Student loan interest rates can increase due to a variety of factors, often tied to broader economic conditions and the type of loan itself. For federal student loans, interest rates are typically set annually by Congress and are based on the 10-year Treasury note yield, plus a fixed margin, which can fluctuate depending on market trends and government policy. Private student loans, on the other hand, are influenced by the borrower’s creditworthiness, with higher interest rates often assigned to those with lower credit scores or insufficient credit history. Additionally, variable-rate loans may rise in response to changes in benchmark interest rates, such as the Prime Rate or LIBOR, while economic factors like inflation and Federal Reserve decisions can also drive up borrowing costs across the board. Understanding these dynamics is crucial for borrowers seeking to manage their student loan debt effectively.

| Characteristics | Values |

|---|---|

| Federal Student Loan Rates | Tied to 10-year Treasury note yield + margin (set by Congress) |

| Economic Conditions | Higher inflation or rising federal borrowing costs increase rates |

| Loan Type | Unsubsidized loans generally have higher rates than subsidized loans |

| Repayment Plan | Income-driven plans may capitalize interest, increasing total balance |

| Credit History | Private loans: Poor credit leads to higher interest rates |

| Loan Term | Longer repayment terms often result in higher total interest paid |

| Market Trends | Rising federal funds rate can indirectly influence student loan rates |

| Legislative Changes | Congressional decisions on rate caps or formulas impact rates |

| Loan Consolidation | Consolidation may reset interest rates based on current market rates |

| Forbearance/Deferment | Interest capitalization during pauses can increase total loan balance |

Explore related products

What You'll Learn

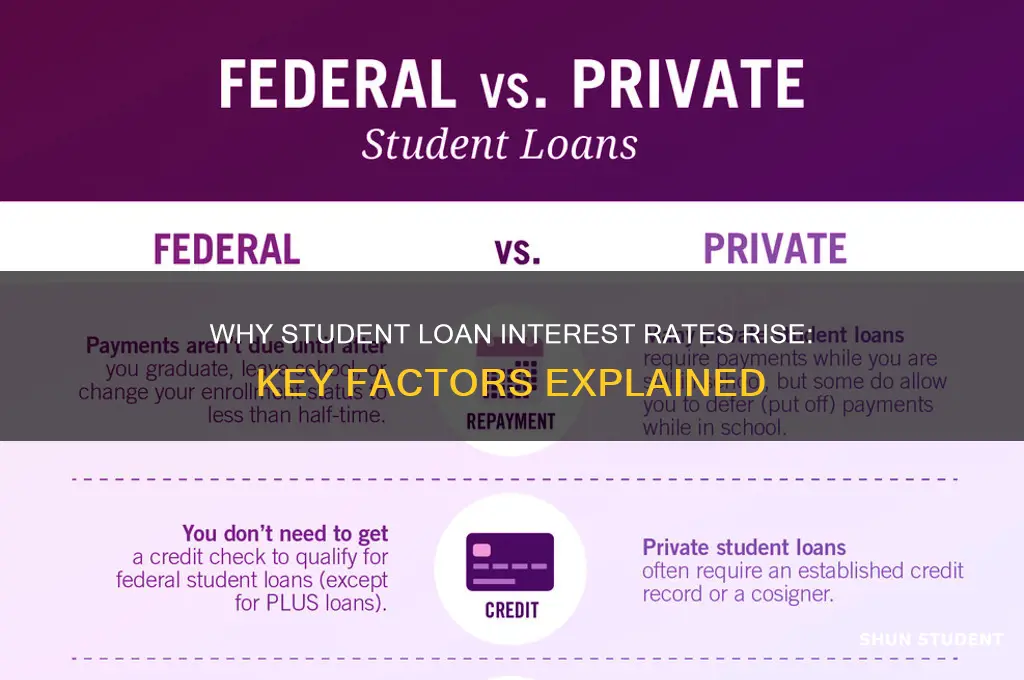

- Federal vs. Private Loans: Federal rates set by Congress; private rates vary by lender and credit

- Economic Conditions: Rising inflation and market interest rates often increase student loan interest

- Repayment Plan Choice: Income-driven plans may extend terms, increasing total interest paid over time

- Credit Score Impact: Poor credit can lead to higher interest rates on private loans

- Variable Rate Risks: Variable-rate loans fluctuate with market changes, potentially raising interest costs

![]()

Federal vs. Private Loans: Federal rates set by Congress; private rates vary by lender and credit

When considering what makes student loan interest rates increase, it's essential to understand the fundamental differences between federal and private loans. Federal student loans have interest rates that are set by Congress, not by market conditions or individual financial circumstances. These rates are typically fixed for the life of the loan and are determined through legislation, often tied to the 10-year Treasury note. For instance, each year, Congress may adjust federal student loan rates based on economic factors, but these changes apply uniformly to all borrowers within the same loan category (e.g., Direct Subsidized Loans or Direct Unsubsidized Loans). This means federal loan rates are generally more predictable and less influenced by personal financial situations.

In contrast, private student loans have interest rates that vary widely based on the lender and the borrower's creditworthiness. Private lenders, such as banks or credit unions, determine rates based on market conditions, the borrower's credit score, income, and debt-to-income ratio. Unlike federal loans, private loan rates can be fixed or variable, meaning they may fluctuate over time in response to economic changes. Borrowers with excellent credit may secure lower rates, while those with poor credit or limited credit history often face higher rates, sometimes significantly above federal loan rates. This variability makes private loans riskier and less predictable in terms of long-term costs.

One key factor that can cause student loan interest rates to rise is legislative changes for federal loans. For example, if Congress passes a bill increasing federal student loan rates, all new loans disbursed after the effective date will carry the higher rate. This is particularly important for students and families planning for future education expenses, as it directly impacts the total cost of borrowing. On the other hand, private loan rates are more susceptible to economic shifts, such as increases in the prime rate or LIBOR index, which can cause monthly payments to rise for borrowers with variable-rate loans.

Another aspect to consider is the role of credit in private loan interest rates. Lenders assess a borrower's credit profile to determine the likelihood of repayment. A low credit score or insufficient credit history can lead to higher interest rates or the need for a cosigner. Over time, if economic conditions worsen or default rates rise, private lenders may increase rates across the board to mitigate risk. This stands in stark contrast to federal loans, where eligibility is not based on credit, and rates are standardized, making them a more stable option for borrowers with limited or poor credit.

Lastly, it's crucial to recognize that while federal loan rates are set by Congress and offer consistent terms, private loans provide no such guarantees. Borrowers with private loans may experience rate increases due to changes in their personal financial situation or broader economic trends. For this reason, financial experts often advise exhausting federal loan options before considering private loans. Understanding these differences empowers borrowers to make informed decisions and minimize the impact of rising interest rates on their student loan debt.

Understanding US Banks' Interest Rates for Student Loans: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Economic Conditions: Rising inflation and market interest rates often increase student loan interest

Economic conditions play a significant role in determining student loan interest rates, and one of the primary factors is inflation. When inflation rises, it erodes the purchasing power of money, meaning that lenders demand higher interest rates to compensate for the decreased value of future repayments. In the context of student loans, this translates to increased borrowing costs for students. Central banks often respond to inflation by raising benchmark interest rates, which has a ripple effect across the entire lending market, including student loans. As a result, both federal and private student loan interest rates tend to climb in an inflationary environment, making it more expensive for students to finance their education.

Market interest rates, which are heavily influenced by economic conditions, also directly impact student loan rates. These rates are determined by the supply and demand for credit in the broader economy. During periods of economic growth or uncertainty, investors may demand higher returns on their investments, pushing market interest rates upward. Since student loans are a form of credit, they are not immune to these market forces. For instance, federal student loan interest rates in the United States are tied to the 10-year Treasury note, which reflects broader market conditions. When the yield on this Treasury note increases, so do student loan interest rates, reflecting the higher cost of borrowing in the economy.

The relationship between economic conditions and student loan interest rates is further complicated by monetary policy decisions. Central banks, like the Federal Reserve in the U.S., adjust interest rates to control inflation and stabilize the economy. When the central bank raises rates to combat inflation or cool down an overheating economy, lenders typically follow suit by increasing the rates they charge on loans, including student loans. This means that students borrowing during periods of tight monetary policy will likely face higher interest rates than those borrowing during more accommodative periods. Understanding these dynamics is crucial for students and families planning to take on educational debt.

Moreover, rising inflation and market interest rates can disproportionately affect borrowers with variable-rate student loans. Unlike fixed-rate loans, which lock in an interest rate for the life of the loan, variable-rate loans fluctuate with market conditions. During periods of increasing interest rates, borrowers with variable-rate loans may see their monthly payments rise significantly, adding financial strain. This volatility underscores the importance of carefully considering loan terms and economic trends when choosing a student loan. For those already repaying loans, rising interest rates may necessitate adjustments to budgets or repayment strategies to manage the increased costs.

In summary, economic conditions, particularly rising inflation and market interest rates, are key drivers of increasing student loan interest rates. These factors are influenced by broader monetary policies and market dynamics, which ultimately determine the cost of borrowing for students. As inflation erodes the value of money and central banks raise benchmark rates, lenders adjust student loan rates accordingly. Borrowers, especially those with variable-rate loans, must remain vigilant about economic trends to anticipate and plan for potential increases in their loan costs. By understanding these economic forces, students can make more informed decisions about financing their education and managing their debt.

Understanding New Zealand's Student Loan Interest Rates: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Repayment Plan Choice: Income-driven plans may extend terms, increasing total interest paid over time

When considering what makes student loan interest go up, one significant factor is the repayment plan choice, particularly the selection of income-driven repayment (IDR) plans. These plans are designed to make monthly payments more manageable by capping them at a percentage of the borrower’s discretionary income. While this can provide immediate financial relief, it often comes with a trade-off: extended repayment terms. For example, standard repayment plans typically span 10 years, but income-driven plans can stretch repayment periods to 20 or even 25 years. This extension means the loan remains outstanding for a longer period, allowing more time for interest to accrue. As a result, borrowers may end up paying significantly more in total interest over the life of the loan compared to shorter repayment plans.

The mechanics of income-driven plans contribute directly to the increase in total interest paid. Since monthly payments are based on income and family size, they are often lower than those of standard plans, especially for borrowers with lower incomes. While lower payments reduce monthly financial strain, they also mean that the principal balance is paid down more slowly. Interest continues to accrue on the remaining balance, compounding over time. For instance, if a borrower’s monthly payment barely covers the accruing interest, the principal balance may decrease minimally or not at all, leading to a phenomenon known as "negative amortization." This can cause the total interest paid to balloon over the extended repayment period.

Another aspect to consider is the treatment of remaining balances after the repayment term ends. Some income-driven plans offer loan forgiveness for any outstanding balance after 20 or 25 years of qualifying payments. While this can be a financial lifeline, the forgiven amount may be treated as taxable income, creating an additional financial burden. Moreover, not all borrowers will qualify for forgiveness, and those who do not may face even higher interest costs due to the prolonged repayment period. This highlights the importance of carefully weighing the long-term financial implications of choosing an income-driven plan.

Borrowers must also be aware of how changes in income can affect their payments and interest accrual under income-driven plans. If a borrower’s income increases significantly, their monthly payments will rise accordingly, but the extended term remains in place. This means that even with higher payments, the total interest paid may still be substantial due to the initial years of lower payments and slower principal reduction. Additionally, if a borrower’s income fluctuates, recalculating payments annually can lead to uncertainty and potentially higher interest costs if payments do not keep pace with accruing interest.

In summary, while income-driven repayment plans offer valuable flexibility and affordability for borrowers with limited incomes, they can lead to higher total interest paid over time due to extended repayment terms and slower principal reduction. Borrowers should carefully evaluate their financial situation, future income prospects, and long-term goals before choosing an income-driven plan. Alternatives, such as standard or graduated repayment plans, may result in higher monthly payments but can minimize the total interest paid by shortening the loan term. Understanding these trade-offs is crucial for making an informed decision and managing student loan debt effectively.

Reddit's Guide to Understanding Your Student Loan Interest Rate

You may want to see also

Explore related products

![]()

Credit Score Impact: Poor credit can lead to higher interest rates on private loans

When it comes to private student loans, a borrower's credit score plays a pivotal role in determining the interest rate they will be offered. Lenders view a credit score as a snapshot of an individual's financial responsibility and creditworthiness. A poor credit score can significantly impact the cost of borrowing for education, often resulting in higher interest rates. This is because a low credit score indicates a higher risk to the lender; it suggests that the borrower may have a history of late payments, high debt levels, or other financial mismanagement. As a result, lenders may charge a higher interest rate to compensate for this perceived risk, ensuring they are adequately compensated for the potential likelihood of default.

The relationship between credit scores and interest rates is inversely proportional; as credit scores decrease, interest rates tend to increase. Private lenders often have a range of interest rates they offer, and borrowers with excellent credit can secure loans at the lower end of this spectrum. Conversely, those with poor credit may find themselves at the higher end, paying significantly more in interest over the life of the loan. For instance, a borrower with a credit score below 600 might be offered an interest rate several percentage points higher than someone with a score above 750, which can translate to thousands of dollars in additional repayment costs.

Improving one's credit score before applying for a private student loan can be a strategic move to secure a more favorable interest rate. This can be achieved by paying bills on time, reducing credit card balances, and correcting any errors on credit reports. For students with limited credit history, becoming an authorized user on a parent's credit card or taking out a small loan and managing it responsibly can help build a positive credit profile. These steps can demonstrate to lenders that the borrower is a lower risk, potentially leading to better loan terms.

It's important for students to understand that federal student loans, which are need-based, do not rely on credit scores for interest rate determination. However, private loans, which are often sought to cover gaps in funding, are credit-based. This distinction is crucial as it highlights the importance of credit management for students considering private lending options. By being aware of how credit scores influence interest rates, students can make more informed decisions about their borrowing strategies and take proactive steps to improve their financial standing.

In summary, a poor credit score can be a significant factor in the rising cost of student loan interest, particularly in the private loan market. Lenders use credit scores to assess risk, and a low score often results in higher interest rates. Borrowers should be mindful of this relationship and take steps to enhance their creditworthiness before applying for loans. By doing so, they can potentially save a substantial amount of money and manage their student debt more effectively. Understanding this aspect of student loan financing is essential for making informed financial choices during the educational journey.

Understanding the Current Student Plus Loan Interest Rate

You may want to see also

Explore related products

$16.53 $22.99

![]()

Variable Rate Risks: Variable-rate loans fluctuate with market changes, potentially raising interest costs

Variable-rate student loans are inherently tied to market conditions, which means their interest rates can rise or fall based on economic factors. Unlike fixed-rate loans, which maintain the same interest rate throughout the life of the loan, variable-rate loans are directly influenced by benchmarks such as the London Interbank Offered Rate (LIBOR) or the Prime Rate. When these benchmarks increase due to shifts in the economy, such as rising inflation or central bank policy changes, the interest rate on a variable-rate student loan will also increase. This fluctuation can lead to higher monthly payments and overall borrowing costs, making it difficult for borrowers to predict and manage their loan expenses.

One of the primary risks of variable-rate loans is the lack of predictability in interest rate movements. Economic conditions can change rapidly, and factors like inflation, unemployment rates, and monetary policy decisions can cause market interest rates to rise unexpectedly. For example, during periods of economic recovery or expansion, central banks may raise interest rates to control inflation, which in turn increases the cost of borrowing. Borrowers with variable-rate loans may find themselves facing higher interest charges at a time when their financial situation has not improved, creating a strain on their budget.

Another significant risk is the potential for interest rates to climb significantly over the life of the loan. While variable-rate loans often start with lower interest rates compared to fixed-rate loans, they can become more expensive if market rates rise sharply. For instance, a borrower who takes out a variable-rate loan during a period of low interest rates may initially benefit from lower payments. However, if interest rates increase over time, the total interest paid over the life of the loan could surpass that of a fixed-rate loan. This makes variable-rate loans riskier for long-term borrowing, especially for students who may not have a stable income immediately after graduation.

Borrowers with variable-rate loans must also consider the impact of compounding interest rate increases. As market rates rise, not only does the current interest rate on the loan increase, but the higher rate is applied to the remaining balance, leading to greater interest accrual over time. This compounding effect can cause the loan balance to grow faster than anticipated, especially if the borrower is making minimum payments or is in a deferment or forbearance period. Over time, this can result in a much larger debt burden than originally planned.

To mitigate the risks of variable-rate loans, borrowers should carefully assess their financial situation and future prospects before choosing this type of loan. It’s essential to have a contingency plan in place, such as setting aside savings or exploring options to refinance to a fixed-rate loan if interest rates begin to rise. Additionally, staying informed about economic trends and understanding the terms of the loan agreement can help borrowers anticipate changes and make informed decisions. While variable-rate loans can offer initial savings, their susceptibility to market fluctuations makes them a riskier choice for those seeking stability in their student loan repayments.

Maximize Your Savings: Understanding the Student Loan Interest Tax Break

You may want to see also

Frequently asked questions

Student loan interest rates can rise due to changes in federal or private lending policies, fluctuations in the economy, or shifts in benchmark interest rates like the LIBOR or Prime Rate.

For private student loans, yes—a lower credit score can lead to higher interest rates. Federal student loans, however, are not based on credit scores and have fixed rates set by Congress.

Yes, economic conditions such as inflation or rising federal interest rates can lead to higher student loan interest rates, especially for variable-rate private loans.

While missing payments or defaulting doesn’t directly raise the interest rate, it can lead to additional fees, penalties, and capitalization of interest, effectively increasing the total cost of the loan.