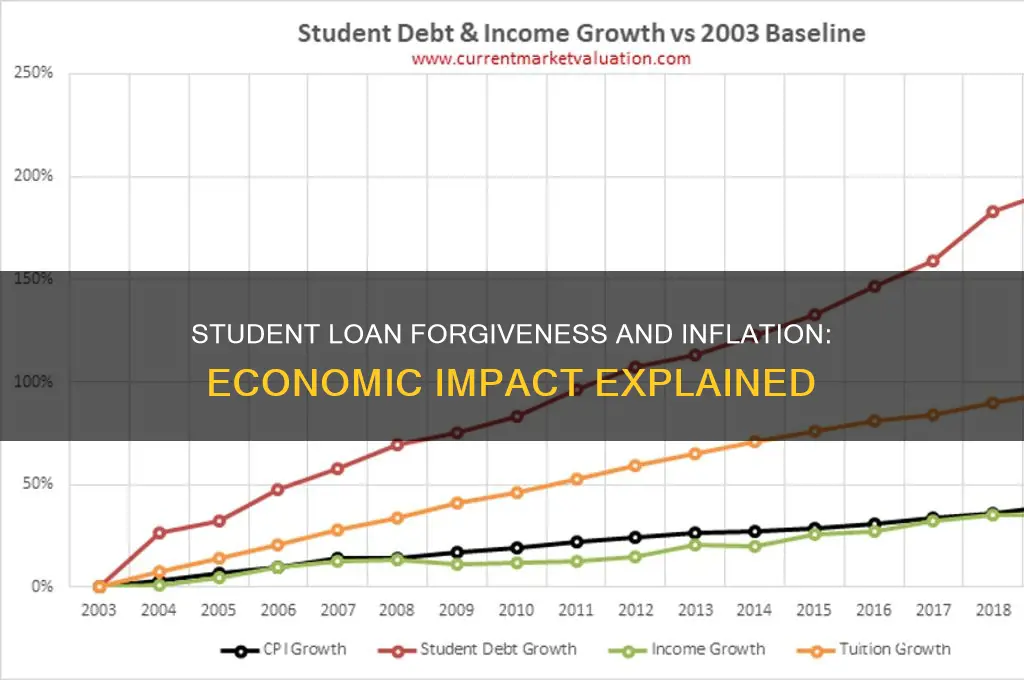

The debate surrounding student loan forgiveness has intensified, with critics arguing that widespread cancellation could exacerbate inflation. Proponents of forgiveness claim it would alleviate financial burdens on millions of borrowers, stimulating the economy through increased consumer spending. However, opponents warn that injecting such a large sum of money into the economy could drive up demand without a corresponding increase in supply, leading to higher prices. This concern is particularly acute in an already inflationary environment, where rising costs of goods and services have strained households nationwide. As policymakers weigh the benefits of debt relief against potential economic repercussions, the question remains: could student loan forgiveness unintentionally fuel inflation, or will its economic benefits outweigh the risks?

| Characteristics | Values |

|---|---|

| Direct Impact on Inflation | Limited. Most analyses suggest student loan forgiveness would have a modest impact on inflation, potentially adding 0.1-0.3 percentage points to inflation over a few years. |

| Mechanism of Impact | Increased disposable income for borrowers could lead to higher consumer spending, potentially driving up demand and prices. |

| Offsetting Factors | Phased implementation of forgiveness could mitigate inflationary effects. Borrowers may use funds to pay down other debts or save, reducing immediate spending impact. |

| Economic Context | Current inflation is driven by factors like supply chain disruptions and energy prices, not primarily by student loan debt. |

| Long-Term Effects | Potential for increased economic growth and productivity due to reduced debt burden, which could offset inflationary pressures over time. |

| Political Debate | Highly contentious issue with arguments both for and against forgiveness based on its potential inflationary impact. |

| Recent Data (as of October 2023) | Specific inflationary impact remains uncertain, with estimates varying widely depending on the scope and implementation of forgiveness programs. |

Explore related products

What You'll Learn

![]()

Impact on Consumer Spending

Student loan forgiveness can act as a financial stimulus, freeing up disposable income for millions of borrowers. When monthly loan payments are eliminated or reduced, households gain immediate access to funds previously allocated to debt servicing. For example, if a borrower saves $300 per month from loan forgiveness, that amount could be redirected toward consumer spending. This influx of available cash is particularly impactful for younger demographics, aged 25 to 34, who often have limited savings and higher debt burdens. Economists estimate that widespread forgiveness could inject billions into the economy annually, as borrowers shift from debt repayment to discretionary purchases.

However, the relationship between loan forgiveness and consumer spending is not uniform across all borrowers. Those with higher incomes or substantial savings may choose to invest the freed-up funds or pay down other debts rather than increase spending. Conversely, lower-income borrowers, who often live paycheck to paycheck, are more likely to allocate the savings toward immediate needs like groceries, utilities, or retail purchases. For instance, a borrower earning $40,000 annually might spend an additional $200 monthly on essentials, while a higher-earning counterpart might save or invest the same amount. This disparity highlights the importance of considering income levels when predicting the economic impact of loan forgiveness.

Critics argue that increased consumer spending from loan forgiveness could exacerbate inflationary pressures, particularly in sectors like housing, education, and healthcare. If demand surges without a corresponding increase in supply, prices may rise, offsetting the benefits of debt relief. For example, if forgiven borrowers enter the housing market en masse, home prices and rents could climb, eroding the financial gains from loan forgiveness. Policymakers must weigh these risks against the potential economic boost, possibly pairing forgiveness programs with measures to stabilize prices, such as increasing housing supply or capping interest rates.

To maximize the positive impact on consumer spending without fueling inflation, targeted forgiveness programs could be designed with specific eligibility criteria. For instance, capping forgiveness at $10,000 for borrowers earning below $75,000 annually would direct relief to those most likely to spend the funds immediately. Additionally, phasing in forgiveness over time, rather than providing lump-sum relief, could prevent sudden spikes in demand. Borrowers could receive $100 in monthly reductions over 10 years, allowing for gradual economic adjustment. Such strategies ensure that loan forgiveness stimulates spending without overwhelming markets or driving up prices.

Ultimately, the impact of student loan forgiveness on consumer spending depends on how borrowers allocate their savings and the broader economic context. Practical steps for borrowers include creating a budget to determine how much of the savings can be spent versus saved, prioritizing high-impact purchases like home repairs or education, and avoiding unnecessary debt accumulation. For policymakers, balancing debt relief with inflation control requires careful design and monitoring. By focusing on targeted, phased relief, both borrowers and the economy can reap the benefits of loan forgiveness without unintended consequences.

Can Private Student Loans Be Forgiven? Exploring Your Options

You may want to see also

Explore related products

![]()

Effect on Interest Rates

Student loan forgiveness, while a relief for borrowers, introduces a complex dynamic into the economy, particularly concerning interest rates. The immediate injection of disposable income into the hands of millions could stimulate consumer spending, a key driver of economic growth. However, this increased demand for goods and services might outpace supply, leading to upward pressure on prices. Central banks, tasked with maintaining price stability, often respond to inflationary pressures by raising interest rates. This mechanism, designed to cool down an overheating economy, could inadvertently make borrowing more expensive for everyone, not just those with student loans.

Consider the Federal Reserve’s dual mandate: maximum employment and stable prices. If student loan forgiveness significantly boosts consumer spending, it could accelerate inflation, prompting the Fed to hike interest rates more aggressively. For instance, if borrowers collectively redirect $100 billion annually from loan payments to consumption, this could amplify inflationary trends, especially in sectors like housing, education, and healthcare. Higher interest rates would then ripple through the economy, affecting mortgage rates, auto loans, and credit card debt, potentially offsetting some of the financial relief intended by the forgiveness program.

From a comparative perspective, the impact of student loan forgiveness on interest rates can be likened to the effects of fiscal stimulus during economic recoveries. Both inject liquidity into the economy, but the former targets a specific demographic—young and middle-aged adults—who are more likely to spend rather than save. This demographic focus could amplify the inflationary impact, as these individuals are often in the market for big-ticket items like homes and cars. In contrast, broader stimulus measures, such as tax cuts, may have a more dispersed effect, mitigating the risk of concentrated inflationary pressures.

To mitigate the risk of rising interest rates, policymakers could pair student loan forgiveness with measures to increase supply. For example, investing in affordable housing, expanding healthcare capacity, and incentivizing domestic manufacturing could help balance demand and supply, easing inflationary pressures. Borrowers, too, can take proactive steps. Instead of immediately increasing spending, they could allocate a portion of their savings to paying down high-interest debt or building emergency funds. This approach not only enhances financial stability but also reduces the likelihood of contributing to inflationary trends that could trigger higher interest rates.

Ultimately, the effect of student loan forgiveness on interest rates hinges on the interplay between increased consumer spending and the economy’s capacity to absorb that demand. While the relief is undoubtedly beneficial for individual borrowers, its macroeconomic implications require careful management. By understanding these dynamics, both policymakers and individuals can navigate the potential trade-offs, ensuring that the benefits of loan forgiveness are maximized without exacerbating inflation or interest rate hikes.

Therapists as Public Health Workers: Qualifying for Student Loan Forgiveness

You may want to see also

Explore related products

$20.99

![]()

Wage Growth vs. Debt Relief

The debate over student loan forgiveness often hinges on its potential to fuel inflation, but a critical aspect of this discussion is the interplay between wage growth and debt relief. If wages stagnate while debt is forgiven, the additional disposable income could indeed drive up demand for goods and services, potentially leading to inflationary pressures. However, if wage growth outpaces debt relief, the economic impact might be more balanced, as increased earnings could offset the stimulative effects of forgiveness. This dynamic underscores the importance of considering labor market trends alongside debt relief policies.

To illustrate, consider a scenario where student loan forgiveness injects $10,000 annually into a borrower’s budget. If their wages remain flat at $50,000 per year, this extra income could significantly boost their spending power, potentially driving up prices in sectors like housing or consumer goods. Conversely, if their wages grow by 5% annually, the relative impact of the $10,000 relief diminishes, as their overall income increases by $2,500. In this case, the inflationary risk is mitigated by the alignment of wage growth with debt relief. Policymakers must therefore pair forgiveness programs with initiatives to strengthen wage growth, such as investments in workforce development or minimum wage adjustments.

A comparative analysis reveals that countries with robust wage growth, like Germany or Australia, have implemented debt relief programs with minimal inflationary consequences. For instance, Australia’s Higher Education Loan Program (HELP) combines income-contingent repayment with strong wage growth, ensuring borrowers can manage debt without relying on forgiveness. In contrast, economies with stagnant wages, such as parts of the U.S., face greater inflation risks when implementing broad debt relief. This suggests that wage growth acts as a buffer against inflation, making it a critical factor in designing effective debt relief policies.

From a practical standpoint, individuals can mitigate the inflationary impact of debt relief by prioritizing savings or investments over increased consumption. For example, a borrower receiving $200 monthly from loan forgiveness could allocate $100 to an emergency fund and $100 to paying down high-interest debt, rather than spending it on discretionary items. Similarly, employers can play a role by offering wage increases or bonuses tied to productivity, ensuring that debt relief complements rather than distorts economic stability. Such strategies demonstrate that the inflationary risks of debt relief are not inevitable but depend on how individuals and institutions respond.

In conclusion, the relationship between wage growth and debt relief is pivotal in determining whether student loan forgiveness contributes to inflation. By fostering wage growth, implementing targeted relief, and encouraging responsible financial behavior, policymakers and individuals can navigate this complex issue effectively. Ignoring this interplay risks exacerbating inflation, but addressing it holistically offers a path to economic resilience.

Will Consolidated Student Loans Be Forgiven? Exploring Potential Debt Relief Options

You may want to see also

Explore related products

![]()

Housing Market Influence

The housing market, a cornerstone of the economy, is intricately linked to consumer spending power. Student loan forgiveness, by injecting disposable income into the hands of millions, could act as a stimulant for this sector. Consider the average borrower: with monthly payments averaging $200 to $300, forgiveness frees up funds that might otherwise be allocated to debt servicing. This surplus could directly translate into higher demand for housing, as individuals and families gain the financial flexibility to pursue homeownership or upgrade their living situations. However, the impact isn’t uniform; regional disparities in housing affordability and borrower demographics will dictate where and how this demand materializes.

To understand the potential ripple effects, examine the mechanics of housing affordability. A key metric is the debt-to-income ratio, which lenders use to assess mortgage eligibility. Student loan forgiveness improves this ratio, making borrowers more attractive candidates for home loans. For instance, a borrower with $30,000 in forgiven debt could see their monthly obligations drop by $300, potentially qualifying them for a mortgage they previously couldn’t afford. This shift could drive up demand in entry-level housing markets, particularly in suburban or exurban areas where prices are more accessible. However, caution is warranted: if demand outstrips supply, prices could rise, exacerbating affordability issues for non-borrowers.

Critics argue that this increased demand could contribute to inflationary pressures in the housing market. As more buyers enter the fray, competition for limited inventory intensifies, driving up prices. Historical precedents, such as the post-2008 housing recovery, show that stimulus-driven demand can lead to rapid price appreciation. To mitigate this risk, policymakers could pair forgiveness programs with initiatives to increase housing supply, such as incentivizing new construction or easing zoning restrictions. Without such measures, the benefits of forgiveness may be offset by higher housing costs, particularly for first-time buyers.

A comparative analysis reveals that the housing market’s response to student loan forgiveness depends on broader economic conditions. In a high-interest-rate environment, for example, the impact of increased demand might be muted, as higher mortgage rates dampen purchasing power. Conversely, in a low-rate scenario, the effect could be amplified, potentially leading to overheating. Borrowers aged 25–34, who represent the largest demographic of student loan holders, are also prime first-time homebuyers. Targeted financial education programs could help this group navigate the housing market responsibly, ensuring that newfound disposable income is allocated wisely rather than fueling speculative bubbles.

In conclusion, student loan forgiveness has the potential to reshape the housing market by boosting demand and improving borrower eligibility. However, its inflationary impact hinges on supply dynamics, interest rates, and policy interventions. For individuals, the takeaway is clear: assess your financial situation post-forgiveness, prioritize savings or debt reduction, and approach homeownership with a long-term perspective. For policymakers, the challenge is to balance stimulus with stability, ensuring that forgiveness benefits borrowers without destabilizing the housing market.

Understanding the Reasons Behind Recent Student Loan Forgiveness Programs

You may want to see also

Explore related products

![]()

Long-term Economic Consequences

Student loan forgiveness, while offering immediate relief to borrowers, can have nuanced long-term economic consequences that ripple through the broader economy. One of the primary concerns is its potential to exacerbate inflationary pressures. When large-scale debt forgiveness injects additional disposable income into the economy, it can increase consumer spending. While this might stimulate growth in the short term, it also risks driving up demand for goods and services faster than supply can adjust, leading to higher prices. For instance, if forgiven loans free up $100 billion in annual consumer spending, sectors like housing, education, and healthcare could face upward price pressures, particularly if they are already supply-constrained.

Analyzing historical precedents provides insight into this dynamic. The 2009 Cash for Clunkers program, which aimed to stimulate the auto industry, temporarily boosted sales but also led to higher used car prices due to reduced supply. Similarly, student loan forgiveness could create a surge in spending that outpaces productivity gains, embedding inflationary expectations into the economy. This is especially risky in sectors with inelastic supply, such as housing, where increased demand from debt-free individuals could push prices higher without a corresponding increase in available homes.

However, the inflationary impact isn’t inevitable and depends on policy design. Targeted forgiveness programs, such as those limited to low-income borrowers or specific professions, could mitigate macroeconomic risks by distributing relief more gradually. For example, capping forgiveness at $20,000 per borrower or phasing it in over several years would reduce the immediate shock to the economy. Policymakers could also pair forgiveness with fiscal measures to curb inflation, such as increasing taxes on higher income brackets or investing in supply-side initiatives like affordable housing construction.

A comparative analysis of student loan forgiveness versus other economic interventions reveals trade-offs. Unlike infrastructure spending, which directly expands productive capacity, debt forgiveness primarily shifts purchasing power without addressing underlying supply constraints. This makes it more prone to inflationary effects, particularly in an economy already near full employment. For instance, if 10 million borrowers receive $10,000 in forgiveness, the $100 billion in newfound spending could outstrip the economy’s ability to produce additional goods and services, especially in labor-intensive sectors.

In conclusion, while student loan forgiveness can alleviate financial burdens and stimulate economic activity, its long-term consequences require careful management. Policymakers must balance the benefits of debt relief with the risk of inflation by designing targeted, phased programs and complementing them with supply-side policies. Without such safeguards, the unintended consequence could be an economy where higher prices erode the very gains intended for borrowers, underscoring the delicate interplay between fiscal policy and macroeconomic stability.

Understanding Student Loan Forgiveness Hardship Criteria and Eligibility Requirements

You may want to see also

Frequently asked questions

Student loan forgiveness could contribute to inflation if it increases consumer spending significantly, as borrowers may have more disposable income. However, its impact depends on the scale of the program and broader economic conditions.

Student loan forgiveness can stimulate the economy by freeing up income for other spending or saving, but it may also increase demand for goods and services, potentially driving up prices and contributing to inflation if not balanced by other economic measures.

Student loan forgiveness may be less inflationary than direct stimulus checks or tax cuts because it targets a specific group and spreads its economic impact over time. However, its inflationary effects still depend on the overall economic context.

Yes, student loan forgiveness can be structured to minimize inflation by targeting lower-income borrowers, capping forgiveness amounts, or phasing it in gradually to avoid a sudden surge in consumer spending.