The student loan forgiveness fee is a topic of significant interest and confusion among borrowers, as it often refers to the costs or implications associated with qualifying for and maintaining loan forgiveness programs. These programs, such as Public Service Loan Forgiveness (PSLF) or income-driven repayment plans, aim to alleviate the burden of student debt for eligible individuals. However, borrowers may encounter fees related to loan consolidation, application processing, or potential tax liabilities upon forgiveness, depending on the program and their financial situation. Understanding these fees is crucial for borrowers to make informed decisions and maximize the benefits of loan forgiveness while minimizing unexpected financial obligations.

Explore related products

What You'll Learn

![]()

Eligibility criteria for loan forgiveness

Student loan forgiveness isn't automatic; it's a privilege earned through specific eligibility criteria. These criteria vary depending on the forgiveness program, but generally revolve around your profession, employer, repayment plan, and years of service.

Understanding these requirements is crucial for anyone seeking to shed the burden of student debt.

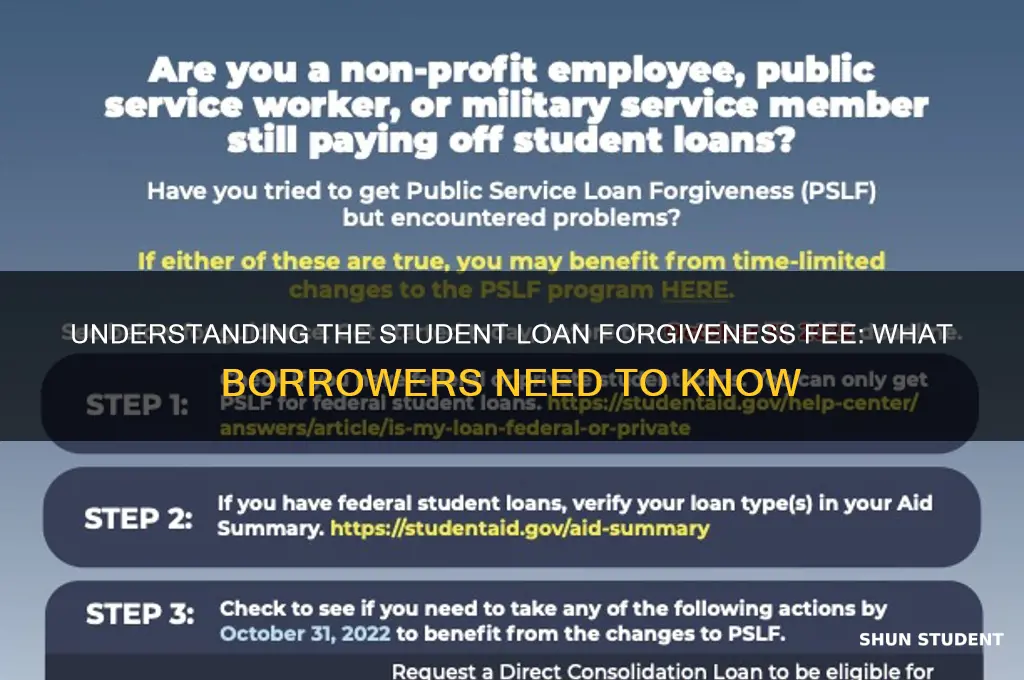

Public Service Loan Forgiveness (PSLF) stands out as a beacon for those dedicated to serving the greater good. This program offers tax-free forgiveness of remaining loan balances after 120 qualifying payments (10 years) while working full-time for a qualifying employer. Eligible employers include government organizations at any level (federal, state, local), 501(c)(3) non-profits, and some other types of non-profits providing specific public services. Crucially, the type of loan matters – only Direct Loans qualify for PSLF. Consolidating other federal loans into a Direct Consolidation Loan can make them eligible, but beware: any payments made before consolidation don't count towards the 120 required.

Pro Tip: Submit an Employment Certification Form annually to ensure your payments are tracking towards forgiveness.

Teacher Loan Forgiveness rewards educators who dedicate themselves to low-income schools. This program offers forgiveness of up to $17,500 on Direct Subsidized and Unsubsidized Loans after five consecutive years of teaching full-time in a low-income elementary or secondary school. Highly qualified teachers in math, science, or special education may be eligible for the maximum amount, while others can receive up to $5,000. Important Note: This program cannot be combined with PSLF.

Income-Driven Repayment (IDR) plans offer a lifeline for borrowers struggling with high loan payments relative to their income. These plans cap monthly payments at a percentage of your discretionary income and offer forgiveness of any remaining balance after 20-25 years of qualifying payments. The specific forgiveness timeline depends on the IDR plan chosen. Caution: Forgiven amounts under IDR plans may be considered taxable income.

Strategic Tip: Recertify your income annually to ensure your payments remain affordable and continue counting towards forgiveness.

Other forgiveness programs cater to specific professions and circumstances. For example, the National Health Service Corps offers loan repayment assistance to healthcare professionals serving in underserved areas. Similarly, some states and employers offer their own loan forgiveness programs. Action Step: Research programs specific to your field and location to uncover hidden opportunities.

Student Loan Forgiveness: Top Places to Apply for Relief

You may want to see also

Explore related products

![]()

Types of student loan forgiveness programs

Student loan forgiveness programs are not one-size-fits-all solutions. They vary widely in eligibility, requirements, and benefits, often tailored to specific professions, financial situations, or public service commitments. Understanding these distinctions is crucial for borrowers seeking relief from their student debt. Here’s a breakdown of the primary types of forgiveness programs available.

Public Service Loan Forgiveness (PSLF) stands out as one of the most well-known programs. Designed for borrowers working full-time in qualifying public service jobs, such as government, education, or nonprofit sectors, PSLF offers tax-free forgiveness of the remaining loan balance after 120 eligible payments. A critical detail: only federal Direct Loans qualify, and payments must be made under an income-driven repayment plan. Borrowers should submit an Employment Certification Form annually to ensure they’re on track, as mistakes in loan type or payment plan can disqualify them.

Teacher Loan Forgiveness targets educators in low-income schools, offering up to $17,500 in forgiveness for secondary math or science teachers, or special education teachers, and $5,000 for other qualifying teachers after five consecutive years of service. This program is less stringent than PSLF but caps forgiveness at a fixed amount. Teachers must work full-time in a Title I school, ensuring their efforts directly benefit underserved communities. Combining this program with PSLF is possible, but careful planning is required to maximize benefits.

Income-Driven Repayment (IDR) Forgiveness benefits borrowers with high debt relative to their income. Under plans like Pay As You Earn (PAYE), Revised Pay As You Earn (REPAYE), or Income-Based Repayment (IBR), remaining balances are forgiven after 20–25 years of qualifying payments. While this option is accessible to most federal loan borrowers, the forgiven amount is taxed as income, potentially resulting in a significant tax bill. Borrowers should consult a tax professional to plan for this liability.

Perkins Loan Cancellation is a lesser-known but valuable program for borrowers with Federal Perkins Loans. Forgiveness is granted incrementally over five years of service in eligible professions, such as teaching, nursing, or public defense. For example, teachers can receive up to 100% cancellation, with 15% forgiven for the first and second years, 20% for the third and fourth years, and 30% for the fifth year. This program is particularly beneficial for those in high-need fields but is limited to Perkins Loan holders, a dwindling group since the program ended in 2017.

Each forgiveness program requires meticulous documentation and adherence to specific rules. Borrowers should regularly review their eligibility, track payments, and stay informed about policy changes. While the "fee" for forgiveness is often time and commitment rather than a monetary charge, the long-term financial relief can be life-changing for those who qualify.

Do Students Embrace Grade Forgiveness in College? Insights and Opinions

You may want to see also

Explore related products

![]()

Application process and requirements

The application process for student loan forgiveness programs is a critical step for borrowers seeking relief from their financial burden. It’s not a one-size-fits-all procedure; instead, it varies depending on the specific forgiveness program. For instance, the Public Service Loan Forgiveness (PSLF) program requires borrowers to submit an Employment Certification Form annually or when changing employers, ensuring they remain on track for forgiveness after 120 qualifying payments. In contrast, income-driven repayment (IDR) plan forgiveness, which applies after 20–25 years of payments, necessitates consistent annual income and family size recertification to adjust payment amounts. Understanding these program-specific steps is essential to avoid delays or disqualification.

Analyzing the requirements reveals a common thread: documentation is key. Borrowers must provide proof of employment, income, and loan payments, often through forms like the PSLF Employment Certification Form or tax returns for IDR plans. For teacher loan forgiveness, applicants must submit an application to their loan servicer along with certification from their school’s chief administrative officer. Missing or incomplete documents can derail the process, so meticulous record-keeping is non-negotiable. Additionally, eligibility criteria such as loan type (e.g., Direct Loans for PSLF) and repayment plan (e.g., IDR plans for IDR forgiveness) are strictly enforced, leaving no room for error.

Persuasively, borrowers should approach the application process with a proactive mindset. Waiting until the last minute to apply for forgiveness can lead to missed deadlines or insufficient payment counts. For example, PSLF applicants are encouraged to submit Employment Certification Forms early and often to catch any discrepancies in qualifying payments. Similarly, those pursuing IDR forgiveness should monitor their payment counts and ensure their servicer is accurately tracking progress. A strategic approach, including regular check-ins with loan servicers and staying informed about program updates, can significantly increase the likelihood of success.

Comparatively, the application process for student loan forgiveness differs from other financial relief programs, such as loan consolidation or refinancing. While consolidation simplifies multiple loans into one, it resets the clock on forgiveness programs like PSLF, potentially costing borrowers years of progress. Refinancing with a private lender eliminates eligibility for federal forgiveness programs altogether. This highlights the importance of understanding the trade-offs before making decisions that could impact forgiveness eligibility. Borrowers must weigh their options carefully, prioritizing long-term forgiveness goals over short-term payment reductions.

Descriptively, the application journey can feel like navigating a maze, but with the right tools, it becomes manageable. Online resources, such as the Federal Student Aid website, offer step-by-step guides and downloadable forms for each program. Workshops and webinars hosted by financial aid experts provide additional support, particularly for complex programs like PSLF. Borrowers can also enlist the help of loan servicers or nonprofit organizations specializing in student debt relief. By leveraging these resources, applicants can transform a daunting process into a structured, achievable task, ultimately paving the way to financial freedom.

Understanding Obama's Student Loan Forgiveness Program: Eligibility and Benefits

You may want to see also

Explore related products

![]()

Tax implications of forgiven loans

Forgiven student loans can feel like a financial lifeline, but they often come with a hidden cost: taxes. The IRS generally considers forgiven debt as taxable income, meaning you could owe taxes on the amount forgiven. This is because the forgiven amount is treated as if you received it as income, even though you never actually saw the cash. For example, if $10,000 of your student loan is forgiven, you might need to report that $10,000 as income on your tax return, potentially pushing you into a higher tax bracket.

However, there are exceptions to this rule, particularly under specific programs like Public Service Loan Forgiveness (PSLF) or income-driven repayment plans. Under PSLF, the forgiven amount is tax-free, providing a significant advantage for those who qualify. Similarly, the Tax Cuts and Jobs Act of 2017 temporarily made student loan forgiveness under income-driven repayment plans tax-free until 2025. This means that if your loans are forgiven through these programs before 2026, you won’t owe taxes on the forgiven amount. But beware: this provision could expire or change, so staying informed about current tax laws is crucial.

If your forgiven loan is taxable, you’ll receive a Form 1099-C from your lender, reporting the amount to both you and the IRS. This form is your cue to include the forgiven amount as income on your tax return. Failing to report it could lead to penalties or audits. To minimize the tax impact, consider adjusting your tax withholdings or making estimated tax payments throughout the year. For instance, if you anticipate $5,000 in taxable forgiven loans, you might increase your quarterly estimated payments by $1,250 to avoid a large tax bill in April.

Comparing the tax implications of different forgiveness programs can help you make informed decisions. For example, while PSLF offers tax-free forgiveness, it requires 10 years of qualifying payments and employment in public service. In contrast, income-driven repayment plans may offer forgiveness after 20–25 years but could result in taxable income unless the current tax exclusion is extended. Weighing these options requires considering your career path, income stability, and long-term financial goals.

Finally, consulting a tax professional can be invaluable when navigating forgiven loan taxes. They can help you understand your specific situation, explore deductions or credits to offset the tax burden, and ensure compliance with IRS rules. For instance, if you’re self-employed or have other deductions, a professional can strategize to minimize your overall tax liability. While forgiven loans can provide relief, being proactive about their tax implications ensures you don’t face unexpected financial strain.

Indiana's Tax Treatment of Student Loan Forgiveness: What You Need to Know

You may want to see also

Explore related products

![]()

Common mistakes to avoid in applications

Applying for student loan forgiveness can be a lifeline for many, but the process is riddled with pitfalls that can derail even the most deserving applicants. One of the most common mistakes is submitting incomplete documentation. Forgiveness programs like Public Service Loan Forgiveness (PSLF) require specific forms, such as the Employment Certification Form, to be filed regularly. Missing a single document or failing to update employment details can reset the forgiveness clock, costing years of progress. Always double-check the required paperwork and maintain a checklist to ensure nothing slips through the cracks.

Another frequent error is misunderstanding eligibility criteria. Not all loans or repayment plans qualify for forgiveness. For instance, PSLF requires borrowers to have Direct Loans and make 120 qualifying payments under an income-driven repayment plan. Private loans or payments made under the wrong plan do not count. Before applying, verify your loan type and repayment plan using tools like the Federal Student Aid website. Ignoring these details can lead to disqualification, leaving you with a debt burden you thought was forgiven.

A third mistake is failing to track payment counts. Many applicants assume their servicer will accurately count qualifying payments, but errors are common. Keep a personal record of every payment, including dates, amounts, and confirmation numbers. If discrepancies arise, this documentation can serve as proof. Additionally, request an annual payment count from your servicer to cross-reference your records. Proactive tracking ensures you meet the required payment threshold without unpleasant surprises.

Lastly, delaying the application process is a costly oversight. Some programs, like PSLF, require 10 years of qualifying payments, but the clock doesn’t start until you submit your first Employment Certification Form. Waiting until the 10-year mark to begin the process can result in lost time. Start early, submit forms annually, and stay in regular communication with your loan servicer. Early action not only safeguards your progress but also allows time to correct mistakes before they become irreversible.

By avoiding these mistakes—incomplete documentation, eligibility misunderstandings, payment tracking errors, and procrastination—you can navigate the student loan forgiveness process with confidence. Each step requires diligence, but the reward of debt relief is well worth the effort.

Will OSLA Student Loans Be Forgiven? Exploring Potential Relief Options

You may want to see also

Frequently asked questions

There is no official "student loan forgiveness fee" charged by the government for legitimate forgiveness programs like Public Service Loan Forgiveness (PSLF) or income-driven repayment (IDR) forgiveness. Beware of scams claiming to require a fee for forgiveness.

No, applying for federal student loan forgiveness programs is free. You can submit applications and required forms directly through the U.S. Department of Education or your loan servicer without any fees.

Some third-party companies charge fees to help borrowers navigate forgiveness programs, but these services are unnecessary. Borrowers can apply for forgiveness on their own for free through official channels.

Yes, any request for a "student loan forgiveness fee" is likely a scam. Legitimate forgiveness programs do not require payment. Report such requests to the Federal Trade Commission (FTC) or the Department of Education.

If you paid a fee to a scam company, contact your bank or credit card provider to dispute the charge. Additionally, report the scam to the FTC and the Department of Education to help prevent others from falling victim.