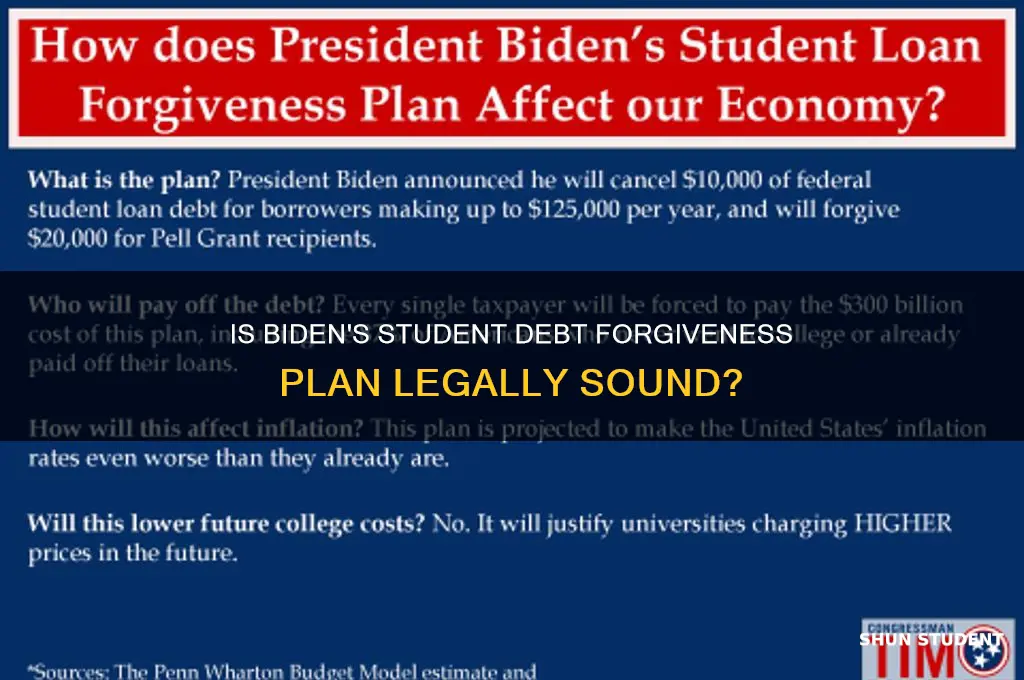

The question of whether it is legal for President Biden to forgive student debt has sparked intense debate and legal scrutiny. Advocates argue that the Higher Education Act of 1965 grants the Secretary of Education broad authority to modify or waive federal student loans, providing a legal basis for such action. However, critics contend that large-scale debt forgiveness could overstep executive authority, violate the separation of powers, and require congressional approval. The issue has been further complicated by legal challenges, with several lawsuits questioning the constitutionality and statutory grounds of such a move. As the Biden administration navigates these complexities, the outcome will likely have significant implications for millions of borrowers and the broader debate over the role of government in addressing student debt.

| Characteristics | Values |

|---|---|

| Legal Authority | Biden's administration claims authority under the Higher Education Act (HEA) of 1965, specifically Section 432(a), which allows the Secretary of Education to modify or waive federal student loans in certain circumstances. |

| Legal Challenges | Multiple lawsuits have been filed challenging the legality of Biden's student debt forgiveness plan, arguing it exceeds executive authority and violates the Administrative Procedure Act (APA). |

| Supreme Court Ruling (June 2023) | The Supreme Court ruled in Biden v. Nebraska (6-3) that the HEROES Act does not grant the executive branch the authority to forgive student debt on a mass scale without explicit congressional approval. |

| Current Status | As of October 2023, Biden's broad student debt forgiveness plan remains blocked due to the Supreme Court ruling. However, targeted relief programs (e.g., Public Service Loan Forgiveness, income-driven repayment adjustments) continue. |

| Congressional Action | No legislation has been passed by Congress to authorize mass student debt forgiveness, leaving the issue largely in the hands of the executive branch and courts. |

| Public Opinion | Opinions are divided, with supporters arguing it addresses economic inequality and opponents claiming it is unfair to taxpayers and legally questionable. |

| Alternative Measures | The Biden administration has focused on expanding existing loan forgiveness programs, fixing administrative issues, and providing temporary relief (e.g., payment pauses) instead of broad forgiveness. |

| Political Implications | The issue remains a key political talking point, with Democrats advocating for relief and Republicans opposing it as overreach of executive power. |

Explore related products

$14.99 $11.69

What You'll Learn

- Constitutional Authority: Does Biden have the power to forgive debt without Congress

- Legal Challenges: Potential lawsuits and their basis against debt forgiveness

- HEROES Act: Use of the HEROES Act to justify executive action

- Economic Impact: Legal implications of debt forgiveness on the economy

- Precedent: Historical examples of executive actions on debt relief

![]()

Constitutional Authority: Does Biden have the power to forgive debt without Congress?

The debate over President Biden's authority to forgive student debt without congressional approval hinges on the interpretation of the Higher Education Act of 1965, specifically Section 432(a). This provision grants the Secretary of Education the power to "enforce, pay, compromise, waive, or release any right, title, and claim of the United States" related to federal student loans. Proponents argue this language provides a clear legal basis for executive action, while critics contend it was never intended to authorize mass debt cancellation.

Example: In August 2022, the Biden administration announced a plan to forgive up to $20,000 in student debt for eligible borrowers, citing this section as its legal foundation.

Analyzing the constitutional framework, the separation of powers doctrine raises questions about whether debt forgiveness constitutes legislative action disguised as executive authority. Article I of the Constitution vests Congress with the power to "lay and collect taxes" and "borrow money on the credit of the United States," both of which are implicated in large-scale debt cancellation. If forgiving debt is seen as equivalent to spending taxpayer funds, it could infringe on Congress's exclusive budgetary authority.

From a persuasive standpoint, supporters of executive action emphasize the urgency of the student debt crisis, arguing that congressional gridlock justifies bold presidential intervention. They point to historical precedents, such as the use of executive powers during the COVID-19 pandemic to pause student loan payments, as evidence of the administration's flexibility in addressing national emergencies. However, this argument risks normalizing unilateral action, potentially undermining the checks and balances inherent in the Constitution.

A comparative analysis with past executive actions reveals a mixed record. For instance, President Trump's use of executive orders to bypass Congress on immigration and trade faced legal challenges but was upheld in some instances. Yet, debt forgiveness differs in scale and financial impact, making it a more contentious exercise of power. Courts may scrutinize whether the administration has exceeded its statutory authority or violated the non-delegation doctrine, which limits Congress's ability to grant unchecked powers to the executive branch.

In practical terms, borrowers awaiting resolution should monitor legal developments, as ongoing lawsuits could delay or invalidate the forgiveness plan. *Tip:* Keep documentation of loan balances and eligibility status, and stay informed through official channels like the Department of Education’s website. Ultimately, the constitutionality of Biden's action will likely be decided by the Supreme Court, setting a precedent for the scope of executive authority in fiscal matters.

Complete Guide to Applying for PSLF Student Loan Forgiveness

You may want to see also

Explore related products

![]()

Legal Challenges: Potential lawsuits and their basis against debt forgiveness

The legality of President Biden's student debt forgiveness plan hinges on whether the executive branch has the authority to unilaterally cancel such debts. Critics argue that this action oversteps constitutional boundaries, potentially inviting legal challenges. These challenges could arise from various parties, including taxpayers, debt holders, and states, each with distinct legal bases for their claims. Understanding these potential lawsuits is crucial for assessing the plan's viability and its broader implications.

One potential legal challenge could come from taxpayers who argue that debt forgiveness constitutes an unlawful use of public funds. Plaintiffs might claim that the executive branch lacks the statutory authority to allocate taxpayer money for debt cancellation without explicit congressional approval. This argument would likely center on the Administrative Procedure Act (APA), which requires federal agencies to follow specific procedures when creating or modifying regulations. If the Department of Education’s actions are deemed arbitrary or capricious, courts could invalidate the forgiveness plan. For instance, a lawsuit might highlight the lack of public notice and comment periods, a procedural requirement under the APA, as a basis for challenging the policy’s legitimacy.

Another avenue for litigation could involve states suing the federal government on grounds of sovereign injury. States might argue that debt forgiveness harms their economies by reducing tax revenue or disrupting financial markets. For example, states with significant investments in student loan servicing companies could claim financial injury if those companies suffer losses due to widespread debt cancellation. Such lawsuits would likely rely on the doctrine of standing, requiring states to demonstrate concrete and particularized harm. While this basis is more complex, it underscores the potential for multijurisdictional conflicts in implementing the policy.

Debt holders themselves could also file lawsuits, though their legal standing is less clear. Some borrowers might argue that the forgiveness plan creates unequal treatment, violating the Fifth Amendment’s equal protection principles. For instance, individuals who paid off their loans before the policy’s announcement could claim unfair disadvantage. However, courts generally defer to the government’s discretion in financial matters, making such challenges less likely to succeed. Nonetheless, these lawsuits could delay implementation and create uncertainty for millions of borrowers.

In navigating these legal challenges, the Biden administration’s defense will likely rest on the Higher Education Relief Opportunities for Students (HEROES) Act of 2003. This law grants the Secretary of Education broad authority to modify student loan programs during national emergencies, such as the COVID-19 pandemic. However, opponents argue that debt cancellation exceeds the scope of this authority, as it goes beyond providing temporary relief. The outcome of these legal battles will depend on judicial interpretation of the HEROES Act and the limits of executive power, setting a precedent for future policy actions.

Biden's Student Loan Forgiveness: $10K Relief Plan Explained

You may want to see also

Explore related products

![]()

HEROES Act: Use of the HEROES Act to justify executive action

The Higher Education Relief Opportunities for Students (HEROES) Act of 2003 grants the Secretary of Education broad authority to waive or modify regulations related to student financial assistance programs during national emergencies. President Biden’s administration has leveraged this act to justify executive action on student debt forgiveness, particularly in response to the COVID-19 pandemic. By invoking the HEROES Act, the Department of Education argues it can provide targeted relief to borrowers facing economic hardship, such as pausing loan payments or reducing interest rates. However, the act’s scope and limits have sparked legal debates, with critics questioning whether it authorizes blanket debt cancellation.

To understand the HEROES Act’s application, consider its original intent: to assist service members and their families during wartime. The act was later expanded to include national emergencies declared by the President. During the pandemic, the Department of Education used this authority to pause federal student loan payments and halt interest accrual, benefiting millions of borrowers. The Biden administration extended this pause multiple times, citing ongoing economic challenges. The next logical step, proponents argue, is to use the act’s waiver authority to forgive debt for specific groups, such as low-income borrowers or those with disabilities, rather than implementing universal cancellation.

Critics, however, argue that the HEROES Act does not grant the executive branch the power to cancel debt outright. They contend that such action requires congressional approval, as it involves significant fiscal implications and policy changes. Legal challenges to Biden’s student debt relief plan, including the $10,000 to $20,000 cancellation proposal, have hinged on this interpretation. Courts have scrutinized whether the act’s language permits such sweeping measures or if it is limited to administrative adjustments like payment pauses. The Supreme Court’s eventual ruling on this issue will set a precedent for the boundaries of executive authority under the HEROES Act.

Practical considerations for borrowers include staying informed about ongoing litigation and policy updates. If the HEROES Act is upheld as a legal basis for debt forgiveness, targeted relief programs could emerge, focusing on borrowers with the greatest need. For example, public service loan forgiveness or income-driven repayment plans might be expanded. Borrowers should also prepare for potential repayment resumption by reviewing their loan terms and exploring repayment options. Advocacy groups and legal experts recommend documenting financial hardship to support eligibility for future relief programs.

In conclusion, the HEROES Act serves as a critical tool for the Biden administration’s student debt relief efforts, but its legal limits remain contested. While it has successfully justified administrative actions like payment pauses, its application to debt cancellation is uncertain. Borrowers must navigate this evolving landscape by staying informed and proactive, while policymakers and courts determine the act’s ultimate reach. The outcome will shape not only individual financial futures but also the balance of power between the executive and legislative branches in education policy.

Unlock Student Loan Relief: Guide to Securing Interest Forgiveness

You may want to see also

Explore related products

![]()

Economic Impact: Legal implications of debt forgiveness on the economy

The legal implications of student debt forgiveness under President Biden’s executive actions extend beyond constitutional debates to significant economic consequences. Forgiving trillions in student loans could inject liquidity into the economy as borrowers redirect funds from debt payments to consumption or savings. However, this stimulus effect is tempered by concerns about inflationary pressures, particularly in sectors like housing and education, where increased demand could drive up prices. The legal framework must balance these economic trade-offs, ensuring that short-term gains do not lead to long-term instability.

Consider the distributional impact: debt forgiveness disproportionately benefits higher-income earners with advanced degrees, who hold a larger share of student debt. While this could stimulate spending in high-value sectors, it may exacerbate wealth inequality. Legal challenges often highlight this inequity, arguing that broad forgiveness violates principles of fairness by shifting the burden to taxpayers who did not attend college. Policymakers must weigh these ethical and economic considerations, potentially tailoring relief to target lower-income borrowers for maximum societal benefit.

Another critical aspect is the potential crowding-out effect on government spending. If debt forgiveness is funded through deficit spending, it could compete with other fiscal priorities, such as infrastructure or healthcare. Legal debates often center on the authority to reallocate funds without congressional approval, as seen in challenges to Biden’s use of the HEROES Act. Economically, this raises questions about sustainability: will increased debt levels hinder future growth, or can the stimulus offset these costs? The legal framework must address these fiscal risks to avoid unintended economic consequences.

Finally, the psychological and behavioral effects of debt forgiveness cannot be overlooked. Removing financial burdens could boost entrepreneurship and risk-taking, as individuals feel freer to pursue new ventures without the weight of debt. However, this assumes borrowers use freed-up funds productively rather than increasing consumption or savings. Legal decisions must consider these behavioral dynamics, as they influence the overall economic impact. For instance, targeted forgiveness programs with conditions, such as public service requirements, could maximize positive outcomes while minimizing moral hazard.

In navigating these complexities, the legal implications of student debt forgiveness must prioritize economic stability and equity. While the immediate stimulus potential is clear, long-term effects on inflation, inequality, and fiscal health require careful consideration. Legal frameworks should incorporate economic analysis to ensure that debt relief serves as a tool for sustainable growth rather than a source of future crises. This nuanced approach is essential for balancing the legal authority to act with the economic responsibility to act wisely.

Disability Student Loan Forgiveness: A Step-by-Step Application Guide

You may want to see also

Explore related products

![]()

Precedent: Historical examples of executive actions on debt relief

The legality of President Biden's student debt forgiveness plan hinges on historical precedents of executive actions on debt relief. Examining past instances where presidents have used their authority to alleviate debt burdens provides critical context for understanding the current debate.

Example: During the Great Depression, President Franklin D. Roosevelt used executive orders to restructure farm mortgages and provide debt relief to struggling farmers through the Farm Credit Administration. This action was justified under the Emergency Farm Mortgage Act of 1933, which granted the president broad authority to address the agricultural crisis.

Analysis: Roosevelt's actions set a precedent for using executive power to address economic emergencies through debt relief. While the scale and scope differ, the legal rationale—leveraging existing statutes to respond to a national crisis—parallels arguments made in favor of Biden's student debt forgiveness. Both cases involve interpreting congressional authority broadly to address systemic issues.

Takeaway: Historical examples like Roosevelt's farm debt relief demonstrate that presidents have exercised authority to alleviate debt burdens during times of crisis. However, the key distinction lies in the statutory basis for such actions. Biden's plan relies on the Higher Education Relief Opportunities for Students (HEROES) Act of 2003, which grants the Secretary of Education authority to modify student loans during national emergencies. Critics argue this stretches the law's intent, while supporters point to past precedents of expansive executive interpretation.

Comparative Perspective: Another relevant example is President Gerald Ford's 1974 clemency program for Vietnam War draft evaders, which effectively forgave their legal debts to the government. While not directly related to financial debt, this action illustrates the executive branch's ability to waive obligations in the public interest. Similarly, Biden's plan frames student debt relief as a measure to address economic inequality and pandemic recovery, aligning with past uses of executive authority to promote societal welfare.

Practical Tip: When evaluating the legality of executive actions on debt relief, focus on the underlying statutory authority and the context in which it is applied. For instance, the HEROES Act explicitly allows modifications to student loans during emergencies, but the extent of such modifications remains a point of legal contention. Understanding these nuances can help distinguish between precedent-setting actions and potential overreach.

Canada Student Loan Forgiveness: A Step-by-Step Application Guide

You may want to see also

Frequently asked questions

The legality of President Biden's student debt forgiveness plan is a matter of ongoing debate. The Biden administration argues that the Higher Education Relief Opportunities for Students (HEROES) Act of 2003 grants the Secretary of Education the authority to modify student loans during national emergencies, such as the COVID-19 pandemic. However, critics and legal challenges argue that such broad forgiveness exceeds executive authority and requires congressional approval.

Yes, the Supreme Court ruled on Biden's student debt forgiveness plan in June 2023. In a 6-3 decision, the Court struck down the plan, stating that the administration overstepped its authority under the HEROES Act and that such significant policy changes required explicit congressional approval.

After the Supreme Court ruling, Biden's ability to forgive student debt through executive action is severely limited. However, the administration has explored alternative avenues, such as targeted loan forgiveness programs for specific groups (e.g., public service workers) and improving existing repayment plans, which may not face the same legal challenges.

Yes, Congress has the constitutional authority to pass legislation forgiving student debt. Such a law would likely be considered legal, as it would come from the legislative branch, which has the power to create and modify federal programs. However, passing such legislation would require bipartisan support or a majority in both chambers, which has proven challenging.

Yes, there are legal alternatives to widespread student debt forgiveness. These include income-driven repayment plans, public service loan forgiveness, and targeted relief for borrowers who were defrauded by predatory schools. Additionally, the Biden administration has expanded existing programs and streamlined processes to provide relief to specific groups of borrowers without requiring broad executive action.