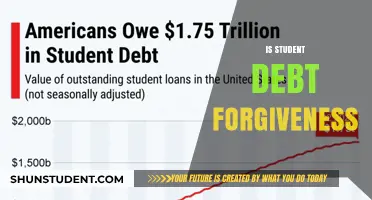

The topic of whether the student forgiveness plan is legitimate has sparked considerable debate and scrutiny, as millions of borrowers seek relief from mounting student loan debt. With various programs and proposals emerging, including those from government agencies and private entities, it is crucial to evaluate their authenticity, eligibility criteria, and long-term implications. While some plans, such as those offered by the U.S. Department of Education, are backed by official policies and regulations, others may be scams or misleading offers targeting vulnerable borrowers. Understanding the differences between legitimate forgiveness programs and fraudulent schemes is essential for students and graduates to make informed decisions and avoid potential financial pitfalls.

Explore related products

What You'll Learn

- Eligibility Criteria: Who qualifies for student loan forgiveness under the current plan

- Application Process: Steps to apply and required documentation for forgiveness

- Types of Loans Covered: Which federal or private loans are eligible for forgiveness

- Scams and Red Flags: How to avoid fraudulent forgiveness programs and scams

- Impact on Credit Score: Does applying for forgiveness affect your credit score

![]()

Eligibility Criteria: Who qualifies for student loan forgiveness under the current plan?

The current student loan forgiveness plan, often referred to as the Public Service Loan Forgiveness (PSLF) program, has specific eligibility criteria that borrowers must meet to qualify. Understanding these requirements is crucial for anyone hoping to benefit from this initiative. At its core, the program is designed for individuals who commit to public service careers, but the devil is in the details. To qualify, borrowers must make 120 qualifying payments while working full-time for a qualifying employer. These payments must be made under an income-driven repayment plan, which adjusts monthly payments based on income and family size. This structure ensures that forgiveness is accessible to those who dedicate their careers to public service while managing their loans responsibly.

Qualifying employers under the PSLF program include government organizations at any level (federal, state, local, or tribal), non-profit organizations that are tax-exempt under Section 501(c)(3) of the Internal Revenue Code, and some other types of non-profits that provide certain public services. Notably, labor unions, political organizations, and for-profit organizations do not qualify, even if the borrower’s role involves public service. Full-time employment is defined as working at least 30 hours per week or the employer’s definition of full-time, whichever is greater. Part-time workers in multiple jobs can combine their hours to meet this requirement, provided each employer qualifies.

The type of loans also plays a critical role in eligibility. Only Direct Loans qualify for PSLF. Borrowers with Federal Family Education Loans (FFEL) or Perkins Loans must consolidate them into a Direct Consolidation Loan to become eligible. This step is often overlooked but is essential for those with older loan types. Additionally, the 120 qualifying payments must be made after October 1, 2007, and do not need to be consecutive. Periods of deferment, forbearance, or default do not count toward the total, making consistent repayment a key factor.

One common pitfall is the confusion around income-driven repayment plans. Borrowers must enroll in one of these plans—such as Income-Based Repayment (IBR), Pay As You Earn (PAYE), or Revised Pay As You Earn (REPAYE)—to ensure their payments qualify. Standard repayment plans, even if affordable, do not count unless the payment amount is at least as much as it would be under an income-driven plan. This nuance highlights the importance of proactive loan management and staying informed about repayment options.

Finally, borrowers must submit a PSLF form to their loan servicer to track their qualifying payments and ensure they are on the right path. This form can be submitted annually or whenever a borrower changes employers to confirm continued eligibility. While the PSLF program is legitimate, its strict criteria mean that not all borrowers will qualify. However, for those who meet the requirements, it offers a pathway to financial freedom after a decade of dedicated public service. Careful planning, documentation, and adherence to the rules are essential to successfully navigating this program.

Unlocking Debt-Free Futures: Strategies for Student Loan Forgiveness Explained

You may want to see also

Explore related products

![]()

Application Process: Steps to apply and required documentation for forgiveness

Navigating the application process for student loan forgiveness can feel like deciphering a complex puzzle, but breaking it down into manageable steps simplifies the journey. The first step is identifying the specific forgiveness program you qualify for, such as Public Service Loan Forgiveness (PSLF), Teacher Loan Forgiveness, or Income-Driven Repayment (IDR) forgiveness. Each program has unique eligibility criteria, so research thoroughly to ensure you meet the requirements before proceeding.

Once you’ve determined the appropriate program, gather the required documentation. For PSLF, for instance, you’ll need proof of employment certification from a qualifying employer, typically a government or nonprofit organization. Teacher Loan Forgiveness applicants must provide documentation of their teaching service in low-income schools, including employment verification and principal certification. IDR forgiveness applicants will need records of their income-driven repayment plan enrollment and payment history. Organizing these documents beforehand streamlines the application process and reduces the risk of delays.

The next step involves completing the application forms accurately. For PSLF, this includes submitting the Employment Certification Form (ECF) annually or when switching employers to track qualifying payments. Teacher Loan Forgiveness requires the Teacher Loan Forgiveness Application, which must be submitted after completing the required five consecutive years of teaching. IDR forgiveness applications often involve submitting an income recertification form annually to maintain eligibility. Double-check all forms for accuracy, as errors can lead to processing delays or denials.

After submitting your application, monitor its progress and stay proactive. Keep copies of all submitted documents and correspondence for your records. Some programs, like PSLF, allow you to track your qualifying payments through the Department of Education’s website. If you encounter issues or have questions, reach out to your loan servicer or the program’s support team for assistance. Patience is key, as processing times can vary, but staying informed ensures you’re on the right track.

Finally, be cautious of scams targeting student loan borrowers. Legitimate forgiveness programs are free to apply for, and you should never pay a third party to handle your application. If an offer seems too good to be true or requires upfront fees, it’s likely fraudulent. Stick to official government resources and verified loan servicers to protect yourself and your financial future. By following these steps and staying vigilant, you can navigate the application process with confidence and increase your chances of securing legitimate student loan forgiveness.

Unveiling the Hidden Scams in Student Loan Forgiveness Programs

You may want to see also

Explore related products

![]()

Types of Loans Covered: Which federal or private loans are eligible for forgiveness?

Federal student loan forgiveness programs, such as Public Service Loan Forgiveness (PSLF) and income-driven repayment (IDR) plans, exclusively cover federal loans—think Direct Loans, Stafford Loans, PLUS Loans, and Consolidation Loans. Private loans, like those from Sallager or Wells Fargo, are ineligible unless refinanced into a federal Direct Consolidation Loan, a rare and often costly move. For example, a teacher with $50,000 in federal Direct Loans could qualify for PSLF after 10 years of payments, but their private $10,000 Sallager loan remains untouched. Key takeaway: Always verify your loan type through the National Student Loan Data System (NSLDS) before pursuing forgiveness.

The Public Service Loan Forgiveness (PSLF) program is particularly stringent about loan types. Only Direct Loans qualify; Federal Family Education Loans (FFEL) or Perkins Loans must first be consolidated into a Direct Consolidation Loan. For instance, a social worker with FFEL loans would need to consolidate and make 120 qualifying payments under a PSLF-eligible repayment plan. Practical tip: Consolidation resets your payment count, so initiate this process early if switching from ineligible loan types.

Income-driven repayment (IDR) plans, such as REPAYE or IBR, offer forgiveness after 20–25 years of payments, but again, only federal loans apply. Private loans are excluded, even if they’re in default. For example, a nurse with $80,000 in federal loans under REPAYE could see forgiveness after 25 years, while their $20,000 private loan remains in repayment. Caution: IDR forgiveness may trigger taxable income, so consult a tax advisor to plan ahead.

Temporary programs like the one-time IDR account adjustment or the Fresh Start initiative for defaulted loans also focus on federal loans. These programs can retroactively credit payments toward forgiveness, but private loans are ineligible. For instance, a borrower in default on federal loans could use Fresh Start to rehabilitate their account and regain eligibility for PSLF, but their private loans would remain unaffected. Action step: Check if your federal loans qualify for these adjustments by contacting your loan servicer or visiting the Federal Student Aid website.

In contrast, private loan forgiveness is virtually nonexistent outside of rare employer or state-based programs. Some states, like Maryland, offer forgiveness for private loans in specific fields (e.g., nursing), but these are exceptions. For example, a Maryland nurse might receive up to $10,000 in private loan forgiveness through the state’s Nurse Support Program. Comparative insight: While federal forgiveness is structured and widespread, private loan relief is fragmented and limited, making it essential to prioritize federal loan repayment strategies.

Student Loan Forgiveness After Death: A Guide for Borrowers

You may want to see also

Explore related products

$7.99

![]()

Scams and Red Flags: How to avoid fraudulent forgiveness programs and scams

Beware of upfront fees. Legitimate student loan forgiveness programs, such as those offered by the U.S. Department of Education, never require payment to apply or enroll. Scammers often lure borrowers with promises of immediate relief or exclusive access, demanding fees for services that are either unnecessary or fraudulent. If an organization asks for money upfront, especially via unconventional methods like gift cards or wire transfers, it’s a major red flag. Always verify the program’s legitimacy through official government websites before engaging.

Scrutinize guarantees of instant forgiveness. No legitimate program can guarantee loan forgiveness without reviewing eligibility criteria, such as employment in public service or income-driven repayment plans. Fraudulent schemes often use high-pressure tactics, claiming limited-time offers or exclusive deals to rush borrowers into decisions. Legitimate processes take time, involve documentation, and require approval from official agencies. If it sounds too good to be true, it probably is.

Check for official affiliations and credentials. Reputable forgiveness programs are administered by government agencies or certified loan servicers. Scammers often mimic official branding, using names like “Federal Student Loan Assistance” or “Department of Education Services” to appear legitimate. Always cross-reference contact information with the Federal Student Aid website (studentaid.gov) and avoid sharing personal details until you’ve confirmed the organization’s authenticity. A quick search for reviews or complaints can also reveal patterns of fraudulent behavior.

Understand the role of third-party companies. While some private companies offer assistance with navigating forgiveness programs, they cannot expedite or guarantee results. Legitimate third parties charge reasonable fees after services are rendered, not upfront. Be cautious of companies claiming insider connections or special access to government programs. Borrowers can always apply for forgiveness directly through official channels without intermediaries, often at no cost.

Stay informed and proactive. Scammers exploit confusion around student loan policies, especially during periods of change, such as when new forgiveness programs are announced. Regularly check updates from trusted sources like the Department of Education and avoid relying on unsolicited emails, calls, or ads. If you suspect fraud, report it to the Federal Trade Commission (FTC) and your loan servicer immediately. Protecting your financial information and staying vigilant is the best defense against predatory scams.

Did You Receive a Student Loan Forgiveness Email? What to Know

You may want to see also

Explore related products

$27.89 $29.99

![]()

Impact on Credit Score: Does applying for forgiveness affect your credit score?

Applying for student loan forgiveness does not directly impact your credit score. Credit bureaus—Equifax, Experian, and TransUnion—do not consider the act of applying for forgiveness as a negative or positive factor in their scoring models. This is because forgiveness programs, such as Public Service Loan Forgiveness (PSLF) or income-driven repayment (IDR) forgiveness, are government-backed initiatives designed to alleviate financial burden, not to penalize borrowers. However, the process and its outcomes can indirectly influence your credit score through related financial behaviors.

One indirect way forgiveness applications might affect your credit is through payment status during processing. For instance, if you stop making payments while awaiting approval for forgiveness, and your servicer reports missed payments, your credit score could drop. Late payments remain on your credit report for up to seven years and are a significant factor in credit scoring. To avoid this, continue making payments until your forgiveness application is officially approved. Some programs, like PSLF, even allow you to request a refund for payments made during the review period, but this requires proactive management.

Another consideration is the type of forgiveness program. Loan discharge through bankruptcy, for example, is treated differently from PSLF or IDR forgiveness. Bankruptcy discharge appears on your credit report and can severely damage your score for up to 10 years. In contrast, PSLF or IDR forgiveness does not appear on your credit report as a negative mark. Instead, the loan is reported as "paid as agreed," which is neutral. Understanding these distinctions is crucial for borrowers weighing their options.

To protect your credit score during the forgiveness process, monitor your credit report regularly. Use free services like AnnualCreditReport.com to check for inaccuracies, such as incorrectly reported missed payments. Additionally, maintain a low credit utilization ratio (below 30%) and avoid opening new credit accounts unnecessarily. These steps ensure that your credit profile remains strong while you navigate the forgiveness application.

In summary, applying for student loan forgiveness itself does not harm your credit score, but related actions—like pausing payments prematurely or pursuing bankruptcy discharge—can. By staying informed, managing payments carefully, and monitoring your credit, you can safeguard your financial health while pursuing debt relief.

Biden's Student Loan Forgiveness Plan: What You Need to Know

You may want to see also

Frequently asked questions

Yes, the student forgiveness plan, often referred to as Public Service Loan Forgiveness (PSLF) or other federal forgiveness programs, is a legitimate government initiative designed to help eligible borrowers eliminate their student loan debt after meeting specific criteria.

To verify legitimacy, visit official government websites like StudentAid.gov or contact your loan servicer directly. Avoid third-party companies that charge fees for services you can do yourself for free.

Yes, there are scams where fraudulent companies promise loan forgiveness for upfront fees. Legitimate programs do not require payment for application or enrollment. Always use official channels to apply.

Eligibility varies by program. For example, PSLF requires 120 qualifying payments while working full-time for a government or nonprofit organization. Income-Driven Repayment (IDR) plans may offer forgiveness after 20–25 years of payments.

No, legitimate federal forgiveness plans like PSLF or IDR forgiveness apply only to federal student loans. Private loans are not eligible and require separate arrangements with the lender.