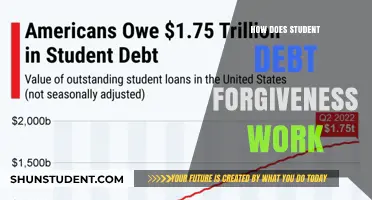

Student loan forgiveness has become a hotly debated topic in recent years, with many borrowers seeking relief from the crushing burden of educational debt. While various programs and proposals have been introduced, such as Public Service Loan Forgiveness (PSLF) and income-driven repayment plans, skepticism remains about their effectiveness and accessibility. The Biden administration’s efforts to implement broader forgiveness initiatives have faced legal challenges and political opposition, leaving many to wonder if meaningful relief is truly attainable. As millions of Americans continue to struggle with student loans, the question persists: Is student loan forgiveness for real, or just an elusive promise?

| Characteristics | Values |

|---|---|

| Is Student Loan Forgiveness Real? | Yes, but with specific conditions and eligibility requirements. |

| Types of Forgiveness Programs | Public Service Loan Forgiveness (PSLF), Teacher Loan Forgiveness, Income-Driven Repayment (IDR) Forgiveness, Perkins Loan Cancellation, and others. |

| Eligibility Requirements | Varies by program; common criteria include employment in public service, teaching in low-income schools, or making qualifying payments under IDR plans. |

| Current Status (as of 2023) | Active, with ongoing updates and temporary waivers (e.g., PSLF Limited Waiver expired Oct 31, 2022, but IDR adjustments continue). |

| Recent Developments | Biden administration's targeted loan cancellations (e.g., $10,000-$20,000 for eligible borrowers) and legal challenges to these initiatives. |

| Tax Implications | Forgiveness may be tax-free for certain programs (e.g., PSLF, IDR) but taxable for others (check IRS guidelines). |

| Application Process | Requires submission of forms (e.g., PSLF Form, IDR recertification) and documentation of eligibility. |

| Common Misconceptions | Not automatic; borrowers must actively apply and meet criteria. Not all loans or borrowers qualify. |

| Scams to Avoid | Beware of companies charging fees for "loan forgiveness" services; legitimate programs are free through official channels. |

| Resources for Verification | Federal Student Aid website (studentaid.gov), loan servicers, and official government announcements. |

Explore related products

What You'll Learn

![]()

Eligibility criteria for loan forgiveness programs

Student loan forgiveness programs are real, but they’re not a one-size-fits-all solution. Eligibility criteria vary widely depending on the program, and understanding these requirements is crucial for anyone hoping to benefit. For instance, the Public Service Loan Forgiveness (PSLF) program requires 120 qualifying payments while working full-time for a government or nonprofit organization. This isn’t just about paying your loans—it’s about committing to a specific career path for nearly a decade. Similarly, income-driven repayment (IDR) plans like PAYE or REPAYE offer forgiveness after 20–25 years of payments, but only if your income remains below certain thresholds. These programs aren’t automatic; borrowers must actively enroll and recertify their income annually to stay eligible.

To qualify for most forgiveness programs, your loans must meet specific criteria. Federal Direct Loans are typically eligible, but older FFEL or Perkins Loans may require consolidation into a Direct Loan first. This step is often overlooked, leading to years of ineligible payments. For example, a teacher pursuing Teacher Loan Forgiveness must have Direct Subsidized or Unsubsidized Loans, not FFEL Loans, to qualify for up to $17,500 in forgiveness after five consecutive years in a low-income school. Similarly, borrowers in the military or healthcare fields may access programs like the Army Loan Repayment Program or the National Health Service Corps Loan Repayment Program, but these require service commitments in underserved areas. Always verify your loan type and program compatibility before assuming eligibility.

Income plays a pivotal role in many forgiveness programs, particularly IDR plans. These plans cap monthly payments at a percentage of your discretionary income, with forgiveness kicking in after 20–25 years. However, if your income rises significantly, your payments could increase, delaying forgiveness. For instance, a borrower earning $40,000 annually with $100,000 in debt might pay just $150 monthly under REPAYE, but if their income doubles, payments could jump to $600. Additionally, forgiven amounts under IDR plans may be taxed as income, potentially resulting in a hefty bill. Borrowers should weigh these factors and consider consulting a tax professional to plan ahead.

Finally, documentation and compliance are non-negotiable. PSLF applicants, for example, must submit an Employment Certification Form annually and a final application after 120 payments. Missing these steps can disqualify years of effort. Similarly, IDR borrowers must recertify their income and family size each year to avoid being kicked out of the program. Keep meticulous records of payments, employer certifications, and correspondence with loan servicers. Proactive management of these details can mean the difference between full forgiveness and starting from square one.

In summary, eligibility for loan forgiveness programs hinges on specific loan types, career choices, income levels, and administrative diligence. While these programs are real and can provide significant relief, they require careful planning and adherence to strict criteria. Borrowers should research their options thoroughly, stay organized, and seek guidance when needed to maximize their chances of success.

Biden's Student Loan Forgiveness Plan: What's Passed and What's Next?

You may want to see also

Explore related products

![]()

Types of student loan forgiveness plans available

Student loan forgiveness is a real and viable option for many borrowers, but the landscape is complex and varies widely depending on factors like employment, loan type, and repayment history. Understanding the specific plans available is crucial for determining eligibility and maximizing benefits. Here’s a breakdown of the primary types of student loan forgiveness programs, each tailored to different circumstances.

Public Service Loan Forgiveness (PSLF) stands out as one of the most well-known programs. Designed for borrowers working full-time in qualifying public service jobs—such as government, education, or nonprofit roles—PSLF offers tax-free forgiveness of the remaining loan balance after 120 eligible payments. A critical detail: only federal Direct Loans qualify, and payments must be made under an income-driven repayment plan. For example, a teacher in a low-income school district could see their balance forgiven after 10 years of consistent payments, provided all criteria are met. The key takeaway? Documentation is paramount; borrowers must submit an Employment Certification Form periodically to ensure payments count toward forgiveness.

Teacher Loan Forgiveness targets educators specifically, offering up to $17,500 in forgiveness for those teaching full-time for five consecutive years in low-income schools. Eligibility is limited to Federal Direct and FFEL loans, and not all teaching positions qualify—only math, science, or special education teachers in secondary schools, or any teacher in an elementary school, are eligible for the maximum amount. A cautionary note: this program cannot be combined with PSLF, so educators must choose the plan that best aligns with their long-term career path.

Income-Driven Repayment (IDR) Forgiveness provides a safety net for borrowers with high debt relative to their income. Plans like Income-Based Repayment (IBR), Pay As You Earn (PAYE), and Revised Pay As You Earn (REPAYE) cap monthly payments at a percentage of discretionary income and offer forgiveness after 20–25 years of payments. For instance, a borrower earning $40,000 annually with $100,000 in loans might pay as little as 10–15% of their discretionary income monthly, with the remaining balance forgiven after 25 years. However, the forgiven amount may be taxed as income, so planning for this financial event is essential.

Loan Forgiveness for Healthcare Professionals includes programs like the National Health Service Corps (NHSC) Loan Repayment Program and Nurse Corps Loan Repayment Program. These initiatives offer substantial forgiveness—up to $50,000 or more—in exchange for a service commitment in underserved areas. For example, a primary care physician working two years in a Health Professional Shortage Area (HPSA) could receive $50,000 in loan repayment through the NHSC program. These programs are highly competitive and require a demonstrated commitment to serving vulnerable populations.

In summary, student loan forgiveness is real, but it’s not automatic. Borrowers must proactively research, enroll in the correct programs, and meet stringent requirements. Whether through public service, teaching, income-driven plans, or healthcare commitments, each forgiveness pathway demands careful planning and adherence to specific rules. The reward? Substantial debt relief for those who qualify.

Public Service Loan Forgiveness: Easing Student Debt Burden for Borrowers

You may want to see also

Explore related products

![]()

Income-driven repayment plan benefits and forgiveness

Student loan forgiveness isn’t a myth, but it’s also not a universal solution. For many borrowers, income-driven repayment (IDR) plans serve as a bridge to eventual forgiveness, offering immediate relief by capping monthly payments at a percentage of discretionary income. These plans—such as Pay As You Earn (PAYE), Revised Pay As You Earn (REPAYE), Income-Based Repayment (IBR), and Income-Contingent Repayment (ICR)—adjust based on earnings, making them ideal for low-to-moderate-income borrowers. For instance, REPAYE limits payments to 10% of discretionary income and offers forgiveness after 20–25 years, depending on loan type. However, the trade-off is that prolonged repayment can accrue interest, potentially increasing the total amount forgiven.

Consider a borrower earning $40,000 annually with $60,000 in federal loans. Under REPAYE, their monthly payment would be roughly $130 (10% of discretionary income), compared to $690 under the Standard 10-Year Plan. While the lower payment provides breathing room, the remaining balance after 240 payments (20 years) could grow due to unpaid interest. For example, if the original interest rate is 6%, the forgiven amount after 20 years might exceed $40,000. This forgiven debt may be taxable as income, though the American Rescue Act of 2021 temporarily exempts forgiveness through 2025. Borrowers must weigh the benefits of manageable payments against potential tax liabilities.

IDR plans aren’t without pitfalls. Enrollment requires annual recertification of income and family size, a step often overlooked, leading to payment increases or plan termination. Additionally, certain plans like IBR calculate payments based on 15% of discretionary income for new borrowers, a higher rate than REPAYE’s 10%. Borrowers must also navigate the complexities of loan types: only Direct Loans qualify for REPAYE and PAYE, while FFEL or Perkins Loans may require consolidation first. Missteps in paperwork or eligibility can delay forgiveness timelines, underscoring the need for meticulous record-keeping and proactive communication with loan servicers.

Despite challenges, IDR plans offer a structured path to forgiveness for those who qualify. Public Service Loan Forgiveness (PSLF), for instance, forgives remaining balances after 120 qualifying payments for borrowers working in government or nonprofit roles. Combining PSLF with an IDR plan can minimize payments while maximizing forgiveness potential. For example, a teacher earning $50,000 annually with $80,000 in loans could pay as little as $250 monthly under REPAYE, achieving PSLF in 10 years without accruing significant interest. Such strategic planning transforms forgiveness from a distant possibility into a tangible goal.

In practice, success with IDR plans hinges on understanding their mechanics and staying disciplined. Borrowers should use tools like the Federal Student Aid Loan Simulator to estimate payments and forgiveness timelines. Automating recertification reminders and maintaining consistent employment (for PSLF seekers) are critical. While IDR plans don’t eliminate debt overnight, they provide a realistic framework for managing loans and achieving forgiveness, proving that, yes, student loan forgiveness is real—for those who play by the rules.

Forgiving Student Loans: Economic Boost or Burden? A Comprehensive Analysis

You may want to see also

Explore related products

![]()

Public Service Loan Forgiveness (PSLF) requirements

Student loan forgiveness is a real possibility for many borrowers, but the path to achieving it can be complex and fraught with pitfalls. Among the various forgiveness programs, Public Service Loan Forgiveness (PSLF) stands out as a viable option for those committed to a career in public service. To qualify, borrowers must meet specific requirements that go beyond simply working in the public sector. Understanding these requirements is crucial to ensuring eligibility and maximizing the benefits of the program.

First and foremost, borrowers must make 120 qualifying payments while working full-time for a qualifying employer. These payments must be made under an income-driven repayment plan, such as Income-Based Repayment (IBR), Pay As You Earn (PAYE), or Revised Pay As You Earn (REPAYE). It’s essential to note that only payments made after October 1, 2007, count toward the 120-payment requirement. Additionally, payments must be made on time and in full to qualify. For example, a borrower working as a public school teacher under the REPAYE plan would need to ensure each monthly payment is submitted by the due date to maintain eligibility.

Qualifying employment is another critical aspect of PSLF. Eligible employers include government organizations at any level (federal, state, local, or tribal), 501(c)(3) nonprofit organizations, and some other types of nonprofits that provide qualifying public services. For instance, a social worker employed by a 501(c)(3) organization dedicated to combating homelessness would meet the employment criteria. However, working for a for-profit company, even in a public service role, does not qualify. Borrowers should use the PSLF Help Tool provided by the U.S. Department of Education to confirm their employer’s eligibility and submit the Employer Certification Form annually to track their progress.

One common pitfall borrowers face is having the wrong type of federal loan. Only Direct Loans are eligible for PSLF. If a borrower has Federal Family Education Loans (FFEL) or Perkins Loans, they must consolidate them into a Direct Consolidation Loan to qualify. For example, a nurse with FFEL loans would need to consolidate them before starting the PSLF process. Failure to do so could result in years of payments not counting toward forgiveness.

Finally, persistence and attention to detail are key. The PSLF program has been criticized for its complexity and low approval rates, often due to administrative errors or misunderstandings of the requirements. Borrowers should keep detailed records of their payments, employment certifications, and correspondence with their loan servicer. Regularly submitting the Employer Certification Form and applying for forgiveness as soon as the 120-payment threshold is met can help avoid complications. While the PSLF requirements are stringent, they offer a clear pathway to debt relief for those who carefully navigate the process.

Kansas Student Loan Forgiveness: 25-Year Rule Explained

You may want to see also

Explore related products

![]()

Potential tax implications of loan forgiveness

Student loan forgiveness can feel like a financial lifeline, but it’s not without strings attached. One often overlooked tether is the taxman. In the U.S., forgiven debt is generally treated as taxable income by the IRS, meaning you could owe taxes on the amount forgiven. For example, if $20,000 of your student loans is forgiven, that $20,000 could be added to your taxable income for the year, potentially bumping you into a higher tax bracket. This is a critical consideration for anyone banking on forgiveness programs like Public Service Loan Forgiveness (PSLF) or income-driven repayment plans.

However, exceptions exist. The American Rescue Plan Act of 2021 temporarily exempts student loan forgiveness from federal taxation through 2025, a reprieve for borrowers. But this exemption doesn’t apply to all states. Some, like California and Virginia, have aligned their tax codes with federal law, while others, like Massachusetts and New York, may still tax forgiven amounts. Borrowers must check their state’s tax laws to avoid unexpected liabilities. This patchwork of rules underscores the importance of staying informed about both federal and state regulations.

Another layer of complexity arises with employer-provided student loan assistance programs. Some employers offer to pay down employees’ student loans as a benefit. While these payments are generally taxable as income, the Consolidated Appropriations Act of 2021 allows employers to contribute up to $5,250 annually tax-free through 2025. This benefit, however, doesn’t extend to forgiven loans outside these programs. Borrowers should clarify with their employers how such contributions are structured to plan accordingly.

For those nearing retirement, the tax implications of loan forgiveness can be particularly thorny. Forgiven debt could increase your taxable income, potentially affecting Social Security benefits or Medicare premiums, which are tied to income thresholds. Retirees or those on fixed incomes should consult a tax professional to strategize timing and minimize financial strain. Proactive planning can mitigate the impact of a sudden increase in taxable income.

In short, while student loan forgiveness can provide relief, it’s not a free pass. Borrowers must navigate a maze of federal and state tax rules, employer program nuances, and long-term financial consequences. Staying informed and seeking professional advice can turn a potential tax trap into a manageable step toward financial freedom. Ignoring these implications could turn a windfall into a financial headache.

Biden's Student Loan Forgiveness Plan: What Borrowers Need to Know

You may want to see also

Frequently asked questions

Yes, student loan forgiveness is real and exists through various federal programs, such as Public Service Loan Forgiveness (PSLF), Teacher Loan Forgiveness, and income-driven repayment (IDR) plans.

Qualification depends on the program. For example, PSLF requires 10 years of qualifying payments while working full-time for a government or nonprofit organization. IDR plans forgive remaining balances after 20–25 years of payments.

No, federal student loan forgiveness programs only apply to federal student loans. Private loans are not eligible unless specifically stated by the lender.

It depends. PSLF and Teacher Loan Forgiveness are typically tax-free, but forgiveness through IDR plans may be taxable unless you qualify for an exclusion under the American Rescue Plan Act (through 2025).

Yes, beware of scams promising immediate forgiveness for a fee. Legitimate forgiveness programs are free to apply for through official government channels like the U.S. Department of Education.