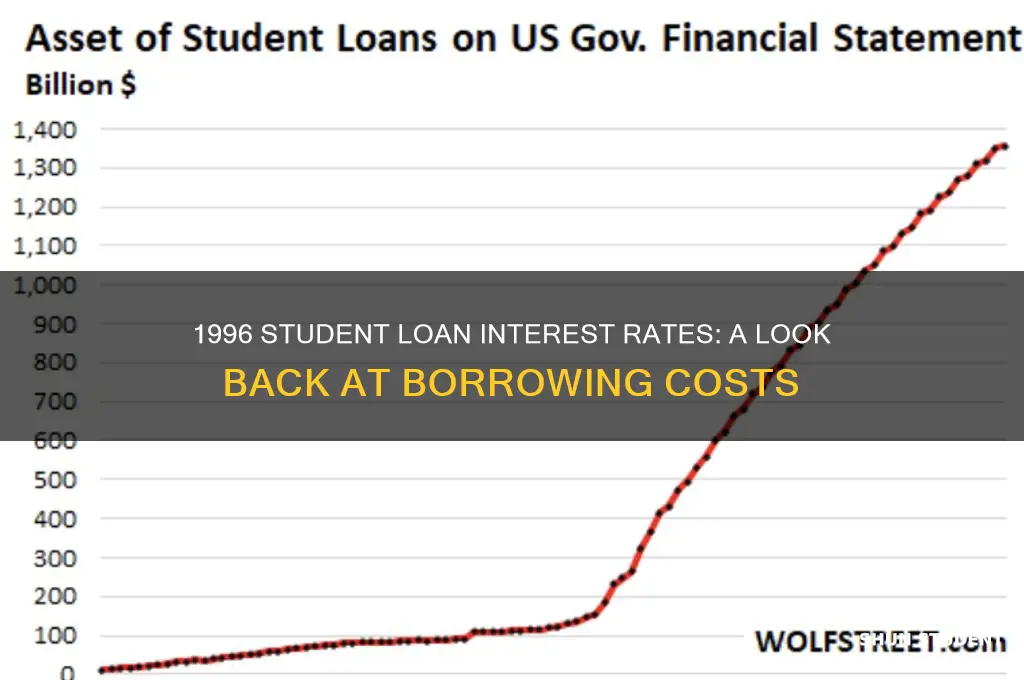

In 1996, the interest rates on student loans in the United States were influenced by federal policies and economic conditions of the time. For federal Stafford loans, which were the most common type of student loan, the interest rates were set by Congress and varied depending on the type of loan (subsidized or unsubsidized) and the borrower's enrollment status. Subsidized Stafford loans, where the government paid the interest while the student was in school, typically had lower rates compared to unsubsidized loans. During this period, interest rates generally ranged between 6% and 9%, reflecting the broader financial environment of the mid-1990s. Understanding these rates provides insight into the financial burden students faced and the evolving landscape of higher education funding during that era.

Explore related products

What You'll Learn

![]()

Historical interest rates for federal student loans in 1996

In 1996, the interest rates for federal student loans in the United States were set by the federal government and varied depending on the type of loan. The Higher Education Act of 1965, as amended, established the framework for these rates, which were designed to make higher education more accessible to students from diverse financial backgrounds. For undergraduate students, the primary federal loan program was the Federal Stafford Loan, which had a fixed interest rate for the life of the loan. During the 1996 academic year, the interest rate for subsidized Federal Stafford Loans, where the government pays the interest while the student is in school, was set at 6.12%. This rate applied to loans first disbursed on or after July 1, 1995, and before July 1, 1996.

Unsubsidized Federal Stafford Loans, which accrue interest while the student is still in school, also carried a fixed interest rate in 1996. For loans first disbursed during the same period, the interest rate was 6.12%, the same as subsidized loans. However, since unsubsidized loans begin accruing interest immediately, borrowers were responsible for paying the interest or capitalizing it, adding it to the principal balance of the loan. This distinction between subsidized and unsubsidized loans was crucial, as it directly impacted the total cost of borrowing for students and their families.

For graduate and professional students, the interest rates on federal student loans in 1996 were slightly different. The Federal Stafford Loan program for graduate students also offered both subsidized and unsubsidized loans, but the interest rates were higher than those for undergraduate students. During the 1996 academic year, the interest rate for subsidized Federal Stafford Loans for graduate students was 7.08%, while the rate for unsubsidized loans was the same. These rates reflected the higher borrowing limits available to graduate and professional students, as well as the increased earning potential associated with advanced degrees.

In addition to Federal Stafford Loans, the Federal PLUS Loan program was available to parents of dependent undergraduate students and to graduate and professional students. In 1996, the interest rate for Federal PLUS Loans was 8.25%, significantly higher than the rates for Federal Stafford Loans. This rate applied to loans first disbursed on or after October 1, 1995, and before October 1, 1996. The higher interest rate on PLUS Loans was justified by the fact that these loans had more flexible borrowing limits and did not require financial need, making them accessible to a broader range of borrowers.

It is essential to note that the interest rates for federal student loans in 1996 were established by federal legislation and were not subject to market fluctuations. This stability provided borrowers with predictability and allowed them to plan their repayment strategies effectively. However, these fixed rates also meant that borrowers did not benefit from lower interest rates during periods of economic downturn. Understanding the historical context of federal student loan interest rates, such as those in 1996, provides valuable insights into the evolution of student lending policies and their impact on borrowers' financial well-being.

Uniting Passions: The Power of Shared Interests Among Students

You may want to see also

Explore related products

![]()

Comparison of subsidized vs. unsubsidized loan rates in 1996

In 1996, the interest rates on student loans were a critical factor for borrowers, with significant differences between subsidized and unsubsidized loans. Subsidized loans, which are need-based and do not accrue interest while the borrower is in school, typically offered lower rates compared to their unsubsidized counterparts. During this period, the federal government set the interest rate for subsidized Stafford loans at a fixed rate, providing a more predictable and affordable option for eligible students. For instance, in the 1995-1996 academic year, the interest rate on subsidized Stafford loans was 6.9%, a rate that remained constant throughout the loan's life as long as the borrower met the eligibility criteria.

Unsubsidized student loans, on the other hand, were available to a broader range of borrowers, regardless of financial need. However, this accessibility came at a cost. In 1996, unsubsidized Stafford loans carried a higher interest rate, which was variable and often adjusted annually based on market conditions. For the same academic year mentioned above, the interest rate on unsubsidized Stafford loans started at 8.25%, a notable difference from the subsidized rate. This higher rate meant that borrowers with unsubsidized loans would accumulate more interest over time, especially if they chose to defer payments while in school.

The disparity in interest rates between these two loan types had long-term implications for borrowers. With subsidized loans, students could focus on their studies without the added burden of growing interest, making repayment more manageable after graduation. In contrast, unsubsidized loan borrowers often faced larger loan balances upon completing their education due to the accrual of interest during the in-school period. This difference in interest treatment could significantly impact the overall cost of education and the financial strategies borrowers needed to employ to manage their debt effectively.

Furthermore, the fixed nature of subsidized loan rates provided stability and predictability for borrowers. Students could plan their finances with a clear understanding of the interest they would be charged, allowing for better budgeting and long-term financial planning. Unsubsidized loan borrowers, however, had to contend with the uncertainty of variable rates, which could fluctuate annually, making it more challenging to estimate the total cost of their loans. This variability added a layer of complexity to financial decision-making for students and their families.

In summary, the comparison of subsidized and unsubsidized student loan rates in 1996 highlights the advantages of need-based subsidized loans, offering lower and fixed interest rates, versus the broader accessibility but higher cost of unsubsidized options. This distinction played a crucial role in shaping the financial landscape for students, influencing their borrowing choices and the subsequent management of their educational debt. Understanding these differences is essential for borrowers to make informed decisions and navigate the complexities of student loan financing.

Where to Report Student Loan Interest on Your 1040 Form

You may want to see also

Explore related products

$16.53 $22.99

![]()

Impact of 1996 interest rates on loan repayment plans

In 1996, the interest rates on student loans in the United States varied depending on the type of loan. For federally subsidized Stafford loans, the interest rate was fixed at 6.9% for loans disbursed between July 1, 1995, and June 30, 1996. Unsubsidized Stafford loans carried a variable rate, which was based on the 91-day Treasury bill rate plus a margin, typically resulting in rates around 8-9%. These rates had a significant impact on loan repayment plans, as they directly influenced the total cost of borrowing and the monthly payments borrowers would face after graduation.

The fixed 6.9% interest rate for subsidized Stafford loans in 1996 provided borrowers with predictability in their repayment plans. Since subsidized loans do not accrue interest while the borrower is in school, graduates could plan their repayment strategies knowing exactly how much interest would be added to their principal balance. This stability allowed borrowers to choose repayment plans, such as the standard 10-year plan, with a clear understanding of their monthly obligations. However, the relatively high rate compared to later years meant that borrowers paid more over the life of the loan, which could strain their finances, especially for those with large loan balances.

For unsubsidized Stafford loans, the variable interest rates in 1996 introduced uncertainty into repayment planning. Borrowers had to account for potential fluctuations in interest rates, which could increase their monthly payments and total repayment amount. This uncertainty often led borrowers to opt for income-driven repayment plans, which capped monthly payments at a percentage of their income. While these plans provided flexibility, they also extended the repayment period, resulting in more interest paid over time. The higher variable rates in 1996 exacerbated this issue, making long-term repayment more costly for borrowers with unsubsidized loans.

The 1996 interest rates also influenced borrowers' decisions regarding loan consolidation. Consolidation allowed borrowers to combine multiple loans into one, often with a fixed interest rate based on the weighted average of their existing rates. For those with a mix of subsidized and unsubsidized loans, consolidation could simplify repayment but might lock in a higher rate if variable rates were expected to decrease. Borrowers had to carefully weigh the benefits of a single monthly payment against the potential for increasing interest costs, especially given the relatively high rates in 1996.

Overall, the interest rates on student loans in 1996 had a profound impact on repayment plans by shaping borrowers' choices and financial outcomes. The fixed 6.9% rate for subsidized loans offered stability but increased the total cost of borrowing, while variable rates for unsubsidized loans introduced uncertainty and potentially higher long-term costs. These factors forced borrowers to make strategic decisions about repayment plans and consolidation, often balancing immediate affordability with long-term financial implications. Understanding the 1996 interest rates is crucial for appreciating how historical lending conditions continue to affect student loan repayment strategies today.

Where to Report Student Interest on Your 1040 Tax Form

You may want to see also

Explore related products

![]()

Legislative changes affecting student loan interest in 1996

In 1996, legislative changes significantly impacted the interest rates on student loans in the United States, reflecting broader efforts to reform the federal student loan program. One of the key pieces of legislation was the Higher Education Amendments of 1996, which built upon earlier reforms to streamline and standardize the student loan system. This law introduced changes to the Federal Family Education Loan (FFEL) Program and the William D. Ford Federal Direct Loan Program, both of which were major sources of student financing at the time. Among its provisions, the amendments aimed to simplify the loan application process and adjust interest rates to make higher education more accessible and affordable for students.

A critical aspect of the 1996 legislative changes was the variable interest rate structure for student loans. Prior to these reforms, interest rates on student loans were often fixed but differed based on the type of loan and the year of disbursement. The 1996 amendments introduced a system where interest rates were tied to the 91-day Treasury bill rate, plus a margin, with caps to protect borrowers from excessively high rates. For example, Stafford Loans, the most common type of federal student loan, saw their interest rates adjusted to reflect market conditions, with a maximum cap of 8.25% for subsidized loans and 9.0% for unsubsidized loans. This shift aimed to align student loan rates more closely with economic realities while providing a measure of predictability for borrowers.

Another important legislative change in 1996 was the expansion of loan consolidation options. The amendments allowed borrowers to consolidate their student loans at a fixed interest rate based on the weighted average of the interest rates on the loans being consolidated, capped at 8.25%. This provision was designed to help borrowers manage their debt more effectively by simplifying repayment terms and potentially lowering monthly payments. Consolidation became an attractive option for many borrowers, especially those with multiple loans at varying interest rates, as it provided a way to lock in a single, lower rate.

Additionally, the Taxpayer Relief Act of 1997, which had implications for the 1996 tax year, introduced tax benefits related to student loan interest. Although enacted in 1997, its effects were felt in 1996 as borrowers began to anticipate the deduction. This act allowed taxpayers to deduct up to $1,000 in student loan interest payments from their taxable income, providing financial relief for borrowers. While not a direct change to interest rates, this tax benefit effectively reduced the overall cost of borrowing for many students and their families.

In summary, the legislative changes affecting student loan interest in 1996 were part of a broader effort to reform the federal student loan system. By introducing variable interest rates tied to market conditions, expanding loan consolidation options, and providing tax benefits, these reforms aimed to make higher education more affordable and manageable for borrowers. While the changes did not eliminate the financial burden of student loans, they represented significant steps toward addressing the growing concerns about student debt in the United States.

Navigating Student Loan Interest: Smart Choices for the Marketplace

You may want to see also

Explore related products

![]()

Private vs. federal student loan interest rates in 1996

In 1996, the landscape of student loan interest rates was significantly different from what it is today, with distinct variations between private and federal student loans. Federal student loans, which are backed by the government, offered borrowers more favorable terms compared to their private counterparts. The interest rates for federal student loans in 1996 were generally lower and often fixed, providing a sense of stability for borrowers. For instance, the Federal Family Education Loan (FFEL) Program, which was a major source of federal student loans at the time, had interest rates that were capped by the government, ensuring that they remained relatively low. These rates typically ranged from 6% to 9%, depending on the type of loan and the year of disbursement.

Private student loans, on the other hand, presented a different scenario. Lenders offering private student loans had more flexibility in setting interest rates, which often resulted in higher costs for borrowers. In 1996, private loan interest rates could vary widely, with some lenders charging rates significantly above those of federal loans. These rates were often variable, meaning they could fluctuate over the life of the loan, adding an element of uncertainty for students and their families. Private lenders based their rates on various factors, including the borrower's credit history, which many students lacked, leading to less favorable terms.

One of the key advantages of federal student loans in 1996 was the availability of subsidized loans. Subsidized federal loans offered a unique benefit where the government paid the interest on the loan while the borrower was in school, during the grace period after graduation, and in certain deferment periods. This feature was not typically available with private loans, making federal loans even more attractive for students from lower-income backgrounds. The interest rates on subsidized federal loans were also generally lower, providing additional financial relief.

The difference in interest rates between private and federal student loans in 1996 had long-term implications for borrowers. Federal loans, with their lower and fixed rates, allowed students to plan their finances more effectively, knowing that their repayment amounts would remain relatively stable. Private loans, with higher and variable rates, could lead to increased financial burden, especially if market interest rates rose over time. This disparity highlighted the importance of understanding the terms and conditions of each loan type before borrowing.

When considering the interest rates of 1996, it's evident that federal student loans provided a more secure and affordable option for borrowers. The government's involvement in setting and capping interest rates ensured that students had access to education funding without being subjected to potentially predatory lending practices. Private student loans, while offering more flexibility in terms of borrowing limits, came with higher financial risks due to their interest rate structures. This comparison underscores the need for students and their families to carefully evaluate their loan options, considering both the immediate and long-term financial implications.

Understanding Maximum Student Loan Interest Adjustment: A Comprehensive Guide

You may want to see also

Frequently asked questions

In 1996, the interest rate on federal Stafford loans for undergraduate students was 8.25% for new loans, while the rate for consolidation loans varied depending on the weighted average of the underlying loans.

Yes, the interest rates on federal student loans in 1996 were lower than in some previous years. For example, in 1992, the rate was as high as 9.0%. The rates gradually decreased in the mid-1990s due to changes in federal legislation.

No, private student loan interest rates in 1996 were typically higher than federal rates and varied widely based on the borrower's creditworthiness and the lender's terms. Federal loans offered fixed rates, while private loans often had variable rates tied to market conditions.