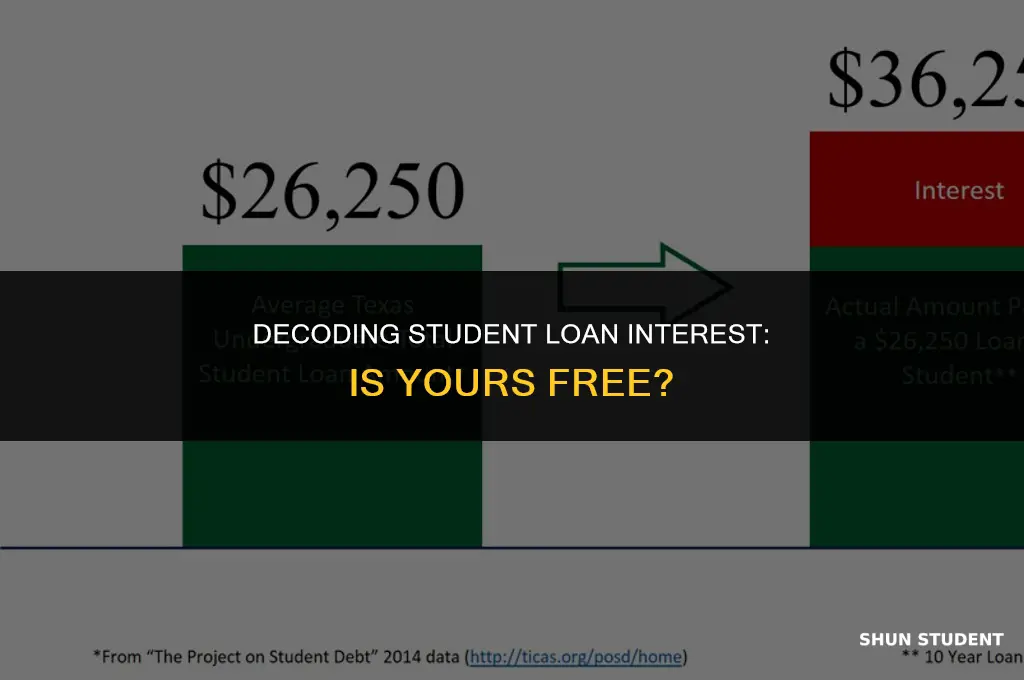

Many students and recent graduates often wonder if their student loans are interest-free. The answer to this question depends on several factors, including the type of loan, the lender, and the borrower's specific circumstances. Generally, federal student loans in the United States do not accrue interest while the borrower is enrolled in school at least half-time. However, private student loans typically do not offer this benefit, and interest may begin accruing immediately after the loan is disbursed. Additionally, some lenders may offer interest-free periods or lower interest rates for borrowers who meet certain criteria, such as maintaining a high credit score or making timely payments. To determine if your student loan is interest-free, it's essential to review the loan agreement and contact your lender for clarification on the terms and conditions of your specific loan.

Explore related products

What You'll Learn

- Eligibility Criteria: Understand the requirements to qualify for interest-free student loans, such as academic performance or financial need

- Application Process: Learn the steps to apply for interest-free student loans, including necessary documentation and deadlines

- Loan Repayment Terms: Discover the repayment conditions, such as grace periods and monthly installments, for interest-free student loans

- Benefits and Drawbacks: Weigh the advantages of interest-free loans against potential downsides, like strict eligibility or limited loan amounts

- Alternatives to Interest-Free Loans: Explore other financial aid options, such as scholarships, grants, or low-interest loans, if interest-free loans aren't available

![]()

Eligibility Criteria: Understand the requirements to qualify for interest-free student loans, such as academic performance or financial need

To qualify for interest-free student loans, understanding the eligibility criteria is crucial. These criteria typically revolve around academic performance and financial need. For instance, many loan programs require students to maintain a certain GPA to demonstrate their commitment to their studies. This ensures that the funds are being used effectively and that the student has a good chance of graduating and repaying the loan.

Financial need is another key factor. Students must often provide proof of their financial situation, such as tax returns or FAFSA (Free Application for Federal Student Aid) forms. This helps lenders determine whether the student genuinely requires assistance to cover their educational expenses. Interest-free loans are usually awarded to those who demonstrate significant financial need, as they are intended to make higher education more accessible to students from lower-income backgrounds.

In addition to these basic criteria, some loan programs may have additional requirements. For example, students may need to be enrolled in a specific field of study or attend a particular institution to qualify. Others may require community service or involvement in certain extracurricular activities. It's essential to research the specific loan programs available and understand their unique eligibility requirements to maximize the chances of approval.

Students should also be aware of any deadlines associated with applying for interest-free loans. Missing these deadlines can result in the loss of valuable financial aid opportunities. Furthermore, maintaining good credit and avoiding excessive debt can also play a role in eligibility, as lenders may view these factors as indicators of the student's ability to manage their finances responsibly.

In conclusion, understanding the eligibility criteria for interest-free student loans is vital for students seeking financial assistance. By focusing on academic performance, financial need, and other specific requirements, students can position themselves to qualify for these beneficial loan programs and reduce the burden of higher education costs.

Maximize Tax Savings: Student Loan Interest Deduction Strategies

You may want to see also

Explore related products

![]()

Application Process: Learn the steps to apply for interest-free student loans, including necessary documentation and deadlines

To apply for interest-free student loans, you must follow a specific application process that includes gathering necessary documentation and meeting deadlines. The first step is to research and identify the loan programs that offer interest-free options. This may include federal loans, state-specific programs, or private lenders that offer interest-free loans to students. Once you have identified the programs, you will need to gather the required documentation, which may include proof of income, tax returns, and academic transcripts.

The next step in the application process is to fill out the loan application form. This form will require you to provide personal and financial information, as well as details about your academic program and enrollment status. Be sure to fill out the form accurately and completely, as any errors or omissions could delay the processing of your application. After submitting the application form, you may need to provide additional documentation or information to the lender.

One important aspect of the application process is meeting deadlines. Interest-free student loans often have specific deadlines for application, and missing these deadlines could result in you being ineligible for the loan. Be sure to mark your calendar with the application deadlines and allow yourself plenty of time to gather the necessary documentation and complete the application form.

In addition to meeting deadlines, it is also important to be aware of any fees associated with the loan application process. Some lenders may charge application fees or origination fees, which could add to the overall cost of the loan. Be sure to carefully review the terms and conditions of the loan program to understand any fees that may be associated with the application process.

Finally, it is important to remember that interest-free student loans are not always easy to obtain. Lenders may have strict eligibility requirements, and the application process can be competitive. Be prepared to provide a strong application and to demonstrate your financial need and academic merit. By following these steps and being diligent in your application process, you can increase your chances of securing an interest-free student loan.

Tax Tips: Where to Input Student Loan Interest on Your Return

You may want to see also

Explore related products

![]()

Loan Repayment Terms: Discover the repayment conditions, such as grace periods and monthly installments, for interest-free student loans

Understanding the repayment terms of an interest-free student loan is crucial for borrowers to manage their finances effectively. These terms outline the conditions under which the loan must be repaid, including the grace period and monthly installment amounts. The grace period is a specified timeframe after graduation or leaving school during which the borrower is not required to make any loan payments. This period allows individuals to establish themselves financially before beginning repayment. Monthly installments are the regular payments made towards the loan principal after the grace period ends. The amount of these installments is typically determined by the loan provider and is based on the total loan amount and the repayment period.

Interest-free student loans often have flexible repayment terms to accommodate the varying financial situations of borrowers. Some loans may offer a longer grace period, while others might have lower monthly installments. It is essential for borrowers to carefully review and understand these terms to ensure they can meet their repayment obligations without financial strain. Additionally, some interest-free loans may have specific conditions or requirements that must be met to maintain the interest-free status, such as maintaining a certain GPA or enrolling in a particular field of study.

Borrowers should also be aware of any potential penalties or fees associated with late or missed payments. Understanding these consequences can help individuals avoid financial pitfalls and maintain a good credit standing. Furthermore, it is advisable for borrowers to explore options for early repayment if they are in a position to do so, as this can save money on interest and reduce the overall loan burden.

In conclusion, comprehending the repayment terms of an interest-free student loan is vital for effective financial planning and management. By understanding the grace period, monthly installments, and any associated conditions or penalties, borrowers can make informed decisions and ensure they meet their repayment obligations successfully.

Understanding Student Loan Consolidation Interest Rates: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Benefits and Drawbacks: Weigh the advantages of interest-free loans against potential downsides, like strict eligibility or limited loan amounts

Interest-free loans can be a significant financial boon, particularly for students burdened by the rising costs of higher education. One of the primary benefits is the absence of interest charges, which can save borrowers substantial amounts of money over the repayment period. This feature is especially advantageous for those who may struggle to secure employment immediately after graduation, as it reduces the financial pressure of accumulating debt.

However, it's crucial to consider the potential drawbacks. Strict eligibility criteria often accompany interest-free loans, limiting access to those who meet specific academic, financial, or demographic requirements. This can create disparities in who benefits from these loans, potentially excluding those who need financial assistance the most. Additionally, interest-free loans may come with limited loan amounts, which might not cover the full cost of tuition, fees, and living expenses. Borrowers may need to supplement these loans with other forms of financial aid or personal savings.

Another consideration is the repayment terms. While interest-free, these loans still require timely repayment, and failure to do so can result in penalties or damage to the borrower's credit score. Furthermore, some interest-free loans may have variable repayment schedules or require payments while the borrower is still in school, adding to the financial strain.

In conclusion, while interest-free loans offer clear advantages, they also come with potential downsides that borrowers must carefully weigh. Understanding the eligibility criteria, loan limits, and repayment terms is essential for making informed decisions about whether an interest-free loan is the right choice for one's educational financing needs.

When Will Normal Student Loan Interest Rates Resume? Key Dates Explained

You may want to see also

Explore related products

![]()

Alternatives to Interest-Free Loans: Explore other financial aid options, such as scholarships, grants, or low-interest loans, if interest-free loans aren't available

If interest-free loans aren't an option for your student loan needs, there are several alternative financial aid options to consider. Scholarships are a popular choice, as they provide funds that don't need to be repaid. There are countless scholarships available, catering to a wide range of students with different backgrounds, interests, and academic achievements. Some scholarships are merit-based, while others are need-based, and there are also scholarships for specific fields of study or for students with unique circumstances.

Grants are another form of financial aid that doesn't require repayment. They are typically awarded based on financial need and can be a significant source of funding for students. Federal grants, such as the Pell Grant, are a common option, but there are also state and institutional grants available. It's important to apply for grants early, as they can be competitive and have limited funding.

Low-interest loans can also be a viable alternative to interest-free loans. While they do accrue interest, the rates are often much lower than those of private loans. Federal student loans, such as the Direct Subsidized Loan and the Direct Unsubsidized Loan, offer relatively low interest rates and come with various benefits, including income-driven repayment plans and loan forgiveness options.

When exploring these alternatives, it's crucial to consider your individual circumstances and financial needs. Research and compare different options to find the best fit for you. Utilize resources such as the Free Application for Federal Student Aid (FAFSA) to determine your eligibility for various forms of financial aid, and don't hesitate to reach out to financial aid advisors for guidance and support.

Remember, while interest-free loans may not be available, there are still numerous options to help make your education more affordable. By carefully considering scholarships, grants, and low-interest loans, you can create a financial aid package that meets your needs and helps you achieve your educational goals.

Curious Minds Engage: Student Questions Signal Interest and Active Learning

You may want to see also

Frequently asked questions

It depends on the type of student loan you have. Federal student loans typically have interest rates that are determined by the government and can vary each year. Private student loans have interest rates set by the lender, which can be fixed or variable. To determine if your specific loan is interest-free, you would need to review the terms and conditions of your loan agreement or contact your loan servicer.

Yes, there are some programs that offer interest-free student loans. For example, the Perkins Loan Program is a federal loan program that offers interest-free loans to undergraduate and graduate students with exceptional financial need. Additionally, some private lenders offer interest-free periods or low-interest rates for certain types of loans. It's important to research and compare different loan options to find the best fit for your financial situation.

There are a few ways to make your student loan interest-free, at least temporarily. One option is to apply for a loan deferment or forbearance, which can pause or reduce your interest accrual for a certain period of time. Another option is to make interest-only payments while you're in school or during your grace period, which can help prevent interest from capitalizing and increasing your overall loan balance. Finally, you may be able to qualify for loan forgiveness or discharge programs, which can eliminate your loan balance entirely, including any accrued interest.