Elizabeth Warren, a prominent U.S. Senator and former presidential candidate, first proposed her comprehensive student loan forgiveness plan in April 2019 as part of her 2020 presidential campaign platform. Her plan aimed to address the growing student debt crisis by canceling up to $50,000 in student loan debt for millions of Americans, with the amount of forgiveness tied to the borrower's income. Warren's proposal gained significant attention and sparked national debate about the role of government in alleviating student debt, positioning her as a leading voice on the issue and influencing broader discussions on education policy and economic inequality.

| Characteristics | Values |

|---|---|

| Date Proposed | April 22, 2019 |

| Plan Name | Student Loan Debt Cancellation Plan |

| Proposed Forgiveness Amount | Up to $50,000 in student loan debt forgiveness |

| Eligibility Criteria | Household income under $100,000 annually |

| Partial Forgiveness | $1 of forgiveness for every $3 in income above $100,000 (up to $250,000) |

| Full Forgiveness | Households earning below $100,000 receive full $50,000 forgiveness |

| Impact on Taxes | Debt forgiveness would not be treated as taxable income |

| Funding Mechanism | Proposed Ultra-Millionaire Tax (2% tax on wealth above $50 million) |

| Additional Provisions | Includes investments in HBCUs and minority-serving institutions |

| Legislative Status | Not passed into law as of October 2023 |

| Public Reception | Mixed; supported by progressives, criticized for cost and scope |

| Related Policies | Influenced later proposals like Biden's targeted forgiveness plans |

Explore related products

![The Law of Debtors and Creditors: Text, Cases, and Problems [Connected eBook] (Aspen Casebook)](https://m.media-amazon.com/images/I/61g0lTTwLZL._AC_UY218_.jpg)

What You'll Learn

- Campaign Announcement: Warren unveiled her plan during her 2019 presidential campaign, gaining significant attention

- $50,000 Forgiveness Proposal: The plan proposed canceling up to $50,000 in student debt for borrowers

- Income-Based Eligibility: Forgiveness was tied to income, with higher benefits for lower-income individuals

- Funding Mechanism: Warren suggested a wealth tax on the richest Americans to fund the plan

- Legislative Push: Despite support, the plan has not yet been enacted into law

![]()

2019 Campaign Announcement: Warren unveiled her plan during her 2019 presidential campaign, gaining significant attention

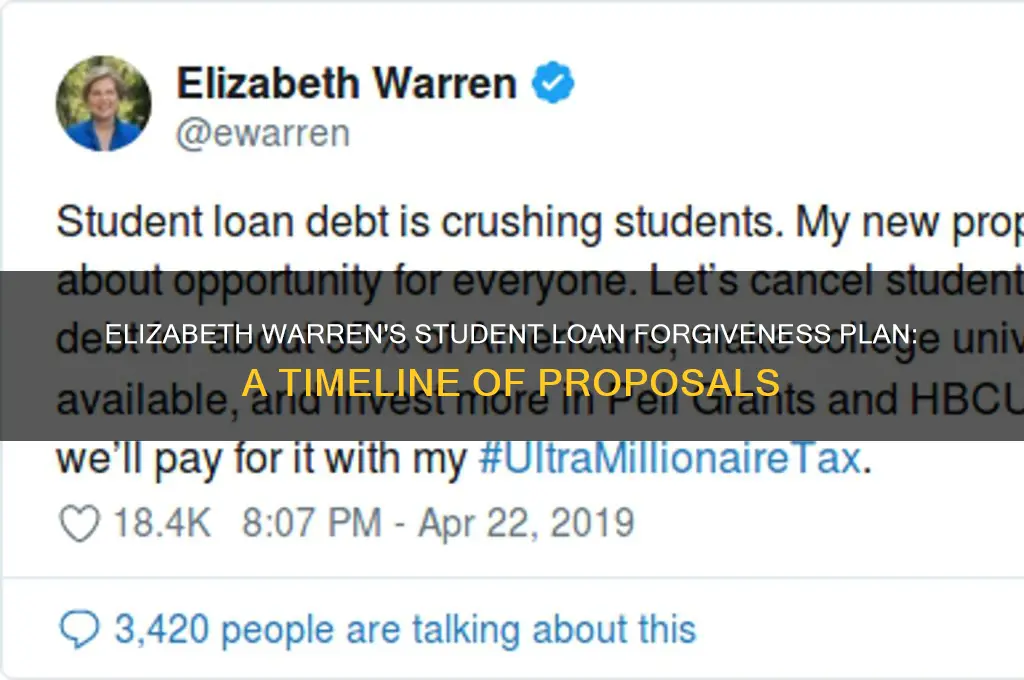

Elizabeth Warren’s 2019 presidential campaign marked a turning point in the national conversation about student debt, as she unveiled a bold plan to cancel billions in student loans. On April 22, 2019, Warren released her proposal, which called for forgiving up to $50,000 in student debt for 95% of borrowers, funded by a tax on the wealthiest Americans. This announcement immediately captured headlines and ignited debates across political and economic circles. By tying debt relief to broader themes of economic inequality, Warren positioned herself as a policy-driven candidate willing to tackle systemic issues head-on. Her plan’s specificity—detailing income thresholds, forgiveness amounts, and funding mechanisms—set it apart from vague promises made by other candidates. This strategic move not only bolstered her campaign but also forced competitors to address the issue, cementing student debt as a central policy topic in the 2020 election cycle.

Warren’s approach was both analytical and instructive, framing student debt as a moral and economic imperative. She argued that canceling debt would stimulate the economy by freeing millions from financial burdens, enabling them to buy homes, start businesses, and invest in their futures. Her plan included a tiered forgiveness structure: borrowers earning under $100,000 annually would receive $50,000 in relief, with partial forgiveness for those earning up to $250,000. This targeted design aimed to benefit lower- and middle-income earners disproportionately affected by debt. Critics questioned the plan’s cost—estimated at $1.25 trillion—but Warren countered with her proposed “Ultra-Millionaire Tax,” a 2% annual levy on fortunes over $50 million. This funding mechanism underscored her campaign’s broader theme of taxing wealth to address inequality, making the plan both ambitious and fiscally grounded.

The persuasive power of Warren’s announcement lay in its appeal to a broad coalition of voters. Young professionals drowning in debt, parents co-signing loans, and even older Americans with lingering debt found resonance in her message. By emphasizing the racial wealth gap—noting that Black and Latinx borrowers are disproportionately burdened—Warren also aligned her plan with social justice goals. Her campaign rallies and media appearances amplified this narrative, using personal stories of debt-strapped individuals to humanize the issue. This emotional and data-driven approach not only garnered media attention but also mobilized grassroots support, as evidenced by surges in campaign donations and volunteer sign-ups following the announcement.

Comparatively, Warren’s plan stood out for its comprehensiveness and immediacy. While other candidates proposed incremental fixes, such as lowering interest rates or expanding income-driven repayment plans, Warren’s call for immediate, large-scale forgiveness was unprecedented. This boldness drew both praise and criticism, with some arguing it was too radical and others hailing it as a necessary corrective to decades of policy failures. The plan’s ripple effects were evident in subsequent proposals from other candidates, who began incorporating debt relief into their platforms. Even after her campaign ended, Warren’s 2019 announcement remained a benchmark, influencing Biden’s eventual executive actions on student debt relief. Her willingness to challenge conventional wisdom demonstrated the power of policy-driven campaigns to reshape political discourse.

In practical terms, Warren’s 2019 announcement offered a roadmap for addressing a crisis affecting 45 million Americans. For borrowers, it provided hope and a clear vision of a future unburdened by debt. For policymakers, it highlighted the need for systemic solutions rather than piecemeal reforms. While the plan faced legislative hurdles and was not fully realized, its impact endures. Borrowers can still draw lessons from its principles: advocate for collective action, demand accountability from lenders, and support policies that address root causes of debt. Warren’s campaign proved that bold ideas, when paired with detailed execution plans, can galvanize public opinion and drive meaningful change. Her 2019 announcement remains a testament to the power of policy to inspire and mobilize, even in the face of formidable obstacles.

Nurse Loan Forgiveness: Unlock Debt-Free Freedom with These Strategies

You may want to see also

Explore related products

![]()

$50,000 Forgiveness Proposal: The plan proposed canceling up to $50,000 in student debt for borrowers

Elizabeth Warren’s $50,000 student loan forgiveness proposal emerged as a bold policy idea during her 2020 presidential campaign, specifically in April 2019. This plan was not just a number thrown into the political arena; it was a calculated response to the escalating student debt crisis, which had surpassed $1.5 trillion by that time. Warren’s proposal aimed to cancel up to $50,000 in federal student loan debt for 95% of borrowers, offering immediate relief to millions. The plan was designed to be progressive, with benefits phased out for higher-income earners, ensuring targeted support for those most burdened by debt.

To understand the impact, consider the mechanics: borrowers with household incomes under $100,000 would receive the full $50,000 in forgiveness, while those earning between $100,000 and $250,000 would see benefits gradually reduced. This structure addressed both the scale of the crisis and concerns about fairness. For instance, a teacher earning $45,000 annually with $30,000 in debt could see their entire balance wiped out, freeing up income for other financial priorities like saving for a home or retirement. Warren’s plan also included provisions to simplify income-driven repayment plans and make public colleges tuition-free, aiming to prevent future debt accumulation.

Critics of the proposal argued it was too costly, with estimates placing the price tag at around $640 billion. However, Warren countered by proposing a wealth tax on fortunes exceeding $50 million to fund the initiative. This approach framed the plan not just as debt relief but as a broader effort to address economic inequality. By targeting the wealthiest Americans, the proposal sought to redistribute resources in a way that directly benefited the middle and working classes, who disproportionately carry student debt.

Comparatively, Warren’s $50,000 forgiveness proposal stood out from other plans, such as those advocating for $10,000 in relief. While smaller amounts would help, they often failed to address the full scope of the crisis, leaving many borrowers still struggling. Warren’s plan was more comprehensive, aiming to eliminate debt entirely for the majority of borrowers. This distinction made it a rallying point for advocates of aggressive debt reform, even as it sparked debates about its feasibility and long-term implications.

For borrowers, the proposal offered a tangible path to financial freedom. Imagine a nurse with $45,000 in debt, earning $60,000 annually, who could redirect $400 monthly loan payments toward building an emergency fund or investing in professional development. Such scenarios highlight the transformative potential of the plan. While it did not become law, Warren’s $50,000 forgiveness proposal remains a landmark in the student debt debate, illustrating how bold policy ideas can reshape public discourse and push for systemic change.

Will Student Debt Forgiveness Be Automatic? What Borrowers Need to Know

You may want to see also

Explore related products

![]()

Income-Based Eligibility: Forgiveness was tied to income, with higher benefits for lower-income individuals

Elizabeth Warren proposed her student loan forgiveness plan in April 2019, and at its core was a progressive approach to debt relief: income-based eligibility. This framework wasn’t about blanket forgiveness but a targeted strategy to address financial disparities. Borrowers with lower incomes stood to gain the most, with up to $50,000 in debt cancellation, while those earning above $250,000 annually received no relief. This sliding scale aimed to alleviate the burden on those most vulnerable to economic hardship, ensuring that forgiveness wasn’t a one-size-fits-all solution but a tool for equity.

Consider the mechanics of this system. Under Warren’s plan, individuals earning less than $100,000 annually would receive full forgiveness of up to $50,000 in student loans. For every $1 in income above $100,000, the amount forgiven would decrease by $0.50, capping at $250,000, where eligibility ended. This structure incentivized economic mobility by providing immediate relief to lower-income borrowers while gradually phasing out benefits for higher earners. It wasn’t just about debt cancellation; it was about creating a pathway for financial stability for those who needed it most.

Critics argued that this approach could disincentivize higher earnings, but the plan’s design countered this by ensuring forgiveness tapered off gradually rather than abruptly. For instance, a borrower earning $150,000 would still receive $25,000 in forgiveness—a significant sum that acknowledges their contribution while prioritizing those further down the income ladder. This balance between relief and responsibility made the plan both ambitious and pragmatic, addressing systemic inequalities without penalizing success.

Practical implementation would require robust income verification systems to prevent abuse. Borrowers would need to submit annual income documentation, potentially through tax returns or payroll data, to determine their eligibility tier. This transparency would ensure the program’s integrity while maintaining its focus on fairness. For lower-income individuals, the immediate impact could be life-changing, freeing up resources for housing, healthcare, or entrepreneurship—a ripple effect that could stimulate broader economic growth.

In essence, Warren’s income-based eligibility model wasn’t just a policy proposal; it was a statement about the role of government in addressing economic inequality. By tying forgiveness to income, the plan acknowledged that not all debt is created equal—and neither should its solutions be. This approach offered a blueprint for future policies, proving that targeted relief can be both effective and equitable, reshaping the conversation around student debt in the process.

Will Private Student Loan Debt Ever Be Forgiven? What Borrowers Need to Know

You may want to see also

Explore related products

![]()

Funding Mechanism: Warren suggested a wealth tax on the richest Americans to fund the plan

Elizabeth Warren’s student loan forgiveness plan, unveiled in April 2019, hinged on a bold funding mechanism: a wealth tax on America’s richest individuals. Dubbed the "Ultra-Millionaire Tax," this proposal aimed to levy a 2% annual tax on households with assets exceeding $50 million, escalating to 3% for those above $1 billion. This approach wasn’t just about raising revenue; it was a deliberate shift in fiscal policy to address both economic inequality and the student debt crisis simultaneously. By targeting the top 0.1% of households, Warren’s plan sought to redistribute wealth in a way that directly benefited the 45 million Americans burdened by student loans.

The mechanics of this funding mechanism are straightforward yet transformative. Instead of relying on general tax increases or budget reallocations, the wealth tax would generate an estimated $2.75 trillion over 10 years, according to Warren’s campaign. This revenue would not only cover the $640 billion cost of canceling student debt but also fund other education initiatives, such as universal free public college. The plan’s design underscores a principle of fairness: those who have benefited most from the economic system should contribute proportionally to alleviate its systemic issues. Critics argue this could stifle investment or drive wealth offshore, but Warren countered with robust enforcement measures, including a 40% exit tax on wealthy individuals renouncing citizenship.

Implementing a wealth tax isn’t without challenges, but Warren’s proposal offers a blueprint for feasibility. For instance, the plan includes a 30% minimum tax rate on profits shifted overseas, closing loopholes often exploited by the ultra-wealthy. Additionally, the IRS would receive increased funding to ensure compliance, addressing concerns about evasion. This isn’t merely a theoretical exercise; countries like Norway and Switzerland have successfully implemented wealth taxes, though their economies differ from the U.S. Warren’s plan adapts these models to the American context, emphasizing transparency and accountability.

From a practical standpoint, the wealth tax serves as a dual-purpose tool: it funds student loan forgiveness while addressing the root causes of economic disparity. By canceling up to $50,000 in debt for 95% of borrowers, the plan would stimulate economic growth through increased consumer spending and homeownership rates. For example, a borrower earning $50,000 annually could save approximately $300–$400 monthly, freeing up funds for other expenses or investments. This ripple effect aligns with Warren’s broader vision of an economy that works for everyone, not just the wealthy elite.

In conclusion, Warren’s wealth tax proposal isn’t just a funding mechanism—it’s a statement about economic justice. By linking student loan forgiveness to a progressive tax on the ultra-wealthy, she challenges the status quo and offers a tangible solution to a pressing issue. While the plan faces political and logistical hurdles, its core idea—that those with the most should contribute to the common good—resonates with millions of Americans. Whether or not it becomes law, this proposal has already reshaped the conversation around wealth, debt, and equity in the United States.

Understanding Student Loan Forgiveness: A Comprehensive Guide for Borrowers

You may want to see also

Explore related products

![Diane Warren: Relentless [DVD]](https://m.media-amazon.com/images/I/71Mk4BYRwTL._AC_UY218_.jpg)

![]()

Legislative Push: Despite support, the plan has not yet been enacted into law

Elizabeth Warren first proposed her student loan forgiveness plan in April 2019, outlining a bold initiative to cancel up to $50,000 in student debt for 95% of borrowers. The plan, which also included tuition-free public college, garnered widespread public support and became a cornerstone of her presidential campaign. Despite its popularity, the proposal has yet to become law, highlighting the complex legislative hurdles that even well-supported policies face.

One of the primary challenges lies in the political polarization of Congress. While Democrats largely endorse Warren’s plan, Republicans have consistently opposed it, citing concerns about its cost and fairness to taxpayers who did not attend college. This partisan divide has stalled progress, as passing such a sweeping measure requires bipartisan cooperation or a unified Democratic front, which has been difficult to achieve. For advocates, this underscores the need to reframe the debate, emphasizing the economic benefits of debt cancellation, such as increased consumer spending and reduced financial stress for millions of Americans.

Another obstacle is the procedural barriers within the legislative process. Even with Democratic control of the White House and Congress, the Senate filibuster has prevented the plan from advancing without a 60-vote majority. Efforts to include student loan forgiveness in budget reconciliation—a process requiring only a simple majority—have been complicated by strict rules governing what can be included in such bills. This has forced proponents to explore alternative avenues, such as executive action, though legal challenges have limited its effectiveness.

Public pressure has played a critical role in keeping the issue alive. Grassroots movements, led by organizations like the Debt Collective and supported by millions of borrowers, have consistently pushed for action. However, translating this momentum into legislative success requires sustained advocacy and strategic coordination. Borrowers can amplify their voices by contacting representatives, sharing personal stories, and participating in campaigns that highlight the urgency of the issue.

Ultimately, the fate of Warren’s plan hinges on a combination of political will, procedural innovation, and public engagement. While its journey from proposal to potential law has been fraught with challenges, it serves as a testament to the resilience of those fighting for systemic change. For now, borrowers must stay informed, remain engaged, and continue pushing for a solution that addresses the crippling burden of student debt.

Can Community College Instructors Get Student Loan Forgiveness?

You may want to see also

Frequently asked questions

Elizabeth Warren first proposed her student loan forgiveness plan in April 2019 as part of her presidential campaign.

Her plan included canceling up to $50,000 in student loan debt for 95% of borrowers and eliminating tuition at public colleges and universities.

Warren proposed funding the plan through her Ultra-Millionaire Tax, a 2% annual tax on households with wealth over $50 million.

No, her plan primarily received support from progressive Democrats and faced opposition from Republicans and some moderate Democrats.