers can alleviate the burden of student loan debt and focus on their careers. It is essential to understand the program’s requirements, ensure loan eligibility, and maintain consistent payments to maximize the benefits of PSLF. For those seeking an answer to when student loan interest cuts out, the PSLF program provides a structured and rewarding solution, recognizing the valuable contributions of public service workers to society.

Navigating Student Loan Interest: Smart Choices for the Marketplace

You may want to see also

Explore related products

![]()

Loan Deferment Periods: Interest may stop accruing temporarily during approved deferment periods

Loan deferment periods offer a valuable opportunity for borrowers to temporarily pause their student loan payments, and in some cases, interest may stop accruing during this time. This can provide significant financial relief, especially for those facing economic hardship, returning to school, or serving in the military. Understanding the conditions under which interest accrual halts during deferment is crucial for managing student loan debt effectively. Generally, for federal student loans, interest does not accrue during deferment periods for subsidized loans, but it does continue to accrue for unsubsidized loans. This distinction is essential because it directly impacts the total amount owed once the deferment period ends.

For subsidized federal student loans, the government pays the interest during approved deferment periods, ensuring that the loan balance remains unchanged. This benefit is particularly advantageous for borrowers who qualify for deferment due to financial hardship or enrollment in school at least half-time. To take advantage of this, borrowers must apply for deferment through their loan servicer and meet specific eligibility criteria, such as demonstrating economic hardship or providing proof of enrollment. Once approved, they can rest assured that their subsidized loan balances will not grow during the deferment period.

In contrast, unsubsidized federal student loans and most private student loans continue to accrue interest during deferment. Borrowers with unsubsidized loans have the option to pay the interest as it accrues during the deferment period, which can prevent the interest from capitalizing and increasing the overall loan balance. If the interest is not paid, it will be added to the principal balance when the deferment period ends, leading to higher monthly payments and total repayment costs. Private student loans often have less flexible terms, and interest typically continues to accrue during deferment, regardless of the loan type.

To qualify for a deferment period, borrowers must meet specific eligibility requirements, which vary depending on the type of loan and the reason for deferment. Common reasons for deferment include economic hardship, unemployment, enrollment in school, and military service. Each of these categories has its own set of criteria, and borrowers must provide documentation to support their application. For example, economic hardship deferment may require proof of income or participation in a federal or state public assistance program. Understanding these requirements and preparing the necessary documentation can streamline the application process and increase the likelihood of approval.

It is also important for borrowers to be aware of the limitations and potential drawbacks of deferment periods. While deferment can provide temporary financial relief, it does not eliminate the debt, and in some cases, it can lead to higher overall repayment costs due to accruing interest. Borrowers should carefully consider their long-term financial goals and explore alternative options, such as income-driven repayment plans or loan forgiveness programs, which may offer more sustainable solutions. Additionally, staying in communication with the loan servicer and monitoring the loan status during deferment can help borrowers avoid surprises and make informed decisions about their student loan debt.

Understanding Limits: Why Taxpayers Can't Deduct All Student Loan Interest

You may want to see also

Explore related products

![]()

Subsidized vs. Unsubsidized Loans: Government pays interest on subsidized loans during school, grace, and deferment

When considering student loans, understanding the difference between subsidized and unsubsidized loans is crucial, especially in the context of when interest accrual stops or is covered. Subsidized loans are a type of federal student loan where the government pays the interest on your behalf while you are in school, during the grace period after graduation, and during any approved deferment periods. This benefit significantly reduces the overall cost of borrowing, as interest does not compound during these times. For example, if you borrow $5,000 in subsidized loans and attend school for four years, you will still owe only $5,000 upon graduation, as the government has covered the interest.

In contrast, unsubsidized loans do not offer this interest-free benefit. With unsubsidized loans, interest begins accruing as soon as the loan is disbursed, even while you are still in school. If you choose not to pay the interest as it accrues, it will be capitalized, meaning it is added to the principal balance of your loan. This can result in a larger total amount owed over time. For instance, if you borrow the same $5,000 in unsubsidized loans and do not pay the interest during school, the interest will compound, increasing the total repayment amount by the time you graduate.

The grace period, typically six months after graduation or leaving school, is another critical phase where the distinction between subsidized and unsubsidized loans becomes evident. For subsidized loans, the government continues to pay the interest during this period, giving borrowers time to find employment and prepare for repayment without the added burden of interest accrual. However, for unsubsidized loans, interest continues to accrue during the grace period, and borrowers are responsible for paying it or having it capitalized.

Deferment periods, which allow borrowers to temporarily pause loan payments due to economic hardship, enrollment in school, or other qualifying reasons, also highlight the difference. During deferment, the government pays the interest on subsidized loans, ensuring the balance does not grow. Conversely, for unsubsidized loans, interest continues to accrue during deferment, and borrowers must either pay the interest or allow it to capitalize, increasing the total debt.

In summary, the key takeaway is that subsidized loans offer a significant advantage by having the government pay the interest during school, grace periods, and deferment, which can save borrowers thousands of dollars over the life of the loan. Unsubsidized loans, while more readily available and not based on financial need, come with the drawback of continuous interest accrual from the moment the loan is disbursed. Understanding these differences is essential for making informed decisions about student loan borrowing and managing repayment effectively.

Understanding the Phase-Out of Student Loan Interest Deduction: What You Need to Know

You may want to see also

Explore related products

![]()

Loan Payoff Strategies: Paying more than minimum can reduce interest faster, cutting it out sooner

When it comes to student loans, understanding how interest accrues and when it can be minimized is crucial for borrowers aiming to pay off their debt efficiently. One of the most effective strategies to reduce the overall interest paid and cut it out sooner is by paying more than the minimum required payment each month. This approach directly targets the principal balance, which is the primary driver of interest accumulation. By allocating extra funds toward the principal, borrowers can significantly shorten the loan term and save thousands of dollars in interest over time.

The mechanics behind this strategy are straightforward: student loan interest is calculated based on the outstanding principal balance. When borrowers make only the minimum payment, a substantial portion of that payment goes toward interest rather than reducing the principal. However, by paying more than the minimum, a larger share of the payment is applied to the principal, thereby reducing the balance on which future interest is calculated. Over time, this compounds, leading to less interest accrual and a faster path to becoming debt-free.

To implement this strategy effectively, borrowers should first ensure their additional payments are designated specifically toward the principal balance. This often requires contacting the loan servicer to specify how the extra amount should be applied. Without this clarification, the additional payment might be treated as an advance on future minimum payments, which does not reduce the principal as intended. Additionally, borrowers should prioritize paying extra on loans with the highest interest rates first, as these accrue interest more quickly and contribute most to the overall debt burden.

Another key aspect of this strategy is consistency. Even small additional payments can make a difference over time, but regular and substantial extra payments yield the most significant results. For example, allocating an extra $50 or $100 per month toward the principal can shave years off the loan term. Borrowers can also consider making biweekly payments instead of monthly ones, effectively adding one extra payment per year without feeling the strain of a larger monthly commitment.

Finally, it’s important to monitor progress and adjust the strategy as financial circumstances change. Tools like loan payoff calculators can help borrowers visualize the impact of extra payments and stay motivated. As the principal balance decreases, the interest portion of each payment shrinks, accelerating the payoff process. By staying disciplined and committed to paying more than the minimum, borrowers can cut out student loan interest sooner and achieve financial freedom faster.

Average Student Loan Interest Rates in the Year 2000 Revealed

You may want to see also

Frequently asked questions

Student loan interest generally stops accruing when the loan is fully paid off, forgiven, or discharged. Additionally, interest may temporarily stop accruing during certain deferment or forbearance periods, depending on the type of loan.

For subsidized federal student loans, interest does not accrue while you are enrolled in school at least half-time. For unsubsidized loans, interest begins accruing immediately, but you can choose to pay it while in school to avoid capitalization.

For subsidized federal loans, interest does not accrue during deferment. For unsubsidized loans and private loans, interest typically continues to accrue during both deferment and forbearance, unless specified otherwise by the lender.

Student loan interest does not automatically stop based on age or retirement. However, borrowers may qualify for income-driven repayment plans or loan forgiveness programs that could reduce or eliminate payments, indirectly affecting interest accrual.