The maximum adjustment for student loan interest is a critical aspect of managing educational debt, as it directly impacts the overall cost of repayment. This adjustment, often referred to as an interest rate reduction or discount, is typically offered by lenders as an incentive for borrowers who demonstrate consistent on-time payments or enroll in automatic debit programs. For federal student loans, the maximum adjustment can vary depending on the type of loan and the repayment plan, with some programs offering up to 0.25% reduction in interest rates. Private lenders may provide similar or even larger reductions, but these offers often come with specific eligibility criteria. Understanding the maximum adjustment available can help borrowers save significantly over the life of their loans, making it essential to explore all options and stay informed about potential benefits.

| Characteristics | Values |

|---|---|

| Maximum Interest Rate Adjustment | 0.25% (25 basis points) |

| Eligibility Requirement | Enroll in automatic payments (auto-debit) for federal student loans |

| Loan Types Covered | Direct Loans, Federal Family Education Loan (FFEL) Program loans |

| Application Process | Automatic upon enrollment in auto-debit; no separate application needed |

| Duration of Adjustment | Applies for the life of the loan as long as auto-debit is active |

| Impact on Monthly Payments | Slightly reduces monthly payments due to lower interest accrual |

| Reversibility | Adjustment is lost if auto-debit is discontinued |

| Tax Implications | Interest paid may be tax-deductible, but the adjustment itself is not |

| Frequency of Adjustment | Applied monthly to the loan balance |

| Availability for Private Loans | Not applicable; only for federal student loans |

Explore related products

What You'll Learn

- Federal vs. Private Loan Limits: Compare interest adjustment caps for federal and private student loans

- Income-Driven Repayment Plans: How income-based plans affect maximum interest adjustments

- Loan Refinancing Impact: Refinancing’s role in altering maximum interest adjustment possibilities

- Tax Deduction Limits: Maximum interest deduction allowed for student loan payments

- Temporary Relief Programs: Government or lender programs offering temporary interest adjustments

![]()

Federal vs. Private Loan Limits: Compare interest adjustment caps for federal and private student loans

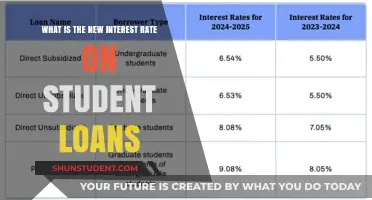

When comparing federal and private student loans, one critical aspect to consider is the maximum adjustment for student loan interest, often referred to as interest rate caps. These caps determine the highest possible interest rate a borrower may face over the life of the loan. Federal student loans, backed by the U.S. Department of Education, typically offer more borrower protections and standardized terms, including fixed interest rates that are set by Congress annually. For federal loans, the interest rates are generally lower and more predictable compared to private loans. For example, as of recent data, undergraduate Direct Subsidized and Unsubsidized Loans have a fixed interest rate of around 5.5% for the 2023-2024 academic year, with no adjustment beyond this rate unless Congress enacts new legislation.

Private student loans, on the other hand, are offered by banks, credit unions, and other financial institutions, and their interest rates can vary widely based on the borrower’s creditworthiness, market conditions, and the lender’s policies. Unlike federal loans, private loans often come with variable interest rates, which means the rate can fluctuate over time based on an index like the LIBOR or Prime Rate. While some private lenders may offer initial rates that are competitive with or even lower than federal rates, the maximum adjustment for interest on private loans can be significantly higher. For instance, variable rates on private loans can sometimes reach upwards of 12% to 15% or more, depending on market conditions and the borrower’s credit profile.

One key difference in interest adjustment caps between federal and private loans lies in the absence of a legal maximum for private loans. Federal loans have statutory limits set by Congress, ensuring borrowers are protected from exorbitant rate increases. Private loans, however, are subject to the terms agreed upon in the loan contract, which may include high caps or no caps at all. This lack of regulation can expose borrowers to financial risk if interest rates rise sharply. Some private lenders may offer interest rate caps as part of their loan terms, but these are not standardized and vary widely across lenders.

Another important factor is the availability of interest rate reductions or adjustments through benefits like auto-pay discounts or loyalty programs. Federal loans occasionally offer incentives such as a 0.25% interest rate reduction for enrolling in automatic payments, but these adjustments are modest and do not change the fundamental cap on interest rates. Private lenders, however, may provide more substantial rate reductions for similar actions, though these discounts are often temporary and do not alter the maximum potential interest rate outlined in the loan agreement.

In summary, when comparing federal and private student loan limits, federal loans provide greater stability and protection through fixed interest rates and statutory caps, while private loans offer less predictability due to variable rates and higher potential maximum adjustments. Borrowers should carefully review the terms of private loans to understand their exposure to interest rate increases and consider federal loans as a more secure option for managing long-term repayment obligations. Understanding these differences is essential for making informed decisions about student loan borrowing.

Maximize Your Deduction: Understanding State Student Loan Interest Limits

You may want to see also

Explore related products

![]()

Income-Driven Repayment Plans: How income-based plans affect maximum interest adjustments

Income-Driven Repayment (IDR) plans are designed to make federal student loan payments more manageable by capping monthly payments based on the borrower’s income and family size. These plans also play a significant role in determining the maximum adjustment for student loan interest. Under IDR plans, if the calculated monthly payment is less than the accrued interest, the government may cover a portion of the unpaid interest, effectively acting as an interest adjustment. This subsidy varies depending on the specific IDR plan and the borrower’s financial situation. For example, in the Revised Pay As You Earn Repayment Plan (REPAYE Plan), the government pays 100% of unpaid interest on subsidized loans for the first three years and 50% thereafter, while for unsubsidized loans, it covers 50% of unpaid interest. This mechanism ensures that interest does not capitalize and add to the loan balance, providing a form of maximum interest adjustment tied to the borrower’s income level.

The Pay As You Earn Repayment Plan (PAYE Plan) and the Income-Based Repayment Plan (IBR Plan) also offer interest adjustments, though the terms differ. Under PAYE, the government covers 50% of unpaid interest, preventing it from capitalizing. Similarly, IBR provides interest subsidies, but the specifics depend on whether the borrower is a new or existing borrower as of July 1, 2014. These adjustments are directly tied to the borrower’s income, as lower income levels result in lower monthly payments, which in turn trigger the need for interest subsidies. Thus, IDR plans effectively create a dynamic maximum interest adjustment based on the borrower’s financial circumstances, ensuring that interest does not overwhelm the borrower.

The Income-Contingent Repayment Plan (ICR Plan) operates slightly differently. While it does not offer the same level of interest subsidies as other IDR plans, it still provides a form of maximum interest adjustment by capping monthly payments at 20% of discretionary income. If the borrower’s payment is insufficient to cover the accruing interest, the unpaid interest may capitalize, but the overall payment structure is still income-driven. This means that the effective interest adjustment is tied to the borrower’s ability to pay, as higher income levels would result in payments that cover more of the interest, while lower income levels would necessitate a greater adjustment.

It’s important to note that the maximum interest adjustment under IDR plans is not a fixed amount but rather a function of the borrower’s income and the specific plan terms. Borrowers with very low incomes may receive significant interest subsidies, effectively maximizing the adjustment, while those with higher incomes may receive little to no subsidy. This income-based approach ensures that the interest adjustment is tailored to the borrower’s financial reality, making student loan repayment more sustainable. However, borrowers must recertify their income and family size annually to maintain eligibility for these adjustments, as changes in income can alter the subsidy amount.

In summary, Income-Driven Repayment plans directly influence the maximum adjustment for student loan interest by tying interest subsidies to the borrower’s income level. Plans like REPAYE, PAYE, and IBR offer explicit interest subsidies, while ICR provides a more indirect adjustment through income-based payment caps. These mechanisms ensure that interest does not compound uncontrollably, offering borrowers a measure of financial protection. Understanding how IDR plans affect interest adjustments is crucial for borrowers seeking to manage their student loan debt effectively, as it highlights the importance of selecting the right plan based on their income and long-term financial goals.

Explore related products

![]()

Loan Refinancing Impact: Refinancing’s role in altering maximum interest adjustment possibilities

Loan refinancing plays a pivotal role in altering the maximum interest adjustment possibilities for student loans, offering borrowers a strategic tool to manage their debt more effectively. When a borrower refinances their student loans, they essentially replace their existing loans with a new one, often from a private lender, at a potentially lower interest rate. This process can directly impact the maximum adjustment for student loan interest by providing an opportunity to secure a fixed or variable rate that is more favorable than the original terms. For instance, if a borrower’s original loan had a high interest rate due to market conditions or creditworthiness at the time of borrowing, refinancing allows them to capitalize on improved financial circumstances or a better credit score to lock in a lower rate. This reduction in interest rate effectively lowers the maximum interest adjustment, as the borrower is no longer subject to the higher rates of their previous loan.

One of the key ways refinancing impacts maximum interest adjustment is by eliminating the constraints of federal loan programs. Federal student loans often come with standardized interest rates set by the government, which may not always be the most competitive. By refinancing with a private lender, borrowers can access rates that are tailored to their current financial profile, potentially reducing the overall interest burden. Additionally, private refinanced loans may offer more flexibility in repayment terms, such as shorter or longer repayment periods, which can further influence the total interest paid over the life of the loan. This flexibility allows borrowers to choose terms that align with their financial goals, thereby indirectly affecting the maximum interest adjustment by optimizing their repayment strategy.

Another critical aspect of refinancing is its ability to consolidate multiple loans into a single loan with a unified interest rate. For borrowers with multiple student loans, each carrying its own interest rate, refinancing can simplify their debt structure and potentially lower the weighted average interest rate. This consolidation not only makes repayment more manageable but also reduces the maximum interest adjustment by eliminating the highest rates among the original loans. For example, if a borrower has one loan at 7% and another at 9%, refinancing both into a single loan at 6.5% would significantly decrease the overall interest burden.

However, it’s important to note that refinancing federal student loans with a private lender can limit access to certain federal benefits, such as income-driven repayment plans, loan forgiveness programs, and interest rate adjustments tied to federal policies. These programs often provide mechanisms for reducing interest payments or adjusting rates based on financial hardship, which could otherwise serve as a form of maximum interest adjustment. Borrowers must carefully weigh the benefits of lower interest rates through refinancing against the potential loss of these federal protections. In some cases, the reduction in interest rates achieved through refinancing may outweigh the value of federal benefits, but this depends on individual financial circumstances and long-term goals.

In conclusion, loan refinancing is a powerful mechanism for altering the maximum interest adjustment possibilities for student loans. By securing lower interest rates, consolidating multiple loans, and customizing repayment terms, borrowers can significantly reduce their overall interest burden. However, the decision to refinance must be made with a clear understanding of the trade-offs involved, particularly when transitioning from federal to private loans. When executed strategically, refinancing can provide substantial financial relief and empower borrowers to take control of their student debt in a way that aligns with their long-term financial objectives.

Explore related products

![]()

Tax Deduction Limits: Maximum interest deduction allowed for student loan payments

The Tax Deduction Limits for student loan interest payments are an essential aspect of financial planning for borrowers, offering a potential reduction in taxable income. When it comes to maximizing your tax benefits, understanding the rules around the maximum interest deduction is crucial. The Internal Revenue Service (IRS) allows taxpayers to deduct a certain amount of student loan interest paid during the tax year, providing some financial relief to those managing educational debt. This deduction can be claimed as an adjustment to income, even if you don't itemize your deductions.

For the tax year 2023, the maximum amount of student loan interest that can be deducted is $2,500. This limit applies to qualified education loans used to pay for tuition, fees, and other necessary expenses for the taxpayer, their spouse, or their dependents. It's important to note that this deduction is gradually reduced (phased out) for taxpayers with higher incomes. The phase-out begins for taxpayers with a modified adjusted gross income (MAGI) of $70,000 ($140,000 for joint returns) and is completely phased out for taxpayers with a MAGI of $85,000 or more ($170,000 or more for joint returns).

To qualify for this deduction, the student loan must have been taken out solely to pay for qualified higher education expenses, including tuition, fees, books, supplies, and equipment required for enrollment or attendance. Room and board, insurance, and transportation costs are generally not considered qualified expenses for this deduction. Additionally, the loan must have been used for the taxpayer, their spouse, or a dependent, and the student must have been enrolled at least half-time in a degree, certificate, or other recognized credential program.

It's worth mentioning that the student loan interest deduction is an above-the-line deduction, meaning it can be claimed regardless of whether you itemize your deductions or take the standard deduction. This makes it a valuable tax benefit for many borrowers. However, if you are married and file separately, you cannot claim this deduction. Proper documentation is essential when claiming this deduction, so borrowers should keep records of their loan statements and payments to ensure they can provide evidence of the interest paid if required by the IRS.

Understanding these tax deduction limits can help student loan borrowers optimize their tax strategy. By staying informed about the maximum interest deduction allowed, borrowers can make informed decisions to minimize their tax liability and potentially increase their tax refunds. It is always advisable to consult a tax professional or refer to the latest IRS guidelines for the most accurate and up-to-date information regarding student loan interest deductions.

Explore related products

![]()

Temporary Relief Programs: Government or lender programs offering temporary interest adjustments

In response to economic hardships or unforeseen circumstances, both government and private lenders often introduce temporary relief programs aimed at easing the financial burden on student loan borrowers. These programs typically involve temporary interest adjustments, which can significantly reduce monthly payments and overall loan costs. One of the most well-known examples is the interest rate reduction during the COVID-19 pandemic, where the U.S. Department of Education set federal student loan interest rates to 0% for a specified period. This measure provided immediate relief to millions of borrowers, allowing them to pause payments without accruing additional interest.

Another example of temporary interest adjustments is the economic hardship deferment or forbearance programs offered by both federal and private lenders. During periods of unemployment, underemployment, or financial distress, borrowers may qualify for reduced or zero interest on their loans for a limited time. For federal loans, the government may cover the interest on subsidized loans during deferment, preventing balance growth. Private lenders, while not obligated to offer such benefits, often provide forbearance options with temporary interest rate reductions to retain borrowers and avoid defaults.

Some lenders also introduce disaster relief programs in the aftermath of natural disasters or regional crises. For instance, borrowers affected by hurricanes, wildfires, or other catastrophic events may be eligible for temporary interest waivers or reductions. These programs are typically announced by the Department of Education or private lenders and require borrowers to apply for relief by providing proof of their situation. The maximum adjustment in these cases often involves a complete suspension of interest accrual for a defined period, such as 3 to 12 months.

In addition to federal initiatives, state-sponsored programs occasionally offer temporary interest adjustments for student loans. These programs are often targeted at specific demographics, such as public servants, teachers, or healthcare workers, and may include interest rate caps or reductions for a limited time. For example, some states have implemented programs that reduce interest rates to as low as 1% for borrowers working in high-need fields during declared emergencies.

Borrowers should actively monitor announcements from the Department of Education, their loan servicers, and financial news sources to stay informed about available temporary relief programs. While these adjustments are not permanent, they can provide critical breathing room during challenging times. It’s important to note that the maximum adjustment for student loan interest under these programs varies widely depending on the program’s terms, the borrower’s eligibility, and the duration of the relief offered. Always review the specific conditions of each program to understand how much interest relief you may qualify for.

Frequently asked questions

The maximum adjustment for student loan interest depends on the type of loan and repayment plan. For example, under income-driven repayment plans, interest capitalization is limited to 10% of the original loan balance.

No, the maximum adjustment varies by loan type. Federal loans under income-driven plans have specific caps, while private loans may have different terms based on the lender’s policies.

The maximum adjustment can limit the amount of interest added to the loan balance, potentially reducing monthly payments under certain repayment plans, especially income-driven ones.

In some cases, additional interest subsidies or waivers may apply, such as through Public Service Loan Forgiveness (PSLF) or temporary relief programs, but these are not automatic and require specific eligibility.