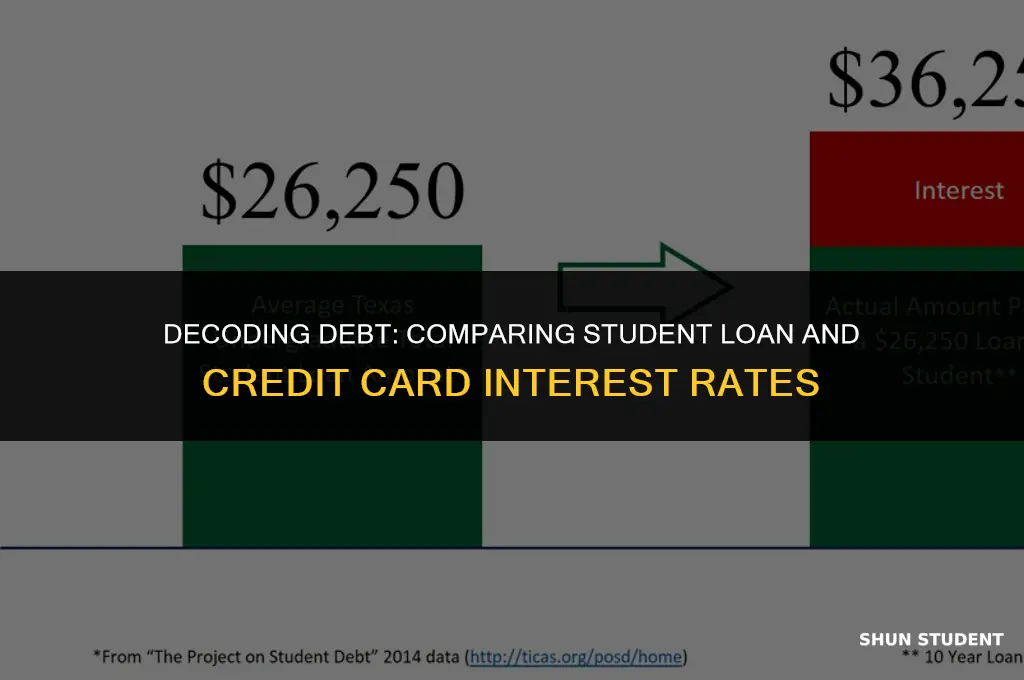

When comparing the interest rates on student loans versus credit cards, it's essential to understand the differences in how these financial tools operate. Student loans are designed to help cover the cost of higher education and typically come with lower interest rates than credit cards, which are meant for short-term borrowing and can carry much higher rates. Additionally, student loans often have fixed interest rates, meaning the rate stays the same over the life of the loan, whereas credit card rates can be variable and fluctuate based on market conditions. Understanding these distinctions can help you make informed decisions about managing your debt and prioritizing your financial goals.

Explore related products

What You'll Learn

- Comparing Interest Rates: Evaluate the interest rates of your student loan and credit card to determine which is lower

- Grace Periods: Understand if your student loan has a grace period where interest doesn't accrue, unlike credit cards

- Repayment Terms: Compare the repayment terms and schedules of your student loan versus credit card debt

- Tax Benefits: Explore potential tax deductions or benefits available for student loan interest payments, which credit cards may not offer

- Credit Impact: Consider how each type of debt affects your credit score and overall financial health differently

![]()

Comparing Interest Rates: Evaluate the interest rates of your student loan and credit card to determine which is lower

To effectively compare the interest rates of your student loan and credit card, you need to look beyond the surface-level annual percentage rates (APRs). Start by gathering detailed information about both accounts, including the exact interest rates, any variable rate indices, and the frequency of rate adjustments. For variable-rate loans or credit cards, research the historical trends of the indices to which they are tied, such as the LIBOR or Prime Rate, to anticipate potential future rate changes.

Next, calculate the total interest cost for both the student loan and credit card over a specific timeframe, such as the next 12 months or the life of the loan. This will give you a clearer picture of which option is more cost-effective in the long run. Consider using online calculators or spreadsheets to automate this process and ensure accuracy.

When comparing interest rates, it's also crucial to factor in any additional fees or charges associated with each account. For example, credit cards may have annual fees, late payment fees, or balance transfer fees that can significantly impact the overall cost. Similarly, student loans may have origination fees, prepayment penalties, or other charges that should be taken into account.

Another important aspect to consider is the tax implications of each type of debt. Student loan interest is often tax-deductible, which can reduce the effective interest rate. Credit card interest, on the other hand, is generally not tax-deductible. This means that the true cost of credit card debt may be higher than it initially appears.

Finally, evaluate your personal financial situation and goals when deciding between paying off your student loan or credit card debt. If you have a high-interest credit card balance that is causing significant financial stress, it may be more beneficial to focus on paying that off first, even if your student loan interest rate is slightly lower. Conversely, if you have a stable financial situation and are looking to minimize long-term costs, prioritizing your student loan repayment may be the better choice.

By taking a comprehensive approach to comparing interest rates, you can make an informed decision about which debt to tackle first and develop a strategic plan for managing your finances effectively.

Understanding When Student Loan Interest Begins: A Guide for Borrowers

You may want to see also

Explore related products

![]()

Grace Periods: Understand if your student loan has a grace period where interest doesn't accrue, unlike credit cards

Unlike credit cards, which typically start accruing interest immediately after a purchase, many student loans offer a grace period. This is a set timeframe during which no interest is charged on the loan balance. Understanding whether your student loan includes a grace period, and if so, how long it lasts, can be crucial in managing your debt effectively.

The grace period on student loans varies depending on the type of loan and the lender. Federal student loans, such as Direct Subsidized and Unsubsidized Loans, generally offer a six-month grace period after graduation or when the borrower's enrollment status changes to less than half-time. During this period, interest does not accrue, providing a temporary reprieve from the growing balance. However, it's important to note that not all student loans come with a grace period, and private loans may have different terms or no grace period at all.

To determine if your student loan has a grace period, you should review your loan agreement or contact your lender directly. They can provide specific details about your loan terms, including any grace period provisions. If you're unsure about your loan type or lender, you can also consult with a financial aid advisor at your educational institution or a student loan counselor.

Knowing about your grace period can help you plan your finances better. For instance, if you have a six-month grace period, you might choose to allocate those months to finding a job and getting settled before you start making loan payments. Additionally, understanding the grace period can help you avoid unnecessary interest charges. If you have the means, you might consider making payments during the grace period to reduce the principal balance, which can save you money on interest in the long run.

In summary, a grace period on a student loan is a valuable feature that can provide temporary relief from interest charges. By understanding the specifics of your loan's grace period, you can make informed decisions about managing your student debt.

Unraveling the Tax Benefits of Reporting Student Loan Interest

You may want to see also

Explore related products

![]()

Repayment Terms: Compare the repayment terms and schedules of your student loan versus credit card debt

Understanding the repayment terms of your student loan and credit card debt is crucial in managing your finances effectively. Student loans typically offer more flexible repayment plans compared to credit cards. For instance, student loans may provide options such as income-driven repayment plans, which adjust your monthly payments based on your income and family size. Additionally, student loans often have longer repayment terms, ranging from 10 to 25 years, which can result in lower monthly payments.

In contrast, credit card debt usually requires a minimum monthly payment, which may not be as flexible as student loan repayments. Credit card companies often set a fixed percentage of the outstanding balance as the minimum payment, which can make it challenging to pay off the debt quickly. Furthermore, credit cards typically have shorter repayment terms, and if you only make the minimum payments, it could take years to pay off the balance in full.

One key difference between student loans and credit card debt is the treatment of interest. Student loans generally have fixed interest rates, which means the rate remains the same throughout the life of the loan. This predictability can help you plan your repayments more effectively. On the other hand, credit card interest rates are often variable and can increase over time, especially if you miss payments or if the prime rate changes. This variability can make it more difficult to anticipate your future payments and pay off the debt.

When comparing the repayment terms of your student loan and credit card debt, it's essential to consider the total cost of borrowing. While student loans may have lower interest rates, they often involve borrowing larger amounts of money. Credit card debt, although typically associated with higher interest rates, usually involves smaller balances. Therefore, it's crucial to calculate the total interest you will pay over the life of each loan and factor this into your repayment strategy.

In summary, the repayment terms of student loans and credit card debt differ significantly. Student loans offer more flexible repayment plans, longer terms, and fixed interest rates, while credit card debt requires minimum monthly payments, has shorter repayment terms, and often features variable interest rates. Understanding these differences can help you prioritize your debts and develop a more effective repayment strategy.

Why Your Student Loan Interest Payments Aren't Tax Deductible

You may want to see also

Explore related products

![]()

Tax Benefits: Explore potential tax deductions or benefits available for student loan interest payments, which credit cards may not offer

One significant advantage of student loans over credit cards is the potential for tax benefits. Unlike credit card interest, student loan interest payments may be eligible for tax deductions, which can lower your overall tax liability. This benefit is particularly valuable for individuals in higher tax brackets. To qualify for this deduction, you must meet certain criteria, such as being legally responsible for the loan, using the funds solely for education expenses, and maintaining accurate records of your interest payments.

The tax deduction for student loan interest is subject to income limits and phase-out thresholds, which means that the benefit may be reduced or eliminated for higher-income earners. Additionally, you cannot claim this deduction if you are married and filing separately, or if someone else claims you as a dependent on their tax return. It's essential to consult with a tax professional to determine your eligibility and the potential impact of this deduction on your tax situation.

Another tax benefit associated with student loans is the possibility of claiming the American Opportunity Tax Credit or the Lifetime Learning Credit, depending on your circumstances. These credits can help offset the cost of tuition and other education-related expenses, further reducing your tax burden. To take advantage of these credits, you must meet specific requirements, such as being enrolled in a qualified educational institution and incurring eligible education expenses.

In contrast, credit card interest payments generally do not qualify for tax deductions or credits. This means that the interest you pay on a credit card is typically not tax-deductible, and you cannot claim any tax benefits for using a credit card to finance your education. This difference in tax treatment is a crucial factor to consider when comparing the cost of student loans versus credit cards.

When evaluating the tax benefits of student loans versus credit cards, it's important to consider the long-term implications of each option. While student loans may offer immediate tax advantages, they also come with longer repayment terms and potentially higher overall interest costs. Credit cards, on the other hand, may have higher interest rates but offer more flexibility in terms of repayment and can be paid off more quickly. Ultimately, the decision between student loans and credit cards should be based on a comprehensive analysis of your financial situation, including your income, expenses, and long-term financial goals.

Student Loan Interest Resumes Post-COVID: What Borrowers Need to Know

You may want to see also

Explore related products

![]()

Credit Impact: Consider how each type of debt affects your credit score and overall financial health differently

Student loans and credit card debt are two common types of debt that can have significantly different impacts on your credit score and overall financial health. While both types of debt can negatively affect your credit score if not managed properly, student loans tend to have a more gradual and long-term impact, whereas credit card debt can have a more immediate and severe impact.

One reason for this difference is that student loans are typically considered installment loans, which means that you make regular, fixed payments over a set period of time. This can help to demonstrate to lenders that you are responsible and reliable, as long as you make your payments on time. Credit card debt, on the other hand, is considered revolving debt, which means that you can borrow and repay funds as needed, up to a certain credit limit. This can make it more difficult for lenders to assess your creditworthiness, as they do not have a clear picture of your repayment habits.

Another factor that can contribute to the different credit impacts of student loans and credit card debt is the interest rates associated with each type of debt. Student loans typically have lower interest rates than credit cards, which can make them less costly in the long run. However, credit card debt can quickly become more expensive if you are not able to pay off your balance in full each month, as the interest charges can compound over time.

In terms of overall financial health, student loans can have a significant impact on your ability to save for other financial goals, such as buying a home or starting a family. This is because student loan payments can be a substantial monthly expense, which can limit your ability to allocate funds to other areas of your budget. Credit card debt can also have a negative impact on your financial health, as high interest rates and fees can make it difficult to pay off your balance and move forward with your financial goals.

Ultimately, it is important to manage both student loans and credit card debt responsibly in order to minimize their impact on your credit score and overall financial health. This may involve making timely payments, keeping your credit utilization ratio low, and seeking assistance from a financial advisor or credit counselor if needed. By taking a proactive approach to managing your debt, you can work towards achieving your financial goals and maintaining a healthy credit score.

Understanding the Student Loan Interest Phaseout: What You Need to Know

You may want to see also

Frequently asked questions

Typically, student loan interest rates are lower than credit card interest rates. Federal student loans, for example, have interest rates that are set by Congress and are generally lower than those offered by credit card companies. Private student loans may have variable rates that could be lower or higher than credit card rates, depending on the lender and your creditworthiness.

To compare your student loan interest rate to a credit card's interest rate, you'll need to know the Annual Percentage Rate (APR) of both. The APR is the total cost of borrowing, including interest and fees, expressed as a yearly rate. You can find the APR on your student loan documents or by contacting your lender. For credit cards, the APR is usually listed on your monthly statement or on the card issuer's website. Once you have both APRs, you can compare them directly.

Having a lower interest rate on your student loan compared to a credit card can have several implications. Firstly, it means you'll pay less in interest over the life of the loan, which can save you money. Secondly, it may allow you to pay off your student loan faster, as more of your monthly payment will go towards the principal balance rather than interest. Finally, it can also impact your credit score positively, as lower interest rates are often associated with better credit terms and responsible borrowing behavior.