President Biden has taken significant steps to address the student loan crisis in the United States, implementing several forgiveness programs aimed at providing relief to borrowers. One of the most notable initiatives is the Public Service Loan Forgiveness (PSLF) program overhaul, which has expanded eligibility and streamlined the application process for public servants. Additionally, Biden's administration has canceled billions in student debt for borrowers who were defrauded by for-profit colleges through the Borrower Defense to Repayment program. In August 2022, Biden announced a sweeping plan to forgive up to $20,000 in federal student loans for eligible borrowers, targeting low- and middle-income individuals. These actions reflect a broader effort to alleviate the financial burden on millions of Americans and address systemic issues within the student loan system.

| Characteristics | Values |

|---|---|

| Total Forgiveness Amount | Over $132 billion (as of October 2023) |

| Number of Borrowers Benefited | Over 3.6 million borrowers |

| Public Service Loan Forgiveness (PSLF) | Expanded eligibility, resulting in $42 billion in forgiveness for 650,000+ borrowers |

| Income-Driven Repayment (IDR) Fixes | $39 billion in forgiveness for 804,000 borrowers due to IDR account adjustments |

| Targeted Forgiveness for Defrauded Borrowers | $12.5 billion for 1.3 million borrowers under Borrower Defense to Repayment |

| COVID-19 Payment Pause Adjustments | $1.6 billion in forgiveness for borrowers with qualifying payments during the pause |

| Closed School Discharges | $1.5 billion for 92,000 borrowers who attended closed schools |

| Disability Discharges | $8.1 billion for 425,000 borrowers with total and permanent disabilities |

| Maximum Forgiveness per Borrower | Up to $20,000 (Pell Grant recipients) or $10,000 (non-Pell Grant recipients) under the one-time debt relief plan (currently blocked by courts) |

| Eligibility Criteria | Federal student loan borrowers earning < $125,000 (individual) or < $250,000 (married) |

| Loan Types Covered | Federal Direct Loans, FFELP loans (if consolidated into Direct Loans), and Perkins Loans |

| Current Status of One-Time Relief | Blocked by court rulings; Supreme Court decision in June 2023 upheld the block |

| Ongoing Forgiveness Programs | PSLF, IDR, Borrower Defense, Closed School Discharges, and Disability Discharges remain active |

Explore related products

What You'll Learn

![]()

Public Service Loan Forgiveness (PSLF) Expansion

One of the most significant moves by the Biden administration in addressing the student loan crisis has been the expansion of the Public Service Loan Forgiveness (PSLF) program. This initiative, designed to alleviate debt for those in public service, has seen substantial changes under Biden’s leadership, offering a lifeline to thousands of borrowers. By broadening eligibility criteria and simplifying the application process, the administration aims to fulfill the program’s original promise: debt relief for those who dedicate their careers to public service.

To understand the impact of the PSLF expansion, consider the practical steps borrowers must take to qualify. First, ensure your employment falls under the public service umbrella, which includes government organizations, nonprofits, and certain other qualifying employers. Second, consolidate your loans into a Direct Loan if they aren’t already, as only this type qualifies for PSLF. Third, submit the Employment Certification Form annually or when switching jobs to track your progress toward the required 120 qualifying payments. These steps, though detailed, are now more accessible due to temporary waivers introduced by the Biden administration, allowing past payments on ineligible loans to count toward forgiveness.

The expansion’s most notable change is the introduction of the Limited PSLF (LPSLFWaiver), a temporary measure that expired in October 2023. This waiver allowed borrowers to receive credit for past payments made on loans that previously didn’t qualify, such as Federal Family Education Loans (FFEL) or Perkins Loans, without consolidating them into Direct Loans. For example, a teacher with 10 years of payments on an FFEL loan could suddenly qualify for forgiveness under this waiver, provided they met public service employment criteria. This single change has led to billions in forgiven debt, transforming the financial futures of countless public servants.

Critics argue that the PSLF program, even with its expansion, remains complex and difficult to navigate. Borrowers often face confusion over qualifying payments, eligible employers, and loan types. However, the Biden administration has addressed these concerns by launching a user-friendly online tool and providing clearer guidance through the Department of Education. Additionally, the expansion includes a commitment to reviewing previously denied applications, ensuring that borrowers who were wrongly disqualified get a second chance. These efforts underscore a shift toward making PSLF more inclusive and less bureaucratic.

In conclusion, the PSLF expansion under Biden represents a targeted effort to honor the commitment made to public servants burdened by student debt. While challenges remain, the program’s broadened scope and simplified processes have already yielded tangible results. For borrowers, the key takeaway is to act promptly: review your eligibility, consolidate if necessary, and take advantage of remaining waivers or updates. The PSLF expansion is not just a policy change—it’s a recognition of the value public servants bring to society, and a step toward ensuring their financial stability.

Do You Qualify for Student Debt Forgiveness? Key Eligibility Criteria Explained

You may want to see also

Explore related products

![]()

Income-Driven Repayment (IDR) Plan Reforms

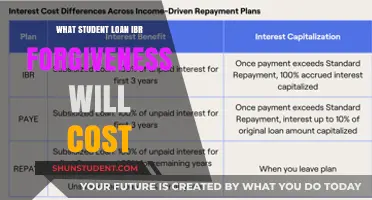

The Biden administration has significantly revamped Income-Driven Repayment (IDR) plans, aiming to provide more immediate and long-term relief for borrowers. One key reform is the reduction of monthly payments to a maximum of 5% of discretionary income for undergraduate loans, down from the previous 10%. This change, coupled with a more generous definition of discretionary income, ensures that borrowers have more manageable payments, particularly those with lower incomes. For instance, a borrower earning $40,000 annually with a family size of two could see their monthly payment drop from $200 to $100 under the new rules.

Another critical reform is the forgiveness of remaining balances after a shorter repayment period. Under the new IDR plans, borrowers with balances of $12,000 or less will have their loans forgiven after 10 years of payments, instead of the previous 20 or 25 years. This accelerated timeline is a game-changer for borrowers with smaller loan amounts, offering a clear path to debt-free status. For example, a borrower with a $10,000 loan and an annual income of $35,000 could be debt-free in a decade, provided they remain in the program and make consistent payments.

The administration has also addressed the issue of unpaid interest capitalization, a major contributor to loan balance growth. Under the reformed IDR plans, interest will no longer accrue for borrowers who make their monthly payments, even if those payments are as low as $0 due to their income level. This prevents balances from ballooning over time, a common frustration under previous plans. For a borrower with a $30,000 loan and an income that results in a $0 monthly payment, this reform could save thousands of dollars in interest over the life of the loan.

To ensure these reforms reach those who need them most, the Biden administration has simplified the application and recertification process for IDR plans. Borrowers can now apply directly through the Federal Student Aid website, with a streamlined form that reduces the paperwork burden. Additionally, the Department of Education will automatically enroll borrowers who are at risk of default into IDR plans, using data matching with the IRS to verify income. This proactive approach aims to reduce the number of borrowers falling into default, which can have severe financial consequences.

While these reforms represent significant progress, borrowers must take action to benefit from them. Current IDR participants should review their plans to ensure they are on the most advantageous option under the new rules. New borrowers should explore IDR plans early in their repayment journey, as the benefits of lower payments and faster forgiveness can have a profound impact on long-term financial health. By leveraging these reforms, borrowers can navigate their student loan debt with greater confidence and clarity.

Understanding the Financial Impact of IBR Forgiveness on Student Loans

You may want to see also

Explore related products

![]()

Fresh Start Initiative for Defaults

The Fresh Start Initiative is a lifeline for borrowers drowning in defaulted federal student loans, offering a rare second chance to regain financial stability. Launched in 2022 as part of Biden’s broader loan forgiveness efforts, it temporarily removes the harsh penalties of default, such as wage garnishment and tax refund seizures, allowing borrowers to re-enter repayment plans without immediate financial strain. This initiative targets the 7.5 million borrowers in default, providing a one-time opportunity to reset their loan status and avoid long-term credit damage.

To qualify, borrowers must have defaulted on federal loans held by the Department of Education. The initiative automatically pauses collections through September 30, 2024, giving borrowers time to enroll in income-driven repayment plans or consolidate their loans. For example, a borrower earning $40,000 annually could reduce their monthly payment to as little as $50 under an income-driven plan, making repayment manageable. Practical steps include logging into StudentAid.gov to review loan status, contacting the Default Resolution Group, and exploring consolidation options to combine multiple loans into one with a fixed interest rate.

Critically, Fresh Start is not permanent forgiveness but a pathway to rehabilitation. Borrowers must act before the initiative expires to avoid reverting to default status. Cautions include avoiding scams promising instant forgiveness and ensuring accurate income documentation for repayment plans. While the initiative eases immediate burdens, it requires commitment to long-term repayment strategies, such as budgeting tools or financial counseling, to prevent future defaults.

Comparatively, Fresh Start stands out from other Biden-era programs like Public Service Loan Forgiveness (PSLF) or the now-blocked $10,000 forgiveness plan. Unlike PSLF, it doesn’t require a decade of public service, and unlike broad forgiveness, it focuses on a specific demographic—defaulted borrowers. Its success hinges on borrower awareness and action, making outreach campaigns and simplified enrollment processes vital. For those overwhelmed by default, Fresh Start is a pragmatic, actionable solution to reclaim financial footing.

Unlocking Canadian Student Loan Forgiveness: A Comprehensive Guide to Debt Relief

You may want to see also

Explore related products

![]()

Targeted Forgiveness for Specific Groups

The Biden administration has strategically implemented targeted student loan forgiveness programs, focusing on specific groups disproportionately burdened by debt. This approach acknowledges that a one-size-fits-all solution fails to address systemic inequities in higher education financing. By pinpointing vulnerable populations, these initiatives aim to alleviate financial strain and promote economic mobility.

One notable example is the Public Service Loan Forgiveness (PSLF) waiver, which temporarily relaxed eligibility rules, allowing borrowers in public service careers to receive credit for previously disqualified payments. This targeted measure recognized the sacrifices made by teachers, nurses, and social workers, often underpaid despite their societal contributions. Another instance is the forgiveness for borrowers defrauded by for-profit colleges, primarily affecting low-income and minority students lured by false promises of career advancement. These institutions disproportionately targeted marginalized communities, leaving graduates with worthless degrees and insurmountable debt.

Targeted forgiveness also extends to disabled borrowers, who face unique financial challenges. The administration automatically discharged loans for individuals receiving Social Security Disability Insurance, streamlining a previously cumbersome process. This move acknowledged the intersection of disability and economic vulnerability, providing relief to a group often excluded from traditional workforce opportunities. Additionally, veterans have benefited from expanded forgiveness programs, recognizing their service and addressing the financial barriers many face upon returning to civilian life.

While these initiatives represent progress, critics argue they are piecemeal solutions to a systemic problem. However, their targeted nature allows for immediate impact on the most affected populations. For instance, the $1.5 billion in debt cancellation for borrowers who attended Corinthian Colleges directly addressed a specific instance of predatory lending, setting a precedent for holding fraudulent institutions accountable. This approach contrasts with broader forgiveness proposals, which face political and legal hurdles.

To maximize the effectiveness of targeted forgiveness, policymakers should prioritize data-driven identification of vulnerable groups, such as first-generation college students or those from historically underserved communities. Additionally, public awareness campaigns are crucial to ensure eligible borrowers know how to access these programs. For example, simplifying application processes and partnering with community organizations can bridge the gap between policy and implementation.

In conclusion, targeted forgiveness serves as a pragmatic tool to address the nuanced challenges of student debt. By focusing on specific groups, the Biden administration has delivered tangible relief to those most in need, setting a framework for future policies that prioritize equity and justice in higher education financing.

Student Loan Forgiveness Legislation: Who's Leading the Charge?

You may want to see also

Explore related products

![]()

One-Time $10,000 Cancellation Plan (Blocked)

The One-Time $10,000 Cancellation Plan, a cornerstone of President Biden’s early student loan relief efforts, promised to wipe out up to $10,000 in federal student debt for eligible borrowers, with an additional $10,000 for Pell Grant recipients. This plan, announced in August 2022, aimed to provide immediate financial relief to millions of Americans burdened by student loans. However, it faced swift legal challenges, culminating in a Supreme Court ruling in June 2023 that blocked its implementation. The Court determined the administration lacked the authority to enact such broad debt cancellation without explicit congressional approval.

To understand the plan’s scope, consider its eligibility criteria: borrowers earning less than $125,000 annually (or $250,000 for married couples) qualified for the relief. For context, this threshold covered approximately 90% of student loan borrowers. The plan targeted federal loans, including Direct Loans, Perkins Loans, and Federal Family Education Loans (FFEL) held by the Department of Education. Notably, privately held FFEL loans were excluded, leaving some borrowers in a precarious position. The cancellation would have been automatic for those with income data on file, while others would need to apply through a simple online form.

The plan’s blockage highlights a critical tension between executive action and legislative authority. While the Higher Education Act of 1965 grants the Secretary of Education broad powers to modify federal student loans, the Supreme Court ruled that debt cancellation on this scale required explicit congressional approval. This decision underscores the limits of presidential power and the need for bipartisan cooperation on such transformative policies. For borrowers, the ruling meant dashed hopes of immediate relief, with many left to navigate existing repayment plans or pursue Public Service Loan Forgiveness.

Despite its failure, the One-Time $10,000 Cancellation Plan sparked a national conversation about the student debt crisis. It forced policymakers, advocates, and the public to confront the systemic issues driving skyrocketing tuition costs and unsustainable debt burdens. While the plan itself remains blocked, its legacy includes targeted relief measures like the Saving on a Valuable Education (SAVE) repayment plan, which caps monthly payments at a lower percentage of discretionary income and forgives balances after 10–20 years. Borrowers should explore these alternatives, ensuring they stay informed about future policy changes.

In practical terms, borrowers should take proactive steps to manage their debt. First, verify your loan type and servicer through the Federal Student Aid website. Second, enroll in income-driven repayment plans like SAVE to lower monthly payments. Third, consider Public Service Loan Forgiveness if you work in a qualifying field. Finally, stay updated on legislative developments, as Congress remains the key player in any future broad-scale debt relief efforts. While the One-Time $10,000 Cancellation Plan is blocked, its impact on the student debt debate endures, offering lessons for both policymakers and borrowers alike.

Student Loan Forgiveness Update: Did the Bill Pass in 2023?

You may want to see also

Frequently asked questions

As of October 2023, President Biden has approved over $127 billion in student loan forgiveness for approximately 3.6 million borrowers through various programs, including targeted relief for public service workers, borrowers defrauded by for-profit schools, and those with total and permanent disabilities.

Eligibility varies by program. Key groups include borrowers earning under $125,000 (or $250,000 for married couples) who received Pell Grants or federal loans, public service workers under the PSLF program, and those with loans from specific for-profit schools or with total and permanent disabilities.

The broad $10,000 forgiveness plan (up to $20,000 for Pell Grant recipients) was blocked by the Supreme Court in June 2023. However, targeted forgiveness programs, such as those for public service workers and defrauded borrowers, remain active.

Visit the Federal Student Aid website (studentaid.gov) to review eligibility criteria for specific programs. Borrowers can also log in to their accounts to check their loan status and apply for forgiveness if applicable. Updates are regularly posted on the site.