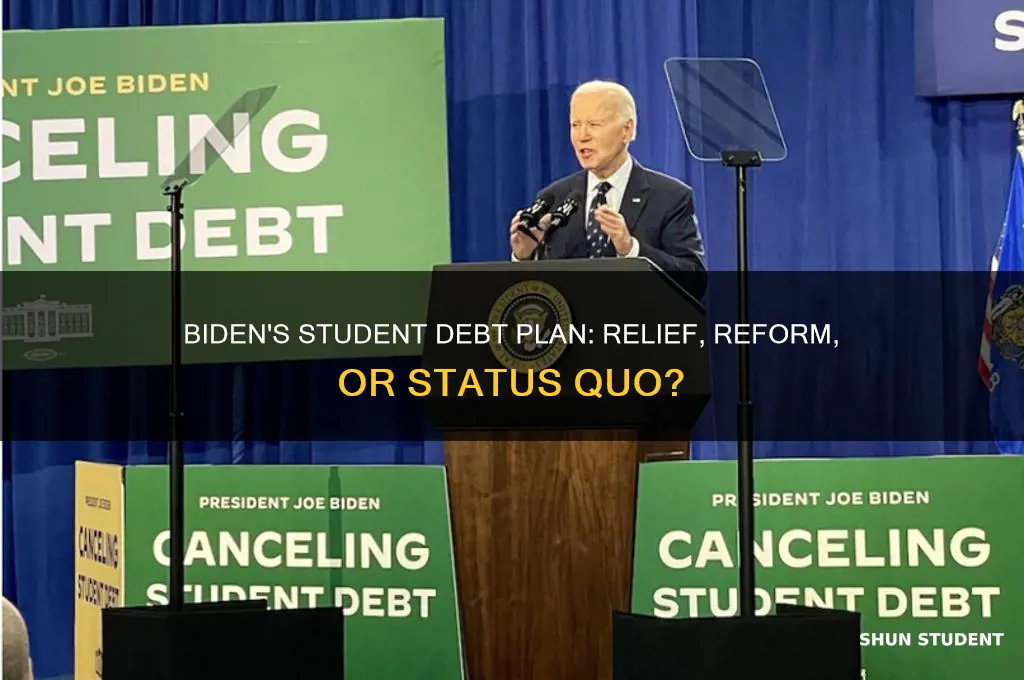

As the issue of student debt continues to burden millions of Americans, many are eagerly awaiting President Biden's next move to address this growing crisis. With over $1.7 trillion in outstanding student loan debt, borrowers are struggling to make ends meet, and the economic consequences are far-reaching. During his presidential campaign, Biden promised to tackle this issue head-on, proposing various solutions such as debt forgiveness, income-driven repayment plans, and increased funding for education. Now, as he navigates the complexities of the presidency, the question remains: what concrete actions will Biden take to alleviate the student debt burden, and how will these measures impact borrowers, the economy, and the future of higher education in the United States?

| Characteristics | Values |

|---|---|

| Debt Cancellation | Up to $20,000 in debt cancellation for Pell Grant recipients; up to $10,000 for non-Pell Grant recipients (income-capped at $125,000 for individuals and $250,000 for married couples). |

| Income-Driven Repayment (IDR) Reform | Proposed changes to IDR plans to reduce monthly payments to 5% of discretionary income (down from 10%) and forgive remaining balances after 10 years for borrowers with $12,000 or less in loans. |

| Public Service Loan Forgiveness (PSLF) | Streamlined PSLF application process and temporary waivers to help more borrowers qualify for forgiveness. |

| Pause on Student Loan Payments | Extended the pause on federal student loan payments and interest accrual until October 1, 2023 (as of latest updates). |

| Legal Challenges | Facing lawsuits challenging the debt cancellation plan, with the Supreme Court hearing arguments in February 2023. Outcome pending. |

| Targeted Relief | Additional relief for borrowers with disabilities, defrauded students, and those in default. |

| Long-Term Reforms | Proposals to increase Pell Grants, reduce college costs, and hold colleges accountable for student outcomes. |

| Eligibility Criteria | Borrowers must have federally held loans (not private loans) and meet income thresholds for cancellation. |

| Implementation Status | Debt cancellation on hold due to legal challenges; other reforms (e.g., IDR, PSLF) in progress. |

| Estimated Cost | Approximately $400 billion for the debt cancellation plan. |

| Political Opposition | Facing opposition from Republicans and legal challenges arguing the plan exceeds presidential authority. |

Explore related products

What You'll Learn

- Loan Forgiveness Plans: Potential expansion of existing programs or new initiatives for widespread debt cancellation

- Income-Driven Repayment: Reforms to make repayment plans more affordable and accessible for borrowers

- Public Service Loan Forgiveness: Enhancements to streamline and expand eligibility for public service workers

- Interest Rate Reductions: Proposals to lower or cap interest rates on federal student loans

- Accountability for Colleges: Measures to hold institutions accountable for student debt and outcomes

![]()

Loan Forgiveness Plans: Potential expansion of existing programs or new initiatives for widespread debt cancellation

The Biden administration has already taken steps to address the student debt crisis, but the question remains: will there be a broader, more transformative approach to loan forgiveness? One potential avenue is the expansion of existing programs, such as Public Service Loan Forgiveness (PSLF) and income-driven repayment (IDR) plans. By lowering the eligibility requirements and streamlining the application process for PSLF, more borrowers who dedicate their careers to public service could see their debts canceled after 10 years of qualifying payments. For instance, reducing the necessary number of payments from 120 to 90 could provide faster relief, especially for those in lower-paying public sector jobs.

Another strategy could involve creating new initiatives for widespread debt cancellation, targeting specific demographics or debt thresholds. For example, a one-time cancellation of $10,000 to $50,000 in federal student loans for borrowers earning below a certain income level could provide immediate financial relief. This approach, often discussed in policy circles, would require careful consideration of equity and fiscal responsibility. Pairing such a plan with reforms to prevent future debt accumulation, like increasing Pell Grant amounts or lowering interest rates, could address both the symptom and the root cause of the crisis.

Critics argue that broad cancellation could be regressive, benefiting higher-earning borrowers disproportionately. To counter this, the administration might consider a means-tested approach, where forgiveness is capped based on income or debt-to-income ratios. For example, borrowers with incomes below $50,000 could receive full cancellation, while those earning between $50,000 and $100,000 might receive partial relief. This tiered system would ensure that the most vulnerable borrowers receive the greatest benefit.

Implementing these changes would require legislative action or executive authority, depending on the scope. While executive action could provide quicker relief, it may face legal challenges. Legislation, though slower, would offer more permanent solutions. Borrowers should stay informed about policy updates and prepare necessary documentation, such as employment certification for PSLF or income verification for IDR plans, to maximize their chances of benefiting from any new initiatives.

Ultimately, the expansion of loan forgiveness programs or the introduction of new initiatives could significantly alleviate the burden of student debt for millions of Americans. By combining targeted relief with systemic reforms, the Biden administration has the opportunity to create a more equitable and sustainable higher education financing system. Borrowers should remain engaged with advocacy efforts and policy developments to ensure their voices are heard in this critical conversation.

College Ave Student Loans: Direct Bank Account Disbursement Explained

You may want to see also

Explore related products

![]()

Income-Driven Repayment: Reforms to make repayment plans more affordable and accessible for borrowers

One of the most pressing issues for student loan borrowers is the burden of monthly payments that often exceed their financial capacity. Income-Driven Repayment (IDR) plans, which cap monthly payments based on income and family size, are designed to alleviate this strain. However, these plans are not without flaws. Biden’s administration has signaled a commitment to reforming IDR to make it more affordable and accessible, addressing both the complexity of enrollment and the long-term financial viability for borrowers. By simplifying the application process and reducing payment thresholds, these reforms aim to ensure that borrowers can manage their debt without sacrificing their financial stability.

Consider the current challenges: borrowers often struggle to navigate the IDR application process, which requires annual recertification of income and family size. This bureaucratic hurdle can lead to missed deadlines, payment increases, or even default. Biden’s proposed reforms include streamlining this process by allowing automatic income verification through the IRS, eliminating the need for manual paperwork. For example, if a borrower earns $40,000 annually with a family of three, their payment under a reformed IDR plan might be capped at 8% of their discretionary income, rather than the current 10-15%, reducing their monthly obligation from $300 to $200. This not only makes payments more manageable but also reduces the risk of default.

Another critical aspect of IDR reform is addressing the long-term implications of these plans. Under current rules, any remaining balance after 20-25 years of payments is forgiven, but the forgiven amount is treated as taxable income. This can result in a significant tax liability for borrowers, undermining the intended relief. Biden’s reforms propose eliminating this tax burden, ensuring that loan forgiveness under IDR plans is truly debt-free. For instance, a borrower with $50,000 in remaining debt after 20 years of payments would save approximately $10,000 in taxes under this reform, providing a substantial financial benefit.

To maximize the impact of these reforms, borrowers should take proactive steps. First, stay informed about policy changes by subscribing to updates from the Department of Education or trusted financial news sources. Second, if currently enrolled in an IDR plan, ensure timely recertification until automatic verification is implemented. Third, consider refinancing private loans separately, as they are not eligible for federal IDR plans or forgiveness programs. Finally, maintain detailed records of payments and correspondence with loan servicers to protect against administrative errors.

In conclusion, Biden’s proposed reforms to Income-Driven Repayment plans represent a significant step toward making student loan repayment more equitable and manageable. By simplifying enrollment, reducing payment thresholds, and eliminating tax penalties on forgiven debt, these changes address both immediate and long-term challenges faced by borrowers. While the reforms are not yet fully implemented, understanding their potential impact and taking proactive measures can help borrowers navigate their student debt with greater confidence and financial security.

Clergy and Student Loan Forgiveness: Eligibility and Options Explained

You may want to see also

Explore related products

![]()

Public Service Loan Forgiveness: Enhancements to streamline and expand eligibility for public service workers

Public service workers, from teachers to nurses, often carry significant student debt while earning modest salaries. Recognizing this, the Biden administration has prioritized enhancing the Public Service Loan Forgiveness (PSLF) program to make it more accessible and user-friendly. These enhancements aim to streamline the application process, expand eligibility criteria, and ensure that more public servants can benefit from debt relief. By addressing long-standing issues with the program, the administration seeks to fulfill its promise of supporting those who dedicate their careers to serving the public good.

One key enhancement is the temporary waiver introduced in 2021, which allowed past payments on any federal loan type and repayment plan to qualify for PSLF. This waiver, extended through October 31, 2023, provided a lifeline for borrowers who had been excluded due to technicalities, such as having Federal Family Education Loans (FFEL) or being on the wrong repayment plan. For example, a social worker with 10 years of payments on an FFEL loan could now have those years count toward forgiveness, provided they consolidated into a Direct Loan and certified their employment by the deadline. This measure alone has the potential to erase billions in debt for eligible borrowers.

Another critical improvement is the simplification of the PSLF application process. Historically, the program has been criticized for its complexity, with many borrowers denied forgiveness due to paperwork errors or confusion about eligibility requirements. The Biden administration has introduced a more intuitive online tool and clearer guidance, reducing barriers for applicants. For instance, public service workers can now submit their employment certification form electronically, eliminating the need for manual processing and reducing the risk of errors. This shift not only saves time but also increases the likelihood of approval for qualified borrowers.

Expanding eligibility is also a cornerstone of these enhancements. Previously, only Direct Loans were eligible for PSLF, leaving out borrowers with other federal loan types. The administration has addressed this by allowing borrowers to consolidate ineligible loans into Direct Loans, making them eligible for forgiveness. Additionally, part-time workers in public service roles are now included, provided they meet the hourly equivalent of full-time work. This change benefits individuals like adjunct professors or part-time firefighters, who previously fell through the cracks despite their contributions to society.

While these enhancements represent significant progress, borrowers must take proactive steps to maximize their benefits. First, consolidate any non-Direct Loans into a Direct Consolidation Loan to ensure all payments qualify. Second, submit the PSLF Help Tool or Employment Certification Form annually to track qualifying payments. Third, enroll in an income-driven repayment plan to lower monthly payments and align with PSLF requirements. Finally, stay informed about deadlines, particularly for the temporary waiver, to avoid missing out on this limited-time opportunity. By leveraging these enhancements, public service workers can finally achieve the debt relief they deserve.

Student Loan Forgiveness Reimbursement: What Borrowers Need to Know

You may want to see also

Explore related products

![]()

Interest Rate Reductions: Proposals to lower or cap interest rates on federal student loans

Federal student loan interest rates have long been a burden for borrowers, often compounding the challenge of repayment. Proposals to lower or cap these rates aim to provide immediate relief and long-term financial stability. For instance, the Biden administration has explored reducing interest rates to reflect current economic conditions, such as tying them to the 10-year Treasury note plus a minimal margin. This approach would ensure rates remain fair and responsive to market fluctuations, preventing borrowers from being locked into high rates during periods of low inflation.

Analyzing the impact, a 1% reduction in interest rates could save the average borrower thousands of dollars over the life of their loan. For example, a borrower with a $30,000 loan at 6% interest would pay approximately $9,900 in interest over 10 years. Lowering the rate to 5% would reduce that amount to $8,000, freeing up $1,900 for other financial priorities. Such savings could be particularly transformative for low-income borrowers, who often struggle disproportionately with loan repayment.

Implementing interest rate reductions requires careful consideration of potential drawbacks. Critics argue that lowering rates could reduce revenue for federal loan programs, which fund other education initiatives. To mitigate this, policymakers could introduce targeted caps, such as applying lower rates only to undergraduate loans or setting income-based thresholds. Additionally, pairing rate reductions with incentives for on-time payments could encourage responsible borrowing behavior while maintaining program sustainability.

Persuasively, capping interest rates aligns with broader efforts to make higher education more accessible and equitable. High interest rates often deter students from pursuing degrees, particularly those from underserved communities. By capping rates at, say, 3% for all federal loans, the Biden administration could signal a commitment to reducing financial barriers to education. This move would not only benefit individual borrowers but also stimulate economic growth by enabling more graduates to invest in homes, businesses, and communities.

In practice, borrowers can prepare for potential rate reductions by staying informed about legislative updates and exploring current options like income-driven repayment plans. Advocacy groups and financial advisors can play a role in educating borrowers about the implications of lower rates and how to maximize their benefits. Ultimately, interest rate reductions represent a pragmatic step toward alleviating the student debt crisis, offering both immediate relief and a pathway to long-term financial security.

Understanding Federal Student Loan Interest Rates: What to Expect

You may want to see also

Explore related products

![]()

Accountability for Colleges: Measures to hold institutions accountable for student debt and outcomes

Colleges often escape scrutiny for their role in the student debt crisis, despite their influence on borrowing and outcomes. Biden’s administration has signaled a shift toward holding institutions accountable, not just borrowers. One proposed measure is tying federal funding to graduation rates, loan repayment rates, and post-graduation earnings. For instance, schools with consistently low outcomes could face reduced access to federal student aid programs, forcing them to improve or risk financial instability. This approach mirrors the "risk-sharing" model, where institutions share the burden of defaulted loans, incentivizing better support systems and career preparation.

Another strategy involves increasing transparency through standardized data reporting. Currently, students struggle to compare institutions based on debt loads, graduation rates, and employment outcomes. Biden’s plan could mandate colleges to publish clear, accessible data on these metrics, allowing students to make informed decisions. For example, a dashboard could show the average debt of graduates from a specific program alongside their median salary five years post-graduation. Such transparency would pressure underperforming schools to improve or lose prospective students to competitors with better records.

Accountability also extends to for-profit colleges, which have historically saddled students with high debt and poor outcomes. The Biden administration has revived the "gainful employment" rule, requiring career programs to meet debt-to-earnings thresholds to qualify for federal aid. Programs failing this metric would lose funding, effectively shuttering those that exploit students. This measure protects borrowers by eliminating predatory options and encouraging all institutions to prioritize student success over profit.

Finally, accountability requires addressing the root causes of rising tuition. Biden’s plan could cap tuition increases at public colleges, linking them to inflation or state funding levels. Simultaneously, institutions could be required to reinvest a portion of endowment or tuition revenue into financial aid, reducing reliance on loans. For private colleges, a "tuition transparency" rule might mandate clear breakdowns of costs and aid, discouraging excessive price hikes. These steps would curb institutional behavior that exacerbates debt while ensuring colleges remain accessible.

By implementing these measures, Biden’s administration can shift the narrative from borrower blame to institutional responsibility. Colleges would no longer operate without consequence for their role in the debt crisis, fostering a system where student success is the priority, not profit or prestige. Such accountability not only alleviates the burden on borrowers but also restores trust in higher education as a pathway to opportunity.

Do Student Loans Disappear in Probate? Understanding Debt Forgiveness

You may want to see also

Frequently asked questions

Biden has not committed to canceling all student debt for every borrower. His administration has focused on targeted relief, such as forgiving debt for specific groups (e.g., those defrauded by for-profit colleges) and implementing income-driven repayment plans.

As of October 2023, Biden’s administration has forgiven over $127 billion in student debt for nearly 3.6 million borrowers through targeted programs, including Public Service Loan Forgiveness and relief for borrowers defrauded by schools.

The student loan payment pause ended in October 2023, and payments resumed in October 2023. Biden has not announced plans to extend the pause further, but his administration has emphasized support for borrowers through affordable repayment options.

Biden’s campaign promise included forgiving $10,000 in student debt per borrower, with an additional $10,000 for Pell Grant recipients. However, this plan was blocked by the Supreme Court in 2023. His administration continues to explore other avenues for targeted relief.

![EidolonGreen [China Medicinal Herb] Bidens Tripartita(Bidens Tripartita L./Trifid Bur-marigold/Gui Zhen Cao/鬼针草/귀신침 초) Dried Bulk Herb 3 Oz (88 g)](https://m.media-amazon.com/images/I/61B8U7-NK2S._AC_UL320_.jpg)