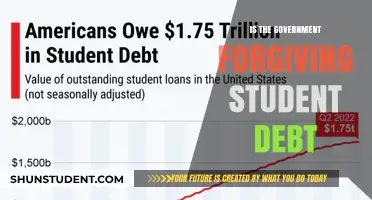

The topic of student loan forgiveness has become a pressing issue for millions of borrowers in the United States, as many struggle with the burden of mounting debt. With the cost of higher education continuing to rise, borrowers are increasingly looking to the government for relief. The question of whether the government is offering student loan forgiveness has gained significant attention, particularly in light of recent policy proposals and executive actions. While some targeted forgiveness programs have been implemented, such as those for public service workers and borrowers defrauded by predatory institutions, a broader, comprehensive solution remains elusive. As a result, borrowers, advocates, and policymakers are engaged in ongoing debates about the feasibility, scope, and potential impact of widespread student loan forgiveness.

| Characteristics | Values |

|---|---|

| Current Federal Programs | Public Service Loan Forgiveness (PSLF), Income-Driven Repayment (IDR) Forgiveness, Teacher Loan Forgiveness, Perkins Loan Cancellation, Borrower Defense to Repayment, Total and Permanent Disability Discharge |

| Eligibility Requirements | Varies by program (e.g., employment in public service, specific repayment plans, teaching in low-income schools, proof of school misconduct, total disability) |

| Loan Types Covered | Federal Direct Loans (for most programs), FFEL and Perkins Loans (limited programs) |

| Forgiveness Amount | Full or partial forgiveness depending on the program and eligibility |

| Tax Implications | Forgiveness may be tax-free under certain programs (e.g., PSLF, IDR, disability discharge) or taxable (e.g., Borrower Defense) |

| Application Process | Requires submission of specific forms (e.g., PSLF form, IDR forgiveness application, disability discharge application) |

| Recent Updates (as of 2023) | One-time IDR account adjustment (2023), temporary PSLF waiver (ended Oct. 31, 2023), ongoing litigation affecting Borrower Defense claims |

| Biden Administration Initiatives | Limited one-time student debt cancellation (blocked by Supreme Court in 2023), focus on improving existing programs (e.g., IDR, PSLF) |

| State-Level Programs | Some states offer loan repayment assistance programs (LRAPs) for specific professions (e.g., healthcare, law, education) |

| Private Loan Forgiveness | No federal forgiveness for private loans; some employers or state programs may offer repayment assistance |

| Scams and Warnings | Beware of companies charging fees for "student loan forgiveness" services; use official government resources (e.g., studentaid.gov) |

Explore related products

What You'll Learn

![]()

Eligibility criteria for student loan forgiveness programs

Student loan forgiveness programs are not one-size-fits-all. Eligibility criteria vary widely depending on the program, but certain common threads emerge. Generally, these programs target borrowers who work in public service, teach in low-income schools, or face financial hardship. For instance, the Public Service Loan Forgiveness (PSLF) program requires 120 qualifying payments while working full-time for a government or nonprofit organization. Similarly, the Teacher Loan Forgiveness program offers up to $17,500 in forgiveness for educators who teach for five consecutive years in low-income schools. Understanding these specific requirements is the first step to determining if you qualify.

Beyond profession-based programs, income-driven repayment (IDR) plans offer a pathway to forgiveness after 20–25 years of payments, depending on the plan. These plans cap monthly payments at a percentage of your discretionary income, making them ideal for borrowers with high debt relative to their earnings. For example, the Revised Pay As You Earn (REPAYE) plan sets payments at 10% of discretionary income and forgives remaining balances after 20 years for undergraduate loans and 25 years for graduate loans. However, borrowers should be aware that forgiven amounts may be taxed as income, unless they qualify for exceptions like PSLF.

Not all loans qualify for forgiveness programs. Federal Direct Loans are typically eligible, while Federal Family Education Loans (FFEL) and Perkins Loans may require consolidation into a Direct Consolidation Loan to qualify. Private student loans are generally excluded from government forgiveness programs, though some states and employers offer assistance. For instance, the New York State Young Farmers Loan Forgiveness Incentive Program forgives up to $10,000 annually for farmers under 62 with eligible loans. Always verify your loan type and program compatibility before applying.

Finally, maintaining eligibility requires vigilance. For PSLF, borrowers must submit an Employment Certification Form annually and apply for forgiveness after 120 qualifying payments. Missing payments or switching to a non-qualifying employer can reset the clock. Similarly, IDR plan participants must recertify their income and family size annually to avoid payment increases or loss of eligibility. Proactive management of your loans and adherence to program rules are critical to securing forgiveness.

In summary, eligibility for student loan forgiveness hinges on specific criteria tied to profession, loan type, repayment plan, and consistent compliance. By understanding these requirements and taking deliberate steps to meet them, borrowers can navigate the complexities of these programs and work toward a debt-free future.

Unraveling the Truth About Student Loan Forgiveness: Fact or Fiction?

You may want to see also

Explore related products

![]()

Income-driven repayment plans and loan forgiveness options

Income-driven repayment (IDR) plans are a lifeline for borrowers struggling to manage federal student loan payments. These plans cap monthly payments at a percentage of discretionary income, typically ranging from 10% to 20%, depending on the plan. For instance, the Revised Pay As You Earn (REPAYE) plan sets payments at 10% of discretionary income for all borrowers, while the Income-Based Repayment (IBR) plan adjusts this rate based on when the loan was first disbursed. These plans not only make payments more manageable but also offer a pathway to loan forgiveness after 20 or 25 years of qualifying payments, depending on the plan and borrower type.

Consider the case of a borrower earning $40,000 annually with $50,000 in student loans. Under the REPAYE plan, their discretionary income would be calculated as the difference between their income and 150% of the federal poverty guideline for their family size. For a single borrower, this would result in a monthly payment of approximately $150, significantly lower than the standard 10-year repayment plan’s $500 monthly payment. Over time, this reduced payment structure, combined with the possibility of forgiveness, can provide substantial financial relief.

However, enrolling in an IDR plan requires annual recertification of income and family size, a step borrowers must not overlook. Failure to recertify on time can result in a return to the standard repayment plan, potentially causing payments to skyrocket. Additionally, while forgiven amounts under IDR plans are generally taxed as income, borrowers may qualify for tax-free forgiveness under the Public Service Loan Forgiveness (PSLF) program if they work full-time for a qualifying employer, such as a government or nonprofit organization, and make 120 qualifying payments.

A critical but often misunderstood aspect of IDR plans is the treatment of interest. If monthly payments are insufficient to cover accruing interest, the difference may capitalize, increasing the loan balance. For example, a borrower on an IBR plan with a low income might see their balance grow over time due to unpaid interest. To mitigate this, borrowers should explore options like REPAYE, which offers a subsidy covering 50% of unpaid interest for the first three years.

In conclusion, income-driven repayment plans are a powerful tool for managing student loan debt, offering both immediate payment relief and long-term forgiveness opportunities. Borrowers must navigate these plans carefully, staying vigilant about recertification and understanding the nuances of interest accrual. By doing so, they can leverage IDR plans to achieve financial stability and, ultimately, debt-free status.

Is Your SoFi Student Loan Eligible for Forgiveness? Find Out Now

You may want to see also

Explore related products

![]()

Public Service Loan Forgiveness (PSLF) requirements

The Public Service Loan Forgiveness (PSLF) program is a lifeline for borrowers committed to careers in public service, offering tax-free forgiveness of federal student loans after 120 qualifying payments. However, navigating its requirements demands precision. First, only Direct Loans qualify—Federal Family Education Loans (FFEL) or Perkins Loans must be consolidated into a Direct Consolidation Loan. Second, borrowers must work full-time for a qualifying employer, such as government organizations, 501(c)(3) nonprofits, or certain other eligible entities. Part-time workers can qualify if combined employment meets 30+ hours per week. Payments must be made under an income-driven repayment plan, ensuring affordability based on income and family size. For instance, Revised Pay As You Earn (REPAYE) caps payments at 10% of discretionary income for single borrowers earning under $22,000 annually. Crucially, each payment must be on time and for the full amount due. Missteps, like submitting payments late or enrolling in the wrong repayment plan, can reset the 120-payment counter. To avoid pitfalls, borrowers should annually submit the Employment Certification Form to confirm eligibility and track progress. While PSLF’s requirements are stringent, they offer a clear path to debt relief for those dedicated to public service.

Consider the case of a social worker earning $45,000 annually with $60,000 in student loans. Under REPAYE, their monthly payment would be approximately $208, compared to $666 under the Standard 10-Year Plan. By committing to a qualifying employer and maintaining consistent payments, they could save over $50,000 in total repayment. However, this example underscores the importance of meticulous record-keeping and adherence to PSLF rules. For instance, switching employers without verifying eligibility could disqualify previous payments. Borrowers should also beware of common pitfalls, such as assuming all nonprofits qualify—only 501(c)(3) organizations and specific government entities meet the criteria. Practical tips include setting payment reminders, keeping detailed employment records, and consulting the Federal Student Aid website for updates.

From a comparative perspective, PSLF stands out among forgiveness programs for its tax-free benefit and relatively short 10-year timeline. Unlike income-driven repayment forgiveness, which requires 20–25 years of payments and taxes forgiven amounts, PSLF rewards public service with quicker, tax-free relief. However, its strict eligibility criteria make it less accessible than other programs. For example, Teacher Loan Forgiveness offers up to $17,500 after five years in low-income schools but does not eliminate the entire balance. Borrowers must weigh their career trajectory and financial situation when choosing between programs. A persuasive argument for PSLF is its alignment with long-term public service careers, offering a tangible reward for societal contributions.

Descriptively, the PSLF application process is a meticulous journey requiring patience and organization. Borrowers must first confirm their loan type and consolidate if necessary, a step that can take 60–90 days. Next, they must secure full-time employment with a qualifying employer, ensuring their role aligns with the organization’s mission. Each year, submitting the Employment Certification Form provides a snapshot of progress and flags potential issues early. The final step, submitting the PSLF application after 120 payments, is both a culmination and a test of adherence to the program’s rules. Success stories abound, such as a nurse practitioner who eliminated $120,000 in debt after a decade of service, but they highlight the importance of understanding and meeting every requirement.

In conclusion, PSLF is a powerful tool for public service professionals, but its requirements demand vigilance and planning. By focusing on loan type, employer eligibility, repayment plan, and payment consistency, borrowers can maximize their chances of success. Practical steps, like annual certification and staying informed, mitigate risks and ensure progress. While the program’s rules may seem daunting, the reward of debt-free living makes it a worthwhile pursuit for those committed to serving their communities.

ITT Tech Student Loan Forgiveness: What Borrowers Need to Know

You may want to see also

Explore related products

![]()

Biden administration’s student loan forgiveness updates

The Biden administration's student loan forgiveness initiatives have been a focal point of policy debate, with significant updates shaping the landscape for millions of borrowers. One of the most notable actions was the announcement of a one-time debt cancellation of up to $20,000 for Pell Grant recipients and up to $10,000 for other federal loan borrowers earning less than $125,000 annually (or $250,000 for married couples). This move, unveiled in August 2022, aimed to alleviate financial strain on lower- and middle-income borrowers. However, legal challenges swiftly followed, leading to a Supreme Court ruling in June 2023 that struck down the program, citing a lack of congressional authorization. This decision left millions in limbo, awaiting further action.

In response to the setback, the Biden administration pivoted to alternative strategies, emphasizing targeted relief rather than broad cancellation. One such effort is the expansion of the Saving on a Valuable Education (SAVE) repayment plan, which caps monthly payments at a more manageable percentage of discretionary income and forgives remaining balances after 10 years for borrowers with original loan amounts of $12,000 or less. Additionally, the administration has prioritized fixing administrative issues in income-driven repayment (IDR) plans, leading to $39 billion in debt cancellation for 804,000 borrowers who had made qualifying payments but were not receiving credit toward forgiveness. These measures reflect a shift toward incremental, legally defensible solutions.

Another critical update is the administration’s focus on Public Service Loan Forgiveness (PSLF) reforms. By streamlining the application process and allowing previously ineligible payments to count toward forgiveness, the program has delivered $42 billion in relief to 650,000 public servants. This initiative underscores the administration’s commitment to supporting borrowers who dedicate their careers to public service. However, critics argue that these reforms, while impactful, do not address the systemic issues of rising tuition costs and the overall student debt crisis.

For borrowers navigating these updates, practical steps include enrolling in the SAVE plan to reduce monthly payments and tracking eligibility for targeted forgiveness programs like PSLF. It’s also crucial to monitor official announcements from the Department of Education, as the administration continues to explore new avenues for relief, such as rulemaking under the Higher Education Act. While broad cancellation remains uncertain, these updates offer tangible benefits for specific borrower groups, highlighting the importance of staying informed and proactive in managing student debt.

Biden's Student Loan Forgiveness: How Many Borrowers Benefited?

You may want to see also

Explore related products

![]()

State-specific student loan forgiveness initiatives

While federal student loan forgiveness programs often dominate headlines, a patchwork of state-specific initiatives offers targeted relief to borrowers based on profession, location, and financial need. These programs, though smaller in scale, can provide significant assistance to eligible individuals.

Understanding these state-level options is crucial for borrowers seeking comprehensive debt relief strategies.

Targeting Essential Professions: Many states recognize the value of attracting and retaining professionals in high-demand fields. For instance, California's "Bachelor of Science in Nursing Loan Repayment Program" offers up to $50,000 in loan repayment assistance to nurses working in underserved areas. Similarly, New York's "Doctors Across New York" program provides loan forgiveness to physicians practicing in designated shortage areas. These initiatives not only alleviate debt burdens but also address critical workforce shortages in healthcare and other vital sectors.

Geographic Incentives: Some states leverage loan forgiveness as a tool for economic development and community revitalization. For example, Kansas's "Rural Opportunity Zones" program offers student loan repayments of up to $15,000 over five years to individuals who relocate to designated rural counties. This approach not only benefits borrowers but also injects talent and economic activity into areas facing population decline.

Repayment Assistance for Public Service: States often prioritize supporting individuals dedicated to public service. Illinois's "Public Service Loan Repayment Program" provides up to $5,000 annually for four years to borrowers working in qualifying public service jobs, including teaching, social work, and law enforcement. These programs acknowledge the societal value of these professions and aim to make them more financially viable.

Navigating State Programs: Researching and applying for state-specific loan forgiveness programs requires diligence. Borrowers should:

- Identify Eligibility: Carefully review program criteria, including profession, employment location, income limits, and loan type eligibility.

- Meet Deadlines: Application deadlines vary, so staying informed is crucial.

- Gather Documentation: Prepare necessary documents, such as proof of employment, loan statements, and tax returns.

- Seek Guidance: Utilize resources like state higher education agencies and financial aid offices for assistance.

Missouri's Tax Rules on Student Loan Forgiveness: What You Need to Know

You may want to see also

Frequently asked questions

Yes, the government has offered various student loan forgiveness programs, such as Public Service Loan Forgiveness (PSLF) and income-driven repayment (IDR) plans. Additionally, temporary relief measures and targeted forgiveness initiatives have been introduced in recent years.

Qualification depends on the program. For example, PSLF requires working full-time in public service and making 120 qualifying payments. IDR plans forgive remaining balances after 20–25 years of payments. Recent initiatives may have specific eligibility criteria based on income, loan type, or other factors.

No, eligibility varies. Federal student loans, such as Direct Loans, are typically eligible for forgiveness programs. Private student loans are generally not eligible for government forgiveness initiatives.

To apply, review the specific requirements of the program you qualify for. For PSLF, submit an Employment Certification Form annually and a forgiveness application after 120 payments. For IDR forgiveness, ensure your loans are enrolled in an eligible plan and track your payments. Check the Federal Student Aid website for updates and application instructions.