The topic of student debt forgiveness has become a pressing issue in recent years, as millions of borrowers struggle under the weight of mounting educational loans. With the average student debt in the United States exceeding $30,000, many are left wondering about the possibility of widespread debt relief. The chance that student debt will be forgiven largely depends on political, economic, and social factors, including government policies, public opinion, and the financial health of the nation. Advocates argue that forgiveness could stimulate the economy and alleviate financial stress for millions, while critics raise concerns about fairness, cost, and long-term implications. As debates continue and proposals emerge, understanding the likelihood and potential scope of student debt forgiveness remains a critical concern for borrowers, policymakers, and the broader public.

| Characteristics | Values |

|---|---|

| Current Status (as of Oct 2023) | No widespread student debt forgiveness program is currently active. Biden administration's previous forgiveness plan was blocked by Supreme Court in June 2023. |

| Supreme Court Ruling (June 2023) | Struck down Biden's plan to forgive up to $20,000 in federal student debt for eligible borrowers, citing lack of congressional authorization. |

| Pending Legislation | Several bills proposing targeted forgiveness (e.g., for public service workers, low-income borrowers) are in Congress but face uncertain passage. |

| Biden Administration's Stance | Exploring alternative pathways for debt relief, including income-driven repayment (IDR) reforms and Public Service Loan Forgiveness (PSLF) improvements. |

| Public Opinion | ~60% of Americans support some form of student debt forgiveness, though opinions vary by political affiliation (Pew Research, 2023). |

| Economic Impact | Widespread forgiveness could stimulate consumer spending but may increase inflationary pressures and national debt concerns. |

| Targeted Forgiveness Programs | Existing programs like PSLF, Teacher Loan Forgiveness, and IDR plans offer limited relief to eligible borrowers. |

| State-Level Initiatives | Some states (e.g., New York, California) offer localized forgiveness programs for specific professions or residents. |

| Chances of Broad Forgiveness | Low in the near term due to legal and political hurdles, but targeted relief remains possible. |

| Key Influencing Factors | Congressional action, legal challenges, economic conditions, and presidential priorities. |

Explore related products

What You'll Learn

![]()

Biden’s Student Loan Forgiveness Plan Updates

As of the latest updates, President Biden's student loan forgiveness plan has been a rollercoaster of legal battles and policy adjustments, leaving borrowers in a state of uncertainty. The initial proposal aimed to forgive up to $20,000 in federal student loan debt for Pell Grant recipients and $10,000 for other eligible borrowers, but its implementation has been halted by court challenges. The Supreme Court’s decision in June 2023 struck down the plan, citing that the administration overstepped its authority under the HEROES Act. This setback has forced the Biden administration to explore alternative pathways to provide relief, such as using the Higher Education Act, though progress remains slow.

Analyzing the current landscape, the chance of widespread student debt forgiveness hinges on legislative and legal maneuvers. The administration’s shift to income-driven repayment (IDR) plans, like the Saving on a Valuable Education (SAVE) plan, offers partial relief by reducing monthly payments and forgiving remaining balances after 10–25 years, depending on the loan type. However, this approach is incremental and does not address the immediate financial burden many borrowers face. Advocates argue that only congressional action, such as passing the Student Loan Forgiveness Act, could provide comprehensive relief, but partisan gridlock makes this unlikely in the near term.

For borrowers navigating this uncertainty, practical steps include enrolling in the SAVE plan to lower payments and tracking public service loan forgiveness (PSLF) eligibility if working in qualifying sectors. Additionally, staying informed through official channels like the Department of Education’s Federal Student Aid website is crucial, as updates often come with short notice. While the odds of broad forgiveness remain uncertain, targeted relief programs and administrative adjustments offer temporary solutions for those in dire need.

Comparatively, other countries like Germany and Norway have implemented tuition-free higher education or automatic debt forgiveness, highlighting the U.S.’s unique challenges in addressing student debt. The Biden administration’s efforts, though ambitious, are constrained by legal and political barriers, making incremental reforms the most viable path forward. Borrowers should focus on maximizing existing programs while advocating for systemic change to increase the likelihood of future forgiveness initiatives.

In conclusion, while the chance of immediate, large-scale student debt forgiveness remains low due to legal and political hurdles, the Biden administration’s pivot to alternative relief measures provides a glimmer of hope. By leveraging available programs and staying informed, borrowers can mitigate their debt burden while pushing for broader solutions. The fight for student debt forgiveness is far from over, but strategic action today can pave the way for progress tomorrow.

Who Passed the No Forgive Student Loan Act? Unveiling the Truth

You may want to see also

Explore related products

![]()

Congressional Support for Debt Relief

Congressional support for student debt relief has been a pivotal factor in shaping the likelihood of widespread forgiveness. Historically, Democrats have championed debt cancellation as a means to address economic inequality, with figures like Senator Elizabeth Warren and Senate Majority Leader Chuck Schumer advocating for up to $50,000 in forgiveness per borrower. Their efforts culminated in President Biden’s 2022 executive order canceling $10,000 to $20,000 in debt for eligible borrowers, though it was later blocked by the Supreme Court. This highlights the party’s commitment but also underscores the fragility of executive action without legislative backing.

In contrast, Republican opposition has consistently framed debt forgiveness as fiscally irresponsible and unfair to taxpayers who did not attend college. GOP lawmakers argue that broad cancellation would inflate the national debt and fail to address the root causes of rising tuition costs. Their resistance has been a significant barrier, as bipartisan support is nearly nonexistent. However, some Republicans have proposed targeted solutions, such as expanding income-driven repayment plans or simplifying loan forgiveness programs for public servants, signaling a willingness to compromise on narrower reforms.

The legislative process itself presents another hurdle. Debt relief requires congressional approval, which has proven elusive due to filibuster rules in the Senate. Democrats’ inability to secure 60 votes for comprehensive forgiveness has forced them to rely on executive actions, which are vulnerable to legal challenges. This dynamic suggests that meaningful progress will depend on either a shift in Republican sentiment, a change in Senate rules, or a Democratic supermajority—none of which are guaranteed in the current political climate.

Despite these challenges, advocacy groups and grassroots movements continue to pressure Congress to act. Polls consistently show that a majority of Americans support some form of student debt relief, particularly among younger voters. This public sentiment has kept the issue alive, even as legislative efforts stall. For borrowers, the takeaway is clear: while congressional support remains divided, targeted advocacy and strategic voting in key elections could tip the balance in favor of relief. In the meantime, exploring existing programs like Public Service Loan Forgiveness or income-driven repayment plans offers a more immediate path to managing debt.

Government Contractors and Student Loan Forgiveness: What You Need to Know

You may want to see also

Explore related products

![]()

Legal Challenges to Forgiveness Programs

Legal challenges to student debt forgiveness programs have emerged as a significant obstacle, threatening to derail efforts to provide relief to millions of borrowers. One of the most prominent examples is the lawsuit filed against the Biden administration’s 2022 debt forgiveness plan, which was blocked by the Supreme Court in a 6-3 decision. The Court ruled that the administration overstepped its authority under the HEROES Act, a law designed to assist military service members, not to enact sweeping debt cancellation. This case underscores the critical role of statutory interpretation in determining the legality of such programs. Advocates for forgiveness must now navigate this legal precedent, either by crafting new legislation or finding alternative legal grounds to support their initiatives.

To understand the landscape of legal challenges, consider the three primary arguments opponents use: lack of congressional authorization, violation of the Appropriations Clause, and standing to sue. First, challengers often claim that executive actions on debt forgiveness bypass Congress, which holds the power to allocate federal funds. Second, the Appropriations Clause of the Constitution requires that public funds be spent only as Congress directs, a principle that has been central to lawsuits against forgiveness programs. Third, plaintiffs must demonstrate standing—a concrete injury caused by the program—which has been a contentious issue in recent cases. For instance, in *Nebraska v. Biden*, states argued that debt cancellation would harm their tax revenues, though the Supreme Court ultimately dismissed the case on standing grounds.

A strategic approach to overcoming these challenges involves addressing them preemptively in the design of forgiveness programs. Policymakers could explicitly seek congressional approval for debt relief, ensuring a clear legal foundation. Alternatively, they could tie forgiveness to existing statutes with broader authority, such as the Higher Education Act, which grants the Secretary of Education more flexibility in managing federal student loans. Another tactic is to limit the scope of forgiveness to specific groups, such as low-income borrowers or those defrauded by predatory institutions, which could reduce legal vulnerabilities by aligning with established precedents for targeted relief.

Comparatively, legal challenges to student debt forgiveness mirror those faced by other executive actions, such as immigration policies or environmental regulations. In each case, opponents exploit ambiguities in statutory language and constitutional principles to halt progress. However, the stakes in student debt cases are uniquely high, as they directly impact the financial stability of millions. Borrowers awaiting relief must remain informed about ongoing litigation, as court decisions can swiftly alter the landscape. For example, the Supreme Court’s ruling in *Department of Education v. Brown* (2023) clarified that borrowers cannot sue for debt cancellation unless they have exhausted administrative remedies, a cautionary tale for future advocacy efforts.

Ultimately, the chance of student debt being forgiven hinges on the ability to navigate these legal challenges effectively. While the path forward is fraught with obstacles, history shows that persistent advocacy and strategic legal maneuvering can yield results. Borrowers should stay engaged with policy developments, support legislative efforts, and prepare for potential administrative hurdles. As the debate continues, one thing is clear: the legal battlefield will remain a decisive arena in determining the fate of student debt forgiveness.

Student Debt Forgiveness: Who Bears the Cost and How?

You may want to see also

Explore related products

$9.99 $12.99

$14.95 $14.95

![]()

Economic Impact of Debt Cancellation

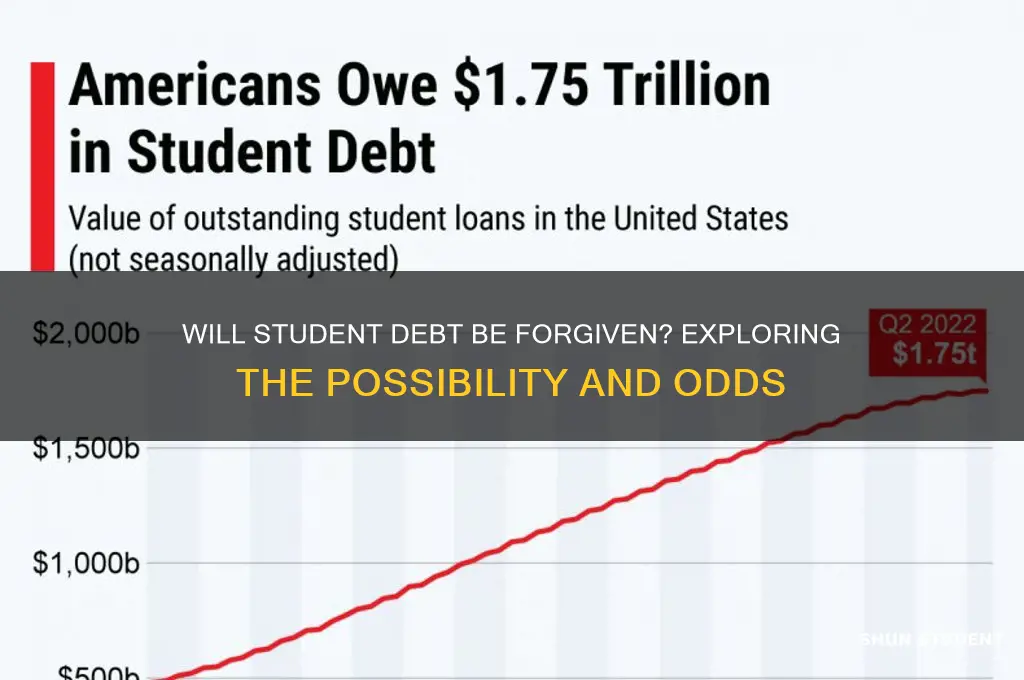

The cancellation of student debt has been a hotly debated topic, with proponents arguing it could stimulate the economy and critics warning of potential inflationary pressures. To understand its economic impact, consider the sheer scale: as of 2023, outstanding student loan debt in the U.S. exceeds $1.7 trillion, held by approximately 43 million borrowers. Forgiveness, even partial, would inject significant liquidity into the economy, as borrowers redirect funds from loan payments to consumption, savings, or investments. For instance, canceling $10,000 per borrower could free up roughly $300 billion in spending power, potentially boosting sectors like housing, retail, and small businesses. However, the effectiveness of this stimulus depends on how borrowers allocate the freed-up funds—whether they spend, save, or pay down other debts.

Analyzing the distributional effects reveals another layer of economic impact. Student debt cancellation would disproportionately benefit lower- and middle-income borrowers, who often struggle with repayment and have higher marginal propensities to consume. For example, a borrower earning $40,000 annually with $30,000 in debt might redirect $200–$300 monthly payments toward groceries, rent, or local services. This targeted relief could reduce income inequality and stimulate demand in underserved communities. Conversely, higher-income borrowers, who hold a larger share of total debt, might save or invest the freed-up funds, contributing less to immediate consumption but potentially driving long-term economic growth through capital formation.

A critical caution lies in the potential macroeconomic risks. Large-scale debt cancellation could exacerbate inflation if the increase in consumer spending outpaces supply. For instance, if $500 billion in debt were forgiven, and 70% of that translated into immediate spending, it could add 2–3 percentage points to GDP growth in the short term but also heighten inflationary pressures. Policymakers would need to balance this stimulus with monetary tightening to avoid overheating the economy. Additionally, the long-term cost of forgiveness—estimated at $1.6 trillion over a decade—would add to the federal deficit, potentially crowding out other government spending or necessitating tax increases, which could offset some of the economic benefits.

To maximize the positive economic impact, debt cancellation should be paired with structural reforms. For example, capping annual loan amounts or implementing income-driven repayment plans could prevent future debt accumulation. Targeting forgiveness to specific groups, such as borrowers in public service or those with incomes below a certain threshold, could enhance equity and efficiency. Practical steps for borrowers post-cancellation include creating emergency funds, investing in retirement accounts, or paying down high-interest credit card debt. By combining immediate relief with long-term solutions, debt cancellation could serve as both a short-term stimulus and a foundation for sustainable economic growth.

Will Graduate Student Loans Qualify for Loan Forgiveness Programs?

You may want to see also

Explore related products

![]()

Public Opinion on Loan Forgiveness

Public opinion on student loan forgiveness is deeply divided, reflecting broader ideological and generational tensions. Surveys consistently show that younger Americans, particularly those aged 18 to 34, overwhelmingly support debt cancellation, with nearly 60% in favor according to a 2023 Pew Research Center poll. This demographic bears the brunt of the $1.7 trillion student debt crisis, with the average borrower owing over $37,000. For them, forgiveness isn’t just a policy—it’s a lifeline to financial stability, enabling homeownership, entrepreneurship, and family planning. In contrast, older generations, especially those over 55, are more skeptical, with only 35% supporting broad cancellation. This divide often hinges on perceptions of fairness: younger borrowers see education as a public good, while older respondents recall paying off their own debts without assistance.

The political lens further polarizes public opinion. Democrats and Democratic-leaning independents are twice as likely as Republicans to support loan forgiveness, with 78% versus 32%, respectively, according to a 2022 Morning Consult poll. This partisan split mirrors debates over government intervention in the economy. Progressives frame forgiveness as a corrective to systemic inequalities, pointing to skyrocketing tuition costs and predatory lending practices. Conservatives, however, argue it rewards irresponsible borrowing and shifts the burden to taxpayers who didn’t attend college. This ideological clash isn’t just about dollars—it’s about the role of government in addressing societal challenges.

Interestingly, public opinion softens when forgiveness is targeted rather than universal. For instance, 70% of Americans support debt cancellation for low-income borrowers, and 65% back relief for those defrauded by for-profit colleges, as revealed by a 2023 Data for Progress study. These findings suggest that while broad forgiveness remains contentious, there’s consensus on helping vulnerable groups. Policymakers could leverage this nuance by designing programs that balance equity with fiscal responsibility, such as capping forgiveness at $10,000 per borrower or tying relief to income-driven repayment plans.

Despite these divisions, one trend is undeniable: public awareness of student debt has reached a tipping point. Social media campaigns like #CancelStudentDebt have mobilized millions, while high-profile figures from Senator Elizabeth Warren to rapper Cardi B have amplified the issue. This visibility has shifted the narrative from individual responsibility to systemic reform, making forgiveness a mainstream policy debate. Yet, translating awareness into action requires navigating legal, economic, and political hurdles—a challenge that will test the resilience of public support in the years ahead.

Will Nevada Tax Student Loan Forgiveness? What Borrowers Need to Know

You may want to see also

Frequently asked questions

As of now, the likelihood of widespread student debt forgiveness remains uncertain and depends on political and legislative actions. While there have been proposals and executive actions, such as targeted forgiveness programs, broad-scale forgiveness faces legal and political challenges.

Yes, the government has forgiven student debt for specific groups, such as borrowers under the Public Service Loan Forgiveness (PSLS) program and those defrauded by predatory schools. However, broad forgiveness for all borrowers has not been implemented.

President Biden has expressed support for limited student debt forgiveness and has taken executive actions to cancel debt for specific groups. However, broad forgiveness through executive action faces legal challenges and opposition, making its likelihood uncertain.

The inclusion of student debt forgiveness in future legislation depends on congressional support and political priorities. While some lawmakers advocate for it, bipartisan agreement is challenging, reducing the chances of immediate passage.

Stay informed by following official government announcements, reputable news sources, and updates from the Department of Education. Additionally, advocacy groups and financial advisors often provide insights into potential changes.