Student debt forgiveness has become a contentious and pivotal issue in contemporary discussions surrounding higher education and economic policy. With millions of graduates burdened by escalating loan balances, the debate centers on whether the government should implement measures to alleviate or eliminate this debt. Proponents argue that forgiveness would stimulate the economy, reduce financial stress, and address systemic inequalities, particularly for marginalized communities. Critics, however, contend that such policies could be unfair to those who have already repaid their loans, potentially exacerbate inflation, and shift the financial burden onto taxpayers. As the cost of education continues to rise and student debt reaches unprecedented levels, the question of debt forgiveness remains a critical and polarizing topic with far-reaching implications for individuals, institutions, and the nation as a whole.

| Characteristics | Values |

|---|---|

| Current Status | As of October 2023, the Biden administration's student debt forgiveness plan is on hold due to legal challenges. The Supreme Court struck down the plan in June 2023. |

| Eligibility Criteria | Originally, individuals earning less than $125,000 (or $250,000 for married couples) were eligible for up to $20,000 in forgiveness. |

| Loan Types Covered | Federal student loans held by the U.S. Department of Education, including Direct Loans and FFELP loans (if consolidated into Direct Loans). |

| Amount of Forgiveness | Up to $10,000 for non-Pell Grant recipients; up to $20,000 for Pell Grant recipients. |

| Legal Challenges | The plan faced multiple lawsuits, culminating in the Supreme Court ruling it unconstitutional under the HEROES Act. |

| Alternative Relief | The Biden administration has expanded income-driven repayment plans and targeted loan cancellation for specific groups (e.g., public service workers, defrauded students). |

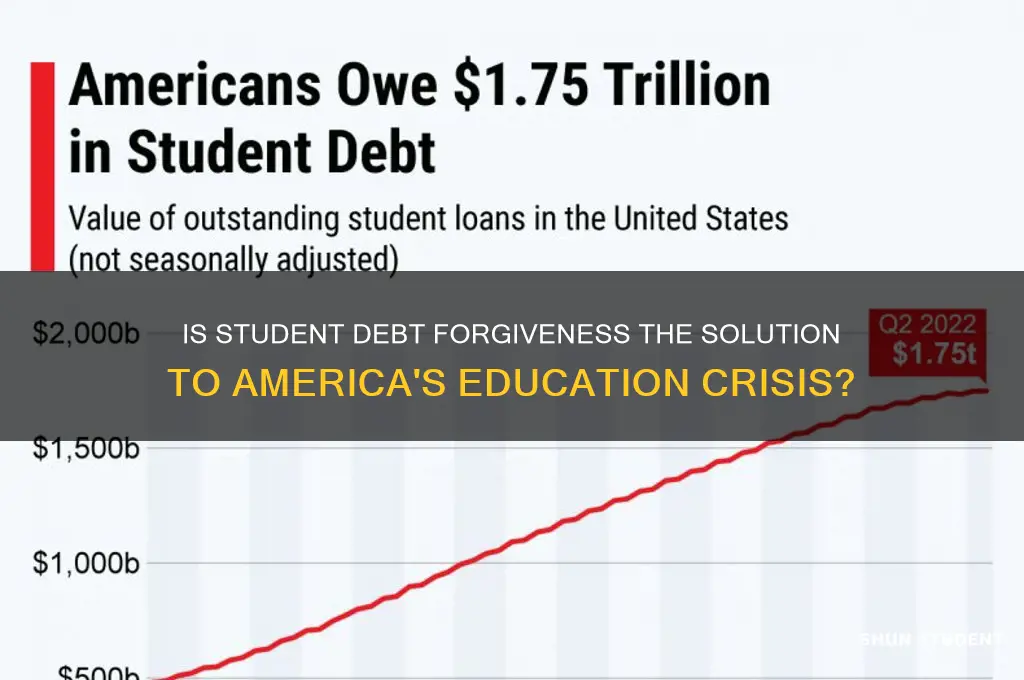

| Outstanding Debt | As of 2023, total U.S. student loan debt exceeds $1.7 trillion, affecting over 43 million borrowers. |

| Political Debate | Student debt forgiveness remains a divisive issue, with supporters citing economic relief and opponents raising concerns about cost and fairness. |

| Future Plans | The administration is exploring alternative pathways for debt relief, including regulatory actions under the Higher Education Act. |

Explore related products

What You'll Learn

![]()

Economic impact of debt forgiveness

Student debt forgiveness, a policy that has gained significant traction in recent years, is often framed as a moral imperative to alleviate the burden on borrowers. However, its economic implications are far-reaching and multifaceted. One immediate effect is the injection of disposable income into the economy. When borrowers are no longer obligated to make monthly payments, they are more likely to spend on goods and services, stimulating consumer demand. For instance, a study by the Roosevelt Institute estimated that canceling $1.4 trillion in student debt could boost GDP by $86 billion to $108 billion per year. This increased spending could particularly benefit sectors like retail, housing, and healthcare, creating a ripple effect of economic growth.

Critics argue, however, that debt forgiveness could lead to inflationary pressures if not carefully managed. By increasing consumer spending power, the policy might drive up prices, especially in sectors with inelastic supply, such as housing. To mitigate this risk, policymakers could pair forgiveness with measures to increase supply, such as investing in affordable housing or expanding access to higher education. Additionally, a phased approach to debt cancellation, rather than a one-time blanket forgiveness, could help prevent sudden shocks to the economy. For example, forgiving $10,000 per borrower annually over a decade would allow for gradual adjustment while still providing relief.

Another economic consideration is the potential impact on government finances. Debt forgiveness would reduce the flow of repayments into federal coffers, creating a short-term revenue gap. However, this could be offset by long-term gains, such as increased tax revenue from higher consumer spending and reduced reliance on social safety nets. For instance, borrowers with lower debt burdens are less likely to default on other loans or require public assistance, reducing strain on programs like SNAP or Medicaid. A cost-benefit analysis by the Levy Economics Institute suggests that the economic benefits of debt forgiveness could outweigh the initial fiscal cost within a decade.

Finally, the economic impact of debt forgiveness would vary significantly by demographic. Low-income borrowers, who often struggle the most with repayment, would experience the greatest relief, enabling them to invest in assets like homes or businesses. This could help narrow wealth gaps, particularly among marginalized communities. Conversely, high-income borrowers, who typically repay their loans more easily, would benefit less proportionally. Policymakers could enhance the equity of such a program by capping eligibility based on income or loan amount, ensuring that resources are targeted where they are most needed. For example, limiting forgiveness to borrowers earning below $75,000 annually could maximize economic and social returns.

In conclusion, while student debt forgiveness offers substantial economic benefits, its implementation requires careful calibration. By balancing immediate stimulus with long-term fiscal sustainability and targeting relief to those most in need, policymakers can maximize its positive impact while minimizing risks. The key lies in viewing debt forgiveness not as a standalone policy but as part of a broader strategy to foster inclusive economic growth.

Income-Based Student Loans: Forgiveness Eligibility and What You Need to Know

You may want to see also

Explore related products

![]()

Eligibility criteria for loan relief

Student debt forgiveness programs often hinge on eligibility criteria that can seem complex, but understanding these requirements is the first step toward potential relief. For instance, the Public Service Loan Forgiveness (PSLF) program requires borrowers to make 120 qualifying payments while working full-time for a government or nonprofit organization. This criterion is specific and demands careful documentation, such as employment certification forms, to ensure compliance. Similarly, income-driven repayment (IDR) plans, which can lead to loan forgiveness after 20–25 years of payments, require borrowers to recertify their income annually to maintain eligibility. These examples highlight how eligibility often ties to employment type, payment history, and financial status.

Analyzing these criteria reveals a pattern: eligibility is rarely automatic and requires proactive steps from the borrower. For example, the Biden administration’s one-time student debt relief plan (up to $20,000 for Pell Grant recipients and $10,000 for others) targeted individuals earning less than $125,000 annually (or $250,000 for married couples). This income threshold underscores how financial need is a recurring factor in forgiveness programs. Additionally, certain programs, like the Teacher Loan Forgiveness initiative, require borrowers to teach full-time for five consecutive years in a low-income school district. Such criteria emphasize the importance of aligning career choices with forgiveness opportunities to maximize eligibility.

To navigate these requirements effectively, borrowers should adopt a strategic approach. Start by identifying which programs align with your circumstances—for instance, federal loan borrowers are typically eligible for PSLF, while private loan holders are not. Next, maintain meticulous records of payments, employment, and income certifications, as these documents are often required to prove eligibility. For IDR plans, set calendar reminders to recertify income annually to avoid losing forgiveness progress. Finally, stay informed about policy changes; for example, the temporary expansion of PSLF in 2021 allowed previously ineligible payments to count toward forgiveness, benefiting thousands of borrowers.

Comparing eligibility criteria across programs reveals both overlaps and unique requirements. While PSLF and IDR plans both require federal loans, their payment structures and timelines differ significantly. State-based programs, such as the Maryland Bar Exam Expense Deduction, often have residency or profession-specific criteria. Borrowers in healthcare might explore the National Health Service Corps Loan Repayment Program, which offers up to $50,000 in exchange for two years of service in underserved areas. This diversity in criteria underscores the importance of researching programs tailored to individual profiles rather than relying on a one-size-fits-all approach.

Ultimately, eligibility for loan relief is a function of preparation, persistence, and precision. Borrowers who understand the nuances of each program, maintain accurate records, and align their careers with forgiveness opportunities are best positioned to benefit. For example, a borrower working in public service might strategically choose an IDR plan to minimize monthly payments while progressing toward PSLF. Conversely, a teacher in a low-income district could combine Teacher Loan Forgiveness with PSLF for maximum relief. By treating eligibility criteria as a roadmap rather than a barrier, borrowers can transform student debt from a burden into a manageable financial obligation.

Unlocking Debt-Free Future: Guide to Federal Student Loan Forgiveness

You may want to see also

Explore related products

![]()

Political debates on forgiveness

Student debt forgiveness has become a lightning rod in American politics, with debates often hinging on its economic and moral implications. At the heart of the argument is whether forgiving student loans constitutes a bailout or a necessary correction to systemic failures in higher education funding. Proponents argue that it would stimulate the economy by freeing millions from financial burdens, enabling them to buy homes, start businesses, and contribute more to consumer spending. Critics, however, contend that it unfairly redistributes wealth, rewarding those who chose higher education at the expense of taxpayers who did not. This divide often falls along partisan lines, with Democrats generally favoring forgiveness and Republicans opposing it, though nuances exist within each party.

Consider the practical mechanics of forgiveness: a one-time cancellation of $10,000 to $50,000 per borrower, as proposed in various plans, would cost the federal government hundreds of billions of dollars. Advocates frame this as an investment in economic mobility, citing studies showing that debt-free graduates are more likely to pursue careers in public service or entrepreneurship. Skeptics counter that such a policy lacks targeting, benefiting high-earning professionals alongside low-income graduates. To address this, some propose income-based eligibility caps, such as limiting forgiveness to borrowers earning under $125,000 annually, though even this raises questions about fairness and administrative complexity.

The moral argument for forgiveness centers on the idea that students were lured into debt by promises of upward mobility, only to face a job market that undervalues their degrees. For instance, the average student loan debt in the U.S. exceeds $30,000, with many borrowers struggling to make payments due to stagnant wages and rising living costs. Critics, however, argue that personal responsibility should prevail—that individuals who signed loan agreements must honor them. This tension highlights a deeper philosophical clash: Is education a public good deserving collective support, or a private investment with individual consequences?

A comparative analysis reveals that countries like Germany and Norway offer tuition-free higher education, reducing the need for debt forgiveness altogether. In contrast, the U.S. relies heavily on student loans, creating a cycle of debt that perpetuates inequality. This suggests that forgiveness, while contentious, could serve as a stopgap measure until systemic reforms—such as lowering tuition or expanding grants—are implemented. However, such reforms face their own political hurdles, as they require significant public investment and a rethinking of education as a societal priority rather than a market commodity.

Ultimately, the debate over student debt forgiveness is as much about values as it is about policy. It forces society to confront questions of equity, accountability, and the role of government in shaping opportunities. While forgiveness may provide immediate relief, it is not a panacea. Policymakers must balance short-term solutions with long-term strategies to prevent future generations from falling into the same debt trap. As the debate rages on, one thing is clear: the stakes are high, and the decisions made today will shape the economic and social landscape for decades to come.

Can Bankruptcy Erase Student Loans in Pennsylvania? What You Need to Know

You may want to see also

Explore related products

$7.99

![]()

Long-term effects on education costs

Student debt forgiveness, while offering immediate relief to borrowers, could inadvertently reshape the landscape of education costs over time. By reducing the financial burden on graduates, such policies might encourage more students to pursue higher education, potentially driving up demand. However, this increased demand could embolden institutions to raise tuition fees, knowing that students are more likely to borrow larger sums under the assumption of future forgiveness. This cycle could perpetuate rising education costs, negating the intended long-term benefits of debt relief.

Consider the behavioral economics at play: if students perceive that future debts might be forgiven, they may be less price-sensitive when choosing institutions or programs. For instance, a student might opt for a more expensive private university over a public one, anticipating that the debt will eventually be wiped clean. Institutions, aware of this mindset, could inflate costs further, citing improved facilities or expanded programs as justification. Over time, this dynamic could lead to a tuition arms race, where colleges compete not on affordability but on the perceived value of increasingly costly offerings.

To mitigate this risk, policymakers could pair debt forgiveness with measures that directly address tuition inflation. One approach would be to tie federal funding for colleges to their commitment to capping tuition increases at or below the inflation rate. Another strategy could involve incentivizing institutions to adopt income-share agreements (ISAs), where students pay a percentage of their future income instead of fixed loan payments. Such models align institutional incentives with student success, potentially curbing the urge to raise costs arbitrarily.

A comparative analysis of countries with universal free education, like Germany or Norway, reveals that eliminating tuition fees altogether can stabilize education costs while ensuring accessibility. While such a model may not be politically feasible in the U.S., it underscores the importance of addressing the root causes of tuition inflation rather than merely treating its symptoms. Debt forgiveness, without structural reforms, risks becoming a temporary band-aid on a systemic issue.

In practical terms, individuals and families should remain vigilant about the long-term implications of borrowing for education. Even in a landscape of potential debt forgiveness, prioritizing affordability and value remains crucial. Prospective students should scrutinize program outcomes, graduation rates, and post-graduation employment data to ensure their investment aligns with future earnings potential. Additionally, exploring alternatives like community college transfers, apprenticeships, or online programs can provide cost-effective pathways to degrees. Ultimately, while debt forgiveness may offer relief, it is not a substitute for informed decision-making in navigating the education market.

Qualifying for VA Student Loan Forgiveness: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Alternatives to debt cancellation

Student debt forgiveness, while a popular solution, is not the only path to alleviating the burden of educational loans. Alternatives to outright cancellation focus on restructuring repayment plans, reducing interest rates, and expanding access to existing relief programs. These approaches aim to provide immediate and long-term financial relief without the sweeping economic implications of mass debt forgiveness.

One effective alternative is income-driven repayment (IDR) plans, which tie monthly payments to a borrower’s earnings. For example, the Pay As You Earn (PAYE) plan caps payments at 10% of discretionary income and forgives remaining debt after 20–25 years of consistent payments. Expanding eligibility for such plans and simplifying the application process could make them more accessible. For instance, automating enrollment for borrowers earning below a certain threshold—say, $40,000 annually—could reduce administrative barriers and ensure more individuals benefit.

Another strategy is refinancing options that allow borrowers to secure lower interest rates. Federal student loans often carry fixed rates, but private refinancing can offer variable rates as low as 2–4% for those with strong credit histories. However, this approach requires caution: refinancing federal loans into private ones eliminates access to IDR plans and forgiveness programs. A hybrid solution could involve government-backed refinancing programs that retain federal protections while lowering rates, ensuring borrowers aren’t forced to choose between affordability and flexibility.

Employer-sponsored repayment assistance programs (LRAPs) are also gaining traction. Companies like Aetna and Fidelity offer up to $2,000 annually to help employees pay down student debt. Expanding tax incentives for businesses that adopt such programs could encourage broader participation. For example, allowing employers to deduct up to $10,000 per employee annually for debt repayment contributions could make this benefit more appealing, benefiting both workers and companies.

Finally, strengthening public service loan forgiveness (PSLF) can provide targeted relief. Currently, PSLF forgives remaining debt after 10 years of qualifying payments for government or nonprofit employees. However, complex eligibility rules have left many applicants disqualified. Streamlining the process—such as by creating a single, standardized certification form—and retroactively applying reforms could ensure more borrowers receive the relief they were promised.

These alternatives address the student debt crisis without the polarizing debate surrounding mass cancellation. By focusing on accessibility, affordability, and targeted relief, they offer practical solutions that can be implemented incrementally, providing immediate benefits while avoiding broader economic disruptions.

Unlock Student Loan Forgiveness: A Step-by-Step Application Guide

You may want to see also

Frequently asked questions

Yes, student debt forgiveness is a real possibility, though it depends on government policies, legislative actions, and eligibility criteria. Programs like Public Service Loan Forgiveness (PSLF) and income-driven repayment plans already exist, and broader forgiveness initiatives have been proposed or implemented in certain cases.

Qualification varies by program. For example, PSLF requires 10 years of qualifying payments while working full-time for a government or nonprofit organization. Income-driven repayment plans may offer forgiveness after 20–25 years of payments. Broad forgiveness initiatives, if enacted, could have specific income or debt thresholds.

Generally, student debt forgiveness does not negatively impact your credit score. In fact, it can improve your financial situation by reducing your debt burden. However, any missed payments or defaults before forgiveness is granted could still harm your credit. Always check the terms of the forgiveness program for specifics.