The student loan interest rate is a critical factor for borrowers to consider when financing their education, and the Student Plus Loan, often part of federal or private lending programs, typically offers competitive rates designed to ease the financial burden on students and their families. As of recent updates, the interest rate for Student Plus Loans varies depending on the type of loan—Direct PLUS Loans for parents or graduate students, for instance, may have different rates compared to those for undergraduate students—and is influenced by factors such as the borrower’s credit history, loan term, and prevailing market conditions. Understanding the current interest rate is essential for borrowers to estimate monthly payments, plan repayment strategies, and make informed decisions about managing their educational debt effectively.

Explore related products

What You'll Learn

![]()

Current Federal Student Loan Rates

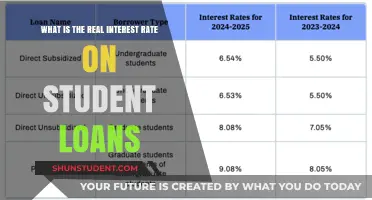

As of the most recent updates, the interest rates for federal student loans, including the Direct PLUS Loans, are set annually by the U.S. Department of Education. These rates are determined based on the 10-year Treasury note index, plus a fixed percentage, and they apply to loans first disbursed between July 1 of the current year and June 30 of the following year. For the 2023-2024 academic year, the interest rates have been adjusted to reflect the economic conditions and federal funding policies.

For Direct PLUS Loans, which are available to graduate and professional students, as well as parents of dependent undergraduate students, the current interest rate is 8.05%. This rate is higher than those for Direct Subsidized and Unsubsidized Loans for undergraduate students, which are set at 5.50%. The higher rate for PLUS Loans reflects the additional risks and costs associated with these loans, as they do not have the same borrower eligibility requirements as other federal student loans. It’s important to note that PLUS Loans also carry an origination fee, which is deducted from the loan amount before disbursement.

The 8.05% interest rate for PLUS Loans is fixed for the life of the loan, meaning it will not change over time, regardless of market fluctuations. This provides borrowers with predictability in their repayment plans. However, the fixed nature of the rate also means that borrowers do not benefit from potential decreases in market interest rates. Borrowers should carefully consider their financial situation and explore all available options, including payment plans and loan forgiveness programs, to manage their debt effectively.

When comparing the PLUS Loan interest rate to private student loan rates, it’s essential to consider factors such as borrower protections, repayment flexibility, and eligibility requirements. Federal student loans, including PLUS Loans, offer benefits like income-driven repayment plans, deferment, forbearance, and potential loan forgiveness, which are typically not available with private loans. While the interest rate for PLUS Loans may be higher than some private loan options, the added protections and flexibility often make them a more secure choice for borrowers.

Prospective borrowers should also be aware of the application process for Direct PLUS Loans, which includes a credit check. Approval is based on the absence of adverse credit history, and applicants with certain credit issues may need to secure an endorser or provide documentation of extenuating circumstances. Understanding the current interest rate and associated terms is crucial for making informed decisions about financing education through federal student loans. For the most up-to-date information, borrowers are encouraged to visit the Federal Student Aid website or consult with their school’s financial aid office.

Understanding Student Loan Interest Rates: A Comprehensive Guide for Borrowers

You may want to see also

Explore related products

![]()

Private Loan Interest Rate Comparison

When considering private student loans, one of the most critical factors to evaluate is the interest rate, as it significantly impacts the total cost of borrowing. Unlike federal student loans, which have fixed interest rates set by the government, private loan interest rates vary widely among lenders and are often based on the borrower’s creditworthiness, income, and other financial factors. For instance, while federal PLUS loans for parents and graduate students currently have a fixed interest rate of around 7.54% (as of the latest updates), private loan rates can range from as low as 3% to over 12%, depending on the lender and the borrower’s financial profile.

To effectively compare private loan interest rates, start by checking your credit score and financial history, as these will heavily influence the rates offered to you. Lenders typically provide lower interest rates to borrowers with excellent credit and stable income. Next, research multiple lenders, including banks, credit unions, and online lenders, to gather a variety of quotes. Many lenders offer pre-qualification tools that allow you to see potential interest rates without affecting your credit score. This step is crucial because even a slight difference in interest rates can save you thousands of dollars over the life of the loan.

Another key aspect of private loan interest rate comparison is understanding whether the rate is fixed or variable. Fixed rates remain the same throughout the loan term, providing predictability in monthly payments. Variable rates, on the other hand, can fluctuate based on market conditions, which may lead to lower initial rates but higher costs if interest rates rise. For example, a private loan with a variable rate starting at 4% might seem attractive compared to a federal PLUS loan’s fixed rate, but if market rates increase, the private loan could become more expensive over time.

Additionally, consider the loan terms and repayment options offered by private lenders. Some lenders provide interest rate discounts for enrolling in automatic payments or for having a co-signer with strong credit. Others may offer flexible repayment plans, such as interest-only payments while in school or deferred payment options. These features can make a private loan more affordable in the short term but should be weighed against the long-term cost of the loan. Comparing these factors alongside interest rates ensures you choose the best option for your financial situation.

Finally, while private loans may offer lower interest rates than federal PLUS loans for some borrowers, it’s essential to consider the benefits of federal loans, such as access to income-driven repayment plans, loan forgiveness programs, and deferment or forbearance options. Private loans rarely offer these protections, making them riskier if you face financial hardship. Therefore, when comparing private loan interest rates, balance the potential savings against the loss of federal loan benefits to make an informed decision. Always exhaust federal loan options before turning to private loans, as they generally provide more favorable terms and borrower protections.

Discovering New Horizons: The Most Fascinating Aspect of Student Life

You may want to see also

Explore related products

![]()

Fixed vs. Variable Rate Loans

When considering student loans, particularly the Student Plus Loan (also known as the Direct PLUS Loan in the U.S.), understanding the difference between fixed and variable interest rates is crucial. As of recent data, the interest rate for Direct PLUS Loans is fixed at 7.54% for the 2023-2024 academic year. This fixed rate means that the interest you pay on the loan remains the same throughout the life of the loan, providing predictability in your monthly payments. Fixed-rate loans are ideal for borrowers who prefer stability and want to avoid the uncertainty of fluctuating interest rates, especially in a rising interest rate environment.

On the other hand, variable-rate loans, which are less common in federal student loan programs like the Direct PLUS Loan, have interest rates that can change periodically based on market conditions. These loans are typically tied to an index, such as the London Interbank Offered Rate (LIBOR) or the Prime Rate, plus a margin. While variable rates may start lower than fixed rates, they carry the risk of increasing over time, potentially leading to higher monthly payments. For students and parents borrowing for education, this unpredictability can make financial planning more challenging.

Choosing between a fixed and variable rate depends on your risk tolerance and market outlook. Fixed-rate loans offer peace of mind, as you know exactly how much interest you’ll pay over the life of the loan. This is particularly beneficial if interest rates are expected to rise. Conversely, variable-rate loans might be advantageous if you believe interest rates will decrease, as your payments could go down. However, this option comes with the risk of higher costs if rates rise.

For Direct PLUS Loans, the fixed rate simplifies the decision-making process, as federal student loans do not offer variable-rate options. Private student loans, however, often provide both fixed and variable rate choices. If you’re considering private loans, carefully evaluate your financial situation and future interest rate projections. Fixed rates are generally recommended for long-term loans like student debt, as they protect against potential rate hikes.

In summary, the Student Plus Loan’s fixed interest rate eliminates the complexity of variable rates, making it easier for borrowers to plan their repayments. While private loans may offer variable rates that initially seem appealing, the stability of a fixed rate is often more beneficial for long-term financial planning. Always compare rates, terms, and repayment options before committing to any loan, ensuring it aligns with your financial goals and capabilities.

Understanding the Phase-Out of Student Loan Interest Deduction: What You Need to Know

You may want to see also

Explore related products

![]()

Interest Capitalization Explained

Interest capitalization is a critical concept for borrowers to understand, especially when navigating the complexities of student loans, including the Student PLUS Loan. When discussing the interest rate on a Student PLUS Loan, it’s essential to grasp how interest capitalization can significantly impact the total cost of the loan. Interest capitalization occurs when unpaid interest is added to the principal balance of the loan, increasing the total amount you owe. This process is particularly relevant for PLUS Loans, which are unsubsidized, meaning interest accrues while the borrower is in school, during grace periods, and in deferment.

For Student PLUS Loans, the interest rate is fixed and determined annually by federal regulations. As of recent data, the interest rate typically hovers around 6% to 8%, depending on the year the loan was disbursed. When interest accrues and is not paid as it accumulates, it capitalizes, becoming part of the loan’s principal. This means you’ll start paying interest on the new, larger principal balance, leading to higher overall interest costs over the life of the loan. For example, if you borrow $20,000 and $1,000 in interest accrues while you’re in school, that $1,000 is added to the principal, making your new balance $21,000.

One of the key times interest capitalization occurs is at the end of the grace period or deferment. For PLUS Loans, the grace period is typically six months after graduation or dropping below half-time enrollment. If you do not make payments on the accruing interest during this time, it will capitalize when the grace period ends. Similarly, if you defer payments due to economic hardship or other qualifying reasons, the unpaid interest will capitalize at the end of the deferment period. This can result in a substantial increase in your loan balance, making it even more challenging to repay.

To minimize the impact of interest capitalization, borrowers have a few strategies. First, paying the accruing interest while in school, during grace periods, or during deferment can prevent capitalization. Even small payments can make a difference. Second, choosing an income-driven repayment plan or exploring loan forgiveness programs can help manage the burden of a capitalized loan balance. Lastly, refinancing the PLUS Loan with a private lender may offer a lower interest rate, though this comes with the loss of federal benefits like deferment and forbearance.

Understanding interest capitalization is crucial for managing Student PLUS Loans effectively. By knowing when and how capitalization occurs, borrowers can take proactive steps to reduce its impact. While the interest rate on PLUS Loans is fixed, the total cost of the loan can escalate due to capitalization. Staying informed and exploring repayment strategies can help borrowers navigate this challenge and minimize the long-term financial burden of their student loans.

Understanding Maximum Student Loan Interest Adjustment: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Repayment Plan Rate Impact

The interest rate on a Student Plus loan, often referred to as a Grad PLUS loan or Parent PLUS loan, plays a significant role in determining the overall cost of borrowing and the repayment plan’s impact on the borrower. As of recent data, the interest rate for these loans is typically higher than that of undergraduate federal student loans, often hovering around 7% to 8% depending on the year of disbursement. This higher rate directly influences the total amount repaid over the life of the loan, making it crucial for borrowers to understand how their repayment plan interacts with this interest rate. For instance, income-driven repayment plans may lower monthly payments but extend the repayment period, allowing more interest to accrue over time. Conversely, standard repayment plans with fixed monthly payments reduce the total interest paid by shortening the loan term.

The choice of repayment plan can either mitigate or exacerbate the impact of the Student Plus loan interest rate. Standard repayment plans, which typically span 10 years, result in higher monthly payments but minimize the total interest paid because the principal is paid off more quickly. This approach is ideal for borrowers who can afford higher monthly payments and want to save on interest. However, for borrowers with limited income or high debt, income-driven repayment plans like Income-Contingent Repayment (ICR) or Pay As You Earn (PAYE) may be more suitable. These plans cap monthly payments at a percentage of discretionary income, often resulting in lower monthly payments but longer repayment terms, which means more interest accrues over time.

Another critical aspect of repayment plan rate impact is the potential for interest capitalization, particularly in income-driven plans or during periods of deferment or forbearance. When payments do not cover the accruing interest, the unpaid interest may be added to the principal balance, increasing the total amount owed. This process, known as capitalization, can significantly inflate the cost of the loan, especially with higher interest rates like those on Student Plus loans. Borrowers should carefully consider whether their repayment plan covers the accruing interest to avoid this additional financial burden.

Additionally, borrowers with Student Plus loans may benefit from exploring refinancing options, particularly if they have a stable income and good credit. Refinancing can replace the federal loan with a private loan at a lower interest rate, reducing the overall cost of repayment. However, refinancing federal loans means losing access to federal benefits like income-driven repayment plans and loan forgiveness programs. Borrowers must weigh the potential savings against the loss of these protections when considering refinancing as a strategy to manage the repayment plan rate impact.

In summary, the repayment plan chosen for a Student Plus loan has a profound impact on how the loan’s interest rate affects the borrower’s financial obligations. Higher interest rates mean that longer repayment terms result in significantly more interest paid over time, while shorter terms reduce the total cost but require higher monthly payments. Borrowers must carefully evaluate their financial situation and long-term goals to select a repayment plan that balances affordability with minimizing interest costs. Understanding these dynamics is essential for effectively managing Student Plus loan debt and avoiding unnecessary financial strain.

Understanding the Federal Student Loan Interest Paid Tax Form

You may want to see also

Frequently asked questions

The interest rate for the Student Plus Loan varies depending on the lender and the borrower's creditworthiness. As of the latest update, it typically ranges from 4.5% to 12%, but it’s best to check with your specific lender for accurate rates.

The Student Plus Loan can offer both fixed and variable interest rates. Fixed rates remain the same throughout the loan term, while variable rates may fluctuate based on market conditions.

The interest rate is typically determined based on factors such as the borrower’s credit score, income, and repayment history. A higher credit score often results in a lower interest rate.

Yes, many lenders offer discounts, such as autopay reductions (usually 0.25% to 0.50%) or loyalty discounts for existing customers, which can help lower the interest rate.

Yes, borrowers can refinance their Student Plus Loan to potentially secure a lower interest rate if their financial situation improves or market conditions change. Refinancing involves taking out a new loan to pay off the existing one.