When considering student loans, one of the most critical factors to evaluate is the interest rate, as it significantly impacts the total cost of borrowing. Generally, federal student loans tend to offer lower interest rates compared to private loans, making them a more affordable option for many borrowers. Among federal loans, Direct Subsidized Loans typically have the lowest rates because the government covers the interest while the borrower is in school, during the grace period, and in certain deferment periods. Unsubsidized Direct Loans and PLUS Loans also have fixed rates but are slightly higher. Private loans, on the other hand, often come with variable rates that can fluctuate over time, potentially increasing the overall repayment amount. Understanding these differences is essential for students and their families to make informed decisions and minimize long-term financial burden.

Explore related products

What You'll Learn

![]()

Federal vs. Private Loans

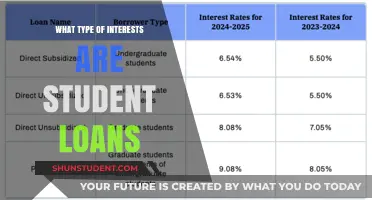

When considering student loans, one of the most critical factors to evaluate is the interest rate, as it significantly impacts the total cost of borrowing. Generally, federal student loans offer lower interest rates compared to private student loans. Federal loans are funded by the U.S. Department of Education and come with fixed interest rates set by Congress, which are typically lower than those offered by private lenders. For the 2023-2024 academic year, undergraduate federal loans have a fixed interest rate of 5.5%, while graduate loans are at 7.05%. These rates are standardized and do not fluctuate based on the borrower's credit history.

In contrast, private student loans are offered by banks, credit unions, and other financial institutions. Their interest rates can be either fixed or variable, and they are often higher than federal loan rates. Private lenders determine rates based on the borrower's creditworthiness, income, and other financial factors. Borrowers with excellent credit may secure competitive rates, but those with limited or poor credit history often face significantly higher rates, sometimes exceeding 10%. Additionally, variable-rate private loans can increase over time, adding uncertainty to repayment.

Another key difference is the repayment flexibility offered by federal loans. Federal student loans come with income-driven repayment plans, which cap monthly payments at a percentage of the borrower's discretionary income. They also offer loan forgiveness programs, such as Public Service Loan Forgiveness (PSLF), after a certain number of qualifying payments. Private loans rarely provide such flexibility, and repayment terms are typically stricter, with fewer options for deferment or forbearance during financial hardship.

Federal loans also provide borrower protections that private loans often lack. For example, federal loans offer deferment or forbearance options for borrowers experiencing economic hardship, unemployment, or other qualifying circumstances. In contrast, private lenders may require immediate repayment regardless of the borrower's financial situation. Furthermore, federal loans do not require a credit check for most loans, making them accessible to students with limited or no credit history.

In summary, federal student loans generally have lower interest rates and more favorable terms compared to private student loans. They offer fixed rates, repayment flexibility, borrower protections, and access to forgiveness programs, making them a more affordable and secure option for most students. Private loans, while useful in certain situations, should be considered only after exhausting federal loan options, as they carry higher risks and costs. Always prioritize federal loans to minimize long-term debt and maximize financial stability.

Monthly Interest Charges: How Student Loan Companies Calculate Your Debt

You may want to see also

Explore related products

![]()

Subsidized vs. Unsubsidized Loans

When considering student loans, understanding the difference between subsidized and unsubsidized loans is crucial, especially in terms of interest rates and long-term costs. Both types of loans are part of the federal student loan program, but they differ significantly in how interest accrues and who is responsible for paying it. Subsidized loans generally offer a lower effective interest rate because the government pays the interest on the loan while the borrower is in school, during the grace period after graduation, and in certain deferment periods. This feature makes subsidized loans the more cost-effective option for eligible students.

Subsidized loans are need-based and available only to undergraduate students who demonstrate financial need. The key advantage is that the government covers the interest on these loans while the borrower is in school at least half-time, during the six-month grace period after leaving school, and during eligible deferment periods. This means the loan balance does not increase during these times, saving borrowers money in the long run. For example, if a student borrows $5,000 in subsidized loans and takes four years to complete their degree, they will still owe only $5,000 upon graduation, as no interest has accrued.

In contrast, unsubsidized loans are available to both undergraduate and graduate students, regardless of financial need. The primary drawback is that interest begins accruing on unsubsidized loans as soon as the funds are disbursed. Borrowers can choose to pay the interest while in school, during grace periods, or in deferment, but if they do not, the interest is capitalized (added to the principal balance), increasing the total amount owed. For instance, if a student borrows $5,000 in unsubsidized loans and does not pay the interest during their four years in school, the interest will compound, resulting in a higher balance upon graduation.

While both subsidized and unsubsidized loans typically have the same fixed interest rate set by the federal government, the effective interest rate for subsidized loans is lower due to the government’s interest coverage. For the 2023-2024 academic year, the interest rate for both types of loans is 5.5% for undergraduates, but the subsidized loan effectively costs less because borrowers avoid paying interest during key periods. Unsubsidized loans, however, can become more expensive over time if interest is not managed properly.

In summary, subsidized loans offer a lower effective interest rate because the government pays the interest during specific periods, making them the more affordable option for eligible borrowers. Unsubsidized loans, while accessible to more students, accrue interest immediately, which can increase the overall cost of borrowing. When deciding between the two, students should prioritize subsidized loans if they qualify, as they provide significant savings on interest and reduce the long-term financial burden of student debt.

Exploring Legal Careers: Ideal Jobs for Law-Enthusiast Students

You may want to see also

Explore related products

![]()

Fixed vs. Variable Rates

When considering student loans, one of the most critical decisions borrowers face is choosing between fixed and variable interest rates. This choice significantly impacts the total cost of the loan over time. A fixed interest rate remains the same throughout the life of the loan, providing predictability and stability in monthly payments. On the other hand, a variable interest rate fluctuates based on market conditions, which means monthly payments can increase or decrease over time. Understanding the differences between these two options is essential for making an informed decision.

Fixed interest rates are generally preferred by borrowers who value consistency and want to avoid surprises. Since the rate does not change, borrowers can easily budget for their monthly payments without worrying about sudden increases. This type of rate is often slightly higher than the initial rate offered for variable loans, but it provides long-term financial security. For example, federal student loans, such as Direct Subsidized and Unsubsidized Loans, typically offer fixed rates, which are set by the government and tend to be lower than private loan options. If you prioritize knowing exactly how much you’ll pay each month and over the life of the loan, a fixed rate is likely the better choice.

Variable interest rates, while initially lower than fixed rates, come with inherent risk. These rates are tied to a benchmark index, such as the London Interbank Offered Rate (LIBOR) or the Prime Rate, and adjust periodically based on market trends. If interest rates in the broader economy rise, so will the rate on your loan, potentially increasing your monthly payments. Conversely, if rates fall, your payments may decrease. Variable rates can be advantageous in a low-interest-rate environment, but they are less predictable and can lead to higher costs if market conditions change unfavorably. Private lenders often offer variable-rate loans, which may appeal to borrowers who plan to pay off their debt quickly or are willing to accept the risk of rate increases.

Choosing between fixed and variable rates depends on your financial situation, risk tolerance, and economic outlook. If you expect interest rates to rise, a fixed rate locks in your current rate and protects you from future increases. However, if you believe rates will remain stable or decline, a variable rate might save you money in the short term. It’s also important to consider your repayment timeline. Borrowers with a short repayment period may benefit more from a variable rate, while those with longer repayment terms might prefer the stability of a fixed rate.

In summary, fixed rates offer stability and predictability, making them ideal for borrowers who prefer consistent monthly payments and long-term planning. Variable rates, while initially lower, carry the risk of increasing payments if market conditions change. When deciding which type of student loan has a lower interest rate, it’s crucial to weigh the immediate savings of a variable rate against the potential risks. Federal loans with fixed rates often provide the lowest and most stable interest rates, while private loans may offer both fixed and variable options, allowing borrowers to choose based on their financial goals and risk tolerance.

Student Loans: Which Ones Start Accruing Interest Immediately?

You may want to see also

Explore related products

![]()

Income-Driven Repayment Plans

Income-Driven Repayment (IDR) Plans are a crucial option for federal student loan borrowers seeking lower monthly payments and potentially lower overall interest costs. These plans adjust your monthly payment based on your income and family size, often resulting in more manageable payments compared to standard repayment plans. While IDR plans themselves do not inherently offer lower interest rates, they can indirectly reduce the financial burden by capping payments at a percentage of your discretionary income. This can be particularly beneficial for borrowers with high loan balances relative to their income.

One of the key advantages of IDR plans is that they can lead to loan forgiveness after a certain period, typically 20 or 25 years, depending on the specific plan. Any remaining balance after the repayment period is forgiven, though it’s important to note that the forgiven amount may be taxable as income. This feature makes IDR plans an attractive option for borrowers who anticipate having a significant balance remaining after making consistent payments for the required period. However, it’s essential to weigh the long-term implications, such as the potential tax liability, when considering this route.

There are four main types of IDR plans: Income-Based Repayment (IBR), Pay As You Earn (PAYE), Revised Pay As You Earn (REPAYE), and Income-Contingent Repayment (ICR). Each plan has different eligibility requirements, payment calculations, and forgiveness terms. For example, PAYE and REPAYE generally cap payments at 10% of discretionary income, while IBR and ICR may have slightly higher caps. Borrowers should carefully review the specifics of each plan to determine which aligns best with their financial situation and long-term goals.

While IDR plans do not directly lower the interest rate on your loans, they can help manage interest accrual by making payments more affordable. For borrowers struggling to keep up with standard payments, IDR plans can prevent delinquency or default, which can have severe financial consequences. Additionally, some plans, like REPAYE, offer a subsidy that covers a portion of the accrued interest for subsidized loans and up to half of the accrued interest for unsubsidized loans during the first three years of repayment.

To enroll in an IDR plan, borrowers must submit an application and provide documentation of their income and family size. Annual recertification is required to ensure payments remain aligned with the borrower’s current financial situation. While IDR plans offer significant benefits, they may not be the best option for everyone, particularly those with high incomes or those who can afford standard payments. Borrowers should consider their long-term financial goals and consult resources like the Federal Student Aid website or a financial advisor to make an informed decision.

In summary, Income-Driven Repayment Plans provide a pathway to lower monthly payments and potential loan forgiveness for federal student loan borrowers. While they do not directly reduce interest rates, they can make managing student debt more feasible by aligning payments with income. By understanding the specifics of each IDR plan and their own financial circumstances, borrowers can choose the option that best supports their repayment journey.

Understanding the Current Student Plus Loan Interest Rate

You may want to see also

Explore related products

![]()

Loan Refinancing Options

When considering loan refinancing options to secure a lower interest rate on student loans, it's essential to understand the types of loans that typically offer the most favorable terms. Generally, federal student loans often have lower interest rates compared to private loans, especially for borrowers with limited credit history. However, refinancing can still be a viable strategy to reduce interest rates further, particularly if you have improved your credit score or financial standing since initially taking out the loan. Refinancing involves replacing your existing loan(s) with a new loan from a private lender, often at a lower interest rate or with better terms.

One of the primary loan refinancing options is refinancing federal student loans into a private loan. While this can potentially lower your interest rate, it’s crucial to weigh the trade-offs. Federal loans come with benefits such as income-driven repayment plans, loan forgiveness programs, and deferment or forbearance options, which are typically lost when refinancing with a private lender. If you’re confident you won’t need these federal protections, refinancing to a private loan with a lower interest rate can save you thousands of dollars over the life of the loan.

Another loan refinancing option is consolidating multiple federal loans into a single Direct Consolidation Loan. While this doesn’t inherently lower your interest rate (the new rate is a weighted average of your existing rates), it simplifies repayment by combining multiple loans into one. This can make it easier to manage payments and potentially qualify for certain repayment plans or forgiveness programs. However, consolidation is different from refinancing and may not result in a lower interest rate unless you pursue a private refinancing option afterward.

For borrowers with private student loans, refinancing is often a straightforward way to secure a lower interest rate. Private lenders compete for borrowers, so shopping around for the best rates and terms is critical. Factors such as credit score, income, and debt-to-income ratio will influence the rates you qualify for. Some lenders also offer additional perks, such as flexible repayment terms, no origination fees, or interest rate discounts for autopay. Refinancing private loans typically doesn’t involve the same trade-offs as refinancing federal loans, making it a more attractive option for many borrowers.

Lastly, variable vs. fixed interest rates play a significant role in loan refinancing options. Variable rates may start lower but can fluctuate over time, potentially increasing your monthly payments. Fixed rates remain consistent throughout the life of the loan, providing stability. When refinancing, consider your risk tolerance and financial goals. If you plan to pay off the loan quickly, a variable rate might save you money, but a fixed rate offers predictability for long-term repayment.

In summary, loan refinancing options can be a powerful tool to secure a lower interest rate on student loans, but it’s important to evaluate your specific situation. Whether refinancing federal loans into private loans, consolidating federal loans, or refinancing private loans, carefully consider the benefits, risks, and long-term financial impact. By researching lenders, comparing offers, and understanding the terms, you can make an informed decision to optimize your student loan repayment strategy.

Understanding Variable Interest Rates on Student Loans: What You Need to Know

You may want to see also

Frequently asked questions

Federal student loans generally have lower interest rates compared to private student loans.

Subsidized loans typically have lower interest rates because the government pays the interest while the borrower is in school, during the grace period, and in certain deferment periods.

Fixed-rate loans usually offer lower and more stable interest rates compared to variable-rate loans, which can fluctuate over time.

Direct Subsidized Loans and Direct Unsubsidized Loans for undergraduate students typically have the lowest interest rates among federal student loans.