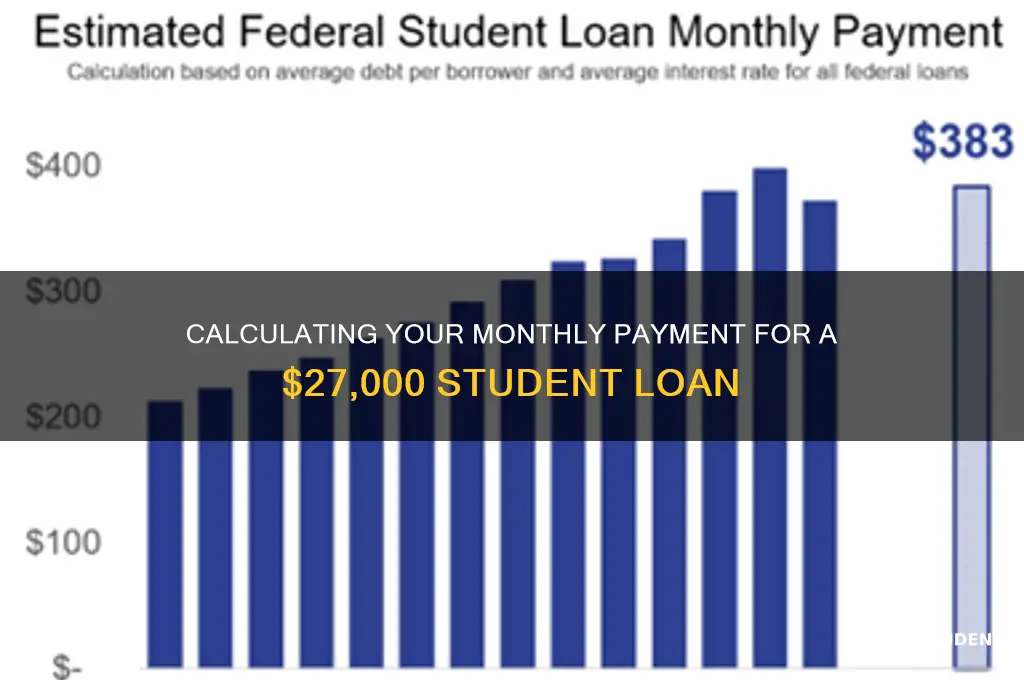

When considering a $27,000 student loan, understanding the monthly payment is crucial for financial planning. The exact amount will depend on factors such as the interest rate, loan term, and repayment plan chosen. For instance, a standard 10-year repayment plan with a 5% interest rate would typically result in monthly payments of around $285, while a longer 20-year term might lower the payment to approximately $165 but increase the total interest paid over time. Additionally, income-driven repayment plans could adjust the monthly amount based on earnings, offering flexibility for borrowers with varying financial situations. Calculating these figures accurately requires using a loan calculator or consulting with a financial advisor to ensure a manageable repayment strategy.

| Characteristics | Values |

|---|---|

| Loan Amount | $27,000 |

| Standard Repayment Term | 10 years (120 months) |

| Average Interest Rate (Federal) | 4.99% (for undergraduate loans as of July 2023) |

| Average Interest Rate (Private) | 5% - 12% (variable based on credit score and lender) |

| Monthly Payment (Federal) | ~$285 (using 4.99% interest rate and 10-year term) |

| Monthly Payment (Private) | ~$285 - $350+ (variable based on interest rate and repayment term) |

| Total Interest Paid (Federal) | ~$6,200 (over 10 years at 4.99%) |

| Total Interest Paid (Private) | ~$6,200 - $15,000+ (variable based on interest rate and repayment term) |

| Repayment Plans Available | Standard, Graduated, Extended, Income-Driven (for federal loans) |

| Deferment/Forbearance Options | Available for federal loans under specific conditions |

| Prepayment Penalties | None for federal or most private loans |

| Tax Deductibility | Up to $2,500 in student loan interest may be tax-deductible (U.S.) |

Explore related products

What You'll Learn

![]()

Interest Rates Impact

Interest rates are the silent architects of your student loan repayment journey, shaping not just the monthly amount but the total cost over time. A 27,000 student loan at a 3% interest rate could result in monthly payments of around $250 over 10 years, totaling approximately $30,000. Bump that rate to 6%, and your monthly payment jumps to roughly $280, with a total repayment of $33,600. That 3% difference adds $3,600 to your overall debt—a stark reminder that interest rates aren’t just numbers; they’re dollars out of your pocket.

Consider this scenario: two borrowers take out identical $27,000 loans but with different interest rates—one at 4.5% and the other at 7%. The first borrower pays about $270 monthly for 10 years, totaling $32,400. The second pays $295 monthly, totaling $35,400. The higher rate borrower pays nearly $3,000 more over the same period. This example underscores how even small rate variations can lead to significant financial differences, making it crucial to prioritize loans with lower rates or explore refinancing options.

To mitigate the impact of interest rates, adopt a proactive strategy. First, understand your loan’s terms—fixed rates remain constant, while variable rates fluctuate with market conditions. If you have a variable rate, monitor economic trends and consider locking in a lower fixed rate if possible. Second, pay more than the minimum monthly amount whenever feasible. Even an extra $50 monthly can shave months or years off your repayment timeline and save hundreds in interest. Third, explore federal programs like income-driven repayment plans or loan forgiveness, which can reduce monthly payments based on your earnings.

A lesser-known tactic is to make interest payments while still in school or during grace periods. For a $27,000 loan at 5%, paying just the monthly interest ($112.50) during a 6-month grace period prevents $675 from being capitalized and added to your principal. This small step keeps your total loan balance lower, reducing future monthly payments and overall interest costs. It’s a simple yet effective way to stay ahead of accruing debt.

Finally, compare private lenders if federal loans aren’t an option. Private student loan rates can range from 3% to 12% or more, depending on creditworthiness. A cosigner with strong credit can help secure a lower rate, potentially saving thousands. Use online calculators to simulate different rates and terms, ensuring you understand the long-term implications before signing. Remember, the interest rate you accept today will influence your financial flexibility for years to come.

Is the Government Forgiving Private Student Loans? What Borrowers Need to Know

You may want to see also

Explore related products

![]()

Loan Term Variations

The length of your loan term significantly impacts your monthly payments. A 27,000 student loan stretched over 10 years will result in lower monthly payments than the same loan condensed into a 5-year term. This is because you're spreading the same principal amount over a longer period, reducing the portion you need to repay each month.

Imagine a 27,000 loan at a fixed 5% interest rate. A 10-year term would yield a monthly payment of approximately $283, while a 5-year term would jump to roughly $515. This stark difference highlights the trade-off: lower monthly payments for a longer repayment period, or higher monthly payments for quicker debt elimination.

Choosing the right loan term requires careful consideration of your financial situation and goals. If you're just starting your career and anticipate income growth, a longer term might be manageable initially, allowing you to allocate more funds towards building savings or investing. However, if you have a stable income and prioritize becoming debt-free quickly, a shorter term, despite higher monthly payments, could save you thousands in interest over the life of the loan.

Remember, while longer terms offer lower monthly payments, they also mean paying more interest overall. A 27,000 loan at 5% over 10 years accrues approximately $4,980 in interest, whereas the same loan over 5 years accrues roughly $2,475.

Some lenders offer flexible repayment options, allowing you to adjust your loan term after a certain period. This can be beneficial if your financial circumstances change. For instance, you might start with a longer term for lower initial payments and then switch to a shorter term once your income increases. It's crucial to understand the terms and conditions of any loan before committing, including any fees associated with term adjustments.

Understanding the Student Loan Forgiveness Debate: Key Issues and Names

You may want to see also

Explore related products

$16.14 $16.99

![]()

Repayment Plan Options

Understanding your repayment plan options is crucial when managing a $27,000 student loan, as it directly impacts your monthly payments and long-term financial health. The federal government offers several plans tailored to different financial situations, each with unique benefits and considerations. For instance, the Standard Repayment Plan typically spans 10 years, offering a fixed monthly payment that ensures the loan is paid off within the shortest time frame, minimizing interest costs. However, this plan may result in higher monthly payments, which could strain tight budgets.

For borrowers seeking lower monthly payments, income-driven repayment (IDR) plans like Pay As You Earn (PAYE) or Revised Pay As You Earn (REPAYE) tie payments to a percentage of discretionary income, usually 10-15%. These plans can significantly reduce monthly obligations, especially for those with lower incomes. For example, a borrower earning $35,000 annually might pay as little as $150-$200 per month under an IDR plan, compared to $280-$300 under the Standard Plan. However, extending the repayment term increases total interest paid, and any remaining balance after 20-25 years may be forgiven but could be taxable.

Graduated and Extended Repayment Plans offer middle-ground options. Graduated plans start with lower payments that increase every two years, assuming income will grow over time. For a $27,000 loan, initial payments might be $150-$200, rising to $300-$350 by the end of the term. Extended plans stretch repayment up to 25 years, reducing monthly payments but significantly increasing total interest. For instance, monthly payments could drop to $180-$220, but total repayment could exceed $40,000 due to accrued interest.

Choosing the right plan requires balancing immediate financial relief with long-term costs. Borrowers should consider their career trajectory, income stability, and financial goals. For example, a recent graduate in a low-paying job might benefit from an IDR plan initially, switching to a Standard Plan once their income increases. Additionally, exploring loan forgiveness programs, such as Public Service Loan Forgiveness (PSLF), can provide further relief for eligible borrowers. Regularly reviewing and adjusting your repayment strategy ensures you stay on track without sacrificing financial flexibility.

Updating Income for Student Loan Forgiveness: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

Extra Payment Effects

Making extra payments on a $27,000 student loan can significantly alter your financial trajectory. Even small additional amounts can shorten the loan term and save thousands in interest. For instance, adding $50 monthly to a 10-year loan at 5% interest reduces the term by 18 months and saves $1,200 in interest. This strategy leverages the mechanics of amortization, where early payments disproportionately reduce interest rather than principal.

To maximize impact, target extra payments toward the principal balance. Most lenders apply payments to interest first, so specify "principal-only" when submitting additional funds. For example, if your monthly payment is $283, adding $100 directly to the principal each month could shave off 2 years and $2,500 in interest. Automate these payments to ensure consistency and avoid the temptation to skip them.

Compare the effects of lump-sum versus regular extra payments. A $1,000 lump-sum payment at the start of a 10-year loan saves $300 more in interest than spreading that $1,000 over 10 months. This is because the lump sum immediately reduces the principal, compounding savings over the loan’s life. If you receive bonuses, tax refunds, or windfalls, prioritize allocating them to your loan for this reason.

However, balance extra payments against other financial priorities. If you have high-interest debt (e.g., credit cards at 18%), pay that off first. Similarly, ensure you have a 3-6 month emergency fund before aggressively paying down student loans. Extra payments are most effective when your other financial foundations are secure.

Finally, track your progress to stay motivated. Use loan amortization calculators to visualize how each extra payment accelerates payoff and reduces interest. Celebrate milestones, like reaching the halfway point or saving a specific amount in interest. This psychological reinforcement can sustain your commitment to the strategy.

Student Loan Forgiveness Under IBR: When and How It Works

You may want to see also

Explore related products

![]()

Fees and Penalties

Understanding the fees and penalties associated with a $27,000 student loan is crucial for accurate monthly payment calculations. Beyond the principal amount, borrowers often face origination fees, late payment penalties, and prepayment charges, all of which can inflate the total cost of the loan. For instance, federal student loans typically charge an origination fee of 1.057% for Direct Subsidized and Unsubsidized Loans, meaning a $27,000 loan could incur an upfront fee of approximately $285, deducted from the disbursed amount.

Late payment penalties are another hidden cost that can disrupt budgeting efforts. Most lenders impose a fee of 5% of the missed payment or a flat rate, whichever is lower. For a $27,000 loan with monthly payments of $270, a single missed payment could result in a $13.50 penalty. Over time, repeated late payments not only add to the financial burden but also damage credit scores, potentially increasing future borrowing costs. Setting up automatic payments or reminders can mitigate this risk, ensuring timely payments and avoiding unnecessary fees.

Prepayment penalties, though less common, are worth noting, especially for borrowers planning to pay off their loans ahead of schedule. While federal student loans do not charge prepayment fees, some private lenders may impose penalties for early repayment to recoup lost interest. For a $27,000 loan, a prepayment penalty could range from 2% to 5% of the remaining balance, translating to hundreds of dollars in additional costs. Always review loan agreements carefully to identify such clauses and choose lenders that allow penalty-free early repayment.

Finally, understanding the impact of capitalization of unpaid interest is essential. When interest accrues and is not paid as it comes due (e.g., during deferment or forbearance), it may capitalize, increasing the loan’s principal balance. For a $27,000 loan with a 5% interest rate, $1,350 in unpaid interest could be added to the principal, raising monthly payments and extending the repayment term. To avoid this, borrowers should consider making interest payments during grace periods or periods of non-repayment, even if not required.

In summary, fees and penalties can significantly alter the monthly payment structure of a $27,000 student loan. By accounting for origination fees, avoiding late payment penalties, steering clear of prepayment charges, and preventing interest capitalization, borrowers can better manage their loan obligations and minimize overall costs. Proactive financial planning and a thorough understanding of loan terms are key to navigating these potential pitfalls.

Biden's Student Loan Forgiveness: Step-by-Step Application Guide for Borrowers

You may want to see also

Frequently asked questions

Your monthly payment depends on factors like interest rate, loan term, and repayment plan. For example, a 10-year term with a 5% interest rate would result in a monthly payment of approximately $287.

A higher interest rate increases your monthly payment, while a lower rate decreases it. For instance, a $27,000 loan with a 6% interest rate over 10 years would have a monthly payment of around $300, compared to $287 at 5%.

Yes, you can lower your monthly payment by choosing a longer repayment term, enrolling in an income-driven repayment plan (if eligible), or refinancing for a lower interest rate. However, extending the term or using an income-driven plan may increase the total interest paid over the life of the loan.