When it comes to understanding student loan interest rates, one crucial aspect to consider is whether the interest is compounded yearly. Compound interest is a powerful financial concept where the interest earned on a principal amount is reinvested, leading to exponential growth over time. In the context of student loans, if the interest rate is compounded yearly, it means that the interest accrued throughout the year is added to the principal balance at the end of the year, and subsequent interest calculations are based on this new, higher balance. This can significantly impact the total amount repaid over the life of the loan. To determine if a student loan's interest rate is compounded yearly, borrowers should carefully review their loan agreement or contact their lender for clarification. Understanding this detail is essential for making informed decisions about loan repayment strategies and managing overall financial health.

Explore related products

What You'll Learn

- Understanding Compound Interest: Explanation of how interest accrues on student loans annually

- Yearly Compounding Impact: Detailed breakdown of how yearly compounding affects loan repayment amounts

- Student Loan Repayment Strategies: Tips and strategies for managing and repaying student loans efficiently

- Fixed vs. Variable Interest Rates: Comparison of fixed and variable interest rates on student loans

- Calculating Yearly Compound Interest: Step-by-step guide on calculating compound interest on student loans

![]()

Understanding Compound Interest: Explanation of how interest accrues on student loans annually

Compound interest is a powerful financial concept that can significantly impact the total amount you pay on a student loan. Unlike simple interest, which is calculated only on the principal amount borrowed, compound interest accrues on both the principal and any accumulated interest. This means that over time, the interest you owe can grow exponentially, leading to a higher overall cost of borrowing.

To understand how compound interest works on student loans, it's essential to know that interest is typically calculated and added to the loan balance annually. This annual compounding can lead to a snowball effect, where the interest charges become increasingly larger each year. For example, if you borrow $10,000 at a 6% interest rate, the first year you would owe $600 in interest, bringing your total balance to $10,600. The following year, the 6% interest rate would apply to the new balance of $10,600, resulting in an interest charge of $636. This process continues each year, with the interest charges growing larger as the loan balance increases.

One of the key factors that influence the impact of compound interest on student loans is the frequency of compounding. While interest is typically added to the loan balance annually, some loans may compound interest more frequently, such as quarterly or monthly. More frequent compounding can lead to even higher interest charges over time, as the interest is added to the balance more often, allowing it to grow at a faster rate.

To minimize the impact of compound interest on your student loan, it's important to make regular payments and pay more than the minimum amount due whenever possible. By doing so, you can reduce the principal balance and lower the amount of interest that accrues over time. Additionally, consider refinancing your loan to a lower interest rate or exploring other repayment options that may help you save money on interest charges.

In conclusion, understanding how compound interest works on student loans is crucial for managing your debt effectively. By recognizing the exponential growth of interest charges and taking steps to minimize their impact, you can save money and pay off your loan more quickly.

Understanding Income Limits for Claiming Student Loan Interest Deductions

You may want to see also

Explore related products

![]()

Yearly Compounding Impact: Detailed breakdown of how yearly compounding affects loan repayment amounts

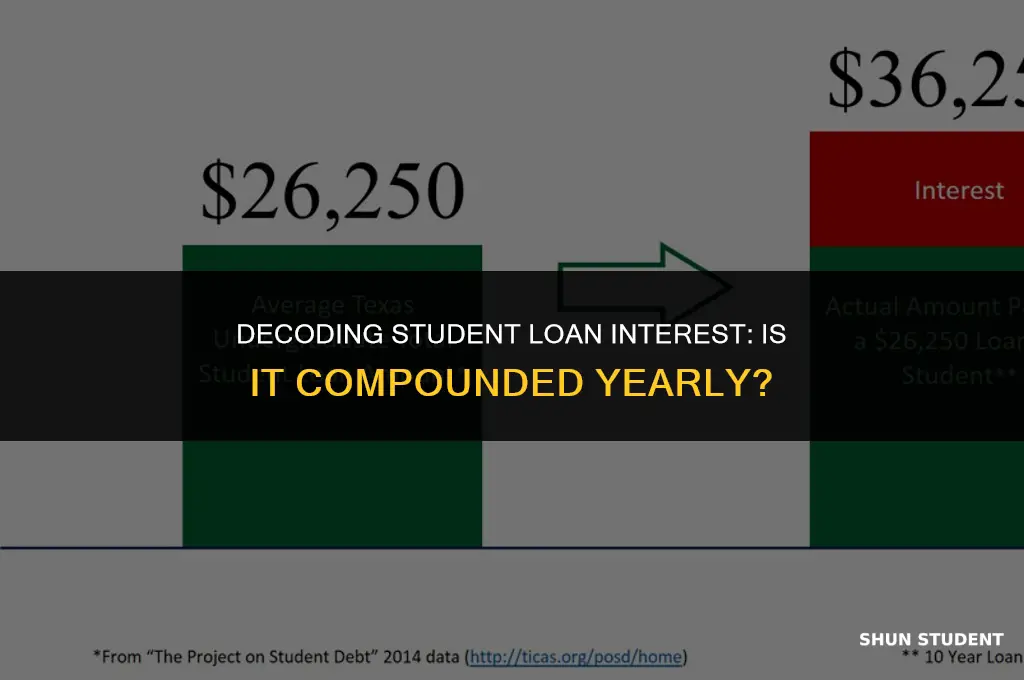

Yearly compounding significantly impacts the total amount repaid on a student loan. To understand this effect, consider a hypothetical scenario: a student borrows $20,000 at a 6% annual interest rate, compounded yearly, with a 10-year repayment term. The first year's interest charge would be $1,200 (6% of $20,000), increasing the loan balance to $21,200. In the second year, the interest charge would be $1,272 (6% of $21,200), raising the balance to $22,472. This pattern continues, with each year's interest charge calculated on the growing loan balance.

Over the 10-year repayment period, the total interest paid would amount to $9,448, in addition to the original $20,000 principal, resulting in a total repayment of $29,448. This example illustrates how yearly compounding can substantially increase the cost of borrowing, emphasizing the importance of understanding the long-term implications of student loan interest rates.

To mitigate the effects of yearly compounding, borrowers can consider making extra payments towards the principal balance whenever possible. Even small, consistent payments can help reduce the overall interest paid and shorten the repayment term. Additionally, borrowers may benefit from exploring loan consolidation or refinancing options that offer lower interest rates or more favorable repayment terms.

In conclusion, yearly compounding can have a profound impact on student loan repayment amounts. By understanding this concept and taking proactive steps to manage their debt, borrowers can potentially save thousands of dollars in interest charges over the life of their loans.

Reigniting Student Engagement: Strategies Teachers Can Use to Rekindle Interest

You may want to see also

Explore related products

![]()

Student Loan Repayment Strategies: Tips and strategies for managing and repaying student loans efficiently

Understanding how interest accrues on your student loan is crucial for developing an effective repayment strategy. If your loan's interest rate is compounded yearly, it means that the interest you owe is calculated once a year based on the principal balance at that time. This can significantly impact your repayment plan, as the interest can add up quickly if not managed properly.

One strategy to consider is making more than the minimum monthly payment. By paying extra each month, you can reduce the principal balance more quickly, which in turn reduces the amount of interest that accrues over time. This can save you money in the long run and help you pay off your loan faster.

Another option is to make bi-weekly payments instead of monthly ones. By doing this, you'll make 26 payments per year instead of 12, which can help you pay down the principal balance more quickly and reduce the interest that compounds annually.

If you have multiple student loans with different interest rates, consider focusing on paying off the loan with the highest interest rate first. This will help you save money on interest charges and can make it easier to manage your overall debt.

Finally, it's important to stay informed about any changes to your loan's interest rate or repayment terms. Keep track of your loan balance and interest charges, and don't hesitate to contact your lender if you have any questions or concerns. By staying proactive and informed, you can better manage your student loan debt and avoid costly mistakes.

Decoding the Tax Code: Understanding Student Loan Interest Deductions

You may want to see also

Explore related products

![]()

Fixed vs. Variable Interest Rates: Comparison of fixed and variable interest rates on student loans

When considering student loans, one of the critical decisions borrowers face is choosing between fixed and variable interest rates. This choice can significantly impact the total cost of the loan and the borrower's financial situation over time. Fixed interest rates remain constant throughout the life of the loan, providing predictability and stability in monthly payments. In contrast, variable interest rates fluctuate based on market conditions, which can lead to changes in the amount of interest charged each month.

One key advantage of fixed interest rates is their predictability. Borrowers know exactly how much they will pay each month, which can help with budgeting and financial planning. This stability can be particularly beneficial for those who prefer a consistent financial routine and want to avoid the uncertainty of fluctuating payments. Additionally, fixed interest rates often come with caps on the maximum interest rate, protecting borrowers from excessive increases if market rates rise sharply.

On the other hand, variable interest rates can offer lower initial rates compared to fixed rates, which can result in lower monthly payments at the beginning of the loan term. This can be an attractive option for borrowers who expect to have a higher income in the future or plan to refinance the loan before the rates increase significantly. Variable rates can also provide flexibility, as they may decrease if market conditions change favorably, potentially reducing the overall cost of the loan.

However, variable interest rates also carry risks. If market rates increase, the borrower's monthly payments can rise, making it more challenging to manage finances. This unpredictability can be stressful and may lead to difficulties in long-term financial planning. Furthermore, variable rates often lack caps, exposing borrowers to the possibility of very high interest charges if market conditions worsen.

In conclusion, the choice between fixed and variable interest rates on student loans depends on the borrower's financial situation, risk tolerance, and long-term goals. Fixed rates offer stability and predictability, while variable rates provide flexibility and potentially lower initial costs. Borrowers should carefully consider their options and consult with financial advisors to make informed decisions that align with their individual needs and circumstances.

Why Student Loan Interest Rates Rise: Key Factors Explained

You may want to see also

Explore related products

![]()

Calculating Yearly Compound Interest: Step-by-step guide on calculating compound interest on student loans

To calculate yearly compound interest on student loans, you'll need to understand the formula and the variables involved. The compound interest formula is A = P(1 + r/n)^(nt), where A is the amount of money accumulated after n compounding periods, P is the principal amount (the initial amount of the loan), r is the annual interest rate (decimal form), n is the number of times that interest is compounded per year, and t is the time the money is invested or borrowed for, in years.

Let's break down the steps to calculate the compound interest on a student loan:

- Identify the principal amount (P) of your student loan. This is the initial amount you borrowed.

- Determine the annual interest rate (r) of your loan. This rate is usually provided by the lender.

- Find out how many times the interest is compounded per year (n). This information should also be provided by the lender.

- Calculate the total number of compounding periods (nt) by multiplying the number of compounding periods per year (n) by the number of years you have the loan (t).

- Plug these values into the compound interest formula: A = P(1 + r/n)^(nt).

- Calculate the result to find the total amount you will owe after the specified time period, including the compound interest.

For example, let's say you have a student loan of $10,000 with an annual interest rate of 6% that is compounded quarterly. You want to know how much you will owe after 5 years.

- P = $10,000

- R = 6% = 0.06

- N = 4 (quarterly compounding)

- Nt = 4 * 5 = 20

- A = $10,000(1 + 0.06/4)^(20)

- A ≈ $13,488.30

So, after 5 years, you will owe approximately $13,488.30 on your student loan, including the compound interest.

Remember, the key to accurately calculating compound interest is to ensure you have the correct values for the principal amount, annual interest rate, number of compounding periods per year, and total number of compounding periods. Always double-check your calculations to avoid any errors.

Decoding the Intrigue: Why Student Loans Captivate Our Interest

You may want to see also

Frequently asked questions

If the interest rate for a student loan is compounded yearly, it means that the interest accrued over the year is added to the principal balance at the end of the year, and the new principal balance will earn interest in the following year. This can lead to a higher total amount paid over the life of the loan compared to more frequent compounding periods.

Yearly compounding can increase the total cost of a student loan because the interest is added to the principal balance less frequently, allowing the interest to grow over a longer period before being paid off. This results in a higher total amount of interest paid over the life of the loan, which increases the overall cost.

Yearly compounding is not the most common method for student loans. More frequently, interest is compounded daily, monthly, or quarterly. However, yearly compounding may be used in some cases, particularly for certain types of loans or in specific countries. It's important to check the terms of your loan to understand how interest is compounded.