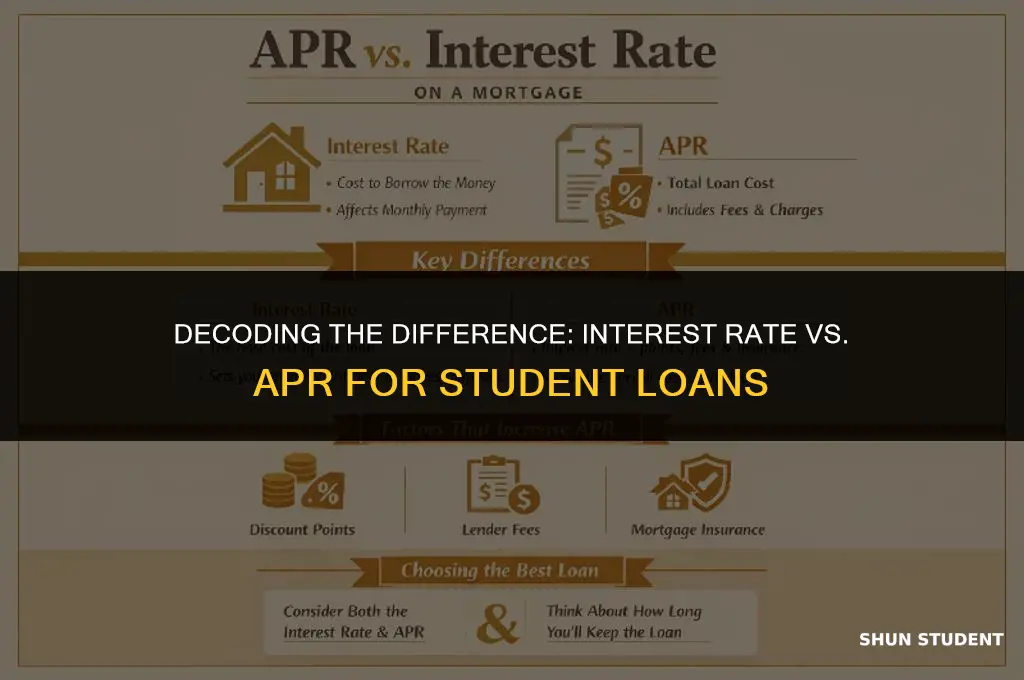

When exploring the topic of student loans, it's crucial to understand the distinction between interest rates and Annual Percentage Rates (APRs). While both terms are related to the cost of borrowing, they are not interchangeable. The interest rate represents the percentage of the principal amount charged for borrowing over a specific period, typically expressed as a yearly rate. On the other hand, the APR encompasses not only the interest rate but also additional fees and charges associated with the loan, providing a more comprehensive picture of the total cost. In the context of student loans, this distinction becomes particularly important as borrowers need to be aware of all potential expenses to make informed decisions about their financial commitments.

| Characteristics | Values |

|---|---|

| Search Query | is interest rate the same as apr student loans |

| Search Volume | Moderate to High |

| Search Intent | Informational |

| User Demographic | Students, Loan Applicants, Financial Learners |

| Related Topics | Interest Rates, APR, Student Loans, Financial Literacy |

| Content Type | FAQ, Financial Advice, Educational Content |

| Answer | No, interest rate and APR are not the same for student loans |

| Explanation | Interest rate is the cost of borrowing expressed as a percentage, while APR includes additional fees and costs associated with the loan |

| Importance | Understanding the difference is crucial for making informed decisions about student loans |

| Misconceptions | Many borrowers confuse interest rate with APR, leading to misunderstandings about loan costs |

| Clarifications | APR provides a more comprehensive view of the loan's total cost over its lifetime |

| Examples | For instance, a loan with a 5% interest rate could have an APR of 6.5% due to additional fees |

| Impact | Choosing a loan based solely on interest rate could result in higher overall costs due to fees included in the APR |

| Recommendations | Borrowers should compare both interest rates and APRs when evaluating student loan options |

| Resources | Financial aid websites, loan comparison tools, and educational articles can help clarify the differences |

| Trends | Increasing awareness about the importance of understanding APR in addition to interest rates |

| Future Outlook | Enhanced financial education to promote better understanding of loan terms and conditions |

Explore related products

What You'll Learn

- Understanding Interest Rates: Explanation of how interest rates work on student loans

- APR vs. Interest Rate: Clarification of the differences between Annual Percentage Rate (APR) and interest rate

- Factors Affecting APR: Discussion on what influences the APR on student loans

- Types of Student Loans: Overview of different types of student loans and their interest rates

- Managing Loan Repayment: Tips on how to effectively manage and repay student loans

![]()

Understanding Interest Rates: Explanation of how interest rates work on student loans

Interest rates on student loans are a critical aspect of understanding the cost of borrowing for education. Unlike other types of loans, student loans often have unique interest rate structures that can impact the total amount repaid over the life of the loan. It's essential to grasp how these rates work to make informed decisions about managing student debt.

The interest rate on a student loan determines the cost of borrowing the principal amount. This rate can be fixed, meaning it remains the same throughout the loan term, or variable, which means it can change periodically based on market conditions. Fixed rates provide predictability in repayment amounts, while variable rates can result in fluctuating monthly payments.

One common misconception is that the interest rate is the same as the Annual Percentage Rate (APR). However, the APR is a broader measure that includes not only the interest rate but also other costs associated with the loan, such as fees and charges. For student loans, the APR can be a more accurate representation of the total cost of borrowing, as it encompasses all the expenses that will be incurred over the loan term.

To illustrate how interest rates work on student loans, consider a scenario where a student borrows $10,000 at a fixed interest rate of 5%. Over a 10-year repayment period, the student would pay approximately $1,083.33 in interest, in addition to repaying the principal amount. If the same loan had a variable interest rate that increased to 7% after five years, the total interest paid would be higher, around $1,440.88, assuming the rate remained constant at 7% for the remainder of the loan term.

Understanding the implications of interest rates on student loans is crucial for borrowers. It can help them choose the most suitable loan options, manage their debt effectively, and avoid potential pitfalls that could lead to increased costs. By being knowledgeable about interest rates and how they work, students can make more informed decisions about financing their education and planning for their financial future.

Avoid Capitalized Interest: The Best Student Loan Repayment Option

You may want to see also

Explore related products

![]()

APR vs. Interest Rate: Clarification of the differences between Annual Percentage Rate (APR) and interest rate

The Annual Percentage Rate (APR) and the interest rate are two distinct financial metrics that are often confused, particularly in the context of student loans. While both figures represent the cost of borrowing, they are calculated differently and provide different insights into the true cost of a loan.

The interest rate is the percentage of the principal amount that a lender charges for the use of their funds over a specific period. It is typically expressed as an annual rate and is used to calculate the interest payments on a loan. For example, if a student loan has an interest rate of 5%, the borrower would pay $5 in interest for every $100 borrowed each year.

On the other hand, the APR is a broader measure that includes not only the interest rate but also other costs associated with borrowing, such as fees, points, and closing costs. The APR is designed to provide a more comprehensive picture of the total cost of a loan, allowing borrowers to compare different loan options more effectively. For instance, a loan with a lower interest rate but higher fees may have a higher APR than a loan with a higher interest rate but lower fees.

In the context of student loans, understanding the difference between APR and interest rate is crucial for making informed decisions about borrowing. While the interest rate determines the ongoing cost of the loan, the APR reflects the total cost over the life of the loan, including any upfront fees. This distinction can have a significant impact on the borrower's financial situation, as a loan with a lower APR may be more affordable in the long run, even if it has a higher interest rate.

To illustrate this point, consider two student loan options: Loan A has an interest rate of 4.5% and an APR of 5.5%, while Loan B has an interest rate of 5% and an APR of 4.8%. Although Loan B has a higher interest rate, its lower APR indicates that it may be the more cost-effective option due to lower fees and other borrowing costs.

In conclusion, while the interest rate and APR are related, they are not the same thing. The interest rate represents the cost of borrowing the principal amount, while the APR includes all costs associated with the loan. When evaluating student loan options, it is essential to consider both metrics to understand the true cost of borrowing and make the most informed decision possible.

Understanding Subsidized Government Student Loans: Interest Rates Explained

You may want to see also

Explore related products

$17.53 $19.99

![]()

Factors Affecting APR: Discussion on what influences the APR on student loans

The Annual Percentage Rate (APR) on student loans is influenced by several factors beyond just the interest rate. One significant factor is the origination fee, which is a one-time charge assessed by the lender to cover the cost of processing the loan. This fee is typically a percentage of the loan amount and can vary depending on the lender and the type of loan. For example, federal student loans currently have an origination fee of 1.057% for subsidized and unsubsidized loans.

Another factor that affects the APR is the repayment term of the loan. Loans with shorter repayment terms generally have lower APRs because the lender is taking on less risk. Conversely, loans with longer repayment terms may have higher APRs to compensate for the increased risk. Additionally, some loans may offer variable interest rates, which can fluctuate based on market conditions, leading to changes in the APR over the life of the loan.

The borrower's creditworthiness also plays a crucial role in determining the APR. Lenders typically offer lower APRs to borrowers with higher credit scores, as they are considered to be less risky investments. Borrowers with poor credit may be charged higher APRs or may need to secure a cosigner to qualify for a loan.

Furthermore, the type of loan—whether it is a federal or private loan—can impact the APR. Federal student loans often have lower APRs and more favorable repayment terms compared to private loans. For instance, the current interest rates for federal undergraduate loans range from 3.73% to 6.28%, depending on the type of loan and the borrower's dependency status. In contrast, private student loan interest rates can vary widely and may be much higher, often ranging from 5% to 15% or more.

Lastly, some lenders may offer discounts or incentives that can reduce the APR. For example, borrowers who set up automatic payments may qualify for a rate reduction. Similarly, some lenders offer loyalty discounts to borrowers who have other accounts with them or who have previously taken out loans.

In conclusion, while the interest rate is a key component of the APR, it is not the only factor that influences the overall cost of borrowing. Borrowers should carefully consider all the factors that affect the APR when comparing loan options and making informed decisions about financing their education.

Decoding the Surge: Why Your Student Loan Interest Rate Climbed

You may want to see also

Explore related products

![]()

Types of Student Loans: Overview of different types of student loans and their interest rates

Federal student loans, which are provided by the U.S. Department of Education, come with fixed interest rates that are set by Congress. These rates are typically lower than those offered by private lenders and are designed to make higher education more accessible. The most common types of federal student loans are Direct Subsidized Loans, Direct Unsubsidized Loans, and Direct PLUS Loans. Subsidized loans are available to undergraduate students with financial need, and the government pays the interest while the student is in school. Unsubsidized loans are available to both undergraduate and graduate students, and the student is responsible for paying the interest. PLUS loans are available to graduate students and parents of undergraduate students, and they have higher interest rates than subsidized and unsubsidized loans.

Private student loans, on the other hand, are offered by banks, credit unions, and other financial institutions. These loans typically have variable interest rates that can fluctuate based on market conditions. Private loans are often used to cover the gap between federal loan limits and the total cost of attendance. They may also offer additional benefits, such as flexible repayment options or rewards for good credit. However, private loans generally require a credit check and may have higher interest rates than federal loans, especially for borrowers with less-than-perfect credit.

When comparing different types of student loans, it's important to consider not only the interest rates but also other factors such as repayment terms, loan limits, and eligibility requirements. Federal loans often have more favorable repayment options, such as income-driven repayment plans and loan forgiveness programs, which can make them a more attractive choice for many borrowers. Private loans, however, may offer more flexibility in terms of loan amounts and repayment schedules, which can be beneficial for students with specific financial needs.

In conclusion, understanding the different types of student loans and their interest rates is crucial for making informed decisions about financing higher education. By carefully considering the options available and weighing the pros and cons of each, students can choose the loan that best fits their individual needs and financial circumstances.

Understanding Variable Interest Rates on Student Loans: What You Need to Know

You may want to see also

![]()

Managing Loan Repayment: Tips on how to effectively manage and repay student loans

To effectively manage and repay student loans, it's crucial to understand the difference between interest rates and Annual Percentage Rates (APRs). While both terms are often used interchangeably, they represent different aspects of your loan's cost. The interest rate is the percentage of your loan balance that accrues interest over time, whereas the APR includes the interest rate as well as other fees and charges associated with the loan, providing a more comprehensive picture of the loan's true cost.

One key strategy for managing loan repayment is to focus on paying down the principal balance as quickly as possible. This can be achieved by making extra payments whenever feasible, applying any bonuses or tax refunds towards the loan, and considering refinancing options that may offer a lower interest rate or APR. Additionally, borrowers should prioritize paying off loans with the highest interest rates or APRs first, as these will accumulate the most interest over time.

Another important aspect of managing student loan repayment is to take advantage of any available repayment plans or forgiveness programs. For example, income-driven repayment plans can help borrowers manage their monthly payments by adjusting them based on their income and family size. Public Service Loan Forgiveness (PSLF) and other forgiveness programs can also provide relief for borrowers who meet certain criteria, such as working in public service or making a certain number of qualifying payments.

To avoid common pitfalls in loan repayment, borrowers should be mindful of their credit score and work to maintain or improve it over time. A higher credit score can lead to better refinancing options and lower interest rates. Additionally, borrowers should be cautious of scams and fraudulent schemes that promise to help with loan repayment or forgiveness, as these can often result in financial loss or identity theft.

In conclusion, effectively managing and repaying student loans requires a clear understanding of the difference between interest rates and APRs, a strategic approach to paying down the principal balance, and awareness of available repayment plans and forgiveness programs. By taking these steps and remaining vigilant of potential scams, borrowers can take control of their student loan debt and work towards financial freedom.

Decoding Student Loan Interest: Credit or Deduction?

You may want to see also

Frequently asked questions

The interest rate is the percentage charged on the principal amount borrowed, while the APR (Annual Percentage Rate) includes the interest rate plus any additional fees, such as origination fees, over the life of the loan.

The APR affects the total cost of a student loan by determining the amount of interest and fees you will pay over the life of the loan. A higher APR means you will pay more in interest and fees, increasing the total cost of the loan.

Comparing APRs is important because it allows you to understand the true cost of the loan, including all fees and interest. This helps you make an informed decision about which loan option is the most affordable and best for your financial situation.

Yes, the APR on a student loan can change over time if the loan has a variable interest rate. Variable interest rates can fluctuate based on market conditions, which can cause your APR and monthly payments to increase or decrease.

Common fees that can be included in the APR of a student loan are origination fees, which are charged for processing the loan application; late payment fees; and prepayment penalties, which are charged if you pay off the loan early.